Send this article to a friend:

November

14

2013

|

Send this article to a friend: November |

|

The Federal Reserve's Centennial Birthday – The Hundred Years' War Against Gold and Economic Common Sense

On December 13, 2013, the Federal Reserve will celebrate its 100th birthday. Undoubtedly, there will be many articles forthcoming about the Fed between now and that infamous date, and I expect most, like this presentation, will be highly critical. Today I will be speaking about the effects central banking and the Federal Reserve have had on our lives, our society and, most important, on the way we think and act. I know many feel overwhelmed by the economic forces that have essentially taken full control of our markets since 2008, but I am here to remind you that the light shines much brighter today than it did when I first began seriously exploring this subject several decades ago. During what I believe are the final years of the U.S. dollar's rule as the world's de facto reserve currency, desperation is confirming what only a few years ago would have been dismissed as conspiracy theories of the lunatic fringe. Desperate acts, like the bailouts of 2008 and the attempts at crushing the gold market in 2013, have opened a window into the dark world of central banking and the most ubiquitous propaganda campaign in history against sound money practices. Today I want to look at the methods used by the Fed to wage such a war over the past one hundred years against gold and economic common sense—practices the Fed would very much like to keep from the public eye. Today we can come to understand the deception of fiat currency, and we can protect our wealth through precious metals ownership at a great discount to its true value. We can regain economic sovereignty by changing the way we think about money, and by acting on that knowledge. So let's begin by looking at a quotation from Ludwig von Mises' On Money and Inflation:

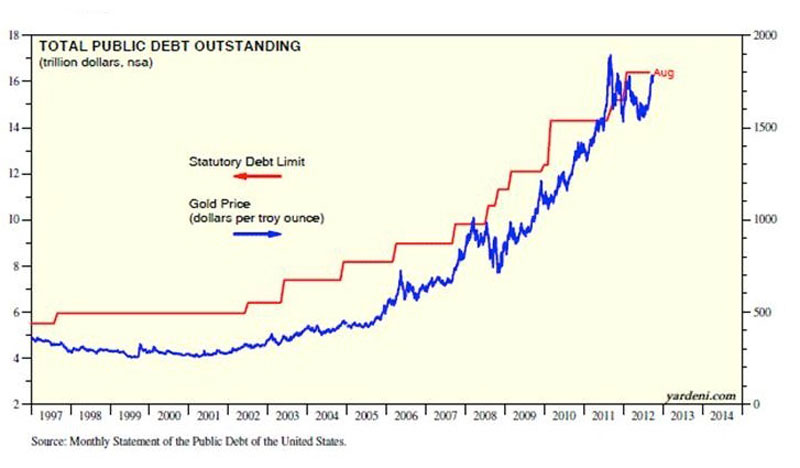

These words were spoken a half-century ago. Yet today, this is still the root of all of the world's major financial problems. Governments have tried to alter our reality to the point that we accept that central banks and, most notably, the Federal Reserve, have the right to create currency out of thin air while the rest of the population exchanges blood, sweat, thought and emotion for that same currency. This wouldn't seem fair to a Neanderthal, yet today most of us accept it as the norm. Many have joined the banking matrix, even though it has nothing to do with common sense. I chose the controversial title of $10,000 Gold only after watching the 2011 debt-ceiling fiasco, because it was clear then that there would never be a serious attempt at reducing debt until the entire system implodes. The October 2013 debt-ceiling debate, which accomplished nothing other than removing the debt-ceiling limit for the next three months, further confirmed that only financial disaster would bring a new system. Washington's decision makers lack the understanding and political will to avert such a disaster. I sincerely doubt that the Fed will ever voluntarily taper its quantitative easing program. My view is shared by many in the gold community, but by very few mainstream financial commentators. The main thesis of the book is that gold will continue rising because several exponential, long-term and irreversible trends will continue forcing the need for greater and greater government debt, and government debt is the main driver of the price of gold, as we can see in Figure 1. For the past decade, debt and the gold price have shared a conspicuously close relationship.

These trends—the rising and aging population, dwindling natural resources, outsourcing and movement away from the U.S. dollar—continue to develop. In order to make the case, a chapter was devoted to the mystery of currency creation that, of course, featured the Federal Reserve and its deceptive sleight-of-hand mechanics, fractional reserve banking, and the reasons banks and government have waged a century-long battle against gold. I was so mewhat shocked when the first draft returned from our publisher, Wiley, with none of the sections on the Federal Reserve redacted. It was further proof that the times are changing, and even a world-class publisher is no longer frightened about telling the truth. The Hundred Years' War Between Fiat and Gold We began work on BMG's first fund in 1998, at a time when gold was trading below $300 an ounce. We wanted to offer the public the opportunity to own uncompromised bullion in an RRSP-eligible fund that was open-end, therefore as liquid as gold; that was not dependent on the skills of a trading manager; and that was not in any way exposed to counterparty risk. We expected the product that took four years to complete would be welcomed with open arms, especially following the modern experience of 'tulip mania,' the dot.com bust. Instead we found investors' eyes glazed over when we spoke about gold. They repeated some familiar mantras: "Gold doesn't earn interest"; "Gold is a barbarous relic"; and my favourite, "You can't eat gold." When did they last eat a cash salad? It was then that we realized our job would involve a major education campaign to counter decades of fiat propaganda, perpetuated by a banking industry that has grown in power for 300 years. It soon became clear that gold was the sworn enemy of this new economic reality, where a chicken was a horse because the government said it was. Federal Reserve History As many of you know, the Federal Reserve was created in secrecy and passed into law on the eve of the Christmas holidays in 1913, at a time when most politicians had left for vacation, having been promised no legislation of importance would be passed in their absence. United States' history is scattered with heroic presidents who fought the concept of a central bank. Andrew Jackson succeeded. McKinley, Lincoln and Kennedy were assassinated. Jackson, of course, survived a failed assassination attempt when both the assassin's pistols misfired. This is serious business. The Fed was born in the golden age of industrialism, as vast fortunes had been made in steel and railroads at a time free of personal income tax. The industrialists and bankers who had benefited most from the capitalist system used their new wealth and influence to bring about legislation such as the Interstate Commerce Act of 1887 that essentially blocked smaller railroads from competing with the larger railroads owned by the industrialists. They wanted to apply the same advantage to banking. The Federal Reserve served as the bank of last resort, and would grant the Morgan, Rockefeller and Rothschild consortium (the impetus for the original Federal Reserve Act) unlimited liquidity, enabling them to vastly expand their empires. It also promised to backstop malinvestment and bad loans. The Federal Reserve would bring to fruition bankers' 200-year dream of privatizing profits and socializing losses. Such a mechanism is the ultimate form of moral hazard, reaching obscene levels by 2008 when the Fed not only bailed out its own shareholder banks like Goldman Sachs, but even refused to divulge the recipients of its bail-outs. Yes, the Federal Reserve has shareholders, unlike any other federal agency, because the Fed is no more federal than FedEx. Its shares were originally owned by the world's largest banks. Those, in turn, are owned to a great extent by the world's most influential banking families. Until recently the Fed has guarded its purpose, its methods and its ownership fiercely. Thanks to true light bearers like former Congressman Ron Paul, organizations like the Mises Institute, and the growth of the Internet, the world has begun to awaken to the deception. I think we can conclude that the Fed, like modern banking, to quote former Bank of England director Josiah Stamp, was "conceived in iniquity and born in sin." Why The Fed Hates Gold Since the Federal Reserve is the most powerful central bank in the world, and central banks are known to be the largest holders of gold bullion, why would we assume that the U.S. Federal Reserve hates gold? Doesn't the United States have the world's largest gold holdings? On paper, yes, but in truth this is far from a proven fact, as Western central bankers have been involved in the practice of leasing, and the even more opaque practice of swapping, their gold holdings for decades. Whatever gold is held in the vaults at the Federal Reserve Bank of New York and even in Fort Knox almost certainly, through hypothecation and re-hypothecation, has several claims to ownership. Dr. Paul not only began a grassroots movement to audit and eventually end the Fed, but also campaigned to audit the Fed's gold holdings, something that has not been done since 1953. This year the New York Fed told Germany's Bundesbank that it must wait seven years to repatriate just 300 tonnes of gold held in U.S. vaults. I believe this, and Holland's second-largest bank, ABN Amro's, default on its gold redemptions were two of the main events that necessitated the Fed-orchestrated gold takedown earlier this year. The Fed has either compromised Germany's gold through leasing or swapping, or simply doesn't have it. There is no other logical explanation.

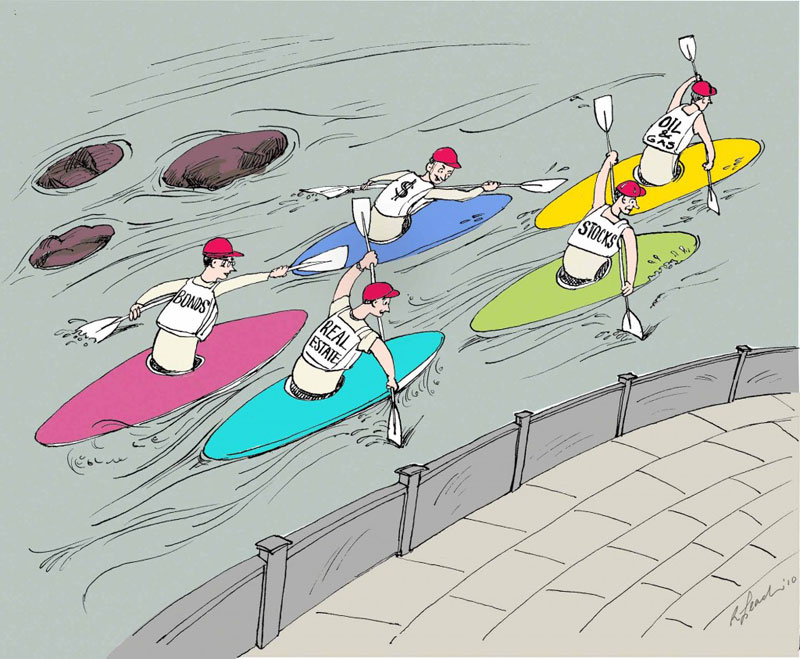

I'm certain everyone here understands why gold is an economic threat to the central banker's crown jewel, the right to create currency out of thin air. It is truth to the lie that paper currency is ultimately worth more than its intrinsic value, which Voltaire appraised as zero. It is also a threat to the entire matrix that government and banks would prefer we not question. This cartoon Figure 2 illustrates this point. In Figure 2 we see the race between asset classes. This is the narrow fiat perspective that many bankers and politicians call reality—a reality they'd like very much if we all accepted as well.

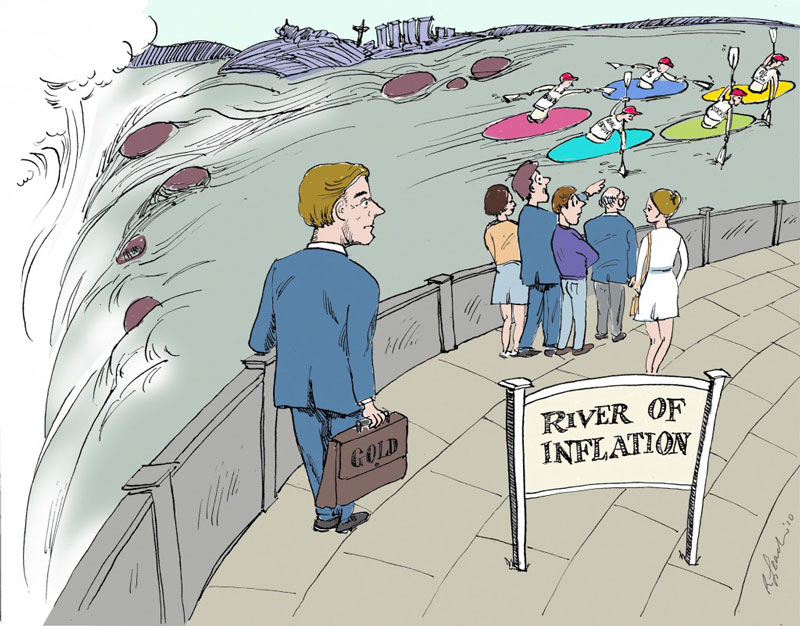

Yet if we broaden our perspective (Figure 3), we see that the canoeists are unaware that the current of the mighty river of inflation is pushing all asset classes except precious metals over the falls to their eventual doom. We call this broader vantage point 'the gold perspective,' because it enables us to see real inflation, the direct result of currency debasement that is now an accelerating global phenomenon. We encourage our clients and readers to break the spell of fiat thinking by thinking in ounces of gold rather than fiat paper such as dollars. There is no faster way to break the central bankers' spell than by owning gold and by evaluating all investments in gold ounces rather than in paper dollars. Gold ownership seems to have the magic ability to break this spell.

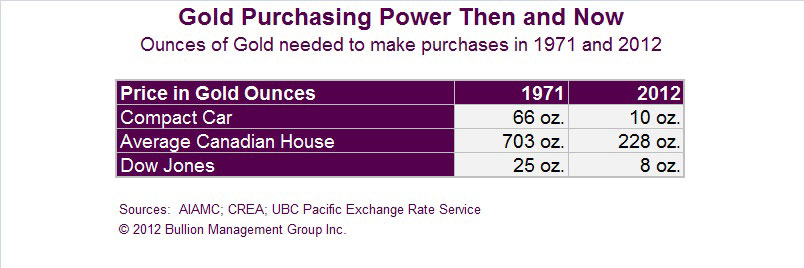

We use examples like this one from my book to show the effectiveness of this change of perspective. For example, a compact car would have cost 66 ounces of gold in 1971, the year President Nixon closed the gold window, and 10 ounces of gold in 2012. How's that for maintaining purchasing power? In fact, gold has maintained purchasing power—and therefore protected wealth—better than any asset class in history.

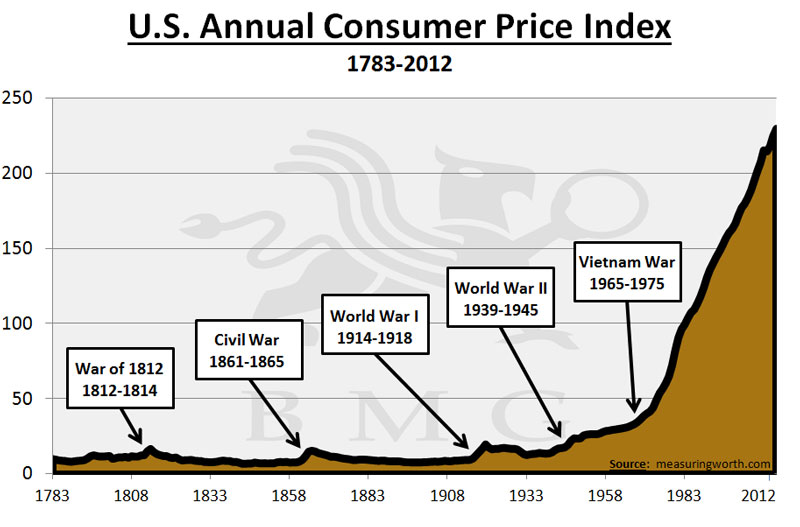

This becomes even more obvious when we look at the loss of purchasing power of the U.S. dollar since 1913. Since that time, the dollar has lost about 96 percent of its purchasing power when measured against gold. To make the point clearer, Figure 5 shows price levels dating back to end of the Revolutionary War. We can see that despite wars and even stock market crashes, the dollar held its value exceptionally well while the United States remained on some form of a gold standard. The exponential loss of purchasing power began to accelerate right around the time of the Fed's inception. A dollar in 1913 had roughly the same purchasing power it had in 1783. The Federal Reserve was sold to the American public as a means of preventing bank failures, and later as a means of preventing stock market crashes through interest rate manipulation. As modern banking was already 200 years old, and a formidable force in the early 1900s, it was not beyond the ability of these powerful institutions to cause enough small bank failures to convince the public that the Fed was indispensable. The public is easily swayed by the promise of big government protecting it. We see this today through the complacency with which most accept the expansion of Homeland Security and NSA spying. They are also more than happy to accept politicians' promises of social benefits and the endless war against terror, all made possible through easy, unsound fiat currency creation. Since its inception, the Fed's powers have increased to unimagined proportions. Who would have imagined one hundred years ago that the Fed would eventually reach a stage of power and corruption that would enable it to pass a $700-billion troubled asset relief program, or TARP, in 2008 to bail out its fellow bankers, and then have the arrogance to tell Congress it was "counter productive" to divulge where the money went.

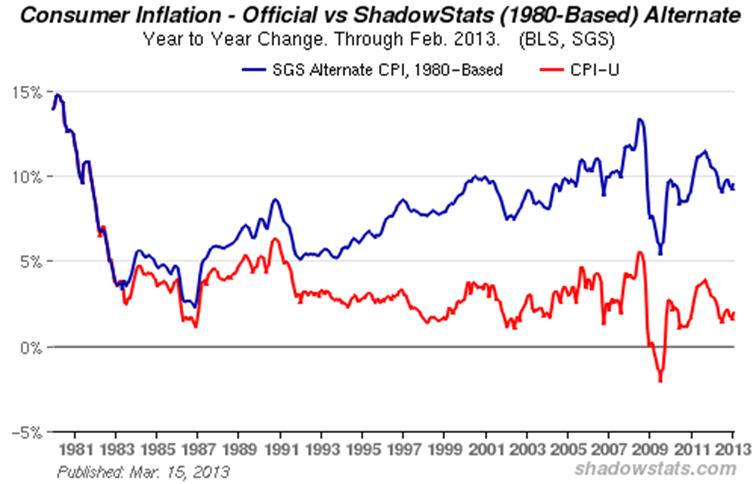

The Fed PR machine repeats endlessly that its major accomplishment is the prevention of institutional failures. That mantra grows pretty thin in light of the hard evidence. The Fed has met each crisis with a flood of liquidity. This simply ensures that the crash of the global economy will be more severe than ever. Rather than protecting the investing public, the Fed has given the world inflation, and because the U.S. dollar is the de facto world reserve currency, this inflation has been exported globally. It is now common knowledge that the U.S. CPI figures are manipulated to the point of being complete fabrications. We could say the same about almost all official government financial reports. Not only has the United States amassed obscene levels of debt since the days of President Clinton, but the U.S. Treasury, as a result of the 1995 Boskin Commission's recommendations, has changed the original basket of goods used to measure the cost of living since that time. The CPI used to measure a fixed standard of living with a fixed basket of goods. Today, it measures the cost of living with a constantly changing basket of goods, measured with metrics that are themselves constantly changing. Low-cost items are substituted for more expensive items (hamburger for steak), and hedonic regression is employed (determining that, for example, a newer-model television with extra features is more valuable than last year's model, even though it costs the same). John Williams's Shadow Stats tracks the original basket of goods, and estimates true inflation is running about six full percentage points higher than officially acknowledged Figure 6. We are currently seeing the early stages of one of economists' worst nightmares: stagflation, or stagnant growth and higher costs. What the cliff at the end of the road will look like is anyone's guess. Dr. Williams feels the United States will experience hyperinflation before the end of 2014. Of course, the United States and the developed world have enjoyed many years of unprecedented growth during the past century, due to the easy money policies of deficit spending. It also experienced a period of remarkable economic growth during the last two decades of the 19th century, when the country's dollar was firmly backed by gold and there was no personal income tax. The Fed's most powerful weapon is its ability to create an unlimited amount of unbacked currency, but its most powerful tool is the illusion of legitimacy it maintains through its incessant propaganda. Banks have simply learned what kings and rulers have known throughout history: Build massive edifices, like the Federal Reserve building in Washington created by the great spendthrift, Roosevelt, in 1937; portray yourself as gods whose utterances must be studied for clues by an entire industry like that of the Fed watchers and mainstream financial media; and continually build dependency through debt at the expense of the serfs and the middle class. History will judge the Fed harshly because, after the inevitable crash of the U.S. economy, much pain and suffering will be caused by the loss of reserve currency status. In fact, it is conceivable that our grandchildren will wonder how we could possibly have been so blind as to allow institutional theft on such a grand scale.

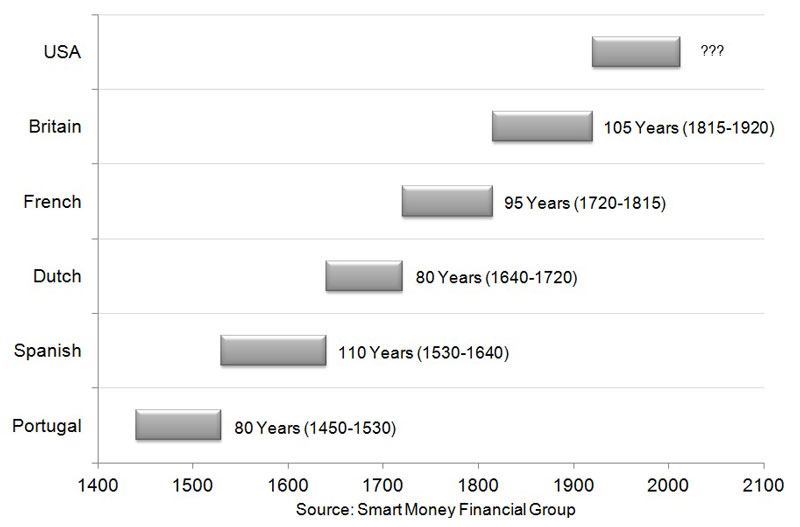

Some will argue that the U.S. dollar is so ubiquitous that the rest of the world's currencies are essentially its derivatives. This is true, but it doesn't guarantee the dollar's perpetuity. Figure 7 shows the lifespan of previous reserve currencies. All die a painful death, because governments abuse the privilege and create too much debt. Modern technology will simply accelerate the process. In the age of high-frequency trading, there is no way of knowing how fast the U.S. dollar might collapse. My guess is we are looking at a much shorter time frame than conventional wisdom expects.

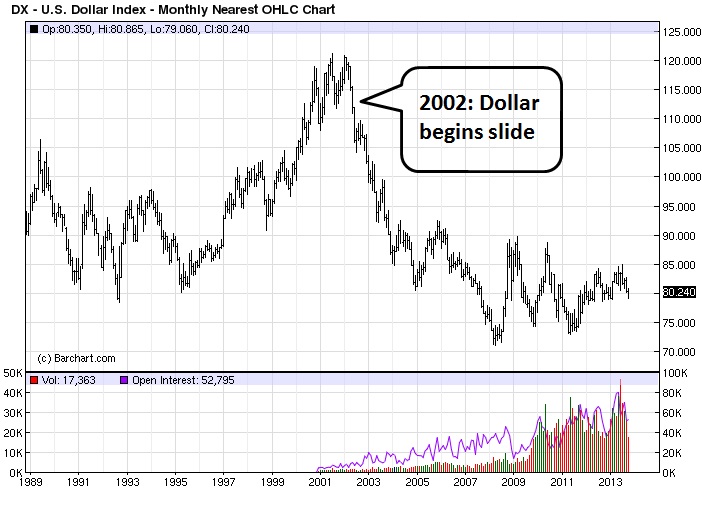

In fact, a look at the 10-year U.S. dollar chart Figure 8 shows that the patient is terminally ill. Recent events, such as the debt ceiling failure and NSA revelations about spying not only on its own population but also on the heads of state of the United States' most trusted allies, exacerbated the dollar's condition. Saudi Arabia recently revealed that ties with the United States had reached a new low. Saudi Arabia is perhaps more responsible for the dollar's success than any other country, because it agreed to denominate OPEC oil in dollars. This gave rise to the petrodollar in 1973, frequently called "Bretton Woods II." Countries around the world are showing aversion verging on disdain for further U.S. debt. This means the Fed has had to step up and buy the Treasuries that Japan, China and Saudi Arabia no longer wish to buy.

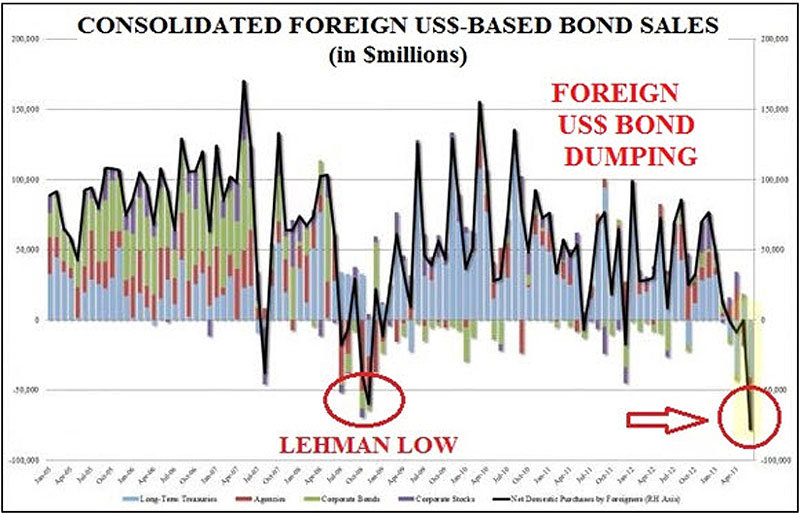

Figure 9 shows what foreigners currently think of U.S. bonds. If the U.S. dollar follows the path of all global currencies and fails, what will replace it? Well, again, we can look to gold for our answer. What country is amassing the most amount of gold? That is, without a doubt, China. The Chinese are taking advantage of the Fed's struggle to remain in control through intentionally suppressing the price of gold. Chinese officials have admitted they have a target goal of 10,000 tonnes of gold, and 2013's Fed-orchestrated takedown of gold has enabled them to make significant strides toward meeting this goal. Some Asian fund managers have suggested China may have already accumulated up to half of this amount. China is extremely secretive about its official gold holdings; it has been known to use the country's opaque sovereign wealth funds to amass gold holdings, which are then moved to official holdings, and announced at China's discretion. China has nothing to gain from divulging its official holdings, and everything to gain from lower gold prices. We can add the migration of gold from West to East to the long list of so-called Fed accomplishments, as history will surely do.

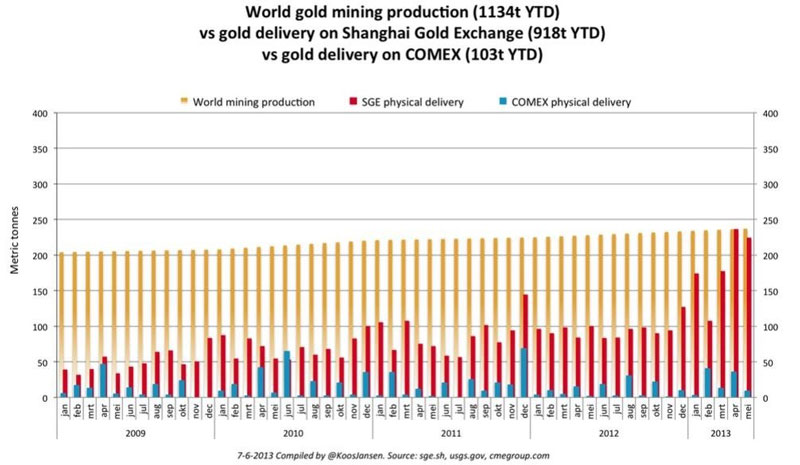

The gold price takedown was a paper takedown, likely orchestrated by the Federal Reserve and the Treasury, through its bullion banks and, possibly, through the off-budget Exchange Stabilization Fund. If it were a true correction, one based on weakening fundamentals, the physical market would not have been on fire, as we see by Eastern physical buying. The gold price takedown was a paper takedown in that most of the selling occurred on the COMEX, a paper market, with little physical gold changing hands. By comparison the Shanghai Gold Exchange, which represents a physical market, saw significant deliveries. The red lines Figure 10 show that physical deliveries matched global mine production in April and May. The blue lines show that, despite the unprecedented activity on the COMEX, it was almost all paper with very few physical deliveries taking place. I urge anyone who cannot clearly explain, in simple terms, the mechanics through which the Fed operates to read The Creature from Jekyll Island and Secrets of the Temple. Education, along with outright bullion ownership, is the best protection we can have against the coming financial crisis the Fed is bringing to the world. Eventually, public school children will understand this fraud.

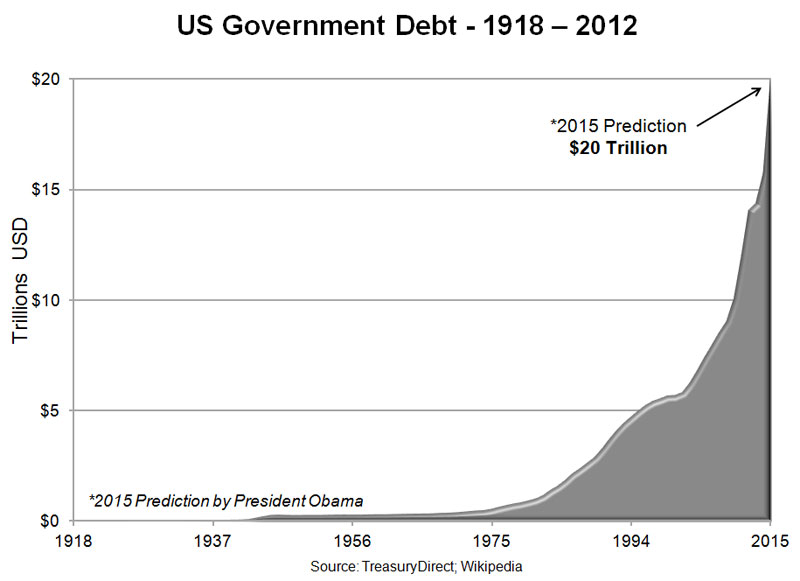

Of course, such claims will be met with accusations that I am just trying to sell bullion and that the world is far too complex to return to a gold standard. I heartily disagree. Although we are in the business of selling bullion for wealth protection, the facts support my words, and even the most fervent supporters of the status quo must admit that something is very seriously amiss with the fiat model. How can anyone in his or her right mind look at this chart of U.S. debt projections to 2015 Figure 11 and not be concerned? This doesn't include the unfunded liabilities that, by some estimates, would make this projection ten times greater.

Throughout history no fiat currency has ever survived, and no gold-backed currency has ever failed; why would this time be different? Figure 12 is an image of a display in BMG's boardroom showing the failed fiat currencies of the past two centuries. The Byzantine gold coin, by contrast, held purchasing power and kept its nation's economy healthy for 600 years. As far as a return to a gold standard goes, I believe it is too soon to make this prediction. This does not mean that every living person that uses paper currency cannot become his or her own central bank through bullion ownership. So far I have made several accusations. Now let's look at the proof.

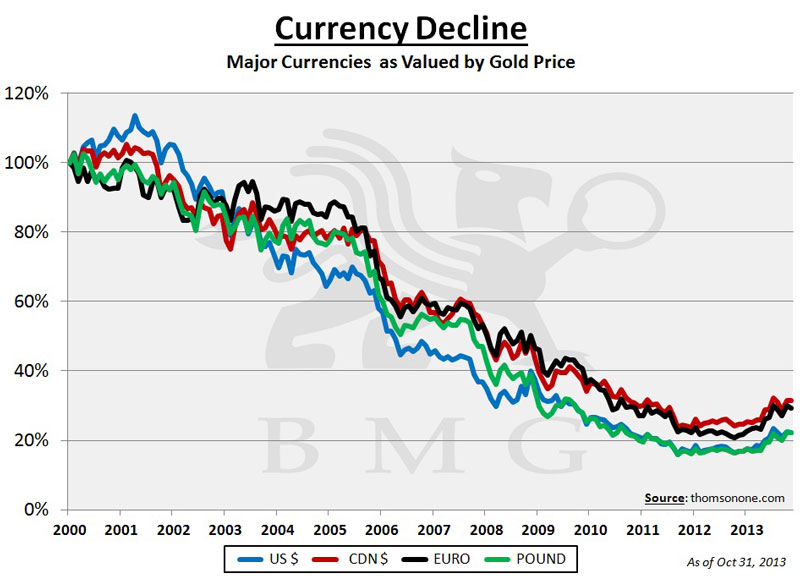

Let's start by looking at the core belief that we can simply print our way out of debt, or that debt itself will bring prosperity. QE, or unabated currency creation, is always presented as a means of saving the economy and of bringing prosperity to the many. Sadly, the facts show that this simply doesn't work. We can start with the loss of purchasing power already mentioned. Figure 13 shows the loss of purchasing power measured against gold—our one reliable standard of wealth preservation—over the past decade. Most of the world's major currencies have lost between 70 and 80 percent of their purchasing power during this time.

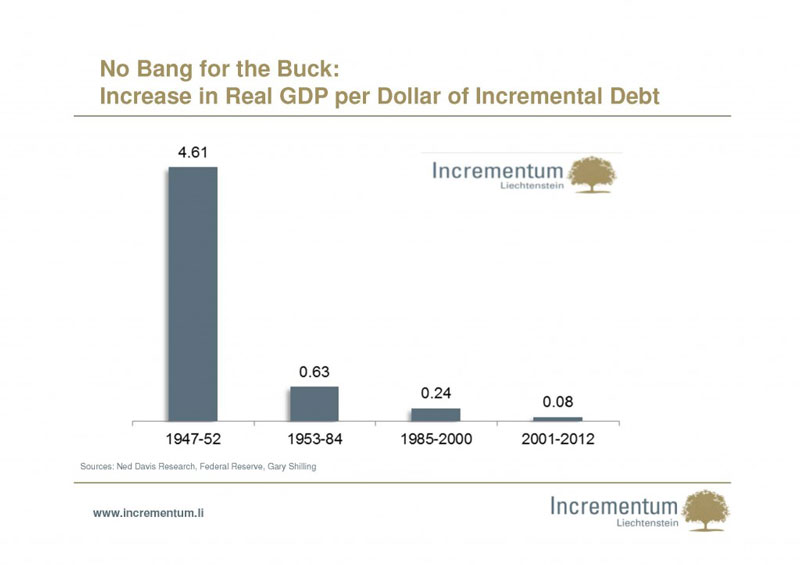

The Fed continually tells us that its quantitative easing bond- and CDO-purchasing program, to the tune of $85 billion a month, will re-ignite the economy and create growth. Creating growth through economic stimulus worked in the years following WWII, when vast amounts of reconstruction were required, the United States was the world's largest creditor nation, and there was still an international gold standard of sorts, as Bretton Woods established that each dollar was 40 percent backed by gold. This chart shows the futility of this approach today. In 1947, one dollar in debt raised the GDP by $4.61. Today, a dollar in debt raises real GDP by only $.08 Figure 14. Fed policies, although sometimes difficult to interpret, are further proof that QE has failed. Two policies that everyone should understand are financial repression and the government's position on bank bail-ins. Financial repression policies were used after WWII when debt to GDP was approaching 100 percent. The policies were continued into the 1980s. Now they are being implemented again, as debt to GDP is reaching record highs in the developed countries. Japan and the United States are both running deficits in excess of 100 percent of GDP. Financial repression policies are a hidden form of wealth confiscation through which governments rob their constituents, particularly retirees, savers, and anyone on a fixed income. In Liquidation of Government Debt, a 2011 NBER paper published by the International Monetary Fund, authors Reinhart and Sbancia discuss how governments use financial repression as a subtle way to reduce debt-to-GDP ratios. The three pillars of financial repression are:

Financial repression policies are fueling the undeclared currency wars, and they are making debtor nations like the United States highly unpopular, because they weaken a country's currency through debasement, and therefore reduce the value of its debt owed to foreign nations. The government must get money from the taxpayers to pay for public services. However, during times of economic stability brought about by adherence to a gold standard, they do this in the open. When the currency is pure fiat, they prefer to work under cover of night.

A second policy concerns depositor insurance. While bail-ins have struck Cyprus and Poland, they have not yet reached North America's shores. This does not mean Canada and the United States are immune. In fact, a careful reading of your banking agreement will show that North Americans have no better protection against such theft than the Cypriots had. Many suffer from the delusion that banks are protected against failure through FDIC and, in Canada, CDIC insurance. However, only deposits up to $100,000 are insured. We see here the exact quote from the Canada Deposit Insurance Corporation. We may think our money is safe in banks, but the banks see us not as depositors, but as unsecured creditors. Cypriot investors were subjected to a 47.5 percent loss of their savings over $100,000 because of the imbalance in the Cypriot banks' reserve ratios. When we look at the derivative exposure of U.S. banks, we can see that such bail-ins are very real possibilities for North American investors. Even if the FDIC wanted to cover more than $100,000, they don't have the money to do this. The following figures, taken from a presentation called "Take Your Money Out of the Bank," illustrate this point.

Financial repression policies and bail-ins would not be occurring in a healthy and sound value-based economy. I know many in the gold community feel there is a vast conspiracy amongst elites to control the world through bringing about a financial collapse and, eventually, a one-world currency and central bank. Others, like Dr. Paul, feel it is more a matter of incompetence. I tend to agree with this second view. Former Fed Chairman Alan Greenspan appears to have sold his soul. In 1966 he published Gold and Economic Freedom, an outstanding defense of the gold standard. When Dr. Paul asked Greenspan if he still agreed with what he wrote, Greenspan commented that he "wouldn't change a word." Yet Greenspan created bubbles and debt at an unprecedented rate during his tenure. In assessing current Fed Chairman Ben Bernanke's legacy, outspoken financial commentator Jim Willie determined that Bernanke would eventually disprove his own doctoral thesis. To quote Dr. Paul on the subject:

When economists and historians can objectively look back at this past century, they will likely find the U.S. Federal Reserve, as well as the world's other central banks, indirectly or directly responsible for:

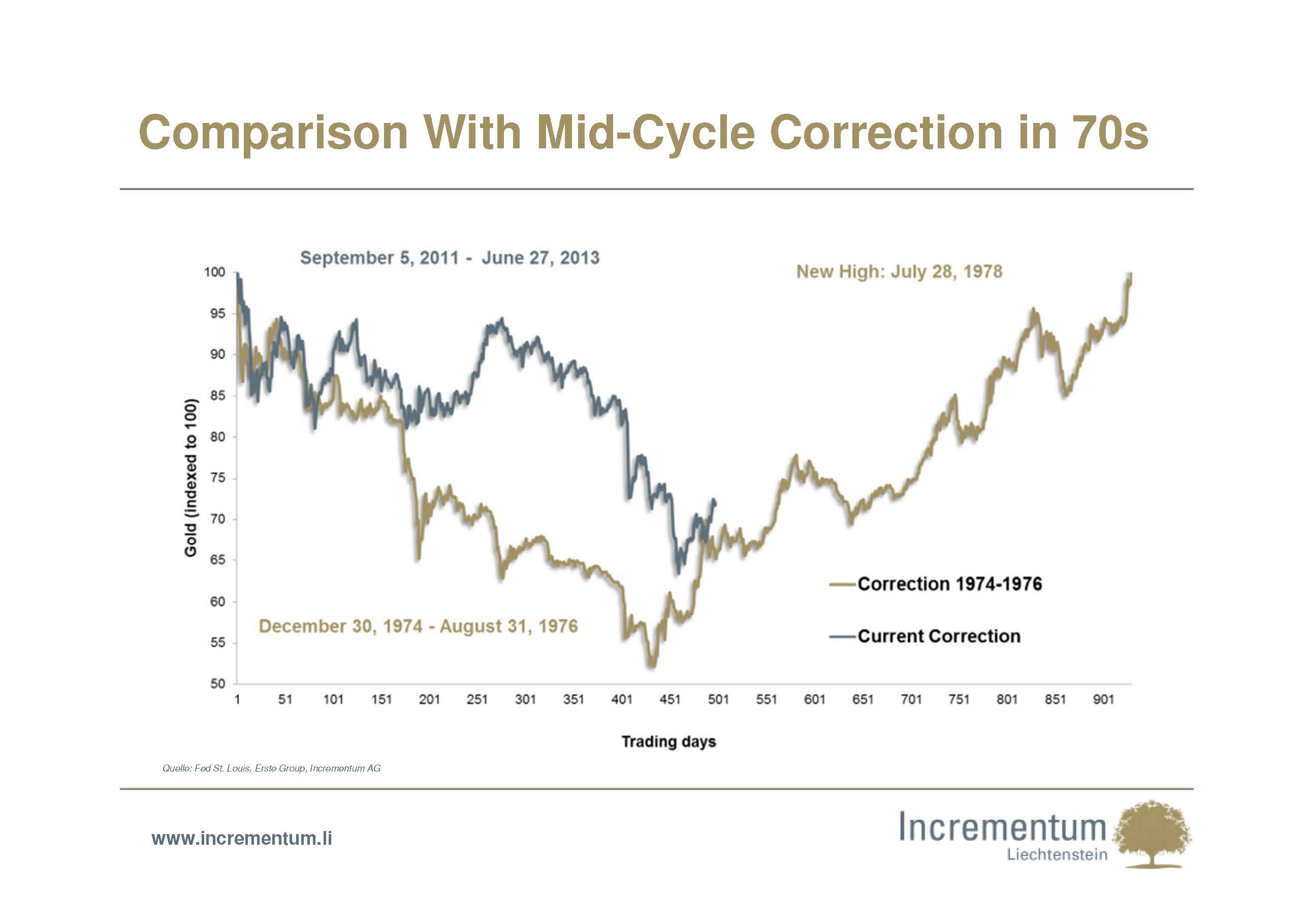

As for gold, I'd like to leave with the chart presented in Figure 15, as I will likely be defending my $10,000 prediction until the day gold reaches that price. This is a comparison to the mid-cycle correction gold experienced in 1976. As you can see, the two corrections both lasted about the same length of time. Gold climbed from $35 an ounce to $195 in 1974, then declined until the autumn of 1976. Gold fell 14 percent below its 55-month moving average, just as it did recently. At that time, the New York Times announced, with complete, unabashed confidence, "the end of the gold bull." Investors had given up on gold, many vowing never to return to it again. However, just as today, investors who understood the fundamental long-term trends that were causing gold to rise waited patiently. Once the weak hands were out of the market, gold changed direction and began climbing for three years, rising to $850 an ounce. A similar 800 percent rise in price from its current levels would take gold to $10,000 an ounce. Of course, if John Williams is right and the United States does see hyperinflation, we can add several zeros to this estimate. Self-education and moving cash out of banks into the only money that stands beyond the grasp of bankers and politicians is the best plan I can advise to prepare for the coming transition. The Mises Institute has provided an invaluable service in providing resources for those who wish to regain their financial and conscious sovereignty, and to step outside of the banking matrix. For this service I would like to offer my sincere congratulations. Corruption and moral hazard can only be fought with truth, and that highest human truth has always been represented by gold in the spiritual world, in the secular world, and in the financial world. Again, to quote Dr. Paul: Ultimately, it all comes down to accepting personal and moral responsibility, swimming against the current of popular thought, and knowing that a chicken is not a horse no matter how many officials in expensive suits tell us it is. Thank you.

Widely recognized as international bullion expert, Nick has written numerous articles on bullion and current market trends that have been published on various news and business websites. Nick has appeared on BNN, CBC, CNBC and Sun Media, and has been interviewed for countless articles by leading business publications across North America, Europe and Asia. His first book, $10,000 Gold: Why Gold's Inevitable Rise Is the Investor's Safe Haven, was published in the spring of 2013. Every investor who seeks the safety of sound money will benefit from Nick's insights into the portfolio-preserving power of gold. www.bmgbullion.com |

|---|

Send this article to a friend:

|

|

|

As anyone who has read my recent book, $10,000 Gold: Why Gold's Inevitable Rise Is the Investor's Safe Haven knows, I am a firm believer in sound money, free markets and the negative impact of central banks. I also stand firmly against global deficit spending and its major proponent, the U.S. Federal Reserve. I am a strong supporter of Austrian economics.

As anyone who has read my recent book, $10,000 Gold: Why Gold's Inevitable Rise Is the Investor's Safe Haven knows, I am a firm believer in sound money, free markets and the negative impact of central banks. I also stand firmly against global deficit spending and its major proponent, the U.S. Federal Reserve. I am a strong supporter of Austrian economics.

Nick Barisheff is the founder, president and CEO of Bullion Management Group Inc., a company dedicated to providing investors with a secure, cost-effective, transparent way to purchase and hold physical bullion. BMG is an Associate Member of the London Bullion Market Association (LBMA).

Nick Barisheff is the founder, president and CEO of Bullion Management Group Inc., a company dedicated to providing investors with a secure, cost-effective, transparent way to purchase and hold physical bullion. BMG is an Associate Member of the London Bullion Market Association (LBMA).