Send this article to a friend:

September

04

2017

|

Send this article to a friend: September |

|

Keynesian Imbecility Trap, Not Liquidity Trap

I shall now perform my legendary Ben Stein imitation for your amusement and edification. What is liquidity? Anyone? Anyone? That's the end of my imitation. But let's assume you are not the kid with his head on his desk, drooling. What is your answer? Why is this idea illogical? Can you figure it out? Let's go to Wikipedia. Here is the opening paragraph of the entry for "Liquidity trap." A liquidity trap is a situation, described in Keynesian Economics, in which injections of cash into the private banking system by a central bank fail to decrease interest rates and hence make monetary policy ineffective. A liquidity trap is caused when people hoard cash because they expect an adverse event such as deflation, insufficient aggregate demand, or war. Common characteristics of a liquidity trap are interest rates that are close to zero and fluctuations in the money supply that fail to translate into fluctuations in price levels Got that? The key phrase is this: "when people hoard cash." HOARDING CASH I realize that the kid with his head on the desk was not going to raise his hand, and tell Ben Stein this: "Nobody hoards cash these days. Everybody has a credit card except me, but I'm going to get one the day I turn 18." But if Ferris had been in class, I think he would have mentioned it. Ferris really understood cash. He didn't have any. If people don't carry much currency, which they don't, then where do they keep their money? They keep it in a bank. What does the bank do with the money? It lends it out. There is only one exception to this, and that is when it turns over depositors' digital money to the Federal Reserve to be held by the Federal Reserve as excess reserves. The Federal Reserve hoards this digital money. It does not spend it. The only significant source of a liquidity trap in the America today is the Federal Reserve. The cash that it hoards is not paper money. It is digital cash. But digital cash and paper currency are identical economically in terms of their economic consequences. Vault cash in a bank is exactly the same as excess reserves held by the Federal Reserve, legally and economically. Have we all got this straight? I'll tell you who doesn't have it straight: Paul Krugman, America's most famous Keynesian economist. But I'm getting ahead of the story. Where did this idea come from? It came from John Maynard Keynes. He never used the words "liquidity trap," but he supplied the concept. Here is how Keynes described the liquidity trap in 1936. This appears on page 207 of his General Theory of Employment, Interest, and Money. There is the possibility, for the reasons discussed above, that, after the rate of interest has fallen to a certain level, liquidity-preference may become virtually absolute in the sense that almost everyone prefers cash to holding a debt which yields so low a rate of interest. In this event the monetary authority would have lost effective control over the rate of interest. There was a problem with this analysis in 1936, at least inside the United States. By 1936, nobody was hoarding currency. There was no reason to hoard currency unless you were so poverty-stricken that you did not have a bank account. But people so poverty-stricken they did not have a bank account were not hoarding enough currency to make a difference for the U.S. economy. Why didn't Americans hoard currency in 1936? Because on January 1, 1934, the Federal Deposit Insurance Corporation opened its doors. Here is what the FDIC says of its own performance. An independent agency of the federal government, the FDIC was created in 1933 in response to the thousands of bank failures that occurred in the 1920s and early 1930s. Since the start of FDIC insurance on January 1, 1934, no depositor has lost a single cent of insured funds as a result of a failure.

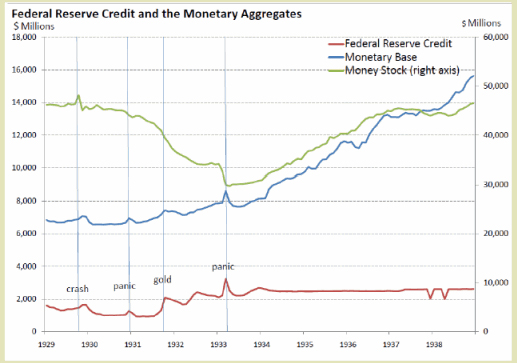

This statement is historically accurate. From late 1929 until March 6, 1933, approximately 9,000 American banks went bankrupt. This was out of a total of approximately 16,000 banks that were not members of the Federal Reserve System. Another 8,000 banks were members. The vast majority of the 9,000 banks that went under were small banks. Some were rural. Most of the others were in small towns. As soon as the FDIC was operational, there were no more bank runs. People knew that their money was protected by the federal government. There was no reason to hoard currency at that point. The bank runs ended. That was in 1934. Keynes, in 1934, was two years away from issuing his General Theory. He should have paid closer attention to what was happening to the banking system and the money supply in the United States. Here is what was happening. This began immediately after Roosevelt unilaterally closed the banks in the first week of his administration, meaning the second week of March 1933. He called this a bank holiday. When they reopened in the third week of March, they were effectively insured by the government. Then he got Congress to pass legislation confirming what he had done unilaterally and without any constitutional authorization at 1 AM Monday morning, March 6. Here is what happened to the money supply.

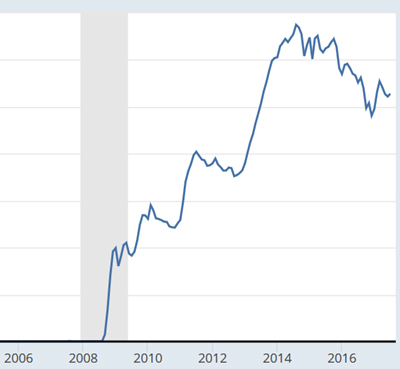

Monetary deflation ended as soon as Roosevelt re-opened the banks on March 13, 1933. I discussed this in 2012. Read what I wrote here: https://www.garynorth.com/public/9871.cfm. So, the problem that Keynes articulated in 1936 was a no longer a problem in the United States after March 13, 1933. That did not stop the depression. But the depression was no longer caused in any way, shape, or form by the hoarding of currency. Whatever was causing the depression, it had nothing to do with the hoarding of currency in the United States. It also had nothing to do with Federal Reserve policy, which was highly inflationary. There was a second recession in 1937. That also was not caused by the hoarding of currency. In other words, everything associated with the phrase "liquidity trap" is fake, both in terms of theory and in terms of practice. In terms of theory, there will not be monetary hoarding unless there is fractional reserve banking which has multiplied the money supply based on promises that the banking system cannot fulfill. In other words, there is monetary hoarding because there was prior deception by the banks, a deception which is, in effect, fraud. But the government allows the fraud because the government allows fractional reserve banking. Monetary hoarding does not come in response to the free market. It comes in response to a prior intervention into the free market by the government. But ever since March 13, 1933, there has been no widespread hoarding of currency in the United States. The threat has not existed for 80 years. Furthermore, in today's world, the overwhelming majority of bank deposits are made by huge investment funds that cannot pull the money out of the banking system in the form of currency. The funds have the option of deciding which banks they deposit their digital money in, but they have no ability to go down to the bank and withdraw $10 billion in small bills. So, there is no threat of bank runs to the banking system. The only people who could get to their money in the form of currency are common depositors, and the average deposit in savings accounts in the United States of the average Joe is under $1,000. Visit the average. It is driven higher by people who have more than $1000 in the accounts. If you're talking about the median size of the typical savings account, it is less than $1,000. This is chump change. It has zero effect on the economy as a whole. KRUGMAN'S DELUSION But this fact doesn't faze Nobel prize-winning economist Paul Krugman, America's most prominent Keynesian economist. Here is what he wrote in The New York Times in January 2012. There has been rather a lot of information coming our way since 2008, wouldn’t you say? If nothing else, we’ve learned that the liquidity trap is neither a figment of our imaginations nor something that only happens in Japan; it’s a very real threat, and if and when it ends we should nonetheless be guarding against its return — which means that there’s a very strong case both for a higher inflation target, and for aggressive policy when unemployment is high at low inflation. In December 2008, the Federal Reserve adopted the policy of paying interest on excess reserves: 0.25%. Excess reserves shot up in response to this guaranteed system of repayment.

The Federal Reserve did not begin raising interest rates until early in 2016. Also, the only rate that it can raise directly is the rate that it pays commercial banks on excess reserves held at the Federal Reserve. This means that the Federal Reserve economists must have known that raising this rate would persuade commercial banks to turn more money over to the Federal Reserve rather than lending it into the economy. This is a law of economics: if buyers raise the price, more will be supplied. The Federal Reserve does not lend out money that is held as excess reserves. It is the legal equivalent of vault currency/cash. This means that the Federal Reserve is doing exactly the opposite of what Krugman thought the Federal Reserve ought not do: tighten money. He had not yet figured out in 2012 that the Federal Reserve can only control the rate that it pays on excess reserves. Therefore, the higher the interest rate goes, the more that the economy falls into the liquidity trap, assuming there is one, which there isn't. Commercial banks do not lend this money into the economy, so nobody spends it. The Federal Reserve also hoards the money. This is exactly what Keynes warned against in 1936. CONCLUSION Keynesians run the country. They run the world. They run the central banks. They worry endlessly about a problem that does not exist. To avoid it, they adopt a central bank policy that would create this problem if it existed. This is why I call Keynesianism an imbecility trap. Keynesian economists cannot think straight. To quote the late Mitch Jayne, patter master of the Dillards half a century ago, two of them would not make a halfwit.

|

Send this article to a friend:

|

|

|

First, let us stroll down memory lane.

First, let us stroll down memory lane.

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/silver/t24_ag_en_usoz_2.gif)