Send this article to a friend:

May

20

2026

|

Send this article to a friend: May |

Gold, War, and the Slow Death of Dollar Confidence

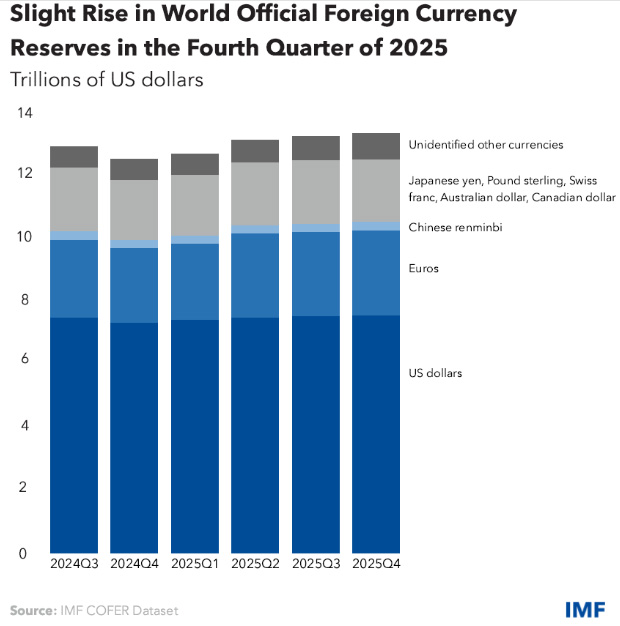

This is not because the dollar disappears overnight. It surely won’t. Reserve-currency regimes do not collapse in a single news cycle. They erode slowly, then suddenly. Trust is chipped away by sanctions, deficits, weaponized payment rails, political dysfunction, inflation, and the growing realization among sovereign nations that dollar dependence is not merely an economic arrangement — it is a geopolitical vulnerability. The recent conflict in the Middle East has pushed that realization to the surface. With energy security once again tied to the Strait of Hormuz, and with governments scrambling to secure oil flows through bilateral, opaque, and sometimes non-dollar arrangements, the old petrodollar architecture is visibly fraying. Recent reporting has highlighted how the Iran war and disruption around Hormuz are forcing Asian buyers to consider barter, alternative currencies, and government-led energy deals outside traditional dollar channels. That is exactly how monetary fragmentation begins. India is openly ignoring U.S. sanctions on Russian crude oil. Meanwhile, Iran is constructing a Hormuz payment architecture completely outside of the US dollar system. Some recent reporting has described proposed or alleged payments in yuan and cryptocurrency, with U.S. officials warning shippers that even indirect payments to Iran for safe passage could trigger sanctions. The dollar is still dominant, but that dominance is not permanent. IMF COFER data show the dollar’s share of global reserves slipped to 56.77% in Q4 2025, down from 56.93% in Q3, while the renminbi’s share ticked higher. The trend is not a straight line, but the direction is clear: central banks are diversifying away from excessive dollar concentration.

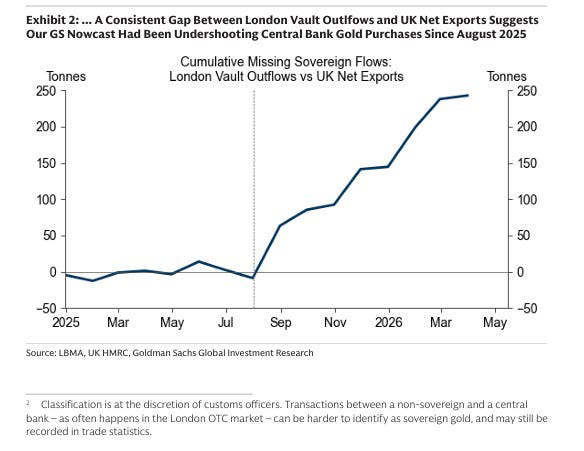

Gold is the cleanest expression of that diversification. It has no counterparty risk. It cannot be sanctioned. It cannot be printed. And in a world where the monetary system is becoming more multipolar, gold is increasingly being revalued not as a relic, but as neutral reserve collateral. Gold constitutes roughly 20% of global official/central bank reserves, depending on the dataset and valuation date. But there is growing evidence that sovereign gold transactions have been consistently underreported, with countries like China and Saudi Arabia quietly accumulating 400 ounce gold bars via London:

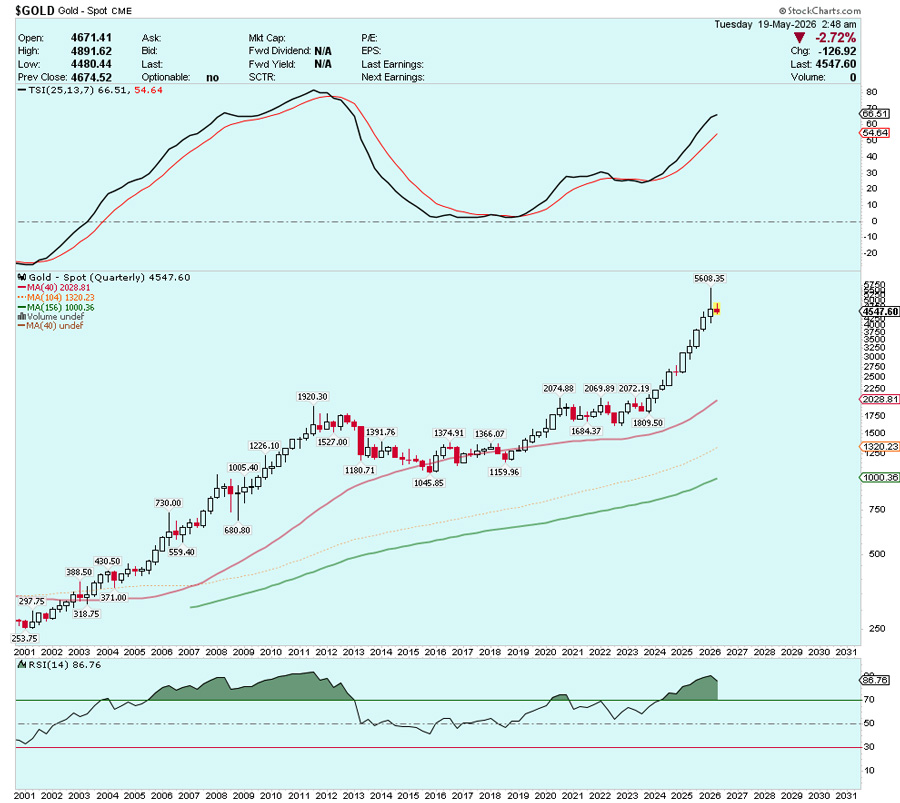

The discrepancy between London vault outflows and UK net exports represent unrecorded sovereign gold flows. Global central banks continue to accumulate gold, but they are reluctant to be fully transparent in terms of the total magnitude of their gold purchases. That is why the recent correction in gold should be viewed for what it is: a correction inside a secular bull market, not the end of the move. Gold recently pulled back from its January 2026 all-time high, with Comex gold still trading around the mid-$4,500s despite short-term pressure from higher bond yields and inflation concerns. Even after the decline, gold remains dramatically above year-ago levels — a sign of a market consolidating a major advance, not collapsing. Gold (Quarterly)

All bull markets climb a wall of worry. This one is no different. The worries are familiar: higher real rates, temporary dollar strength, Fed rhetoric, crowded positioning, ceasefire headlines, and seasonal weakness. But none of these have changed the structural drivers of the gold bull market. The U.S. fiscal position remains deeply challenged. The dollar reserve system is losing credibility at the margin. Geopolitical risk is no longer episodic — it is structural. Central banks continue to seek diversification. And investors are slowly relearning that gold is not merely an inflation hedge; it is a confidence hedge. The U.S./Iran conflict in the Middle East has triggered forced selling in gold, as many countries have been compelled to raise liquidity to offset the strain of higher energy prices. Once a more sustainable peace agreement is reached, I expect gold to rally — not only because lower energy prices would relieve pressure on global balance sheets, but because this conflict has once again underscored a much larger point: nations cannot afford to be overly dependent on the U.S. dollar system or fragile global supply chains. In a world defined by geopolitical shocks, sanctions risk, and energy insecurity, gold remains the ultimate neutral reserve asset. This correction is healthy. It shakes out late buyers. It resets sentiment. It allows moving averages to catch up. It creates the doubt required to fuel the next leg higher. The bigger picture remains intact: gold is in a long-term secular bull market driven by monetary debasement, sovereign diversification, geopolitical fragmentation, and declining confidence in the dollar-based system. The uptrend should resume this summer, and by the end of 2026, gold is likely to be trading at new all-time highs. The market’s message is clear: the world is not abandoning the dollar tomorrow, but it is steadily preparing for a world in which the dollar is no longer the only answer. Gold is the beneficiary of that preparation.

23 year market veteran: futures, metals, junior mining, and biotech. I am an investor, trader, and market commentator. I focus on precious metals, junior mining and biotech.

|

Send this article to a friend: