April

08

2013

08

2013

|

April 08 2013 |

The Theology of Inflation

This is in part because most of us still think of economics as a science akin to physics or mathematics. Inflation is one way economists attempt to measure things. But unlike the distances between stars or atoms, or the certainty implicit in even very abstract mathematical models, our measurement of inflation is limited by and entirely dependent upon the tools we choose. In fact, the methodology we use has as much ability to determine the outcome as the actual data does. This week we begin a series on economic data with a look at inflation, but we'll preface the series with a discussion of how economics may be more akin to philosophy or theology than the hard sciences. If you are an academic economist, you may want to move on to the next letter, unless you are capable of not taking yourself too seriously. First, a little housekeeping. You are getting this letter this week on Friday night or Saturday morning, depending on what part of the globe you inhabit. When Thoughts from the Frontline first started (in August of 2000), I wrote on Friday during the day and hit the send button in the afternoon. The list was smallish and delivery was quick. Over the years, it has taken me longer to research and write. My business life is now focused around thinking about and writing this letter, which suits me just fine. But now "writing day" often stretches late into the night and beyond, into the following morning. Friday nights became Saturday mornings and I ended up sleeping too late on Saturday to really enjoy the day. I should note that since I quit drinking about 19 months, 26 days, and 4 hours ago (but who's counting?) it is taking me about twice as long to write the letter. Seriously. I suspect that, like many writers far more productive and interesting than I am, I was self-medicating my ADD with a little wine and scotch on writing nights. Not a lot, mind you; just enough. Whatever enough is, which is another data point that can be, well, fluid. So I decided to try writing Sunday night, and then moved to Tuesday night due to the publishing schedule of other Mauldin Economics publications. However, readers told me they prefer to read me on the weekend. It finally dawned on me (skilled analyst that I am) that there is little difference between Tuesday and Thursday nights. So the new schedule will be that I will write on Thursday night, reflect and edit on Friday, and make sure the letter gets to you overnight for your weekend reading pleasure. Thanks for your patience as I wandered through the week in order to get back to sending the letter on the weekend when you always wanted it anyway. The Theology of Inflation Long-time readers may know that for sins committed in my past lives I matriculated to Southwestern Baptist Theological Seminary in Fort Worth after graduating from Rice in 1972 (just as slide rules were starting to slip from the pantheon of must-wear gear for the respectable nerd). I decided not to pursue the religious endeavor beyond that point, which was a positive choice both for me and for the poor unsuspecting church that would have employed me. But little did I know that my theological studies were actually preparing me for a career in finance and investments, at least as well as my study of economics at Rice had done. Fast-forward to a few years ago. I was sitting in a pub somewhere in London (I can get very lost in that town), meeting with the new chairman of Anglo-Irish Bank (who was a bank turn-around specialist with very interesting stories), and we were joined by Anatole Kaletsky. Anatole and I had been developing a long-distance relationship of mutual curiosity about all things economic, and he graciously took the time to meet with me late that night. (He needs no introduction to European readers as he is a fixture on the Continent with his economics writing and analysis; but for US readers, he has written since 1976 for The Economist and The Financial Times and was editor-at-large of The Times of London before recently joining Reuters and The International Herald Tribune. He has been named Newspaper Commentator of the Year by the BBC and has twice received the British Press Award for Specialist Writer of the Year. His Rolodex is ridiculous. And he is a founding partner in GaveKal, one of my favorite research firms.) The point is that Anatole is an influence center, and that night in London I wanted to discuss the role of economic writers and analysts in society with someone who had established himself at a level that few attain. While I take the writing of this letter and the importance of economic forecasting seriously, I don't take myself all that seriously. And so that night, encouraged by the better part of a bottle of a good chardonnay, I tossed out what I thought might be a provocative thought:

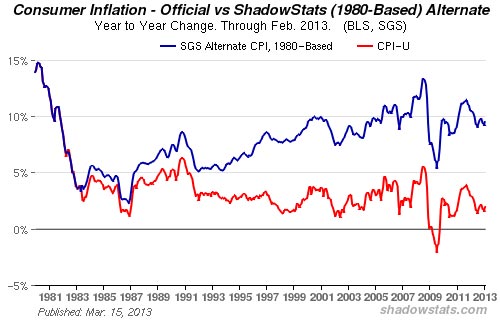

Warming to my topic, I threw in this climactic line: "I think economics is more like religion and less like science than most of us want to admit." I clearly struck a chord in Anatole, and he readily admitted to having voiced the same thought at times. We talked late into the night on the topic. I was reminded of that conversation this week as I read a recent editorial by him on the role of economists. I am going to excerpt a page or so from that piece, as I think it will help frame our discussion of the usefulness of government statistics. Trying to Fix Broken Economics Here is a list of economic questions that have something in common. In a recession, should governments reduce budget deficits or increase them? Do 0 percent interest rates stimulate economic recovery or suppress it? Should welfare benefits be maintained or cut in response to high unemployment? Should depositors in failed banks be protected or suffer big losses? Does income inequality damage or encourage economic growth? Will market forces create environmental disasters or avert them? Is government support necessary for technological progress or stifling to innovation? What these important questions have in common is that professional economists can't answer them. To be more precise, economists can offer plenty of answers about government deficits, printing money, inequality, environmental issues and so on; but none of these answers is authoritative enough any longer to persuade other economists, and never the world at large. Take two examples. On whether government borrowing aggravates recessions or promotes recoveries, the world's most eminent economists fall into one of two violently conflicting schools. The world's most important central banks, the U.S. Federal Reserve and the European Central Bank, hold diametrically opposing views about the effects of quantitative easing. If economics were a genuinely scientific discipline, such disputes over fundamental issues would have been settled decades ago. They are equivalent to astronomers still arguing about whether the sun revolves around the earth or earth around the sun. How should politicians and voters who look to economists for guidance respond to this cacophony? Economics is ultimately a study of politics, psychology and social behavior. It is therefore as close to philosophy or even theology, as to physics, biology or engineering. Just as philosophers and theologians still argue about the same issues that preoccupied Plato, Kant and Descartes, economists see no shame in continuing the debates over budget deficits, monetary policy and full employment launched by Keynes, Wicksell or Walras. This political and moral aspect of economics suggests a reason for the subject's remarkable prestige and power, despite its obvious failings. Economists have become a secular priesthood, turning the political orthodoxies of their times into comprehensible narratives, thereby promoting social stability and democratic consensus. In the 40 years since the mid-1970s, the dominant schools of academic economics have preached the virtues of free markets, competition and small government, helping to legitimize widening disparities of wealth and income as economic necessities, dictated by natural laws of market competition that were impervious to political interference or social control. In the 40 years before that - from the Great Depression and Keynesian revolution to the Great Inflation and monetarist counterrevolution - economists played the opposite political role. Their job was to persuade conservative business interests that active government, fine-tuning of economic cycles, welfare safety nets and redistributive tax systems were indispensable to the success and even survival of capitalist free-market societies. If we look back to the 19th century, to the origins of the modern capitalist system, we can see economists playing other politically legitimizing roles – establishing respect for private property, competition, free trade and voluntary contracts for mutual beneficial exchange, in a world that was still largely feudal, with wealth distribution justified by heredity, violence or military conquest. As Keynes famously said, "The ideas of economists, both when they are right and when they are wrong, are more powerful than is commonly understood. Indeed the world is ruled by little else. Practical men, who believe themselves to be quite exempt from any intellectual influence, are usually the slaves of some defunct economist." What makes Keynes's comment so relevant today is that the economic system is again in a process of transformation. It is now fairly clear, as suggested in my book Capitalism 4.0, that a new model of global capitalism is evolving out of the 2008 crisis, just as it did out of the crises of the 1970s, the 1930s and out of the collapse of feudalism in the early 19th century. We are still waiting for the parallel transformation in economic thinking, but some of its features can be discerned. The first is a recognition that the world is too complex and uncertain to be analyzed with models that assume a natural equilibrium of a future that is predictable, at least in a probabilistic sense. The second is that even competitive and perfect markets can make disastrous mistakes. The third is that a world economy that is highly unpredictable must be managed with fairy broad and flexible tolerance ranges for indicators such as inflation, government borrowing or unemployment, instead of the precise inflation targets of the pre-crisis period. Building on what Anatole states, when it comes to inflation, we need more than just flexible tolerances. What we really need is a healthy dose of recognition that our measurements of inflation may not be able to even get us close to precise targets. A couple weeks ago I published in Outside the Boxa piece by my friend Gary Halbert in which he discussed the slippery slope of government efforts to measure inflation. He talked about the difficulty of measuring inflation and about the manipulation (his term) of inflation statistics over the last 30 years. John Williams of Shadowstats is the most-noted proponent of the position that inflation is running well above the current government number of 2% (for the 12 months ending February 2013). Employing the methodology that was used in 1980 under the Carter administration, inflation is currently about 9.6% (see chart below). Using the government methodology from 1990, inflation today is a little under 6%.

(The following will be regarded as a contentious statement by the gold bugs and hyper-inflationists out there. For some of you, to accept it would be like admitting your religious beliefs are wrong.) I am often asked what I think about those alternate inflation numbers. The answer is that I think it is clear that the methodologies used in 1980 and 1990 are visibly, patently, demonstrably wrong. If inflation were now at 9.6%, then interest rates should be closer to 12% and not the 1.75% we see on the ten-year treasury today (more on that topic in a minute). Over time, markets respond to actual inflation and not government statistics. Argentina's government can state that inflation is "only" 10%, but the market thinks it is 30% and rising. The government calculation of inflation in 1980 or 1990 was the best they could do at the time. Gentle reader, it was a government calculation. There is nothing ex cathedra about either methodology. In religious terms, neither rises to the stature of the original Greek documents or the Latin Vulgate Bible. Changing the words (the equations) in economics should not be seen as somehow equivalent to the changing of the fundamental documents of a religion. There is nothing sacred about 1980 CPI methodology, and in fact we can look at it empirically and understand that it was pretty flawed. You might have some personal investment bias (read quasi-theological reason) to want inflation to be high. But that is a belief system. It is one form of faith-based economics (and I maintain that most economic schools require of their adherents a measure of faith and belief). Expectations of high inflation are for some people a basic tenet of their belief system. Saying there is only a little inflation must therefore be a government manipulation. Let me really get some of you upset, which is one of my roles as an analyst. I think we must constantly be comparing our assumptions against what we observe in the real world, and then see where our models, with their built-in assumptions, bias our conclusions about what the data says. If you think overall general inflation is high, then you have to think the entire world is delusional. (Note: As I will keep saying, your personal inflation rate may be much higher than 2%. I know mine is. But I have seven kids and tuition bills to pay!) G-7 interest rates are at an all-time low today. That can and will change; but right now the bond market does not see inflation as a problem anywhere in the developed world, although yesterday Japan made what I think is their 10th vow in the last 20 years to create inflation. This time, I think they may actually (but for them, catastrophically!) succeed. For now, however, deflation and deleveraging are the order of the day. If we had kept the methodology of 1980 for calculating the Consumer Price Index and then used that number to adjust Social Security and government pensions, the US government would be bankrupt today. Social Security would have gone negative in the 1990s and tripled in cost in the last 12 years (compounding at 10% can do that). Now, those of you living on Social Security might think a tripling of payments is appropriate, given what has happened to your budgets, but younger taxpayers would hasten to differ. (Note: I am not arguing that SS provides a livable income at current levels. Different topic for another letter.) That is not to say that today's inflation methodology is correct or gives us a number that is accurate. It is simply better than it was in 1980 – but it is still just a statistical method that tries to reach for the impossible star and finally has to settle for accuracy in general at the risk of imprecision in the particulars. We will be able to look back in 15 years to see how well we are doing today at measuring inflation. The surprise would be that we don't change methodologies at least a few times between now and 2030. Remember the Jimmy Carter years and those wonderful Dan Aykroyd spoofs of Carter saying "Inflation is your friend?" And if you want to go back to a more innocent era, watch the YouTube of a propaganda newsreel from the 1930s touting the benefits of inflation. Roosevelt is portrayed as the savior bringing inflation to us all. (Pay attention to the religious tones of the piece and the headlines!) Physicists and chemists deal with observable, measurable events occurring in controllable conditions. Economics has physics envy. Economists want to be scientists playing with observable data and precise mathematical models. However, economic experiments are frequently not observable, often not measurable, and almost never controllable. They are typically conducted inside of computers, using models based on assumptions that make the models possible – and often assuming away the real world. Yet we keep conducting our little experiments. It's enough to drive even a normally cheerful person like me to despair. Seeing inflation as religious doctrine might be amusing if inflation were our friend. It may well be our friend, or it may not; we just don't know. The theology-economics parallel is probably more accurate than either side wants to admit. Both fields deal in nebulous concepts. Both believe their work is of profound long-term significance. Neither can prove the accuracy of their claims in the short term. Much like Christians, over time economists have sorted themselves into denominations. Central bankers, finance ministers, and certain economists function as high priests. Each At the risk of pushing the religious analogy a bit too far, I submit that inflation is best defined within an agnostic or polytheistic belief system. You have your inflation, I have my inflation, and both are equally correct. We're all going to the same place, right? More in this in a moment, after we at least try to define some terms. CPI: Right for Everyone, Wrong for You Depending on your point of view, inflation is either monetary or price-based. The oldest definitions viewed it as simply an increase in the money supply. If the amount of money grows and the supply of goods stays the same, the result is higher prices. Today the more common view is that rising (or falling) prices are a different issue, driven by supply and demand rather than simply by the money supply. Without taking sides in that debate, I think it's clear we all prefer to pay less for whatever we buy. Here is where we get polytheistic. Everyone has their own personal money supply and their own personal spending patterns. If the price of liverwurst rises in Germany, I really don't care: I don't like liverwurst and I don't live in Germany. But if you are German, liverwurst inflation can be an issue. The examples can just as easily hit closer to home. If you live in South Florida, the price of snow blowers is not on your mind. Your personal inflation rate gives more weight to air conditioning. If you are a retiree in your 70s, rising college tuition costs have little direct impact on you. Rising prices for prescription drugs are much more important. It is hard to argue with people who point out that prices and the cost of living are going up faster than government-reported inflation. We can all see prices rising. Food, energy, tuition (try doing that for 30 years with seven kids!) – they're all going up. If we used actual home prices in the CPI, inflation would have been seen as very high in the middle of the last decade. Instead, we seemed to be flirting with deflation; and if we used housing prices in 2008-2011, we would certainly have had government-reported deflation. In place of home prices, the Bureau of Labor Statistics decided to use something called Owners' Equivalent Rent a few decades ago; and it is the largest part, a full 24%, of the CPI. (You can see the math and methodology here: http://www.bls.gov/cpi/cpifacnewrent.pdf.) Something called hedonics is probably the most contentious part of the CPI calculation. The BLS says, "The hedonic quality adjustment method removes any price differential attributed to a change in quality by adding or subtracting the estimated value of that change from the price of the old item." Basically that means that, for example, as your computer gets more powerful every year, the BLS says you are getting more for your dollar; therefore the price fell even if you paid as much or more for the computer. Opponents say hedonics can be used to hide "true" inflation. I do know that a lot of items have in fact gone down in price and up in quality. Cell phones are a good example. And the cost of using cells may be ready to really fall. I am testing a full smart phone that uses a major carrier and wifi in combination and that will go on the market for $20 a month for all the voice, data, and text you can eat. It worked on wifi in the middle of the Andes last month. I paid basically nothing for 10-15 hours of talk time, and people called me using a local Dallas number. Most egregiously for me, the CPI also does not take into consideration income taxes. I can tell you that is my largest source of inflation! Yet all of us here in the US are governed by the same people in Washington, and they define inflation in their own way, via the Consumer Price Index and various related benchmarks. Because CPI tries to find a national "average" inflation rate, it is almost by definition inaccurate for any given person, family, business, city, or state. CPI is the least common denominator, a "one size fits all" coat that in reality fits no one very well. (For the record, all the data used to calculate inflation is public. You can calculate inflation for your own local area if you have nothing better to do. In fact, the entire methodology is public, if a little dense.) Given the acknowledged limitations of the CPI, we nevertheless use it in myriad ways. It governs cost-of-living adjustments for Social Security beneficiaries, government employees, and many labor union members. CPI is baked into the general cake, even though we know it is imperfect in almost every situation. As a result, some people get raises when their cost of living drops, while for others the cost of living rises faster than their income. Is this fair? No. Is there a better way? I don't know what it would be. There are hundreds of smart people who build entire careers trying to answer that question. Other inflation measures exist, but they all have their own limitations. Three Federal Reserve Bank regions calculate their own versions of CPI. The Federal Reserve prefers to look at something called PCE, or Personal Consumption Expenditures, which uses chained dollars rather than a fixed basket like the CPI does. Since 2000, the Federal Reserve has used PCE in its reports to Congress about expectations for inflation. In explaining its preference for the PCE, the Fed stated: The chain-type price PCE index draws extensively on data from the consumer price index but, while not entirely free of measurement problems, has several advantages relative to the CPI. The PCE chain-type index is constructed from a formula that reflects the changing composition of spending and thereby avoids some of the upward bias associated with the fixed-weight nature of the CPI. In addition, the weights are based on a more comprehensive measure of expenditures. Finally, historical data used in the PCE price index can be revised to account for newly available information and for improvements in measurement techniques, including those that affect source data from the CPI; the result is a more consistent series over time. ("Monetary Policy Report to the Congress," Federal Reserve Board of Governors, Feb. 17, 2000) Contentious? You bet! PCE and other chained inflation numbers generally yield lower inflation figures. Which is why many in Congress (and the AARP) think "chained dollars" is some conspiracy to defraud seniors on Social Security. CPI is used to calculate adjustments for income taxes. If it is too low, then incomes rise faster in real terms than cost adjustments do, and that acts as a tax increase even as your pension is adjusted lower. But if inflation is calculated too high, then taxes are lower than they would otherwise be and the costs of Social Security and pensions are higher. Talk about using a hammer to fine-tune a highly developed economy. Even small miscalculations will add up over time to large losses for someone. Whatever inflation is, and whatever it does in the short term, we are fairly confident it has a significant long-term correlation with interest rates. This makes perfect sense when we recall that interest rates are simply another price: the price of borrowing money. Many prices are distorted by government policies, but none more so than interest rates. The Federal Reserve Banks directly control short-term rates and have great influence everywhere else. The results of their labors are not always clear, nor do we know exactly who benefits from them. Conspiracy theories abound. In theory, the Fed's job is to use its tools to maintain a balance between maximum employment, stable prices, and reasonable interest rates. The "stable prices" goal refers to inflation. We know from his public statements that Ben Bernanke is satisfied that inflation is under control for now. His benchmark, though, is the same Consumer Price Index whose weaknesses we discussed above. Bernanke and his colleagues are well aware of the imperfections in their data and analysis, even as they defend them. They will admit as much, if pressed. Like the rest of us, they depend on government employment and inflation statistics because they don't have anything better. So what we have is an opaque central bank using blunt instruments to manipulate a statistic relevant to practically no one to ends they cannot define with any specificity. But CPI is the tool we have, and so we use it. For all its problems, the CPI and its cousins are getting better over time and can be useful if you see them as indicators of trends and not as something absolute. And one month does not make a trend, so getting (as my dad would say) your bowels in an uproar over the latest CPI figure is pointless. Looking at year-over-year trends for at least a year or two might actually be useful. We will take up this topic again in the very near future. There is a lot more to say about inflation and deflation. I simply have to note that the Japanese have announced they will do what I have been saying they would do for the last few years, which is that they will print more money and do it faster than the Fed or the ECB. This is going to be a huge economic experiment. I think it will end in tears for Japan, which is why my largest personal investment is basically to short the Japanese government and the Bank of Japan (not their stock market!). Printing money and running massive deficits is not a solution at 240% debtto-GDP. This is what Louis Gave wrote yesterday: Enter the new Bank of Japan. Under new leadership and a new mandate, the BoJ did something yesterday it has not done in any living investor's memory: massively exceeded market expectations. The BoJ is doubling its bond purchase program, with greatly extended duration. Meanwhile, the yen is at 97 and falling. Thus, any Japanese household (and Japanese households are the most liquid-asset rich in the world) has to be thinking of putting some of the US$9trn currently sitting in cash into other currencies. And every hedge fund has to be wondering why they should not sell 10 year JGBs yielding 40bps in a falling currency, and then buy US, UK or French bonds yielding 1.75 to 2%. And for investors who agree with Charles' view that the yen's decline will deliver a global deflationary shock, especially for Japan's biggest export competitors, then even German bunds yielding 1.25% might look attractive for the long side of the trade again st the JGB short. Louis and his father Charles will be at my 10th annual Strategic Investment Conference, where they will be joined by their partner Anatole Kaletsky. I will have them on a panel where we will talk Japan, Asia, and Europe. (Some conference planners think it is great fun to get me and Anatole on the same stage and toss some red meat between us. While we may both think there is a relationship between theology and economics, we seem to be members of different congregations. But afterwards, we agree that we had fun as well.) Kyle Bass will be joining us and of course talking about Japan. Deflation and inflation will also be on the menu, with Lacy Hunt and Gary Shilling). Mohamed El-Erian will be giving us the view from on high, Niall Ferguson will bring us up to date on his latest research and passion, Nouriel Roubini will brief us on his latest conversations with various world leaders (he has been on a roll of late in his writing), David Rosenberg and Jeff Gundlach (some of the brightest hedge fund managers anywhere) will opine on the markets, and Paul McCulley, fresh from his world travels, will take us back and bring us forward. All this and more in two and a half power-packed days! This year I am going to make sure that there is more interaction among speakers while we listen, as well as give you the opportunity to meet and talk with them in a compact setting. And Bloomberg will be shooting live and doing interviews the entire time. There are a very few spots left for attendees. If you want to come (and you should!) then click here to reserve your spot and enjoy a short video of some highlights from last year. On another note, I did an interview last week for King World News, and you can listen to it here. I find myself in Sonoma tonight, where I have to get up all too soon to speak; but as a reward I get to meet and listen to John Hussman for the first time. I am quite curious to see him, as I have read and corresponded with him for years. He just so rarely speaks anywhere. I am truly an admiring fan of his work. And of course I get to meet Michael Pettis, just in from Shanghai, as well as old friend Mike Shedlock. It will be a great day. Then on Monday I head to NYC and dinner with fishing buddies Barry Ritholtz, Jim Bianco, and Scott Frew, as well as Sarah Eisner of Bloomberg. Meetings all day Tuesday and a few on Wednesday, and then it's back for my last Mavericks game of the year. I will leave on Friday for a quick trip to Las Vegas, where my great friend and personal physician Mike Roizen has invited me to come to a weekend 80th birthday party for Michael Caine and Quincy Jones, as part of a charity event involving the Cleveland Clinic. All sorts of parties and goings on. I rarely if ever run in those circles and am a monster fan of Michael Caine, who has given me such pleasure on the screen over the years. How can he be 80? It just seems like too much fun to say no, and since I am in a hotel anyway when I'm in Dallas now, why not be in one in Vegas and hang out with my friends? What's another plane ride on Amer ican Airlines among friends? I will come back and jump on a plane to Singapore via Tokyo (again on AA), where I will be with Grant Williams and Simon Hunt. Now THAT will be an interesting evening. I should figure out how to record that one. And then it's back through San Francisco for a few days for another speech. And I can't sign off without mentioning that I participated in a really interesting event called "Downturn Millionaires" with Rick Rule, Bill Bonner, and Doug Casey (among others) while I was in Argentina. If you follow or are curious about gold and natural resource stocks, this is something you'll want to check out. Gold stocks are in a serious bear market and totally out of favor to a degree I have not seen since the beginning of the last bull-market run. And given central bank actions (like Japan's), maybe it is time to think hard about that question. We found ourselves in strong agreement that what we're looking at here is a once-in-a-decade opportunity. The free video webinar of the event will air on April 8 at 2 pm Eastern, and you can reserve a seat right here. For those who have schedule conflicts, it will be available for viewing after the initial stream. Have a great week. What an interesting time we live in. I am really looking forward to learning how my friends see what is happening, both at my conference and everywhere else I'll go in the next few months! Can the contrast become Japan and Europe get any more clear? Your making even more plans to try and help you analyst,

|

|---|

Send this article to a friend:

|

|

|

We begin this week with a simple pop quiz. Is inflation good or bad? Answer quickly. I'm sorry – your answer is wrong. Or rather, we can't know if your answer is right or wrong because we are not sure what is meant by the question. We may think we know – and we may be right – but we can't be sure, because the word inflation has different meanings for different people in different places and different times. In fact, even the same people in the same place and time can't agree on a precise definition.

We begin this week with a simple pop quiz. Is inflation good or bad? Answer quickly. I'm sorry – your answer is wrong. Or rather, we can't know if your answer is right or wrong because we are not sure what is meant by the question. We may think we know – and we may be right – but we can't be sure, because the word inflation has different meanings for different people in different places and different times. In fact, even the same people in the same place and time can't agree on a precise definition.