|

"Sic Transit Gloria Pecuni" - LME Considering Ending Sterling, Allowing Renminbi Settlement

On a long enough timeline, all things come to an end. Even for such venerable venues as the London Metals Exchange, with its 130 year history, and its annual turnover of over $11 trillion in metal contracts, which also makes it the largest market for non-ferrous metals. As the English FT reminisces, "When the LME was established in 1877, Britain was one of the world’s most important manufacturing powerhouses, and the LME’s benchmark contracts for delivery in three months were designed to mirror the length of time needed to reach British ports for shipments of copper from Chile and tin from Malaysia." Furthermore, in the beginning, and all the way through 1993, the flagship copper contract was denominated in sterling, at which point it was switched to the USD following the "Black Wednesday" ERM sterling crisis, courtesy of George Soros who made about $1 billion by shorting the GBP, and formally ended the sterling's role as even an informal backup reserve currency. As of today, insult follows inury, as the LME has formally asked the members of the exchange to drop the sterling contract denomination (in addition to USD, EUR, and JPY contracts) and replace it with the Chinese renminbi. Why this sudden and dramatic, if gradual and tacit, admission that the CNY is the ascendent reserve currency? Because, as the FT reminds us, China has become the market for non-ferrous metals: it is "the dominant force in the market, accounting for more than 40 per cent of global demand for most metals and a rapidly increasing share of trading in LME futures." Add that to yesterday's news of a widening in the CNY band (which incidentally is much ado about nothing, at least for now: at best it will allow China to devalue its currency when and if it so desires much faster than before, much to Geithner's final humiliation), and to the previously reported extensive network of bilateral CNY-based trade agreements already cris-crossing Asia, and one can see why if America is not worried about the reserve status of the dollar, it damn well should be.

Why China? Because, for better or worse, it has become the marginal buyer.

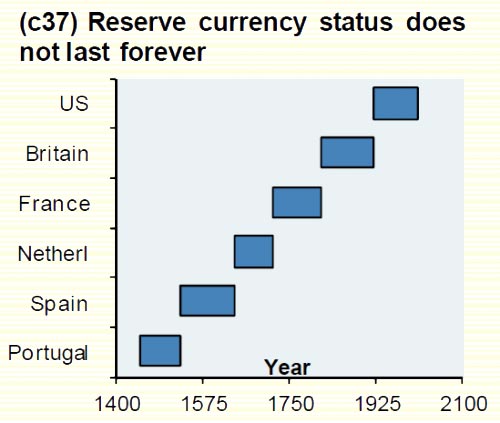

The implications, at least optically, need no further explanation. We would like to conclude with our favorite chart from JPMorgan, which we have dubbed sic transit gloria pecuni.

At this point we are fairly confident which currency is coming next in the new top right space (whether backed by hard assets, and in joint execution with Russia and/or Germany, or not). |

|

|