|

Peak Exorbitant Privilege

45% of containers exported from port operator APM Terminals’ Port Elizabeth facility (part of the Port of New York and New Jersey) are empty, a reflection of the trade imbalance." Source In the wake of WWI (1914-1918) there was an international movement in Europe to return to the stability of fixed exchange rates between national currencies. But all of them had been inflated so much during the war that reestablishing the peg to gold at the pre-war price would have implied an overvaluation of currencies that would have led inevitably to a run on all the gold in the banking system, monetary deflation and economic depression (good thing they avoided that, eh?). At the same time, they feared that raising the gold price would raise questions about the credibility of the new post-war regime, and quite possibly cause a global scramble into gold. This "problem" with gold was viewed at the time as a "shortage" of gold. And so one of the stated goals of the effort to solve this problem was "some means of economizing the use of gold by maintaining reserves in the form of foreign balances." (Resolution 9 at the Genoa Conference, 1922) To economize means to limit or reduce, often used in conjunction with "expense" or "waste". So to "economize the use of gold" meant to limit or reduce the use of gold. Meanwhile, the United States had emerged from the war as the major creditor to the world and the only post-war economy healthy enough to lend the financial assistance needed for rebuilding Europe. And so even though the U.S. wasn't directly involved in the European monetary negotiations that took place in Brussels in 1920 and Genoa in 1922, it was acknowledged that any new monetary order was likely to be a U.S. centered system. The Genoa negotiations were led by the English including British Prime Minister Lloyd George and Bank of England Governor Montagu Norman who proposed a "two-tier" system especially designed to circumvent "the gold shortage". The British proposal described a group of "center countries" who would hold their reserves entirely in gold and a second tier group of (unnamed) countries who would hold reserves partly in gold and partly in short-term claims on the center countries. [1] The proposal was named the "gold-exchange standard" (as opposed to the previous gold standard). In 1932 French economist Jacques Rueff proclaimed the gold-exchange standard that had come out of the Genoa conference a decade earlier "a conception so peculiarly Anglo-Saxon that there still is no French expression for it." [2] The gold-exchange standard that officially came into being around 1926 (and lasted only about six years in its planned form) worked like this: The U.S. dollar was backed by and redeemable in gold at any level, even down to small gold coins. The British pound was backed by gold and dollars and redeemable in both, but for gold, only in large, expensive bars (kind of like the minimum gold redemption in PHYS is 400 oz. bars but you can redeem in dollars at any level). Other European currencies were backed by and redeemable in British pound sterling, while both dollars and pounds served as official reserves equal to gold in the international banking system. [3] Since only the U.S. dollar was fully redeemable in gold, you might expect that gold would have immediately flowed out of the U.S. and into Europe. But as I already explained, the U.S. emerged from WWI as the world's creditor and the U.S. Treasury in 1920 held 3,679 tonnes of gold. By the beginning of the gold-exchange standard in 1926 the U.S. was up to 5,998 tonnes and by 1935 was up to 8,998 tonnes. By 1940 the U.S. Treasury held 19,543 tonnes of gold. After WWII and the start of the new Bretton Woods monetary system, official U.S. gold peaked at 20,663 tonnes in 1952 where it began its long decline. [4] In Once Upon a Time I wrote, "Once sterilized [at the 1922 Genoa Conference], gold flowed uncontrolled into the US right up until the whole system collapsed and beyond." My point was that before the introduction of "paper gold" as official reserves in the form of dollars and pounds, the flow of physical gold in international trade settlement governed as a natural adjustment mechanism for national currencies and exerted the spur and brake forces on their economies. But after 1922, this was no longer the case. After 1922, the U.S. provided the majority of the reserves for the international banking system in the form of printed dollars. And as the world's creditor and reserve printer, dollar reserves flowed out and gold payments flowed in. From the start of the gold-exchange standard in the mid-1920s until 1952, about 26 years, the dollar's monetary base grew from $6B to $50B while the U.S. gold stockpile grew from 6,000 tonnes to more than 20,000 tonnes. [5] The Roaring Twenties was not just a short-lived period of superficial prosperity in America, it was also a time when a great privilege was unwittingly granted to the United States that would last for the next 90 years. And I say "unwittingly granted" because the U.S. did not even participate in the negotiations that led to its privilege. As Jacques Rueff wrote in his 1972 book, The Monetary Sin of the West: "The situation I am going to analyze was neither brought about nor specifically wanted by the United States. It was the outcome of an unbelievable collective mistake which, when people become aware of it, will be viewed by history as an object of astonishment and scandal." [6] I should pause here to note that gold standard advocates and hard money campers will quickly point out that the post-1922 gold-exchange standard is not what they want. They want to return to the gold standard of the 19th century, the one before WWI. But that's not my position. And anyway, it's not gonna happen and even if it would/could happen, it would not fix the fundamental problem. Just like time, we move relentlessly forward and, luckily for us, the future is much brighter than the past. Now, back to this privilege which, in the end, may turn out to be more of a curse. In order to really understand how the gold-exchange standard and its successor systems, the Bretton Woods system and the current dollar standard system translated into a privilege for the United States, we need to understand what actually changed in the mid-20s as it fundamentally relates to how we use money. I will explain it as briefly as possible but I want to caution you to resist the temptation to make judgments about what is wrong here as you read my description. As some of you already know, I think there is only one fundamental flaw in the system and it was present even before the gold-exchange standard and the U.S. exorbitant privilege, but that's not the subject of this post. What changed? People and economies trade with each other using money – mainly credit, denominated in a national currency – as their primary medium of exchange so as to avoid the intractable double coincidence of wants problem with direct barter. So we trade our stuff for their stuff using bank money (aka fungible currency-denominated credit) and the prices of that stuff is how we know if there is any inequity or imbalance in the overall trade. When we periodically net out the bank transactions using the prices of the stuff we traded, we inevitably come up short on one side or the other. And so that imbalance is then settled in the currency itself. But because different countries use different currencies, we need another level of imbalance clearing. And that international level is cleared with what we call reserves. So, in essence, we really do have two tiers in the way we use money. We have the domestic tier where everyone uses the same currency and clearing is handled at the commercial bank level with currency. And then we have the international tier where everyone doesn't use the same currency and so trade imbalances tend to aggregate and then clear with what we call "reserves" (aka international liquidity) at the national or Central Bank level. This is built right into the very money that we use, and have used, for a very long time. To see how, we will regress conceptually back to how our bank money is initially conceived. And because most of you have at least a basic understanding of the Eurosystem's balance sheet from my quarterly RPG posts, this should be a fairly easy exercise. If not, RPG #4 might be a good place to catch up quickly. Recall this chart from Euro Gold:

In our regression exercise we'll see the fundamental difference between reserves and assets. Reserves are the fundamental basis on which the basic money supply of a bank is borne, while assets are the balance sheet representation of the bank's extension of credit. Changes in the ratio between reserves and assets exert opposing (enabling/disabling) influences on the ability of the system to expand. So, now, looking back at the very genesis of our money, we've all heard the stories of the gold banker who issues receipts on the gold he has in his vault, right? Well, that's basically it. Money as we know it today ultimately begins with the monetization of some gold. The Central Bank has some amount of gold in the vault which it monetizes by printing cash. CB

Assets-------Liabilities

Gold | Cash

For the sake of this exercise, let's say that the government deposits its official gold in its newly-created CB and the CB monetizes that gold by printing cash which is now a government deposit. So let's simplify the balance sheet even more. CB = Central Bank, R = reserves, A = assets and C = cash (or also CB liabilities which are electronic obligations of the CB to print cash if necessary, so they are essentially the same thing as cash within the banking system).

CB

R|C That's reserves (gold) on the asset side of the balance sheet and cash (the G's deposit) on the liability side. Now the G can spend that cash into the economy where it will end up at a commercial bank. Let's say COMMBANK1 = commercial bank #1, C = cash (or CB liabilities) and D = deposit.

COMMBANK1

C|D Now that the G spent money into the economy, our first commercial bank has its own reserves and its first deposit from a government stooge who received payment from G and deposited it in COMMBANK1. In the commercial bank, cash is the reserve on the asset side of the balance sheet whereas cash is on the opposite side, the liability side, of the Central Bank's balance sheet. Also, all the cash issued by the CB remains on its balance sheet even after it has left the building and is sitting in the commercial bank (or even in a shoebox under your bed). At this point we have a fully reserved mini-monetary system. Both the CB's and the commercial bank's liabilities are balanced with reserves. The CB's reserves are gold and the commercial bank's reserves are cash or CB liabilities. That's fully reserved. But let's say that the economy is trying to grow and the demand for bank money (credit) is both strong and credible. So now our banks can expand their balance sheets. As credit expands, the asset side will be balanced with assets (A) rather than reserves (reserves are gold in the case of the CB and cash in the case of COMMBANK1). Also, I'm going to put the CB under the commercial banks since it is essentially the base on which the commercial bank money stands.

COMMBANK1

ACC|DDD ________________________________________ CB AR|CC Here we see that our CB now has an asset and a reserve. The asset is a claim denominated in its own currency against a resident of its currency zone, and the reserve is the gold. Let's say that the CB lent (and therefore created) a new C to the government. Meanwhile, our commercial bank COMMBANK1 has had two transactions. It has received the deposit from a second government stooge and it has also made a loan to a worthy entrepreneur. So on the COMMBANK1 (commercial bank) balance sheet, the A is a claim against our entrepreneur and the two Cs are cash reserves. The first C came in when our first stooge deposited his government paycheck and the second C came in when the second stooge deposited his payment which G had borrowed (into existence) from the CB. The three Ds (deposits) belong to our two stooges and the entrepreneur. I'm not going to go much further with this model but eventually, as the economy and bank money expands, we'll end up with something that looks more like this:

COMMBANK1

AAACC|DDDDD

COMMBANK2

COMMBANK3

COMMBANK4

COMMBANK5 And here we have a simple model of our monetary system within a single currency zone. There are two observations that I want to share with you through this little exercise. The first is the tiered nature of our monetary system even within a single currency zone. And the second is the natural makeup of a Central Bank's balance sheet. You'll notice that one thing the Central Bank and the commercial banks have in common is that the asset side of their balance sheets consist of both reserves and assets. Remember that assets are claims denominated in your currency against someone else in your currency zone. But you'll also notice that the commercial bank reserves are the same thing as the Central Bank's liabilities. So the Central Bank issues the reserves upon which bank money is issued to the economy by the commercial banks. The fundamental take-home point here is that reserves are the base on which all bank money expands. CB money rests on CB reserves and commercial bank money rests on commercial bank reserves which are, in fact, CB money which is resting on CB reserves. So you can see that the entire money system is built up from the CB reserves. The deposits (D) in the commercial banks are both redeemable in reserves and cleared with reserves (reserves being cash or CB liabilities). Deposits are not redeemable or cleared (settled) with assets. If a commercial bank has a healthy level of reserves it can expand its credit. But if it expands credit without sufficient reserves for its clearing and redemption needs, it must then go find reserves which it can do in a number of ways. Notice above that we have 25 deposits at 5 commercial banks based on 10 commercial bank reserves. Those commercial bank reserves are Central Bank liabilities which are based ultimately on the original gold deposit. Before 1933, gold coins were one component of the cash, and CB liabilities were also redeemable by the commercial banks in gold coin from the CB to cover redemption needs. So the commercial banks (as well as the Fed) had to worry about having sufficient reserves of two different kinds. As you can imagine, this created another level of difficulty in clearing and especially in redemption. Clearing and Redemption Very quickly I want to go over clearing and redemption and how they can move reserves around in the system. Here's our simple system once again:

COMMBANK1

AAACC|DDDDD

COMMBANK2

COMMBANK3

COMMBANK4

COMMBANK5 Now let's say that one of our depositors at COMMBANK5 withdrew his deposit in cash. And let's also say that another depositor at the same bank spent his money and his deposit was therefore transferred to COMMBANK4 and that transaction cleared. Here's what it would look like:

COMMBANK1

AAACC|DDDDD

COMMBANK2

COMMBANK3

COMMBANK4

COMMBANK5

Those of you who have been reading my blog for a while should be aware that the U.S. has run a trade deficit every year since 1975. You should also know that, since 1971, the U.S. government has run its national debt up from $400B to $15,500B, and that foreign Central Banks buying this debt have been the primary support for both the relatively stable value of the dollar and the perpetual nature of the U.S. trade deficit. But it wasn't always this way. Before 1971 the U.S. was running a trade surplus and the national debt level was relatively steady during both the gold-exchange standard and the Bretton Woods era. During the gold-exchange standard the national debt ranged from about $16B up to $43B. It increased a lot during WWII to about $250B, but then it remained below its $400B ceiling until 1971. Another big difference during this timeline which I have already mentioned is the flow of gold. The U.S. experienced an uncontrolled inflow of gold from the beginning of the gold-exchange standard until 1952, and then a stunted outflow ensued until it was stopped altogether in 1971. The point is that with such a wide array of vastly disparate circumstances, it is a bit tricky for me to explain the common thread that binds this timeline together. Very generally, let's call this common thread the monetary privilege that comes from the rest of the world voluntarily using that which comes only from your printing press as its monetary reserves. It started as a privilege, grew into an exorbitant privilege 35 years later, and then peaked 45 years later at something for which, perhaps, there is not an appropriately strong enough adjective. Robert Triffin thought it had gone far enough to warrant warning Congress in 1960, but just wait till you see how much farther it went over the next four and a half decades. But first, let's go back to 1931. First Warning In his 1972 book [6], Jacques Rueff writes:

On 1 October 1931 I wrote a note to the Finance Minister, in preparation for talks that were to take place between the French Prime Minister, whom I was to accompany to Washington, and the President of the United States. In it I called the Government's attention to the role played by the gold-exchange standard in the Great Depression, which was already causing havoc among Western nations, in the following terms: "There is one innovation which has materially contributed to the difficulties that are besetting the world. That is the introduction by a great many European states, under the auspices of the Financial Committee of the League of Nations, of a monetary system called the gold-exchange standard. Under this system, central banks are authorized to include in their reserves not only gold and claims denominated in the national currency, but also foreign exchange. The latter, although entered as assets of the central bank which owns it, naturally remains deposited in the country of origin.The use of such a mechanism has the considerable drawback of damping the effects of international capital movements in the financial markets that they affect. For example, funds flowing out of the United States into a country that applies the gold-exchange standard increase by a corresponding amount the money supply in the receiving market, without reducing in any way the money supply in their market of origin. The bank of issue to which they accrue, and which enters them in its reserves, leaves them on deposit in the New York market. There they can, as previously, provide backing for the granting of credit. Thus the gold-exchange standard considerably reduces the sensitivity of spontaneous reactions that tend to limit or correct gold movements. For this reason, in the past the gold-exchange standard has been a source of serious monetary disturbances. It was probably one cause for the long duration of the substantial credit inflation that preceded the 1929 crisis in the United States."Then in 1932 he gave further warning in the speech at the School of Political Sciences in Paris which I wrote about in Once Upon a Time: The gold-exchange standard is characterized by the fact that it enables the bank of issue to enter in its monetary reserves not only gold and paper in the national currency, but also claims denominated in foreign currencies, payable in gold and deposited in the country of origin. In other words, the central bank of a country that applies the gold-exchange standard can issue currency not only against gold and claims denominated in the national currency, but also against claims in dollars or sterling.Are you starting to get a sense of the key issue yet? Reserves move from one bank to another to settle a transaction. When our depositor at COMMBANK5 spent his deposit and it was thereby transferred to COMMBANK4, the cash (C) reserve was also moved to COMMBANK4 to settle (or clear) the transaction. This put a certain strain on COMMBANK5 since it had also lost another reserve to redemption which forced COMMBANK5 into the action of seeking reserves. Or when a Central Bank expends its reserves trying to remove a glut of its currency abroad so that the marketplace won't devalue (or collapse) it, that CB is generally limited to a finite amount of reserves which, once spent, are gone. So the movement of reserves serves two purposes. It is not only attained by the receiver but it is also forfeited by the giver. Both are vital to a properly functioning monetary system. But with the system that began around 1926 and still exists today, we end up with a situation in which one currency's reserves are actually deposits in another currency zone:

Notice that I am avoiding the use of gold in my illustration. The warnings given in 1931 and 1960 were presented in the context of a gold exchange standard of one form or another, and therefore they (of course!) heavily reference the problems as they related to ongoing gold redemption. But the real problem, as I have said, transcends the specific issues with gold at that time. The real problem was and is the common thread I mentioned earilier: the monetary privilege that comes from the rest of the world voluntarily using that which comes only from your printing press as its monetary reserves. It was and is, as Jacques Rueff put it, "the outcome of an unbelievable collective mistake which, when people become aware of it, will be viewed by history as an object of astonishment and scandal." Another angle which was apparent from the very beginning—because Rueff mentioned it in 1932 (as quoted above)—was that of international lending. It basically worked in the same way as the three steps above except that the net international (trade) payment was an international loan. Remember that the U.S. was the prime creditor to the world following both wars. This may partly explain the inflow of gold payments that brought the U.S. stockpile up from 3,679 tonnes in 1920 to 20,663 tonnes in 1952. A dollar loan was the same as a gold loan and was payable in dollars or gold. But as Rueff pointed out above, the lent dollars came immediately back to New York just as the pounds came back to London: "During the entire postwar period, Britain was able to loan to Central European countries funds that kept flowing back to Britain, since the moment they had entered the economy of the borrowing countries, they were deposited again in London. Thus, like soldiers marching across the stage in a musical comedy, they could reemerge indefinitely and enable their owners to continue making loans abroad."Now think about that for a moment. The same reserves (base money) getting lent out over and over again like a revolving door. And let's jump forward to the present for a moment to see if we can start connecting some dots between 1932 and 2012. Here's a recent comment I wrote about the revolving door of dollars today: Hello Victor,I highlighted the part relevant to our revolving door discussion, but the whole comment is relevant to the whole of this post because I had this post in mind when I wrote the comment. Anyway, can you see any similarity between what Jacques Rueff wrote about the sterling in 1932 and what I wrote last week? How about a difference? That's right, the U.S. is now the world's premier debtor while it was the world's creditor back in the 30s. But in both cases the dollar currency is being continuously recycled while notations recording its passage pile up as reserves on which foreign bank money is expanded while the U.S. counterpart of reserves and bank money is not reduced as a consequence of the transfer. If you print the currency that the rest of the world uses as a reserve behind its currency, that alone enables you to run a trade deficit without ever reducing your ability to run a future trade deficit. Deficit without tears it was called. For the rest of the world, running a trade deficit has the finite limitation of the amount of reserves stored previously and/or the amount of international liquidity (reserves) your trading partner is willing to lend you. Another thing that happens is that, as the printer of the reserve, the rest of the world actually requires you to run a balance of payments deficit or else its (the rest of the world's) reserves will have to shrink, and its currency, credit and economy consequently contract. So to avoid monetary and economic contraction, the world not only puts up with, but supports your deficit without tears. Here's a little more from Jacques Rueff:

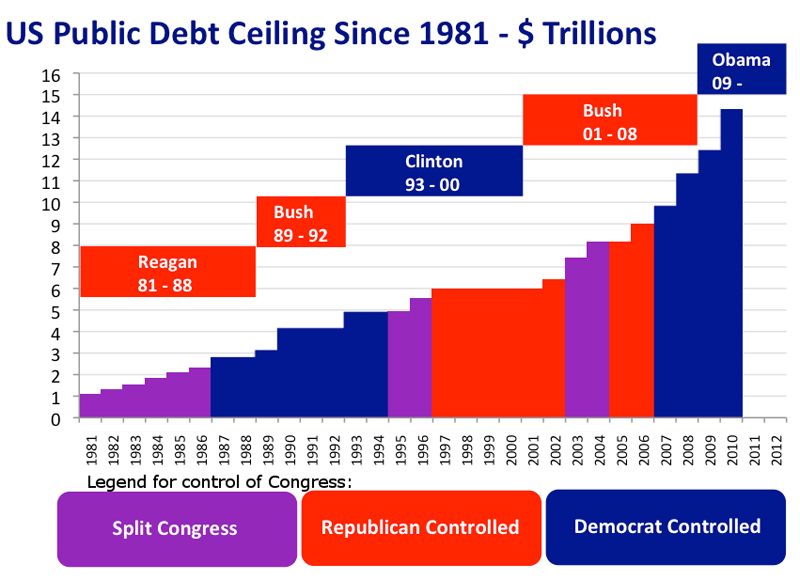

The Secret of a Deficit Without Tears [6]Second Warning By the early 1960s, Jacques Rueff was not alone in speaking out against the American privilege embedded in the monetary system. Another Frenchman named Valéry Giscard d'Estaing, who was the French Finance Minister under Charles de Gaulle and would later become President himself, coined the term "exorbitant privilege". [7] Even Charles de Gaulle spoke out in 1965 and you can see a short video of that speech in my post The Long Road to Freegold. But perhaps more significant than the obvious French disdain for the system was Robert Triffen, who stood before the U.S. Congress in 1960 and warned: "A fundamental reform of the international monetary system has long been overdue. Its necessity and urgency are further highlighted today by the imminent threat to the once mighty U.S. dollar."To put Triffin in the context of our previous discussion, here's what Jacques Rueff had to say about him: "Some will no doubt be surprised that in 1961, practically alone in the world, I had the audacity to call attention to the dangers inherent in the international monetary system as it existed then.And here is what Wikipedia says about Robert Triffin's Congressional testimony: "In 1960 Triffin testified before the United States Congress warning of serious flaws in the Bretton Woods system. His theory was based on observing the dollar glut, or the accumulation of the United States dollar outside of the US. Under the Bretton Woods agreement the US had pledged to convert dollars into gold, but by the early 1960s the glut had caused more dollars to be available outside the US than gold was in its Treasury. As a result the US had to run deficits on the current account of the balance of payments to supply the world with dollar reserves that kept liquidity for their increased wealth. However, running the deficit on the current account of the balance of payments in the long term would erode confidence in the dollar. He predicted the result that the system would not maintain both liquidity and confidence, a theory later to be known as the Triffin dilemma. It was largely ignored until 1971, when his hypothesis became reality, forcing US President Richard Nixon to halt convertibility of the United States dollar into gold, an event with consequences known as the Nixon Shock. It effectively ended the Bretton Woods System." [8](For more on the Triffin dilemma, please see my posts Dilemma and Dilemma 2 – Homeless Dollars. And for a glimpse at what I view as an even more fundamental dilemma, you'll find "FOFOA's dilemma" in my post The Return to Honest Money.) As noted above, Triffin's prescription in the 1960s was at odds with Rueff and the French contingent. In fact, even today, the IMF refers to "Triffin's solution" as a sort of advertisement for its own product, the almighty SDR. [9] From the IMF website: Triffin's Solution  But even though Triffin proposed something like the SDR (a proposal the IMF loves on to this day), I think that actions speak louder than words. Robert Triffin was a Belgian economist who became a U.S. citizen in 1942 after receiving his PhD from Harvard. He worked for the Federal Reserve from 1942 to 1946, the IMF from 1946 to 1948 and the precursor to the OECD from 1948 until 1951. He also taught economics at both Harvard and Yale. But in 1977 he reclaimed his Belgian citizenship, moved back to Europe, and helped develop the European Monetary System and the concept of a central bank for all of Europe which ultimately became the ECB five years after his death in 1993. Final Warning With the end of the Bretton Woods monetary system in 1971, three things (besides the obvious closing of the gold window) really took hold. The first was that the U.S. began running (and expanding) a blatant trade deficit. It went back and forth a couple of times before it really took hold, but starting in 1976 we have run a deficit every year since. [10] The second thing that took hold was something FOA called "credibility inflation". You can read more about it in my aptly-titled post, Credibility Inflation. This phenomenon, at least in part, helped grow the overall level of trade between the U.S. and the rest of the world in both nominal and real terms. In inflation adjusted terms, U.S. trade with the rest of the world is up almost eightfold since 1971. [11] The third thing was that the U.S. federal government began expanding itself in both nominal and real terms by raising the federal debt ceiling and relying more heavily on U.S. Treasury debt sales. From Credibility Inflation (quoting Bill Buckler): Way back in March 1971, four months before Nixon closed the Gold window, the "permanent" U.S. debt ceiling had been frozen at $400 Billion. By late 1982, U.S. funded debt had tripled to about $1.25 TRILLION. But the "permanent" debt ceiling still stood at $400 Billion. All the debt ceiling rises since 1971 had been officially designated as "temporary!" In late 1982, realizing that this charade could not be continued, The U.S. Treasury eliminated the "difference" between the "temporary" and the "permanent" debt ceiling. The way was cleared for the subsequent explosion in U.S. debt. With the U.S. being the world's "reserve currency," the way was in fact cleared for a debt explosion right around the world.Here are the debt ceilings through 2010 as found on Wikipedia:

That's all well and good, but to really see the U.S. exorbitant (is there a stronger word?) privilege of the last 40 years in stark relief, we must think about those empty containers we export from the picture at the top. Those containers come in full and leave empty, just to be refilled again overseas and brought back in. Those empty containers represent the real trade deficit, the portion of our imports that we do not pay for with exports. Those empty containers represent the portion of our imports that we pay for with nothing but book entries which are little more than lines in the sand. [12] Here's my thesis: that the U.S. privilege which began in Genoa in 1922, and was so complicated that only one in a million could even fathom it in 1931 and 1960, became as clear as day for anyone with eyes to see after 1971. And so, to see it in real (not nominal) terms, we can very simply look at the percentage of our imports that is not paid for with exports. So simple, which might be why the government doesn't publish that number and the media doesn't talk about it. All you have to do is compare the goods and services balance (which is a negative number or a deficit every year since 1975) with the total for all goods and service imports. That's comparing apples with apples. For example, in 1971 total imports were $60,979,000,000 and total exports were $59,677,000,000 leaving us with a trade deficit of $1,302,000,000. It doesn't matter what the price of an apple was in 1971, because whatever it was, we still imported 2.14% more stuff than we exported. 1,302 ÷ 60,979 = 2.14%. A trade discrepancy of 2.14% in any given year would be normal under normal circumstances. You'd expect to see it alternate back and forth from deficit to surplus and back again as it actually did from 1970 through 1976. But it becomes something else entirely when you go year after year (for 36 years straight) importing more than you export. And that's why I showed that little dip in the above timeline visualization of the U.S. exorbitant privilege at 1971. And now here's what it looks like charted out from 1970 through 2011:

Here's the data from the chart:

As you can see, the U.S. exorbitant privilege (essentially free imports) peaked in 2005 at an astounding 35.5%, or more than a third of all imports! Stop and think about that for a second. For every three containers coming in full, only two went out full. So how do we reconcile that number (35.5%) with the report at the top of this post that said 45% of containers are exported empty? The answer is simple. The trade deficit includes both goods and services. But services are not imported in containers. In fact, the U.S. has been running a trade surplus on services every year since 1971. Imagine that! So if we look only at the portion of goods coming and going, we get an even higher percentage. So let's look at 2005 in particular. In 2005 we imported $1.692T in goods but we exported only $911B for a goods balance of payments of negative $781B. That equates to 46% of all containers being exported empty in 2005. That goods deficit has since dropped down to around 33% for the last three years, so perhaps 45% empty containers in 2010 can be explained by the location of the Port Elizabeth facility being only 200 miles from Washington DC, consumption capital of the world. But all of this is kind of beside the point. The point is that the U.S. exorbitant privilege peaked in 2005, for the last time, at its all-time high of a third of all imports, and soon it will go negative, where it hasn't been in a really long time. I can say this with absolute confidence because the signs are everywhere, even if nobody is talking about them in precisely these terms. Here's one bloodhound who's at least onto the right scent (from Barrons):

But more recent Treasury data show China has been selling Treasuries outright. And while the markets have been complacent to the point of snarkiness, MacroMavens' Stephanie Pomboy thinks that's wrong. Unlike other Cassandras, she's been right in her warnings -- notably in the middle of the last decade that the U.S. financial system was dangerously exposed to a bubble in U.S. real estate. Hers was a lonely voice then because everybody knew, of course, house prices always rose.That was from March 2nd. Here's another one from the same writer at Barrons just a few days ago:

Our friend, Stephanie Pomboy, who heads the MacroMavens advisory, offers some other inconvenient facts about the Treasury market: Uncle Sam is borrowing some $1.1 trillion a year, while our foreign creditors have been buying just $286 billion.Of course they are looking only at the monetary plane, the silly market for U.S. Treasury debt which the Fed can dominate with infinite demand. As I keep saying, the real threat to the dollar is in the physical plane: the price of all those containers being unloaded and then exported empty. The U.S. government has grown addicted to its exorbitant privilege over the years. It is a privilege that has been supported by foreign Central Banks buying U.S. debt for the better part of the last 30 years. But as I wrote in Moneyness, and as Ms. Pomboy has noticed above, that ended a few years ago. From Moneyness, the blue that I circled below shows the Fed defending our exports **of empty containers** with nothing more than the printing press and calling it QE:

I would like you all to give this some serious thought:

1. The U.S. exorbitant privilege peaked in 2005 (before the financial crisis) and is now on the decline, meaning it is no longer supported abroad. So what could possibly go wrong? The recession has already contracted the U.S. economy, all except the part that resides in Washington, DC. And just to maintain its own status quo (when has it ever been happy doing only that?) our federal government needs to insure our national business of exporting empty containers at its present level. What could go wrong? Prices! If the price of an apple doubles, what do you think happens to the price of a full container? Those of you who think we are due for some more price deflation in the stuff that the USG needs to maintain its status quo should really have your heads examined. Even Obama is winding up to pitch the whole ball of twine at the problem. He just delegated his executive power to print until the cows come home to each of his department heads. I quote from Executive Order -- National Defense Resources Preparedness:

"To ensure the supply… from high cost sources… in light of a temporary increase in transportation cost… the head of each agency… is delegated the authority… to make subsidy payments"

Big Gap in Understanding Weakens Deflationist Argument Just Another Hyperinflation Post - Part 1 Just Another Hyperinflation Post - Part 2 Just Another Hyperinflation Post - Part 3 That's right, I saved the "crazy super-hyperinflation talk" for the tail end of a really long post. Because A) people who think they have it all figured out already tend to abandon a post once they read the word "hyperinflation", and B) the stuff in this post really happened and is still happening so it's only fair to you, the reader, to give its inevitable denouement the appropriate weight of a bold conclusion. If I didn't do that, I would not have done my job, now would I? ;) And in case you didn't figure it out yet, this third and final warning was only for the savers who are still saving in dollars. It's way too late to fix the $IMFS. Sincerely, FOFOA PS. Thanks to reader FreegoldTube for the custom video below! He just happened to send me the link while I was considering songs for this post. The band is Muse and the song is Uprising from their album titled The Resistance. [1] http://mauricio.econ.ubc.ca/pdfs/kirsten.pdf

|

|

Send this article to a friend:

|

|