Send this article to a friend:

February

13

2026

|

Send this article to a friend: February |

Is Silver Being Suppressed? And What's Happening With Gold?

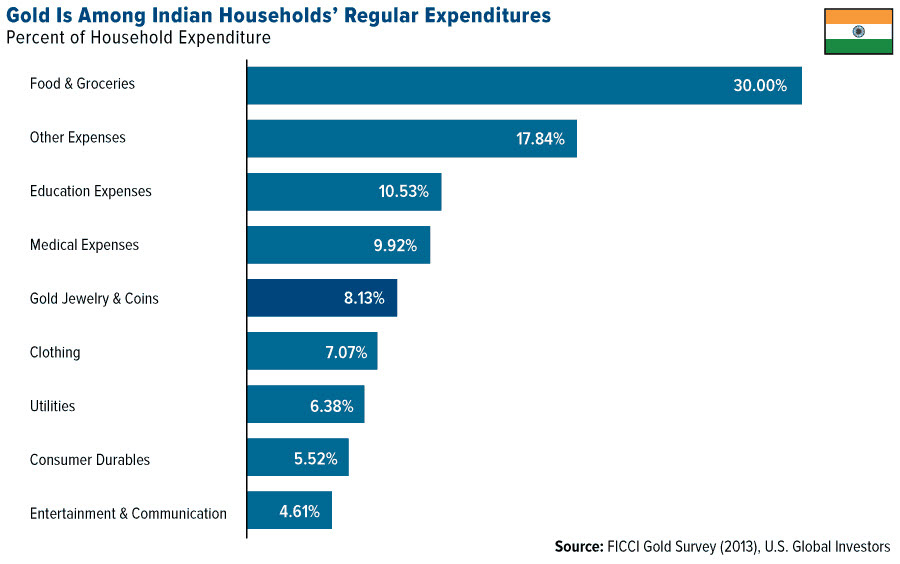

Gold’s recovery came fast – are $6,000 forecasts back on the table? Gold’s return to $5,000 happened faster than most people expected. According to Barron's, strategists at Deutsche Bank pointed to aggressive dip-buying after last week’s pullback, framing the move as a "technical rebound" rather than a "structural signal." That explanation misses the larger context. The announcement of Kevin Warsh as the next Federal Reserve Chair immediately revived the familiar narrative: A “hawkish” Fed is supposedly bad for gold. But hawkish relative to what, exactly? Warsh inherits an economy shaped by the most aggressive rate-hiking cycle in half a century. Historically, such cycles end not with a return to the status quo, but with equally aggressive reversals once economic stress becomes obvious. (That's where the line, the Fed raises rates till something breaks comes from.) And we all know what happens after something breaks... That isn’t a forecast, by the way, just historical precedent. What’s notable this time is how long the Fed delayed cutting. Reuters reporting throughout the past year has consistently pointed to the central bank’s concern about credibility after underestimating inflation earlier in the cycle. Delaying rate cuts wasn’t about economic strength – it was about optics. Meanwhile, major institutions are quietly adjusting expectations. JPMorgan, which has been among the more disciplined forecasters during this cycle, recently lifted its longer-term gold outlooktoward the $6,000–$6,300 range, citing currency debasement and global demand. Strip away the political storytelling and gold’s behavior looks less mysterious. Over the past two weeks, it’s up roughly $100 – hardly the “collapse” implied by so many breathless headlines. The lesson here is simple: The price of gold isn’t reacting to personalities. It’s responding to the reality of the monetary constraints our world finds itself in. Note I'm not talking just about the U.S. but the entire developed world. Which helps explain why global gold buying keeps rising. Silver shorting explains more than investors are being told Silver’s failure to keep pace with gold continues to puzzle casual observers. And frustrate long-time silver owners. Bloomberg recently reported on a massive $288 million silver short from Chinese billionaire trader Bian Ximing, framing it as an aggressive but ordinary speculative wager. Now, that's true, as far as it goes. Except for one thing: scale. A single position of that size can overwhelm physical supply dynamics in a paper-driven market. Especially when no physical silver is required to establish the trade. This matters because silver is already running a structural deficit – estimated by industry groups at 100-200 million ounces annually. For the last six years in a row! Yet much of the mainstream commentary treats silver’s price move as if it were merely “reassessing” its relationship to gold, or reacting to shifting industrial demand. Those factors do matter – but they don’t explain why silver struggles even as gold reclaims $5,000. Gold is routinely described as benefiting greatly from both central bank demand and anticipated interest rate cuts. Silver shares those macro drivers and adds industrial scarcity on top of them. (Unlike gold, silver demand is roughly split between industrial/manufacturing use and investment.) The result is a growing disconnect between fundamentals like supply and demand and the price of silver. For patient savers, the implication is pretty clear. It’s a different perspective. Here at Birch Gold Group, we don't "trade." And we don't want to work with traders, either. We encourage our customers to focus on long-term, buy-and-hold strategies. This is important, because markets can stay distorted for a long time, longer than we can easily anticipate. Especially when leverage can drive price farther and faster than reality. Why Indian savers are being nudged away from gold A different kind of signal came this week from India. CNBC reports that Larry Fink of BlackRock and Mukesh Ambani of Reliance Industries publicly encouraged Indian investors to diversify their savings away from gold and toward financial assets. Before we start making accusations, let's take a step back and consider the larger context: India’s population is estimated to hold more than 25,000 tons of gold – by far the largest private gold hoard in the world. That's more than three times the amount of gold bullion in the U.S. gold reserve (the world's largest central bank gold reserve). In India, though, that gold isn’t owned by institutions. It’s owned by families (often as jewelry), accumulated in small increments over the years and handed down from generation to generation. This is an old chart from 2013, but it still gives you an idea of just how important gold is to families in India:

via Forbes In India, gold functions less like an investment and more like a parallel savings account. One that's outside the banking system, immune to currency and inflation risk and firmly outside the government's or the central bank's control. Indian authorities have spent years promoting “monetization” programs deliberately designed to draw physical gold back out of jewelry boxes and floor safes, back into the financial system. Their success has been limited so far. See, families in India consider gold a safe haven asset exactly because it's outside the financial system. Their cultural memory and lived experience, hard-earned over the decades, still favor tangible wealth immune to government mismanagement. Here's the thing: Encouraging savers to abandon gold isn’t really about modernization. It’s about getting household savings into assets that can be taxed, measured and "managed" by officials. I don't think Bank of India staff aren't laying awake at night fearing their citizens are "missing out" on capital growth. Instead, they're asking themselves, "Why do our citizens distrust the currency so much key keep buying gold?" The strange thing about their response, though? Instead of focusing on creating a stronger, more stable currency, they're working on offers designed to get privately-owned gold into the central bank's vaults. Whether their efforts ultimately succeed remains an open question. So far they haven't resulted in long lines of enthusiastic gold-sellers. History suggests that, when people understand currency risk firsthand, because they've lived through it, simple persuasion struggles to convince them that "this time is different." Here's a personal message to any readers from India: I strongly recommend you hang onto your gold! Lessons from the week Across all three stories, the pattern is the same.

None of these conclusions requires a conspiracy theory, does it? Human incentives explain it well enough. And if you, like those families in India, want to diversify your savings with tangible physical gold and silver, I don't blame you! The whole Birch Gold team is here to help. You can learn more about how to purchase precious metals.

|

Send this article to a friend:

|

|

|

Gold’s rebound has revived $6,000 forecasts, but silver remains oddly stuck. Meanwhile, global financial heavyweights are urging Indian savers to part with their gold. This week’s headlines reveal who still trusts real money, and who doesn’t…

Gold’s rebound has revived $6,000 forecasts, but silver remains oddly stuck. Meanwhile, global financial heavyweights are urging Indian savers to part with their gold. This week’s headlines reveal who still trusts real money, and who doesn’t…