February

27

2013

27

2013

|

February 27 2013 |

How Japanese Hyperinflation Could Turn The Dollar Into Toilet Paper

If you boil water without releasing any steam everything looks perfectly calm... until the entire pot explodes. That's the huge risk with Japan's gargantuan debt load right now. Frequently billed as a highly stable country, Japan's dark secret is that it should have exploded into a hyper-inflationary death spiral years ago. Worse yet, it could easily take the U.S. financial system and U.S. dollar down with it. That's because the U.S. depends on Japan to fund its own debt binge. We're not alone here. These concerns have been heavily informed by the research of Societe Generale. Japanese hyperinflation would be disastrous exactly because it goes against what most investors have been taught to expect. . .

Nobody expects Japanese hyperinflation...

Investors are completely unprepared for Japanese hyperinflation. That's because hyperinflation seems inconceivable for a nation that has been battling deflation ever since the bust of its stock and property bubbles two decades ago. Such complacency is made clear by the fact that investors are happy to buy ten year Japanese government bonds with just a 1.32% yield. They'd be completely blind-sided if Japanese hyperinflation became a reality.

Even though it could turn Japanese yen into toilet paper...

Hyperinflation rapidly makes any currency worthless. This would be particularly shocking in the case of Japan since many central banks hold yen as a portion of their reserves. They'd be hit hard by their past decision to diversify away from the U.S. dollar.

It would slam global markets...

If what was previously seen as a 'safe haven' currency suddenly lost substantial value, markets would be shaken as many investors suddenly realized they're carrying far more risk in their yen-related investments than they expected. Keep in mind that Japan's bond market is the second largest in the world.

And could even trigger an American debt crisis.

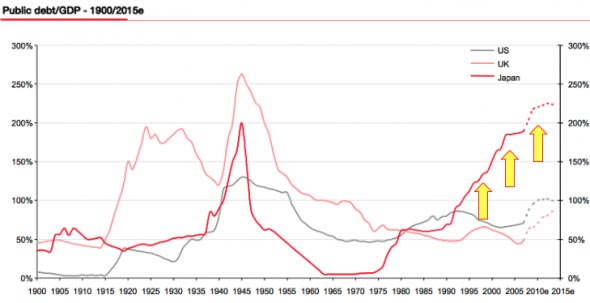

The problem is, Japanese debt has exploded into completely uncharted territory

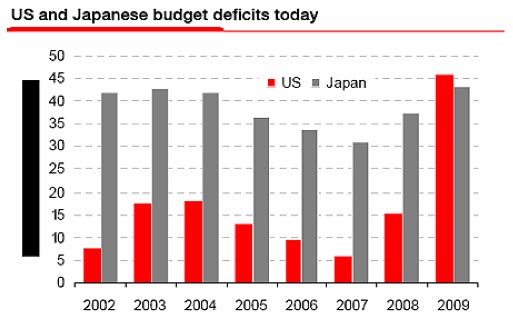

Spending has been out of control for years, well beyond the Japanese government's income

This chart shows government deficits as a percentage of expenditures. If it reads 50% on the left hand axis, then it means the government was spending twice as much as it earns during the year. Note how the U.S. surpassed Japan's level of profligacy in 2009.

Money has been blown on all kinds of make-work, uneconomic, 'stimulus' projects

One example of Japanese government largess is airport construction. The Kansai airport show to the left sits on an artificial island and is one of the most expensive civil works projects in history at $20 billion. "The country’s addiction has created a public debt mountain worth nearly 190 per cent of GDP and a wasteful network of roads to nowhere, suspension bridges over mountain streams and dozens of “zombie airports" - (Times Online)

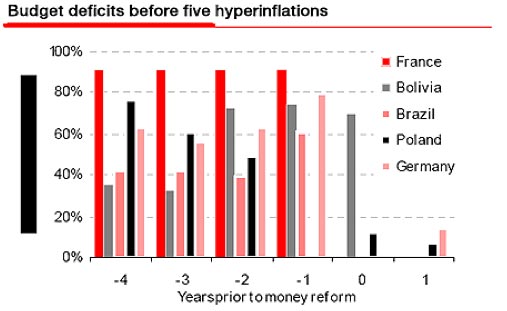

By historical standards, Japan should already be experiencing hyperinflation

Japan’s deficits are already just as bad as many countries who in the past experienced hyperinflation, as highlighted by Ambrose Evans-Pritchard from The Telegraph.

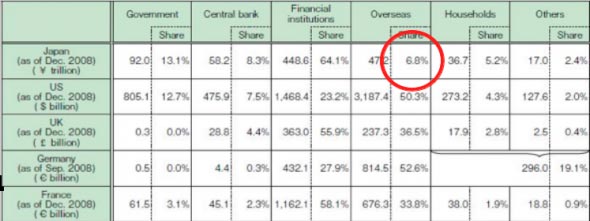

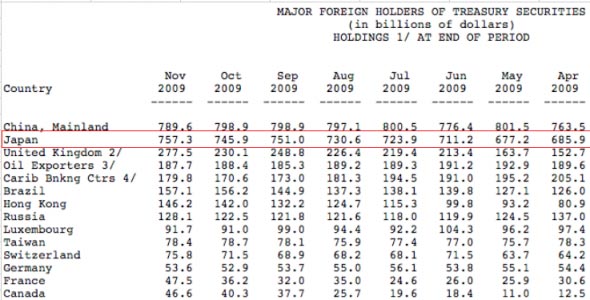

Mr. Bernholz noted that prices begin to skyrocket once government deficits as a share of government expenditure rise above a 33% and then stay there for multiple years. Japan's already there. Hyperinflation has followed such instances, historically. But it hasn't happened yet. Some people say it's because Japan is 'different'. Beset by deflationary forces ever since the bust of its property and stock market bubble two decades ago, Japan has been able to get away with ultra-low interest rates for years, despite its two-decade debt binge. They say that Japanese government debt is mostly held by locals. Only 6.8% is held by foreigners, so it's okay.

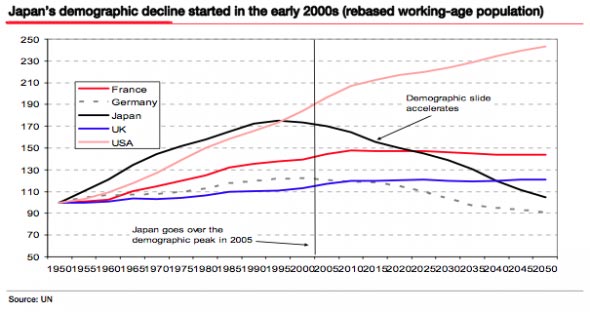

But here's the crisis trigger -- Japan's population decline means less people to buy debt

"Japan's ability to avoid a funding crunch to date despite its rising indebtedness does not prove that it will not at some point see a funding crunch. It does prove that this can be delayed. How has Japan been able to achieve this delay? Primarily because it has enjoyed a captive market - not only were domestic savings abundant, but risk-averse Japanese investors were happy to purchase government bonds.

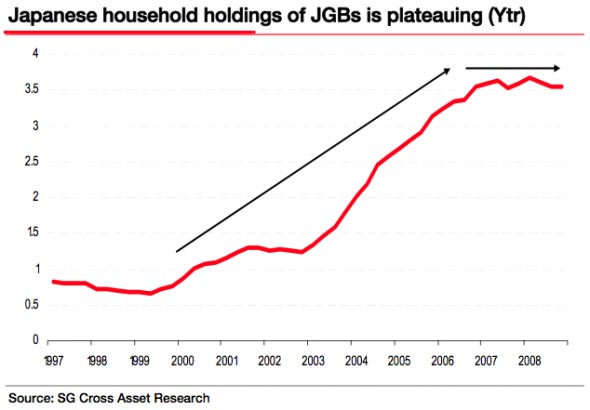

See? Already Japanese households' debt holdings have stopped growing

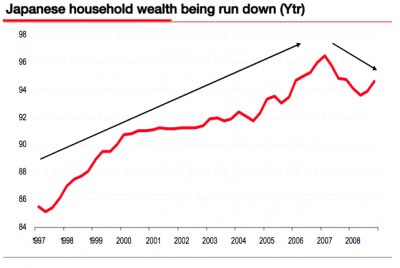

Japanese household wealth is even declining as retirees work down their savings

Also, there are fewer and fewer working age Japanese paying taxes. Thus more debt is needed to fund things.

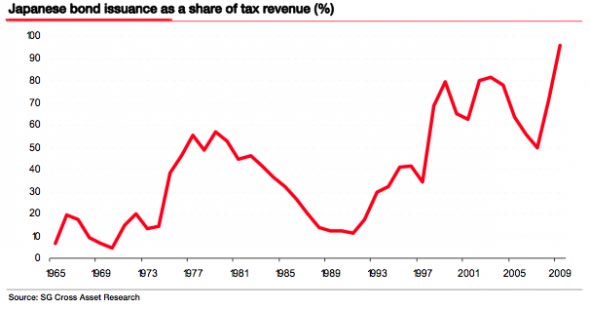

Japanese bond issuance could exceed tax revenue in 2010. That would mean that the majority of their spending would be financed by debt, not actual tax income, for the first time ever. A declining population thus means that more debt is needed for funding, but fewer Japanese are able to buy it. That's the feedback loop that could trigger an explosion of hyperinflation. Foreigners would demand higher interest rates to fund Japan -- rates Japan can't afford.

The yen would rapidly depreciate as it became clear Japan was at risk of debt default. In a debt crisis, Japan would likely be forced to either devalue the yen in order to wipe away debt values or default on all of its own people. Either way, traders would likely flee the yen and the currency would be crushed.

Now the American crisis -- America would be in trouble since it would probably lose its second largest debt buyer.

U.S. bonds yields would rise and the dollar would be under pressure

Japan would likely be selling foreign assets in order to shore up its finances. These assets would include its enormous holdings of U.S. bonds. Less demand for bonds would require higher interest rates to clear the market, all else equal. Higher interest costs could prove impossible for the U.S. to manage.

This would be similar to the problem Japan faces in this hyperinflation scenario. Rates are forced to rise, which makes debt less manageable and puts the government under pressure. Then markets push interest rates even higher since the government looks like it's having trouble handling its debt, making the debt problem even worse. The dollar keeps tanking. Thus Japanese hyperinflation could turn dollars into toilet paper as well.

Finally, should markets believe that the U.S. can no longer fund its own liabilities, the dollar's value would be hammered and America could enter its own hyperinflationary spiral as faith in the dollar and U.S. solvency collapses.

|

|---|

Send this article to a friend:

|

|

|

Mr. Pritchard explains that, if history is any guide, then Japan has already crossed into the hyperinflation “red flag zone" described by the influential economic historian Peter Bernholz.

Mr. Pritchard explains that, if history is any guide, then Japan has already crossed into the hyperinflation “red flag zone" described by the influential economic historian Peter Bernholz.