January

10

2013

10

2013

|

January 10 2013 |

Economic Collapse:

It’s going to get better; but, first, it’s going to get worse -Time of the Vulture, 3rd ed. 2012 When I presented Time of The Vulture: How to Survive the Crisis and Prosper in the Process to the Positive Deviant Network in March 2007, the economic collapse hadn’t yet happened. The next year, it did. At the time, I suggested those in attendance shed debt, sell their homes and buy gold. Then, the US real estate market was functioning without direct government aid, gold was $650 per ounce and the financial system was stable. Those days are gone and are never coming back. The imbalance between credit and debt that occurred during the Great Depression is now back; but, today, the à la 1930s massive deflationary collapse will be accompanied by monetary disorder on a cataclysmic scale. In August 2008, I wrote about the monetary component of the coming collapse in my article, The Four Tires of the Apocalypse:

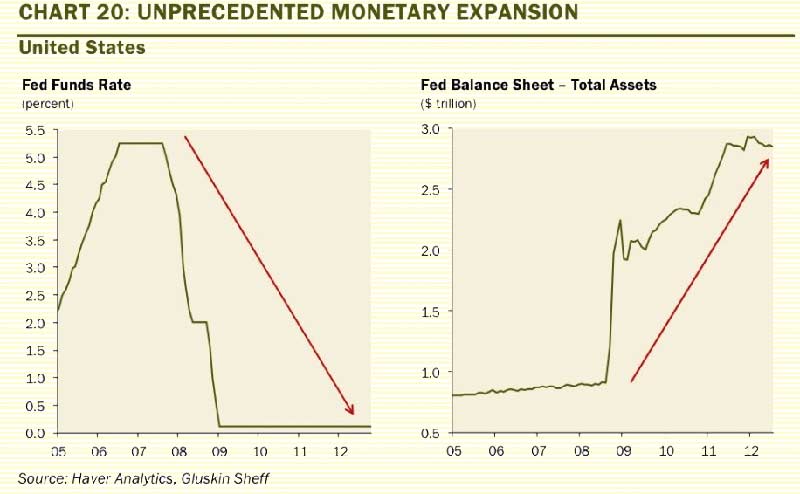

Today in 2013, the focus of the mechanics, i.e. central bankers, is still on the engine which despite trillions of dollars of credit is still in danger of completely seizing-up; and, although the bankers’ solution of even more credit (e.g. QE1, QE2, QE3, etc.) has failed to restore the automobile’s momentum, the failure to do so hasn’t stopped the mechanics’ attempts to add yet more credit to the already flooded engine.

Central banks have the money - after all, they print the coupons that pass as such - to hire academia’s best and brightest; but even their well-paid hirelings cannot solve what cannot be solved. When a paradigm shift occurs, what once worked no longer does. There are no solutions. End of paradigm. End of story. A PARADIGM SHIFT IS IN PROGRESS The inability to revive the bankers’ credit and debt-based economy is a sign that a paradigm shift is underway. Economists today believe the global economy is experiencing a series of exogenous shocks, e.g. the collapse of the US real estate bubble, the collapse of financial markets and investment banks in 2008 and the sovereign debt crisis in 2010, etc.; but such shocks appear to be exogenous only because economists are viewing the shocks from within the current paradigm. The increasingly serious shocks are not exogenous. They are the result of increasing internal systemic instability, an indication that a fundamental paradigm shift is occurring; and, when paradigms shifts occur, the question is not how the paradigm can be saved - the question is when and how it will end. Today, central bankers are unable to control markets just as economists are unable to explain them. This is characteristic of what Thomas Kuhn called a paradigm change. In The Structure of Scientific Revolutions, Kuhn’s uniquely insightful academic monograph published in 1962, Kuhn introduced the concept of paradigm change into the general lexicon.

SYSTEMIC INSTABILITY & PARADIGM CHANGE The present financial crisis is caused by a systemic failure of credit and debt-based economies. The maturation of the modern credit economy has led to such levels of debt that additional credit can no longer induce sufficient growth to service and/or retire previous debt. This is in keeping with Hyman Minsky’s financial instability hypothesis; and, because the modern banking system itself is the cause of the current instability with apparently exogenous forces merely exacerbating systemic weaknesses, efforts by central bankers to respond to these forces will inevitably prove inadequate. The balance between credit and debt, when disrupted in modern economies, fails to produce adequate growth; and efforts of central bankers in post-peak modern economies to induce the necessary growth results only in sequential asset bubbles and the continuing debasement of currencies. Credit-based capitalist economies need to constantly expand in order to deal with constantly expanding levels of compounding debt; and when central bankers are no longer able to induce sufficient expansion, economies collapse as debt levels become unsustainable. That this is now occurring comes as a surprise to modern economists who correlated the previous extraordinary success of credit-based economies with infinite longevity. Economic historian David Hackett Fischer provides evidence to the contrary, that no era lasts forever; that all periods of social, cultural and economic equilibrium end in waves of rising prices resulting in economic collapse. The present era is no exception; and that we have forgotten history does not mean we are immune to its reach. Professor David Hackett Fischer, author of The Great Wave: Price Revolutions and the Rhythm of History, observed that recurring price-revolutions, i.e. waves of rising prices, appear throughout history resulting in the collapse of existing eras, e.g. the Middle Ages, the Renaissance, the Enlightenment, etc. According to Professor Fischer, the current price-revolution will end The Era of Victorian Equilibrium, i.e. the era of modern banking/capitalism; for modern banking/capitalism was responsible for England’s extraordinary power and wealth during that period. Capitalism, an inherently unstable system of vast potential, has played a major role in world events for over two centuries. Today, however, capitalism is in disarray; for we are approaching the culmination of another great wave of rising prices which will bring capitalism’s two-centuries-in-the-sun to a devastating close. The present wave shares characteristics with all price-revolutions. The primary characteristic is rising prices and the present wave will be no exception. In each of the four previous price-revolutions since the 12th century, Professor Fischer noted:

The banker’s credit and debt-based paradigm is ending and despite what central bankers and governments desperately wish, in 2013 or soon thereafter, their economic engine will either seize up or the bankers’ excessive monetary easing will cause one or more of the tires to explode. You can bank on it. PROFESSOR ANTAL E. FEKETE AND THE NEW AUSTRIAN SCHOOL OF ECONOMICS The growing interest in the school of Austrian economics is a function of the times. The present economic paradigm built on paper banknotes, credit and debt is in disarray; and, as the bankers’ credit and debt-based paradigm is increasingly unable to solve the problems it caused, the search for alternative explanations and answers is gathering momentum:

My first exposure to Austrian economics was in 1973 when I read the obituary of Ludwig von Mises in the Wall Street Journal. Von Mises’ belief that through freedom of choice, i.e. the exercise of free will, humanity would reach its full potential resonated strongly with my own core beliefs. A much deeper understanding of Austrian economics occurred as a result of my friendship with Professor Antal E. Fekete, a strong proponent of the Austrian School of Economics. In keeping with that friendship I would like to share an announcement from Professor Fekete:

The contributions of Professor Fekete to the understanding of today’s economic crisis are many and worthy of thought and discussion; and Professor Fekete’s choice of Professor Juan Ramon Rallo to succeed him at the New Austrian School of Economics is an excellent one. Appropriately enough, an article by Professor Rallo, posted by the Ludwig von Mises Institute in January 2009, is entitled Economic Crisis and Paradigm Shift. More commentary and thoughts by Professor Rallo can be viewed on his Facebook (English translation page). THE PARADIGM SHIFT AND GOLD It is not possible to discern a new paradigm before it emerges. When the Middle Ages were still collapsing, the possibility that the Renaissance would succeed it was impossible to then see. So it is today. The transition between the old paradigm and the succeeding paradigm will not be easy. They never are. Professor David Hackett Fischer’s Great Wave has yet to completely crest and break although it now appears to be gathering the terrible and requisite strength to do so. Of such price-revolutions, Professor Fischer writes:

I will not sum up Professor Fischer’s thoughts for they are not hard and fast answers but rather suggestions for navigating the perilous and consequential times ahead. Just as the current paradigm cannot solve the current crisis, neither will reflexive ideological responses by the left and right formed by the present paradigm , e.g. state intervention vs the ‘free market’, work either. Such responses may provide ideological comfort in such times but history shows they have little relevance in transiting what now confronts us. I suggest reading Professor Fischer’s book, The Great Wave, for a deeper understanding what is now about to happen. If you believe you already possess the requisite understanding, you are most likely wrong. When paradigms change, the rules change too. What is known is that gold and silver will provide safety when paper currencies will become worthless; but in a paradigm shift of this magnitude, gold and silver alone will not insure a successful transit. When houses are built on sand Gold and silver will help My current youtube video is titled: Time of the Vulture 2013 wherein I discuss the significance and futility of QE3. The Fed’s decision to provide monetary easing ad infinitum will eventually end in the destruction of paper money itself. When I wrote Time of The Vulture: How to Survive the Crisis and Prosper in the Process, most did not believe an economic crisis of historic magnitude was about to occur. Today, most don’t believe a far better world will emerge out of the coming economic collapse. It will. A better world is coming. You can bank on it. Buy gold, buy silver, have faith.

In the 1990s, I became curious about the Great Depression and in the course of my study, I realized that most of my preconceptions about money and the economy were just that - preconceptions. I, like most others, did not really understand the nature of money and the economy. Now, I have some insights and answers about these critical matters. In October 2005, Marshall Thurber, a close friend from law school convened The Positive Deviant Network (the PDN), a group of individuals whom Marshall believed to be "out-of-the-box" thinkers and I was asked to join. The PDN became a major catalyst in my writings on economic issues. When I discovered others in the PDN shared my concerns about the US economy, I began writing down my thoughts. In March 2007 I presented my findings to the Positive Deviant Network in the form of an in-depth 148-page analysis, "How to Survive the Crisis and Prosper In The Process." The reception to my presentation, though controversial, generated a significant amount of interest; and in May 2007, "How To Survive The Crisis And Prosper In The Process" was made available at www.survivethecrisis.com and I began writing articles on economic issues. The interest in the book and my writings has been gratifying. During its first two months, www.survivethecrisis.com was accessed by over 10,000 viewers from 93 countries. Clearly, we had struck a chord and www.drschoon.com, has been created to address this interest.

|

|

|

|

In college, I majored in political science with a focus on East Asia (B.A. University of California at Davis, 1966). My in-depth study of economics did not occur until much later.

In college, I majored in political science with a focus on East Asia (B.A. University of California at Davis, 1966). My in-depth study of economics did not occur until much later.