Send this article to a friend:

November

18

2023

|

Send this article to a friend: November |

|

Washington’s Fiscal Doomsday Machine

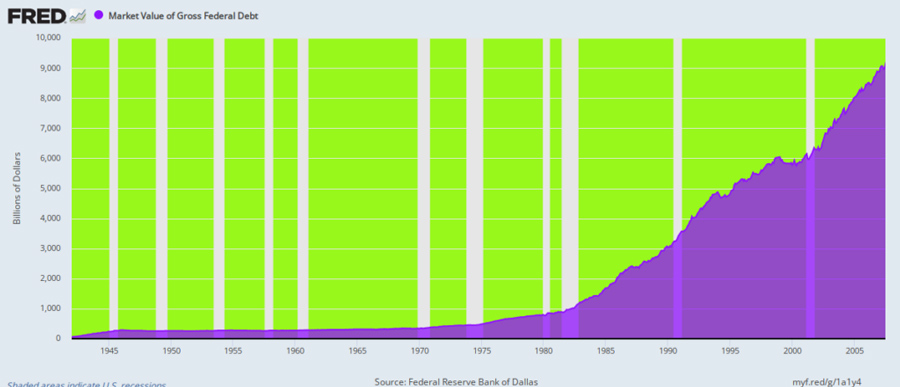

That’s right. During the last 1,461 days (FY 2020 thru FY 2023), Uncle Sam has generated $6.2 billion of red ink each and every day including weekends, holidays and snow-days. For anyone keeping score at home, that’s $4.2 million of red ink per minute. For the purpose of perspective, here’s how long it took to generate the first $9 trillion of US government debt: It took all of 43 presidents and 219 years to reach $9 trillion of public debt in July 2007. So the national debt clock has now accelerated to hyper-drive. Market Value of Public Debt Outstanding, 1940 to July 2007

And, yes, we do mean accelerate. It turns out that when you remove the budgetary Mickey Mouse from the numbers, the federal deficit for FY 2023 clocked in at over $2.0 trillion, or double the comparable level in FY 2022. The reported numbers, of course, do not look quite as alarming, posting at $1.4 trillion last year and $1.7 trillion this year. But as The Wall Street Journal cogently explained recently, that comparison is very misleading because it includes a $380 billion budgetary shuffle between the two years. It seems that Sleepy Joe’s student debt cancellation got recorded as a cost in September 2022, but then got canceled by the courts in FY 2023, turning it into a giant “savings”! When the Biden administration announced its plan to forgive federal student debt held by 40 million Americans in September 2022, it logged the long-term cost of the program, $379 billion, on the budget all at once, even though effectively no money was spent on it that year… But in June 2023, the Supreme Court tossed the debt-cancellation program, meaning most of that money wouldn’t actually be spent. Rather than update last year’s deficit numbers, though, the Treasury recorded the changes as a $333 billion spending cut in August 2023. We do not use the Mickey Mouse epithet lightly, but surely booking the next 50 years of student loan repayments during the single month of August 2023 amounts to exactly that. Still, the “Joe Biden” thing behind the teleprompter has the audacity to keep making the hideous claim that he has been slashing the federal deficit! Actually, Biden is surrounded by the usual Keynesian suspects when it comes to fiscal policy, but even they did not historically recommend a dramatic increase in the deficit at a time of so-called full employment, when the official unemployment rate is just 3.8% and the economy is still straining under severe labor shortages. Indeed, the $2.0 trillion cash deficit for FY 2023 amounted to 7.5% of GDP — a level that was supposed to happen only at the very dark bottom of an unusually bad recession. Needless to say, these dismal fiscal figures are just one more indictment of the baleful rule of Washington’s Uniparty. When they get done funding the nation’s $1.3 trillion Warfare State, ring-fencing $4.2 trillion per year of Social Security, Medicare and other sacrosanct entitlements, filling up the pork barrels of domestic discretionary spending to the brim, warding off any and all ideas about raising revenues and facing the music on the exploding cost of net interest on the public debt, you get a four-year $9 trillion warm-up for an even greater tsunami of red ink in the years just ahead. Indeed, that’s now baked into the cake. The world is on the verge of breaking out into a hot war in the Middle East, and Ukraine is hanging by a thread, both owing to the neocon perfidy of the last several decades. So the $1.3 trillion comprehensive national security budget (Department of Defense, International security assistance and operations and Veterans) is going nowhere except up. Way up. Likewise, Donald Trump has a virtual lock on the Republican nomination even if he ends up behind bars before November 2024. So, his new GOP 11th commandment will prevail. Namely, do not touch Social Security or Medicare, even though they will cost $34 trillion over the next decade, their trust funds will be insolvent by the early 2030s and trillions of those benefits represent pure transfer payments, not a return on payroll taxes contributed by beneficiaries over their working lifetimes. As to the “pork” in the small (less than 15%) part of the budget called “non-defense discretionary spending,” the Washington GOP has already signed its confession papers. Between FY 2017 (Obama’s last budget) and FY 2021 (Trump’s final budget), this fiscal component soared from $610 billion to $895 billion. That’s a 47% gain at a time when the GOP controlled the veto-pen in the White House and one or both houses of Congress. And then you get to the real skunk in the woodpile — namely, the soaring cost of debt service owing to the long-delayed but not nearly finished normalization of interest rates. If there were ever any doubt that Washington was wandering about in financial la-la land thanks to the Fed’s drastic suppression of interest rates, the data for the weighted average cost of debt service should resolve the matter. As it happened, on the eve of FY 2020 and the aforementioned $9 trillion public debt explosion that followed, the federal debt held by the public had already more than tripled, from $5 trillion in late 2007 to nearly $17 trillion at the end of FY 2019. Owing to the Fed’s heavy foot on interest rates, however, the weighted average interest rate on the federal debt was just 2.5% on September 30, 2019. Then came the $9 trillion borrowing explosion, but mirabile dictu (wonderful to relate), the cost of servicing the federal debt just kept on sinking. By early March 2022, when the Fed finally pivoted to inflation fighting, the weighted average interest rate reached just 1.56%! That’s right. Washington was in the midst of the greatest spending and borrowing frenzy in recorded history, but thanks to the Fed, the average yield on the public debt had declined by 40%. Reality has interposed itself painfully ever since. By the end of August 2023, the weighted carry cost was up to 2.92%. Accordingly, the annualized run rate of federal interest expense soared from $578 billion in Q3 2019 to $910 billion in Q2 2023. That’s a 57% gain, but it is barely a warm-up for what’s coming down the pike. Virtually every maturity of Treasury paper from 30-day bills to 30-year bonds is currently trading at +/- 5.0%, meaning that when current outstandings roll over, debt service will rise by a further $500 billion per year, even before new trillions are added to the total of Uncle Sam’s debt load. And besides that, 5% is surely not the ultimate limit on Treasury yields. Given runaway public borrowing and the nation’s historically low savings rate, the average yield on the public debt is likely heading even higher. And there won’t be any rescue from the Fed this time, either, because inflation isn’t collapsing, meaning that a new cycle of “easy money” has only faded further down the horizon. In this context, the core economic policy platform of the Washington GOP is a tale straight from fantasyland. That is to say, even as they want even more for the Warfare State and are loudly taking a powder on the Welfare State, they still feel compelled to demand that the Trump tax cuts be permanently extended when they expire in 2025. That would cost a cool $3.5 trillion in foregone revenue over the next decade, and that’s on top of the $25 trillion of new debt built in under current policy for the 10-year budget window ahead. In short, the Uniparty has seconded the nation’s finances to a fiscal doomsday machine that is literally unstoppable.

Former Congressman David A. Stockman was Reagan's OMB director, which he wrote about in his best-selling book, The Triumph of Politics. His latest books are The Great Deformation: The Corruption of Capitalism in America and Peak Trump: The Undrainable Swamp And The Fantasy Of MAGA. He's the editor and publisher of the new David Stockman's Contra Corner. He was an original partner in the Blackstone Group, and reads LRC the first thing every morning.

www.davidstockmanscontracorner.com

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)