Send this article to a friend:

November

18

2021

|

Send this article to a friend: November |

|

3 Reasons Why Being Reluctant to Retire Could Be the Right Call

In just the last few years the repo markets went crazy, we lived through a pandemic-induced market crash, and now we’re experiencing out-of-control inflation. Strange times like these can create doubt. When it comes to choosing the right time to retire, that doubt can become reluctance. But being reluctant to retire right now could actually be the right call, and here are three reasons why… First: The personal reasons Even if you’re financially prepared to retire, there are personal reasons why you might not want to. Aside from the obvious uncertainty in the markets right now, according to a MyJournalCourier:

These are certainly valid concerns for retirement savers who are planning their exit from the workforce. Especially once you consider that consumer purchasing power keeps draining like water from a bucket full of holes. The list of personal reasons to hesitate includes:

As Cathy Gearig, a certified financial planner, explains, “A lot of the people I see are financially ready before they’re emotionally ready.” Personal reasons are just that. Each of our individual situations is different, so no one can fault you for feeling retirement reluctance over such concerns. There are, however, bigger-picture forces at play here. The decision to retire gets even more interesting as we move away from personal, individual concerns and into concerns about the market itself… Second: Classic retirement rules of thumb are broken In the mainstream media, the “experts” like to offer up “rules” for retirement. For decades, financial planners and investment experts spoke of the “4% rule.” Basically, retirees should expect to withdraw 4% of their total assets in the first year of retirement. This amount, along with pensions or Social Security or other benefits, would pay the bills. Next year, Withdraw the same amount adjusted for inflation, and so on. Here’s an example from CNBC:

But like most rules, thanks to the strange times we live in, that now needs to be reduced by 17.5 percent:

The experts recommending this “rule-change” blame a variety of factors: Negative after-inflation long-term bond yields, the likelihood of below-historical-average stock market returns, and out-of-control inflation as the culprits. In fact, Schwab published a highly critical takedown of the 4% rule. Here are the highlights:

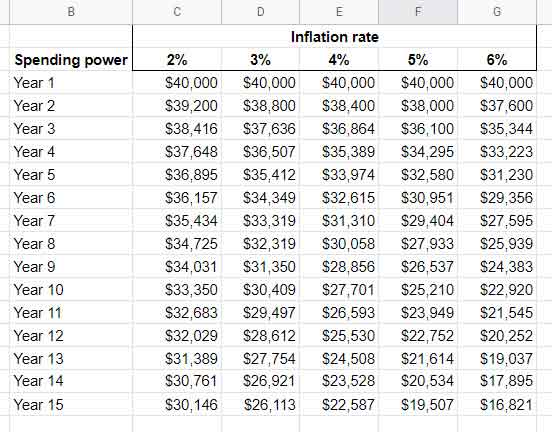

Even at this reduced withdrawal rate, experts still predict a reduction in purchasing power, especially later in retirement, “when accounting for inflation.” Which is a huge mistake many people make! It’s hard to grasp just how inflation can drain away the purchasing power of your money without changing the balance in your bank account. Here’s an example, assuming a retiree withdraws $40,000 in the first year of retirement. This chart shows the spending power of that same $40,000 in later years at different levels of inflation:

Note that even at the Fed’s targeted rate of 2%, even modest inflation has wiped out 25% of your purchasing power in 15 years. At over 2% inflation, the numbers get truly grim. (I didn’t continue this projection beyond 15 years because it’s simply too depressing.) Which brings us to the third and most important reason that reluctance to retire could be the right call… Third: Inflation and your “magic number” Kiplinger’s Kelly LaVigne summarized why any saver might consider putting off retirement for a bit:

No surprise there… Those who believe inflation will “negatively impact their purchasing power over the coming months” don’t seem to realize that’s already happened. And it will keep happening, month after month, year after year. Aside from the well-known but rarely-appreciated fact that inflation robs savers of their wealth, there’s another reason inflation factors into the decision to retire… Inflation changes your “magic number.” For example, let’s say you saved $1 million for retirement because you thought that was your magic number. Thanks to inflation, that amount of savings isn’t going to stretch as far as you might think. Take another look at the chart above: How inflation rips away the value of your 4% annual withdrawal from your $1 million in savings. We’ve heard financial planners joke, “Three million is the new one million.” It would be funny if it wasn’t true. The bottom line is, thanks to inflation and the volatility in the markets, your “magic number” is a moving goal post that is very hard to pin down. Who in their right minds would want to start living on a fixed income when so much, like inflation, market volatility and market valuation are so unfixed and uncertain?. We’re not saying you should give up and resign yourself to dying at your desk. No, what we’re saying instead is, if you want certainty, you’ll have to create it for yourself… Ensuring you’re ready to retire when the time is right Whenever you choose to leave the workforce to start enjoying your “golden years,” make sure your savings are prepared for the journey. Honest examination with an eye toward risk profile and diversification are key steps you can take right now so you can retire with confidence. Knowing what you own, and the level of risk it carries, seems smart. When it comes to certainty, there’s one huge advantage you can give yourself. Precious metals like physical gold and silver have had inherent value for thousands of years because they are valuable, tangible and finite resources. They aren’t controlled by any central bank or any government. You can’t inflate a gold bar. You can’t default on a silver eagle. Furthermore, gold is an internationally-recognized store of value. It can help to provide stability during an uncertain market, like the one the U.S. is in right now. Physical gold and silver also have a unique advantage of being a hedge against inflation. That gives you a better chance of side-stepping the dilemma of planning for tomorrow’s retirement while thinking in today’s dollars.

|

Send this article to a friend:

|

|

|

It’s a strange time to be saving, investing, and planning for retirement.

It’s a strange time to be saving, investing, and planning for retirement.

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)