Send this article to a friend:

September

25

2023

|

Send this article to a friend: September |

|

Robots From China Don't Strike

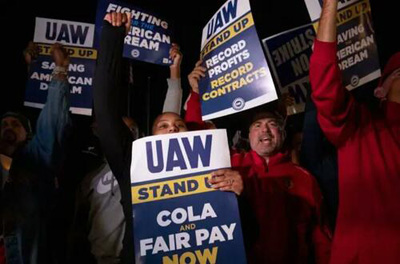

The UAW's demands would roughly double labor costs and, according to management, make the companies unviable. Where will the workers go when the automakers go bankrupt, further mechanize their assembly lines, or move yet more production to China? Many workers in these companies who aren't on strike are already getting fired. Striking unions attempt to inflict maximum pain on their own companies with as little effort and expenditure as possible. The companies are forced to let go of misguided workers, who they can’t keep busy because other misguided workers on whom they depend are striking. All the strikers and fired UAW workers are getting paid from union funds that came from dues imposed on workers, whether they like it or not. They're getting paid by the union to halt production. This ludicrous practice introduces massive inefficiencies into U.S. manufacturing, yet Americans over the decades have gotten used to the deadweight it attaches to the economy. The supply chain chaos of the latest strike is purposefully engineered by the UAW, which keeps management guessing which factory will close next. Downstream and upstream workers, including from hundreds of other companies, depend on a reliable supply chain and are made redundant by the UAW’s actions as soon as the factory can't produce vehicles and supply them to paying customers. Shareholders in these companies have felt more pain than strikers in recent months, with shares of Stellantis falling by more than 7 percent and shares of Ford and GM falling by more than 20 percent. Compare that to rising inflation, which is less and hits the pocketbooks of both shareholders and workers. Yet union bosses want to grab even more value from shareholders in a manner that's ultimately a small win and big loss for not only the workers and companies, respectively, but also for the entire economy. What a tiny percentage of U.S. unionized auto workers hope to gain in increased wages, shareholders lose in multiples, and Americans as a whole lose in our market’s competitiveness. Investors prefer to invest in countries where they aren’t compelled to share profits when times are good. That’s why investors risk their capital. With no significant upside, investors will keep their money in lower-profit but more reliable investments such as bonds, a preference that, if widespread, would impoverish not only the auto industry but all of the American industry. It's an inefficient form of investing and removes the critical element to the economic growth of risk-takers as decision-makers with skin in the game. Shareholders aren't all billionaires. In fact, 158 million Americans own shares in companies—about three-quarters of all adults. As should be clear from those numbers, most shareholders are regular folks, and those regular folks are getting fleeced by the union (full disclosure: This author is a regular guy who holds GM shares). The problem isn't just with the unions. The problem is with our politicians, who can't stand up to the unions, or they get voted out of office. That's why both Republicans and Democrats avoid angering unions, and why they silently endure strikes that debilitate not only the affected companies but the entire economy.

A general view of GMC Hummer EVs is pictured at General Motors' Factory ZERO electric vehicle assembly plant in Detroit on Nov. 17, 2021. The more liberal a country is toward strikers, the more illiberal its economy. Strikers have the power to shut down free markets of labor and capital, which is where they get their power to raise wages beyond what the market bears. That power of shutting down markets, like the power of monopolies, is inherently illiberal. It impinges on the freedom of labor and capital to operate in a manner that maximizes economic efficiency and growth. True liberals should support free markets, including labor markets, as do true conservatives. Yet both liberal and conservative politicians in the United States avoid criticizing unions. That's a historical weakness in the American economy that too few are working to fix. It's the historical weakness that leads our corporations to deindustrialize the United States in favor of nonunionized China and mechanize assembly lines with robots that can increasingly be bought in China. American unions are self-defeating because they lack principles beyond their driving cause, which is more money for themselves in the short term, without regard for long-term consequences and negative externalities. As one honest 20-year-old striker told The Washington Post, “I’m just here for the money.” Fortunately, only about 10 percent of American workers are unionized, which is low for OECD countries. U.S. unionization rates have fallen almost every year since the 1950s, when it reached a peak of 35 percent. Unfortunately, the concentration of wealth appears to be negatively correlated with unionization. Higher rates of unionization cause a more equal distribution of wealth in the United States, but at the cost of lower growth. A more equitable distribution of wealth leads to positives from an American values perspective, such as homeownership, a more vibrant small business sector, broader ownership of stocks and bonds, and more political stability. But there are better ways to achieve this than through damaging strikes, for example, through a combination of right-to-work laws and progressive taxation. The United States already has such taxation, so there's no need for the supply chain dislocations that result from overly aggressive union leaders.

|

Send this article to a friend:

|

|

|

The United Auto Workers (UAW) went on strike on

The United Auto Workers (UAW) went on strike on

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)