August

1

2013

1

2013

|

August 1 2013 |

The Most Important Number In The Entire U.S. Economy

There is one vitally important number that everyone needs to be watching right now, and it doesn't have anything to do with unemployment, inflation or housing. If this number gets too high, it will collapse the entire U.S. financial system. The number that I am talking about is the yield on 10 year U.S. Treasuries. When that number goes up, long-term interest rates all across the financial system start increasing. When long-term interest rates rise, it becomes more expensive for the federal government to borrow money, it becomes more expensive for state and local governments to borrow money, existing bonds lose value and bond investors lose a lot of money, mortgage rates go up and monthly payments on new mortgages rise, and interest rates throughout the entire economy go up and this causes economic activity to slow down. On top of everything else, there are more than 440 trillion dollars worth of interest rate derivatives sitting out there, and rapidly rising interest rates could cause that gigantic time bomb to go off and implode our entire financial system. We are living in the midst of the greatest debt bubble in the history of the world, and the only way that the game can continue is for interest rates to stay super low. Unfortunately, the yield on 10 year U.S. Treasuries has started to rise, and many experts are projecting that it is going to continue to rise. On August 2nd of last year, the yield on 10 year U.S. Treasuries was just 1.48%, and our entire debt-based economy was basking in the glow of ultra-low interest rates. But now things are rapidly changing. On Wednesday, the yield on 10 year U.S. Treasuries hit 2.70% before falling back to 2.58% on "good news" from the Federal Reserve. Historically speaking, rates are still super low, but what is alarming is that it looks like we hit a "bottom" last year and that interest rates are only going to go up from here. In fact, according to CNBC many experts believe that we will soon be pushing up toward the 3 percent mark...

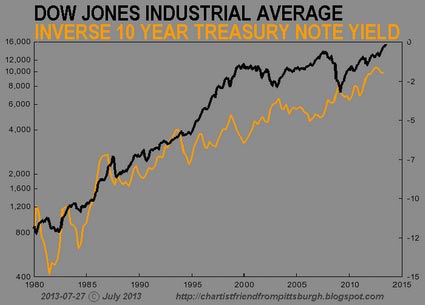

This rise in interest rates has been expected for a very long time - it is just that nobody knew exactly when it would happen. Now that it has begun, nobody is quite sure how high interest rates will eventually go. For some very interesting technical analysis, I encourage everyone to check out an article by Peter Brandt that you can find right here. And all of this is very bad news for stocks. The chart below was created by Chartist Friend from Pittsburgh, and it shows that stock prices have generally risen as the yield on 10 year U.S. Treasuries has steadily declined over the past 30 years...

When interest rates go down, that spurs economic activity, and that is good for stock prices. So when interest rates start going up rapidly, that is not a good thing for the stock market at all. The Federal Reserve has tried to keep long-term interest rates down by wildly printing money and buying bonds, and even the suggestion that the Fed may eventually "taper" quantitative easing caused the yield on 10 year U.S. Treasuries to absolutely soar a few weeks ago. So the Fed has backed off on the "taper" talk for now, but what happens if the yield on 10 year U.S. Treasuries continues to rise even with the wild money printing that the Fed has been doing? At that point, the Fed would begin to totally lose control over the situation. And if that happens, Bill Fleckenstein told King World News the other day that he believes that we could see the stock market suddenly plunge by 25 percent...

And as I have written about previously, we have seen a huge spike in margin debt in recent months, and this could make it even easier for a stock market collapse to happen. A recent note from Deutsche Bank explained precisely why margin debt is so dangerous...

But of much greater concern than a stock market crash is the 441 trillion dollar interest rate derivatives bubble that could implode if interest rates continue to rise rapidly. Deutsche Bank is the largest bank in Europe, and at this point they have 55.6 trillion euros of total exposure to derivatives. But the GDP of the entire nation of Germany is only about 2.7 trillion euros for a whole year. We are facing a similar situation in the United States. Our GDP for 2013 will be somewhere between 15 and 16 trillion dollars, but many of our big banks have exposure to derivatives that absolutely dwarfs our GDP. The following numbers come from one of my previous articles entitled "The Coming Derivatives Panic That Will Destroy Global Financial Markets"...

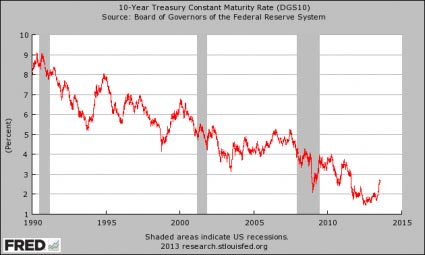

And remember, the biggest chunk of those derivatives contracts is made up of interest rate derivatives. Just imagine what would happen if a life insurance company wrote millions upon millions of life insurance contracts and then everyone suddenly died. What would happen to that life insurance company? It would go completely broke of course. Well, that is what our major banks are facing today. They have written trillions upon trillions of dollars worth of interest rate derivatives contracts, and they are betting that interest rates will not go up rapidly. But what if they do? And the truth is that interest rates have a whole lot of room to go up. The chart below shows how the yield on 10 year U.S. Treasuries has moved over the past couple of decades...

As you can see, the yield on 10 year U.S. Treasuries was hovering around the 6 percent mark back in the year 2000. Back in 1990, the yield on 10 year U.S. Treasuries hovered between 8 and 9 percent. If we return to "normal" levels, our financial system will implode. There is no way that our debt-addicted system would be able to handle it. So watch the yield on 10 year U.S. Treasuries very carefully. It is the most important number in the entire U.S. economy. If that number gets too high, the game is over.

|

|---|

Send this article to a friend:

|

|

|