Send this article to a friend:

July

29

2021

|

Send this article to a friend: July |

|

Not Your Mother's Inflation: Why This Is the Time to Invest in Precious Metals

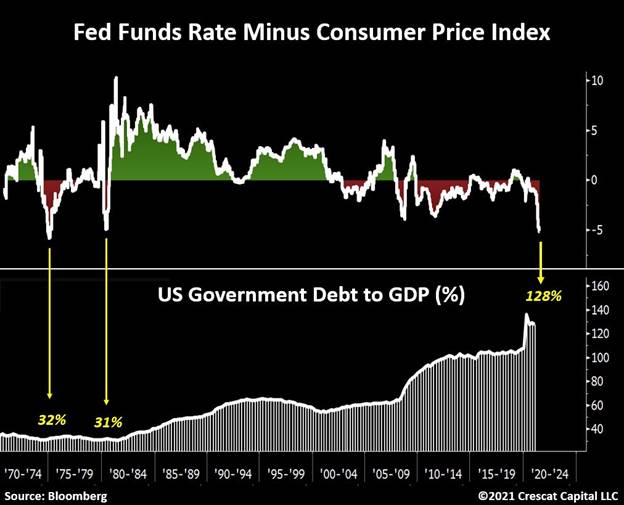

Investors are always looking to history for guidance by attempting to find the most economically comparable period to the present. Two timeframes are the most conspicuous, the 1940s and the 1970s. Some macro investors today are citing the 1940s to validate the Fed's hypothesis that the recent rise in consumer prices will prove to be transitory. Ironically, if the past is prologue, this period supports the idea of inflation getting much worse before it gets better today. The 1970s period, meanwhile, substantiates the risks of an even longer lasting and more gradually rising inflationary trend that could last more than a decade. In our analysis, today's macro imbalances and policy response point to even more extreme inflationary pressures than both analogs. In resemblance to today, the economy of the 1940s had high government debt and large fiscal deficits relative to GDP along with repressive Fed interest rate policies. It was a decade that included two sharp waves of increasing inflation in the Consumer Price Index, the first during World War II and the second right after it. Monthly CPI rose to a short-term peak of 13.2% on a year-over-year basis in 1942, and while it fell back down to 0% in 1944, it then spiked again to a higher peak of 19.7% in 1947, the highest year-over-year CPI increase of the last century. Note that during each of those inflationary spikes, CPI stayed above a 5% YoY rate every month for over two years. To our friends, "the deflationistas," if this is an accurate roadmap to follow, buckle up, the rise in consumer prices is just getting started. Unlike the 1940s, when the US dollar was still pegged to gold, in the 1970s we had the abandonment of the gold standard which marked the onset of five decades of limited financial and monetary discipline ever escalating to the historic macro imbalances we have today. Such a shift in the monetary system was just as significant as today's unlimited QE policies. The consequence of the macro setup during that era was that inflation rose in three waves from the late 1960s through the 1970s to reach a peak of 14.7% in 1980. Those waves were steadier and more persistent than the inflationary waves of the 1940s, we think due to the long-term, trending dynamic of the wage-price spiral that was at work. Interestingly, both of those regimes, along with today's, share one thing in common: negative real interest rates. The 1940s was the most financially repressive environment yet in that respect. The Fed at least allowed interest rates to rise in the 1970s while inflation rose faster. From a market perspective, there was one important lesson from both periods: At times when investable assets yield less than inflation, owning tangible assets becomes imperative. Commodities were far-and-away the best performing asset class in both of those decades. Yes, today's tax policies may not be sustainable. Throughout history, tax revenues relative to GDP have tended to follow government debt levels. Today is the first time we are seeing such a large divergence between the two. However, given the need for fundamental growth to justify today's historic valuations in risky assets, one would wonder how meaningfully the government could really reverse these tax policies.

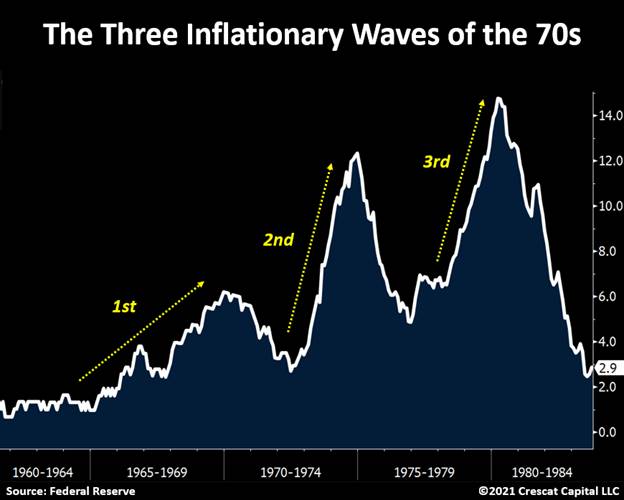

The Three Waves of Inflation While some people like to say that the inflation rate will accelerate in steady fashion, we believe this line of thinking is utterly wrong. Macro forces are cyclical. As inflation gradually becomes the prevailing narrative, households and businesses act accordingly creating a vicious cycle that can result in surprising surges in the cost of living that ebb and flow. Let's return to the 1970s case study.

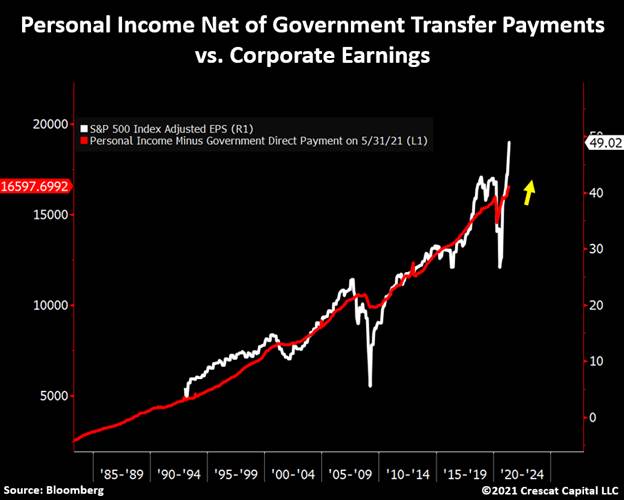

A Structural Shift Is Upon Us The chart below could not illustrate more meaningfully our current conviction in the inflationary thesis. Through monetary and fiscal policies, the historic amounts of liquidity recently added to the economy have translated into one of the hottest economic environments we have ever seen. Consequently, corporate profits surged by 47% on a year over year basis and are now significantly higher than any other prior peak. As illustrated below, personal income less government transfer payments tend to follow the bottom-line fundamentals of companies incredibly close. To us, it suggests that personal income is about to drastically increase in the next quarters. We think it is going to be driven by a large increase in labor cost. After experiencing a secular decline in wage and salary growth for the last 30 years, we believe there is a structural shift upon us that will critically feed into the inflationary thesis. Using our prior analytical work on the 1919 Spanish Flu period as a roadmap, when the cost of living becomes significantly more expensive, workers began to demand materially higher wages. To recall, in the wake of that pandemic, one out of five people in the US work force was engaged in a labor related strike. We believe a similar pattern is developing today. The economy is likely at the early stages of an upsurge in labor-management conflict. In fact, we have not seen an increase in the federal minimum wage since July 2009. When the first numbers on personal income were reported, economists warned that a significant amount of it was related to the stimulus checks and other fiscal programs. They were not wrong. To be exact, today government transfer payments represent over 20% of personal income and reached 33% at their peak in March 2021. As we have said before, US households just experienced their largest wealth increase in history, including the bottom 50%. This was already accompanied by a significant amount of inflation, even if CPI is understated due to government-sponsored fudging. But in our view, if rising personal income is further driven by a new secular rise in wage and salary growth, it would considerably add to the inflationary thesis through a demand-pull dynamic, one that ultimately feeds the classic wage-price spiral.

Dependent on Monetary Policy

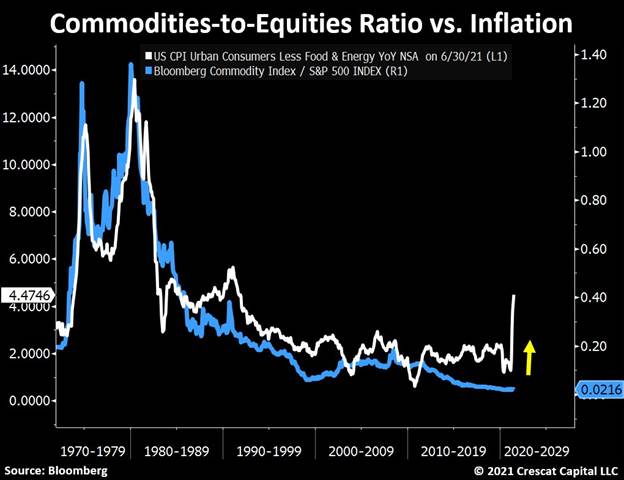

The Rise of the Tangible-to-Financial Assets Ratio Those are extreme scenarios that start to develop when an economy experiences severe capital outflows, particularly from large businesses and institutions, which leads to a sequence of events. First, the capital flight creates downward pressure on the local currency, increasing the likelihood of an inflationary problem. Also, as large corporations exit those countries, the labor market suffers, economic growth turns negative, and the instability of the currency is aggravated. The combination of an economic and currency crisis is what leads to social unrest, major political shifts guided by populist agenda, and a major move in opposition to capitalism. The good news is that these issues take time to evolve, sometimes decades. Aside from the obvious case being Venezuela, we think Argentina could unfortunately be going towards this path. On the other hand, we are clearly not seeing these signs in the US yet. Almost all major corporations in the world continue to be based here and do business with the US economy. Therefore, a hyperinflationary scenario is not in our minds as of now. We think that the inflation rate will continue to rise and be more persistent for longer, the exact opposite of the concept that the Fed is promoting today by characterizing inflation as "transitory". We think, like the 1970s, we will see progressively larger inflationary waves that will build on themselves and set off important changes in market leadership and asset allocation. In this macro backdrop, we believe natural resource industries and their underlying commodity prices will become one of the main beneficiaries. The scarcity of investable assets that yield above inflation expectations is slowly forcing capital allocators out of risky overvalued financial assets and into cheap hard assets. Note how the commodities-to-equities ratio, or what we may call the "tangible-to-financial assets ratio," tends to follow inflation incredibly close throughout history. Given our strong views about the likely longer-lasting inflationary consequences in the economy, we believe this is the time for investors to be long tangible assets and short hyper-overvalued stocks while also avoiding bonds. Keep in mind, commodities remain under-allocated by institutions while stocks now have negative real earnings yield just like bonds.

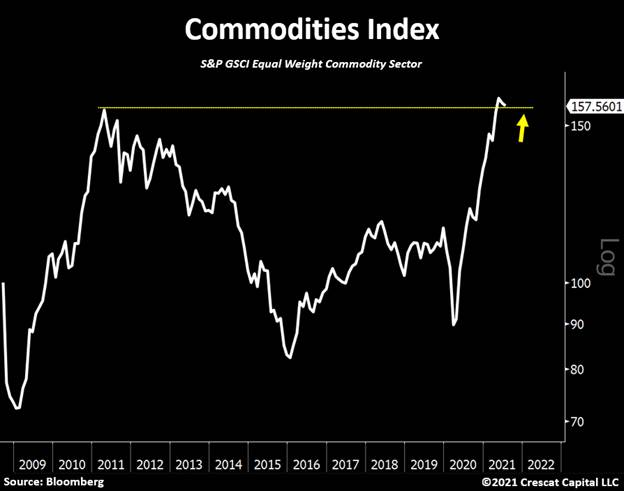

Lumber Prices Are Not Representative of Overall Commodity Markets The 61% decline in lumber prices is often used as a reason to justify how inflation is in fact transitory. In our opinion, this view is largely misguided. While the crash in lumber prices is significant, that is one case versus multiple other commodities. The equal-weighted commodities index just broke out above is 2010 highs and is merely retesting that key support level. We believe these assets are headed significantly higher from here.

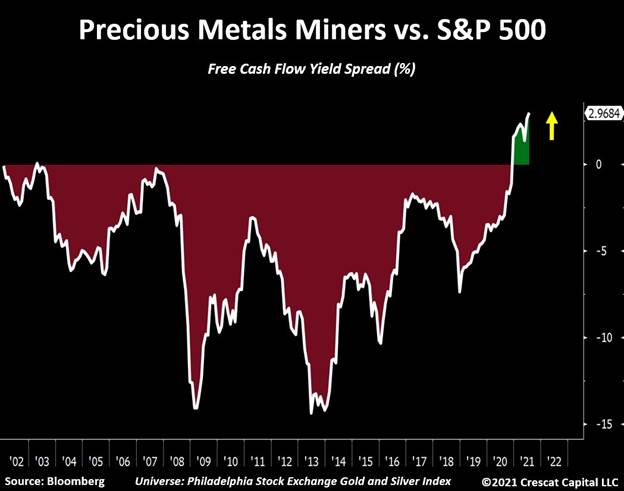

A Uniquely Bullish Setup for Miners In our view, it seems largely inconsistent for fiscal and monetary policies to be pedal to the metal at a time when economic activity is at one of its strongest levels in history. In a way, however, some of the current policies are unavoidable. With overall debt at historic levels and stocks and bonds at excessive valuations, stimulative policies must be targeted towards suppressing the cost of capital. We think this macro environment is what makes commodities, especially monetary metals, to be at a uniquely optimistic setup. Gold and silver miners have never looked this cheap relative to the S&P 500. Their free-cash-flow yield is almost twice the overall market. The value and growth proposition embedded in miners today is unmatched by any other time in history.

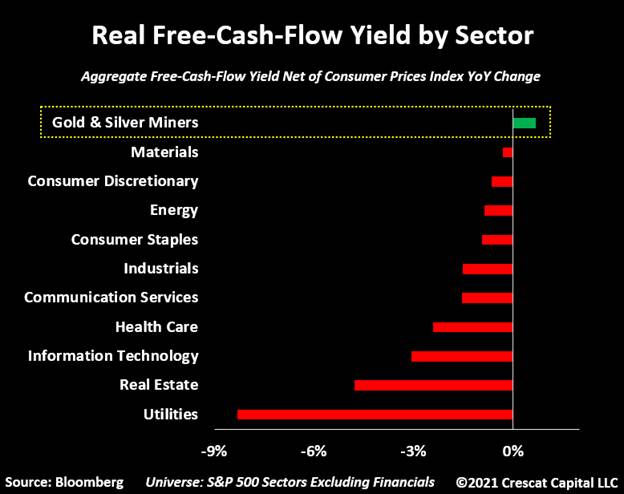

Robust Fundamentals for Miners To follow up on this idea, if gold and silver miners were considered a sector, it would be the only part of the economy today that generates higher free-cash-flow yield than inflation.

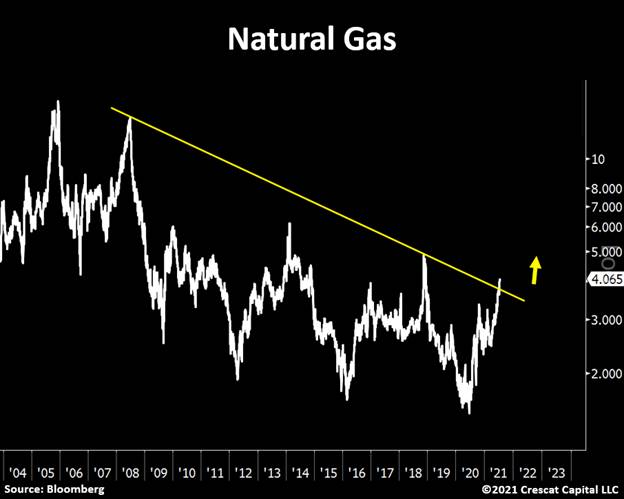

Crescat's Activist Precious Metals Strategy Crescat is working with world-renowned exploration geologist, Quinton Hennigh, PhD, its Geologic and Technical Advisor to identify a portfolio of companies with the most prospective gold and silver deposits on the planet that will feed the next generation of mines. We are leading the charge to fund exploration and discovery of the new, large, high grade deposits to fill the supply void left by the major mining companies after a decade of underinvestment in exploration and development. The majors have not been replacing their reserves and are facing a production cliff beginning in just four years. Permitting new mines takes years. The industry leaders will need to start allocating capital soon to the best projects out there in the hands of the junior mining segment if they want to continue their growth. We believe a new M&A cycle will be ramping up soon as the larger producers are now gushing free cash flow that must be deployed to capture growth in the burgeoning new secular bull market for precious metals. A Meaningful Breakout While we are all focusing on oil, natural gas is now at a critical juncture after breaking out from a multi-year resistance. A sustainable move higher from here would only add to our thesis that inflation is not transitory.

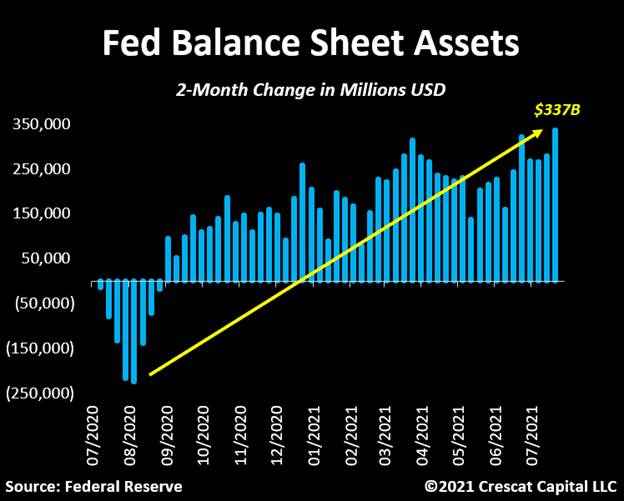

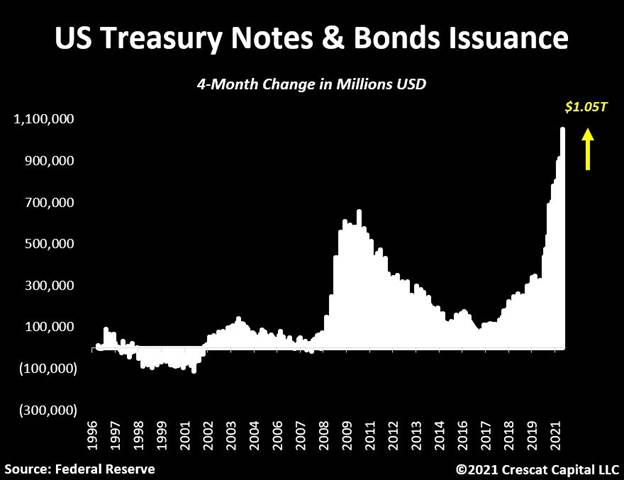

Largest Issuance of Treasury Notes and Bonds in History

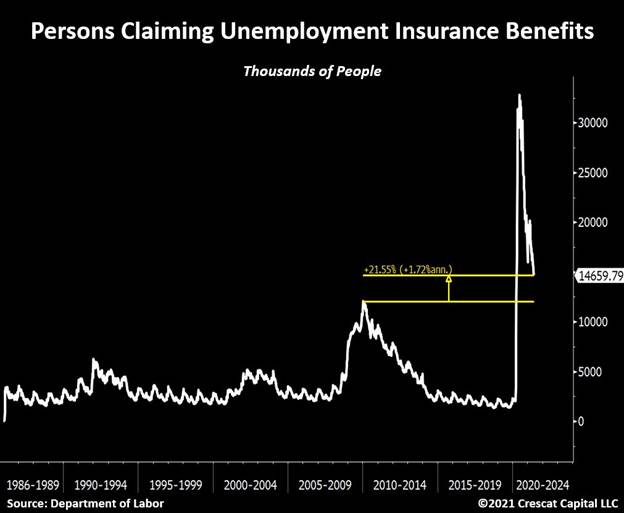

Shortage of Workers Set to Fuel Higher Labor Cost

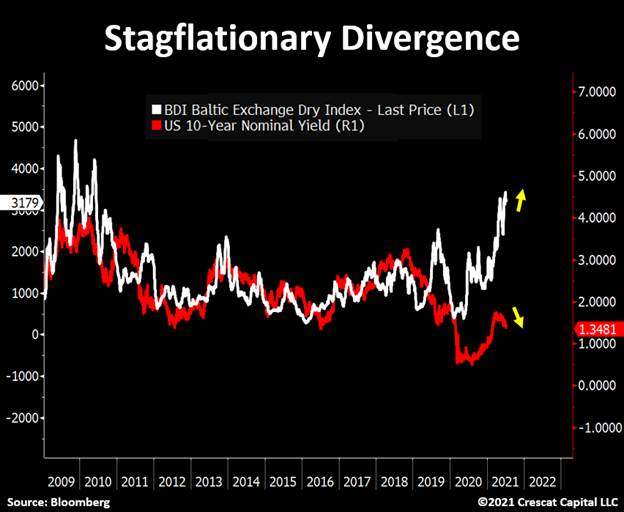

A Stagflationary Divergency

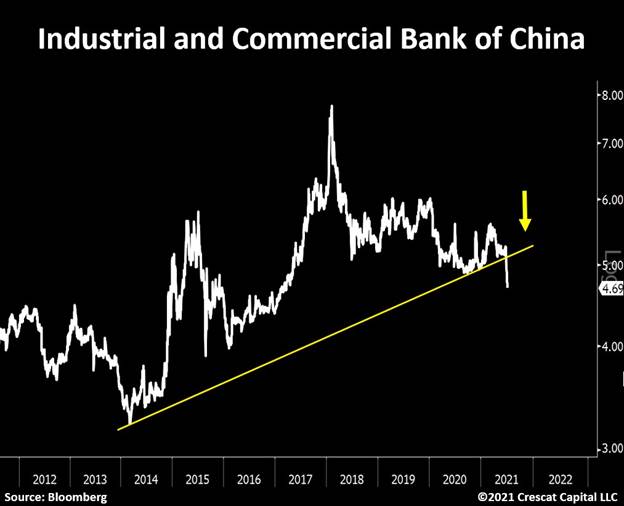

The Great Rotation With inflationary pressures rising in the US, we believe investors will be rotating out of over-valued long duration financial assets and into undervalued commodity cyclicals and inflation hedge assets, including scarce natural resource stocks. First and foremost, we see a coming renaissance in precious metals exploration stocks after a decade long bear market for this segment of the industry that only ended in March of last year. China is the Black Swan We are seeing clear signs that the Chinese economy is under pressure. China has built a highly leveraged $50 trillion-in-assets banking system on top of an inflated $16.5 trillion economy. That's an unprecedented amount of leverage in a banking system for a developing economy, a whopping 303% GDP. The Industrial and Commercial Bank of China is the largest bank in the world with $5.24 trillion in assets. Its stock price has been in a freefall since March. Every other major Chinese bank looks just as dismal. China's overall stock market has been in a steady decline since February that also more recently has morphed into collapse including Chinese ADRs that trade in the US and big tech and education stocks owned by US investors. The latter, for profit-education companies, was just banned by the Chinese government and appear headed to zero. It is hard to believe a systemic crisis is not in the process of unfolding now in China. China's credit impulse also recently dipped lower to -4%. We see an extraordinary risk of capital flight and currency devaluation if not outright currency crisis in China.

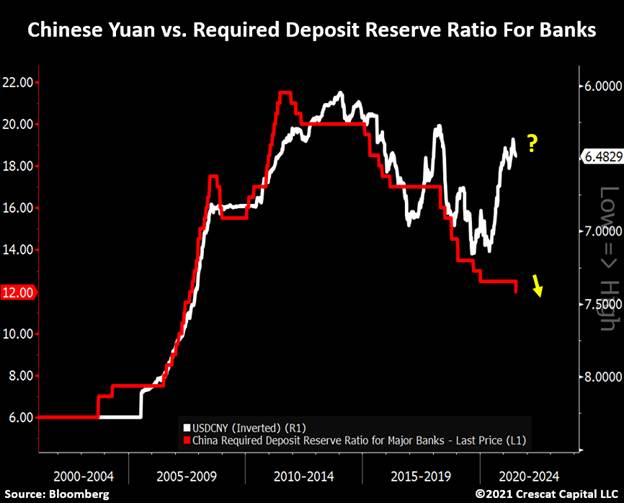

Chinese Yuan Ripe for Devaluation

Cuts in Bank Reserve Requirement Ratio Suggests Weaker Chinese Yuan Ahead China's steady decrease in its banks' reserve requirement ratio is another long-building macro divergence and indicator for an impending currency devaluation.

The Optionality for Gold While Chinese deflationary forces should not be shrugged off today, we should point out that it is the type of deflation that can deliver a flight-to-safety bid for gold. Gold is the one commodity as well as currency that we are most exposed to on the long side at Crescat today. We are further hedged versus China contagion risks in our global macro fund and long/short funds with select highly overvalued US equity short positions as identified by our equity model. Note the divergence between Chinese equities and US equities in the chart below. Similar divergences played to Crescat's advantage in our hedge funds in late 2018 and early 2020 as the US markets followed the Chinese one down.

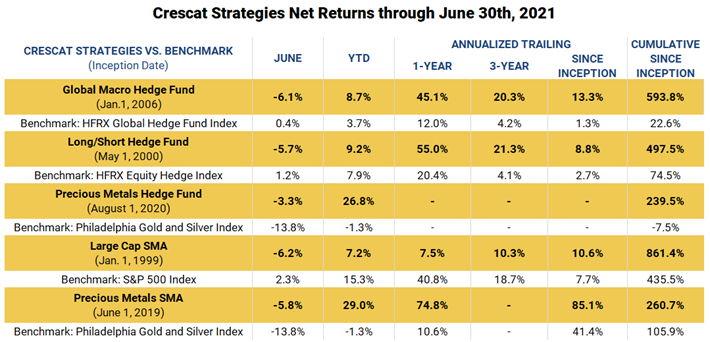

A Short-Term Deflationary Risk In the longer run, we believe a Chinese currency devaluation has global inflationary implications as it should lead to even more monetary easing worldwide including in the US. At the same time, we believe that the West is in the process of disengaging with China. The deglobalization trend currently underway is an inflationary force and a key factor portending a currency crisis. China's entire economic model has been highly reliant on Western capital inflows. China notwithstanding, we are most compelled to acknowledge and position for the risk of serious ongoing inflationary period ahead in the US for all the reasons we have outlined above and in our recent letters. We see average rates of inflation over the next five years substantially higher than in the last five. Today, across all the firm's strategies, we are now positioned in high absolute return opportunities in scarce resource assets with the goal of outperforming future inflation and delivering strong real returns. This positioning is the most focused in our Precious Metals and Large Cap strategies. In our Global Macro and Long/Short strategies, in addition to similar long exposures, we are also positioned in a myriad of short opportunities presented by today's macro climate which includes a historically overvalued US stock market. In our Global Macro Fund, we are further attuned to the risks and opportunities of a highly-levered and faltering Chinese economy with its impossibly over-valued Chinese banking system and currency. June Performance

A Great Time to Invest if Not Yet Positioned For those who are not already positioned with Crescat, we believe it is an incredible time to put money to work now, after the recent pullback in precious metals, which we believe is unsustainable for the reasons we have laid out above. The gold and silver selloff has continued into July month to date as the Chinese equity market has been melting down, but our precious metals positions have improved for us in four of the last six trading days. Precious metals mining is one of the very few areas of the market that offer both deep value and strong growth. We are encouraged that the worst of the precious metals pullback could be behind us already and view this as a great time to be picking up bargains. Meanwhile, we are positioned to capitalize on the short side of the market in Global Macro and Long/Short with exposure to extremely overvalued assets ripe for correction. Our team is approaching this market in a highly constructive manner through a comprehensive macro and fundamental investment process. We are very excited about the opportunities ahead for our portfolios. Sincerely, Kevin C. Smith, CFA Tavi Costa Kevin C. Smith is the chief investment officer and Tavi Costa is the portfolio manager of Crescat Capital. Crescat Capital is a global macro asset management firm. Its mission is to grow and protect wealth over the long term. It deploys tactical investment themes based on proprietary value-driven equity and macro models. Crescat's goal is industry leading absolute and risk-adjusted returns over complete business cycles with low correlation to common benchmarks. It applies its investment process across a mix of asset classes and strategies to assist with each client's unique needs and objectives. For more information including how to invest, please contact: Marek Iwahashi Cassie Fischer Linda Carleu Smith, CPA © 2021 Crescat Capital LLC Important Disclosures Performance data represents past performance, and past performance does not guarantee future results. An individual investor's results may vary due to the timing of capital transactions. Performance for all strategies is expressed in U.S. dollars. Cash returns are included in the total account and are not detailed separately. Investment results shown are for taxable and tax-exempt clients and include the reinvestment of dividends, interest, capital gains, and other earnings. Any possible tax liabilities incurred by the taxable accounts have not been reflected in the net performance. Performance is compared to an index, however, the volatility of an index varies greatly and investments cannot be made directly in an index. Market conditions vary from year to year and can result in a decline in market value due to material market or economic conditions. There should be no expectation that any strategy will be profitable or provide a specified return. Case studies are included for informational purposes only and are provided as a general overview of our general investment process, and not as indicative of any investment experience. There is no guarantee that the case studies discussed here are completely representative of our strategies or of the entirety of our investments, and we reserve the right to use or modify some or all of the methodologies mentioned herein. Separately Managed Account (SMA) disclosures: The Crescat Large Cap Composite and Crescat Precious Metals Composite include all accounts that are managed according to those respective strategies over which the manager has full discretion. SMA composite performance results are time weighted net of all investment management fees and trading costs including commissions and non-recoverable withholding taxes. Investment management fees are described in Crescat's Form ADV 2A. The manager for the Crescat Large Cap strategy invests predominatly in equities of the top 1,000 U.S. listed stocks weighted by market capitalization. The manager for the Crescat Precious Metals strategy invests predominantly in a global all-cap universe of precious metals mining stocks. Hedge Fund disclosures: Only accredited investors and qualified clients will be admitted as limited partners to a Crescat hedge fund. For natural persons, investors must meet SEC requirements including minimum annual income or net worth thresholds. Crescat's hedge funds are being offered in reliance on an exemption from the registration requirements of the Securities Act of 1933 and are not required to comply with specific disclosure requirements that apply to registration under the Securities Act. The SEC has not passed upon the merits of or given its approval to Crescat's hedge funds, the terms of the offering, or the accuracy or completeness of any offering materials. A registration statement has not been filed for any Crescat hedge fund with the SEC. Limited partner interests in the Crescat hedge funds are subject to legal restrictions on transfer and resale. Investors should not assume they will be able to resell their securities. Investing in securities involves risk. Investors should be able to bear the loss of their investment. Investments in Crescat's hedge funds are not subject to the protections of the Investment Company Act of 1940. Performance data is subject to revision following each monthly reconciliation and annual audit. Current performance may be lower or higher than the performance data presented. The performance of Crescat's hedge funds may not be directly comparable to the performance of other private or registered funds. Hedge funds may involve complex tax strategies and there may be delays in distribution tax information to investors. Investors may obtain the most current performance data, private offering memoranda for a Crescat's hedge funds, and information on Crescat's SMA strategies, including Form ADV Part II, by contacting Linda Smith at (303) 271-9997 or by sending a request via email to [email protected]. See the private offering memorandum for each Crescat hedge fund for complete information and risk factors.

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)