Send this article to a friend:

July

24

2021

|

Send this article to a friend: July |

|

Connecting the Dots: The Making of a Gold Heist, Part 1

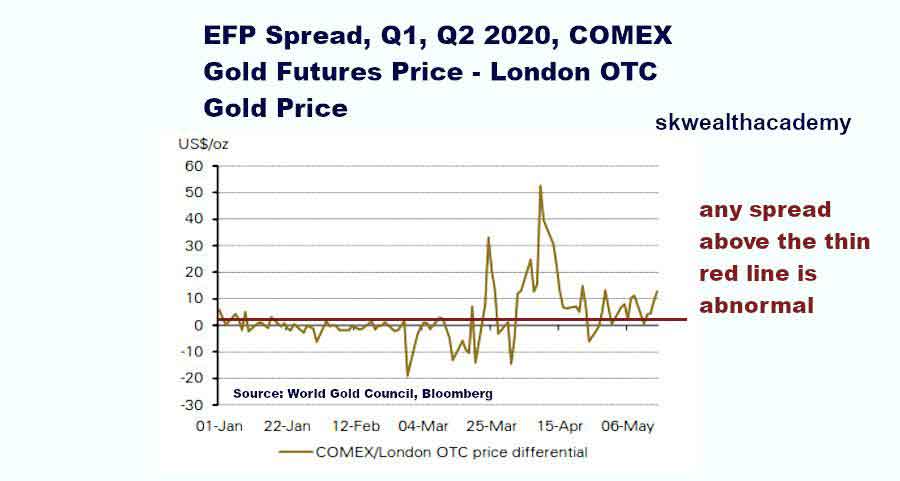

I have been writing about how the global banking cartel fraudulently uses EFP (Exchange for Physical) transactions for at least a decade or longer to cover for physical gold shortages with the use of swapping paper products for physical gold supply, even allowing for the substitution of shares of the NYSE traded silver ETF (NYSE: SLV) and shares of the NYSE traded gold ETF (NYSE: GLD) in the EFP exchange. Since I’ve written about this transaction extensively in the past, you may simply reference one of the many articles I’ve written about EFPs here, to get up to speed with how these transactions work. In this decade old article, you will see that I referenced something called EFS transactions as well, Exchange of Futures for Swaps. These seemed to have been phased out and replaced with EFR (Exchange of Futures for Risk) transactions. This is how the Chicago Mercantile Exchange explains EFRs: A position in an Over-the-Counter (OTC) swap or other OTC derivative in the same or related instrument for a position in the corresponding futures contract. What does this mean in simple to understand terminology? If you would like a one-word summary: fraud. If you would like a multiple word summary, in regard to precious metal derivative contracts, they would involve he exchange of unregulated contracts in private transactions in the shadowy opaque OTC market of synthetic derivative gold for regulated contracts of synthetic derivative gold in more transparent markets. In other words, just a lot of movement of synthetic gold between New York and London markets, most likely for the purpose of manipulating gold prices in derivative markets. Obviously, if you reference the link above that is from an article I published about these shady means of settling futures contracts, swapping paper for paper in 2011, I’ve been aware of these dealings for well over a decade. For years, I wrote about how such shady financial operations would always cause a massive disconnect between prices of real physical gold and silver and the spot gold and silver prices during times of tight physical gold and silver supplies. In Q1 this predictive relationship materialized into reality, and I spoke about this violently divergent spread between fake paper prices and real physical prices in this video I published on YouTube in March of 2020 (Please note that since Google/YouTube demonetized and shadow banned all my content, I discontinued posting content on the authoritarian YouTube channel; however, you can continue to support my video content here on Rokfin and my article/podcast/financial analysis content here on Patreon). Within weeks after I released this video, in which I spoke of the massive developing spreads in spot gold and silver prices with physical gold and silver coin prices, EFP gold spreads leapt from $2 to more than $75 an ounce. Remember the Exploding EFP Spreads Last Year? The EFP spread is the difference between London market gold spot prices and New York futures market gold prices, with the EFP spread a positive amount if futures exceed spot and a negative amount if spot exceeds futures. When the spread was its typical $2 obviously for big institutions to make real profits on such an arbitrage opportunity they would have to trade millions of gold ounces. However, when the EFP spread leapt to a $60 or $70 an ounce in 2020, a big financial institution could have locked in enormous profits by buying physical gold in the London spot market and agreeing to sell it at a $75 an ounce higher price in the New York futures market at a later date. Thus if a banker executed this arbitrage opportunity for a million ounces of gold, that would equate to a locked in guaranteed profit of $75M. Given the absurd amount of the EFP spread, many articles tried to tackle the mystery of these enormous spreads. The usual banking suspects emerged from the dark shadows in which they normally dwell to offer explanations that were never questioned by the mass media and forwarded to the world as the truth. Of course, as the banking oligarchs used covid as the scapegoat for nearly every global problem back then and for nearly every global problem even today as well, even for millions of starvation deaths directly caused not by the virus but by politically and financially motivated lockdown agendas, the mass media jumped on the false narrative to blame these massive EFP spreads on production and supply chain disruption caused by the virus. On the surface level, both of these explanations seem rational, but as I will explain, they are not. Recently for my Patron members, I completely deconstructed 95% of the garbage that was spread about the Basel III regulation effects on future gold prices in a massive investigative two-part series that required more than 14 hours to research and write, the point being that often the narrative spread by the establishment is in direct contradiction to the truth they would like hidden from the masses.

Consequently, if we took pause back then for just a few minutes to uncover the real reasons for the massive arbitrage opportunities that developed between paper New York and physical loco London markets in Q1 2020, we would have acknowledged that the establishment explanation would only explain perhaps as wide as a $6 to $8 spread that was three to four times larger than normal. However, the given mass media explanations were certainly insufficient to explain $30 to $75 spreads that were 15X to 35X larger than normal. Bankers used their same sneaky tricks as usual to mislead the masses into believing correlation was causation. To account for spreads that were 15X to 35X larger than normal, covid lockdowns alone could not have been fully responsible, especially since they developed in March 2020, at the very start of global lockdowns, and the lockdown consequences of disrupted mining production and supply chain distribution would not have been felt until a few months later. Many of the disruptions to the precious metals mining industry did not occur until about mid-March 2020, a development that could not have cause such an immediate shortage in physical gold (and silver) supplies that backed derivatives trading in New York and London. Thus, a reasonable person would have concluded that there were serious gold supply problems developing well before the mining production and supply chain disruptions and many serious gold analysts indeed arrived at this conclusion. In fact, if we simply compare the current gold spot price on 22 July 2021 of about $1,797 per ounce and we extend two months out from the front month contract in the current Western gold futures markets, zero arbitrage opportunity exists, unlike during H1 2020. August 2021 futures are selling at about the same price as current spot prices at $1,797.20. However, even though bankers have managed to since fix the massive arbitrage opportunities in gold that existed in 2020, that fiasco was wholly embarrassing to the establishment as it exposed the fraud of their paper derivative markets as well as the mechanisms by which bullion bankers use derivative markets to suppress precious metal prices. The Likely Mechanism that Created These Enormously Abnormal Spreads Here's what I believe caused those massive EFP spreads back in 2020 in the global gold markets. Physical gold supplies stored in NY and London gold vaults are always insufficient to meet the many multiples of synthetic gold that trade in Western gold derivative markets. However, the bankers can always get away with their executed fraudulent smoke and mirrors game because of the very low percentage of gold derivative contracts that stand for delivery. However, with the supply chain and operational production capacity of many major global gold mines coming to a halt, those that understand the fraud of the gold derivative markets in London and New York so this as the perfect opportunity to take advantage of the systemic fraud to dive the EFP spread ballistic. Quite simply, when you have a chance to squeeze a criminal, you don’t let this opportunity go to waste. Thus, how was this heist executed? As I explained above the exploding EFP spread allowed for institutions and even very well-heeled individuals to create guaranteed profits for themselves in the tens of millions and even hundreds of millions of dollars, a veritable easy score, at the bankers’ expense, for once. So don’t think a multiple heists did not take place during this time. The way to drive the EFP spread as high as it was driven would have been to stand for physical delivery of gold as the mechanism to close out open positions in the New York gold markets. This would result in the receipt of warrants on physical gold held in COMEX vaults that back gold derivatives trading. As I mentioned above, the amount of physical gold that is held in COMEX vaults to back gold derivatives trading has always been suspect in only being enough to truly back a tiny fraction of the daily trading volume every day. However, just taking warrants would be insufficient to squeeze EFP spreads 15Xs to 30Xs higher than normal. One would have to actually cash in the warrants and remove physical gold from COMEX vaults. I explain the entire process here in this article, but just because one closes out an open position in gold futures contracts does not mean that gold necessarily leaves COMEX vaults. This is the important part of the gold heist to understand. To actually cause soaring EFP spreads that were absurdly insane, I believe that massive amounts of physical gold had to have been removed from New York and London vaults during this time. Because often even physical gold represented by owners of gold futures contract that stand for delivery leave the physical gold vaulted in banker vaults, only removal would cause major stresses that would cause gold prices in the near future to soar over current spot prices in such an abnormal fashion. So removal is the key. And during a gold supply disruption, this would have been the perfect time to execute this gold heist. Why? Because as long as regular annual gold production is occurring, then if a large bank finds itself in a bind from unexpected percentages of gold futures contracts standing for delivery, then available supply can be easily enough transferred from one vault to another to meet unusually high demand for physical gold in gold derivative markets, as normally gold futures financially settle. And if regular gold production is occurring, bankers can execute their magik and sorcery of turning physical gold into paper through EFP an EFR transactions in which paper gold masquerades as physical. So the only real time to execute this bank heist is to stand for delivery, immediately cash in all warrants received, and to drain banker vaults of physical gold and to not allow them to continue to vault the physical gold that have warrants attached to them. This is the process by which massive EFP spreads would have been created? Is this actually what happened? I don’t know. Why? Because even if one digs up the corresponding data for that period of time for gold futures contracts that stood for delivery and observed a higher percentage than normal that would support my theory, then retrieving data about whether or not these players actually exercised their warrants to drain physical gold from bank vaults would be extremely difficult to gather. One may say that there is a way to do this and that methodology would be to track the eligible and registered amounts of gold in the COMEX and London vaults. But in my opinion, with so many documented cases of bankers reporting false data about their gold trades in the past, it is just downright foolish to believe that reported data about registered and eligible amounts of gold and silver stored in banking vaults is accurate. Thus, in reality, analysis of this data would never yield any data worthwhile of supporting or rebutting my theory, as any banker-reported data about gold that has not been confirmed by a certified audit executed by an independent third party with zero ties to the banking industry is of low utility in my opinion. I can tell you that you would be hard pressed to find a single person that has seriously researched the gold reserve holdings of the US, listed as 8,133.5 metric tonnes, and of China, listed as 1,948.3 metric tonnes as a remotely accurate reflection of actual holdings, simply because zero evidence exists from an independent third party unaffiliated with the US Federal Reserve or the PBOC that has provided evidence of these numbers. So why should we believe that bankers have suddenly discovered a conscience and are now honestly reporting accurate numbers about the physical gold and silver amounts vaulted in New York and London that back gold and silver derivative trading? But if you are an uber wealthy institution, and another major disruption to the physical gold and silver supply chain ever develop in the future, I just provided you with the blueprint for how you can create massive EFP spreads again, to buy precious metals on the cheap in London spot markets for future delivery at much higher prices in the in New York futures markets. In reality, this blueprint could still be used today, but with all the shenanigans that happen in gold and silver derivative markets on a regular basis, it would be much harder to pull off a successful heist without the benefit of a massive extended disruption in the supply chain. That said, one can still easily observe ongoing tightness in global gold and silver supplies simply by observing the very significant premiums between 1-ounce US American Eagle gold and silver coins and the current spot prices that exist in July of 2021. Critical Global Physical Gold and Silver Supply Shortages Still Exist Despite the Resolution of EFP Spreads Back to Normal If we look up the prices for quantities of less than $20,000 of American Eagle coins on the websites of coin dealers that offer prices toward the more competitive end of the price spectrum, right now, in mid-July 2021, the premium of current year 1-ounce US gold coins over spot is still a considerable $137 and 7.6%, much higher than the 4.5% premium that existed just a few years ago. And the spread between physical and spot in silver markets is even greater, with the premium of current year 1-ounce US silver coins over spot, for purchases of $18,000 or less, a whopping $10.42 and 41.5% higher than spot prices that are barely over $25 an ounce. If you have never purchased gold and silver coins, these whopping premiums may shock you, but every physical stacker has known about these increasingly bigger spreads between spot prices and 1-ounce coin prices that is a direct testament to real shortages of physical supplies of gold and silver, though merely following the highly banker managed EFP spread would lead one to falsely believe that these physical supply problems have completely disappeared today in comparison to Q1 2020. Let’s REALLY Dig Deep Down the Rabbit Hole To really understand why paper gold NY and physical gold London price spreads exploded, we need to dig deep in the US interest rate markets and follow the trail of monetary crumbs all the way back to September 2019. Yes, to really understand the tightness in global gold and silver supply and the relentless banker suppression of gold and silver futures and spot prices in recent months, we have to travel back to nearly two years ago. By following the money, we can also understand how much longer bankers are likely to hold gold and silver futures and spot prices within the fairly defined trading range in which they’ve been held for the past year, and when they are likely to break out. So what happened in September 2019. If we look at the below SOFR chart, we see a massive spike in SOFR (Secured Overnight Financing Rate) to 5.25%. The SOFR is the interest rate at which banks lend money to one another overnight, in which the lent money is secured by pledged collateral, usually US Treasury bills. This interest rate is dependent on an extremely tight lending timeframe (o/n) and is determined for many secured by what is supposed to be unbreakable collateral, US T-bills. Thus, if all was copasetic in the US banking system, the SOFR should always be close to zero. The fact that it spiked to 5.25% was an indication of massive structural breaks in the foundation of the US banking system. However, just because these massive cracks were already forming in 2019, this did not serve as urgent impetus to Central Bankers to actually repair the foundation. As we all know, their preferred methodology of addressing urgent structural breakdowns is to plaster over cracks that provide an aesthetic illusion of repair without the actual provision of any repair.

The September SOFR spike essentially indicated that commercial US banks no longer trusted each other to provide liquidity to the commercial banking system, and a couple of years of this distrust manifested in this year’s exploding o/n (overnight) volumes in the repo and reverse repo markets, of which I discussed the basis behind this extremely problematic development here. In this article, I discussed that there would be three important outcomes in US financial markets of these exploding o/n reverse repo markets, one of them being a near inevitable future breaking of the buck of US commercial banking MMF (Money Market Funds). Unsurprisingly, just a few days after I offered this opinion, the US Treasury Secretary Janet Yellen also expressed concern about MMFs breaking the buck in the near future, but as is the modus operandi of bankers, said that the threat to MMFs was not decreasing liquidity of the US commercial banking system instigated by exploding o/n reverse repo markets, but the explosion of the adoption and market cap of cryptocurrency stablecoins! Now if we travel back in time just a little bit to the start of the global economic lockdowns, inspired by the spread of coronavirus, you will note that I was already starting to connect all the dots of these seemingly unrelated financial events that I’ve thus far discussed in this article, as I released a podcast just two weeks after my warnings about a growing violent divergence in paper versus physical gold and silver prices about how the then just beginning global economic lockdowns had very little to do with protecting the health of billions of citizens, but was based upon enormous under the surface threats to hundreds of trillions of nominal amounts of global interest-rate derivative products that were threatened with complete meltdown by the threat of rising interest rates in the global economy. If you don’t understand why perpetual banker narratives that nominal amounts of derivative financial markets are not “real” and that the only risks lie in the face value of these contracts are false, let me quickly explain. Let’s assume a company purchases a derivative product from a bank for a face value of $1M that guarantees the repayment of a $100M loan from a company with a AAA rating of its corporate issued debt. On the surface, this seems like a good arrangement for everyone. The company that lends $100M pays a $1M expense as the cost of doing business to guarantee repayment of a loan 100Xs the size of the insurance it purchase. The banker is willing to take the risk of being on the hook for $100M because the company the banker is guaranteeing repayment of its borrowing is rated AAA and the banker asses the risk is being close to zero. However, if the company was lying about its financials, which really is not rare these days and actually happened with regularity during the 2008 global financial crisis during which Moodys and Standard and Poors handed out AAA ratings, like candy, to companies that really deserved junk bond ratings, then the risk of this $1M derivative contract is likely to be multiples higher than the banker assessment. If the company, because of their fraud, goes bankrupt after only repaying $2M of the $100M loan, guess who has to step in to repay the remaining unpaid $98M? The bank that entered into the liability side of this derivative product contract. And therefore the risk of this contract becomes $98M, much higher than the cost of the contract. Consequently, I don’t know if the entirety of the hundreds of trillions of nominal amounts of interest rate derivative contracts were bets on continued near zero interest rates, but let’s just say real global economic growth, economic recovery and higher interest rates on March 2020 presented an enormous problem to the global banking cartel that had tied their wealth to ZIRP. Though I’m engaging in speculation now, if you want to know how to crush the massive problem of rising interest rates induced by recovering economies that the global banking cartel faced in March of 2020 that threatened to crush the wealth of global bankers, it was coincidentally exactly what has happened throughout the world since that time frame - Fear monger to the point where you foment enough hysteria in the masses to create acquiescence and blind obedience to brutal lockdowns of the world economy highly inconsistent with the level of threat posed by a virus, subsequently destroy the global economy and in the process, destroy the threat of rising interest rates until the banker-placed bets on hundreds of trillions of dollars on forever low interest rates reach maturity and disappear. This speculation was the very basis behind my “Bitcoin to Soar in 2021” video I released in November 2020 as well as the basis for my “I Can’t Wait for This Year to Be Over!” video released a month prior in October 2020 in which I labeled every single person injected with hopium for a free society as of January 2021 as completely delusional. In the latter video, I predicted that global lockdowns would be pushed forth well into 2021 as the oligarchs and bankers could not afford to let the world’s economy recover in 2021 if they wanted to protect their wealth and prevent their hundreds of trillions of dollars of low interest rate market bets from imploding in derivative markets. Furthermore, if my above hypothesis is correct as being the real impetus behind the continuing waves of global lockdowns, then I’m sorry to inform you, if you reside in any of the European nations, the Canadian and Australian provinces and states and the Asian nations that have continued to implement brutal lockdown policies this year, that these waves of brutal lockdowns are unlikely to end until the start of 2023 at the very earliest. Why? Because this is the earliest time when the bulk of these low interest rate derivative products mature and the risk of a massive derivative market implosion from a massive bankers’ commitment to ZIRP will significantly dissipate. So are political oligarchs responsible for deliberately issuing lockdown mandates that they knew upfront had very little to do with protecting our overall health and everything to do with protecting their wealth? Should they be held responsible for the subsequent collateral damage of the descent of hundreds of millions of the poorest on planet Earth into a never-ending spiral of starvation, hunger and death that is still tragically ongoing? Recent investigations have hinted of deaths of many millions of the poorest citizens, around the world, in the past 18-months than have gone unreported by the media and completely ignored by the apathetic that live among the global population largely unaffected by these lockdowns (more than 4 million deaths attributable to lockdown policies in excess of deaths solely attributable to the virus in the nation of India alone). I will leave the answer of these questions up to you. This concludes Part 1 of this investigative report. In Part 2, I will discuss why precious gold and silver metal stackers and BTC and ETH traders and HODLers should be immensely curious about the outcome of US Treasury Secretary Janet Yellen’s recently called Presidential Working Group (PGW) meeting about stablecoins. I will also discuss how the agreed upon plan as a consequence of this July 2021 PGW meeting is likely to very significantly move BTC, ETH and gold and silver prices, possibly within the next few weeks to months, and in what direction and by what timeframe. I will also connect the dots of the July 2021 PGW event to an event that took place more than eight years ago that provides many clues to the answers of these aforementioned proposed questions. If you think I went deep down the rabbit hole in Part 1 of this two-part article, then you are going to be absolutely riveted by Part 2, so please be sure to check back for part 2. You will be able to find Part 2 of this article published on the skwealthacademy news site here within the next few days. Important: It takes a tremendous commitment of time, energy and resources to produce long multi-part articles such as this one. As I have been completely shadowbanned from all major social media platforms, if you would like to help support my content creation and prevent my publications from going extinct, you may do so by becoming a premium member on my Patreon and Rokfin platforms or simply make a donation here. Significant increases in the premium memberships on these platforms will be necessary to finance the continued free future publication of similar articles to this one.

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)