Send this article to a friend:

May

14

2021

|

Send this article to a friend: May |

|

The end of the LBMA is nigh

In recent months there has been some limited commentary concerning the introduction of Basel 3 regulations and the implications for precious metals trading. These new regulations are scheduled to be introduced for European banks at the end of June — only seven weeks’ time — and in the UK from 1 January next, affecting all LBMA member banks. This article explains the new regulations and concludes that the recent joint LBMA/WGC consultation paper addressed to the British regulator is unlikely to save London’s unallocated gold trading market. And because Basel 3 regulations are scheduled to be introduced into the UK at the year-end all banks in the London gold market can be expected to wind down their exposure well ahead of the deadline.

The unallocated forward settlement market will effectively be shut down. Hedging into Comex futures from this source will also cease. As it is unwound, the withdrawal of synthetic supply has enormous implications for future precious metals prices by transferring pricing power to physical markets, now dominated by China. Abbreviations in this article

Introduction On 4 May, the London Bullion Market Association in conjunction with the World Gold Council submitted a paper to the Prudential Regulation Authority making the case for unallocated gold to be spared a required stable funding factor (RSF) of 85% under new Basel 3 regulations. The new regulations are due to be implemented in Europe by the European Banking Authority at the end of June, to be followed in the UK on 1 January 2022.[i] The paper claims that if the proposed RSF of 85% is imposed on gold and other precious metals it would undermine clearing and settlement, drain liquidity, dramatically increase financing costs and curtail central bank operations.These are very serious statements to the effect that unless the London bullion market gets a waiver on the net stable funding ratio calculation (NSFR), it may as well shut up shop. And with the LBMA severely curtailed, the CME’s gold and silver futures contracts would lose out badly on both volumes and liquidity as well, with the number of active bullion bank trading desks (the Swaps) reduced to very few at the least. At first sight it seems crazy that the impact of Basel 3 regulations will be permitted to radically undermine forwards and futures markets, which have been so instrumental to deflecting hoarding demand from physical bullion. It is through paper derivatives that the gold price in particular has been kept suppressed in conjunction with central bank leasing, and therefore prevented from challenging the US dollar’s credibility, following gold’s replacement as the world’s reserve currency fifty years ago. The disruption to forwards and futures markets from Basel 3 will be a major shock, yet wider markets appear to be blithely ignoring the problem. When it goes ahead, Basel 3 will mean that banks will be forced to wind down their positions in unallocated precious metals, almost certainly causing massive disruption to physical bullion markets as well. If the expansion of paper markets has suppressed the prices of gold and silver for the last fifty years, then a severe contraction of paper equivalents at a time of escalating fiat money inflation could send prices to the moon. In order to understand the proposed regulations, we need to look at them while taking into account the standard accounting practice of double entry bookkeeping as it is applied to bank balance sheets. There are three new Basel 3 definitions that matter in this regard:

We cannot be sure yet that this will definitely happen, because it was put out for consultation in the UK by the PRA until 3 May. The end-June deadline after which Basel III applies in Europe might be extended again — which seems increasingly unlikely. In a patched-up compromise, unallocated gold could be rescheduled for a higher ASF and/or RSF, though again, that seems unlikely. Furthermore, the LBMA’s plea to the PRA, if successful, would only apply to UK regulated banks, not those in other jurisdictions, unless they set up full-blown London subsidiaries. And even that is unlikely to be acceptable to European and other regulators regulating their parents, because it is normal practice for regulators to look through such arrangements. The LBMA paper suggests a compromise, that London could follow Switzerland which intends to rely on a clause in the European Banking Authority’s rule book allowing banks to make returns to the regulator instead, and for the regulator to decide stable funding matters.[ii] For this to work, the PRA would have to obtain agreement on a common approach with banking regulators in Europe and elsewhere. If that is to be the case, time is running out rapidly. But the Swiss option only works on the basis that unallocated positions on both sides of the balance sheet are classified as interdependent. Any mismatch between unallocated gold liabilities and assets would not be covered. One assumes that hedging through Comex futures could resolve this issue partially, but that is only an assumption. And even if this get-out is adopted, liquidity will still dry up, because bullion bank trading desks will be given minimal trading discretion, limited to maintaining even books across the markets because of the NSFR issue. The Swaps category on Comex (the bullion bank trading desks) is currently net short of about $24bn in the GC gold futures contract and $1.6bn in silver futures. Pressure to pare back ownership of these positions to a few genuine market makers and American bank trading desks is bound to increase, because the short positions held by European bullion banks would have to be covered in the next six weeks. And in London, all LBMA banking members will similarly reduce their unallocated activities because unbalanced books would be heavily penalised by the rule changes when they come in for the UK as well. That would make Comex gold and silver contracts entirely dependent on producer hedging. The Bank of England will almost certainly express a view to the PRA as well as has the LBMA/WGC, not least because through swaps and leases for earmarked central bank gold in its custody it has been instrumental over the years in arranging for physical liquidity to be provided to the market in London. But it behoves the PRA to look more closely at the whole question of trading in unallocated gold, and specifically at the risks to the UK and European banking systems of a daily settlement average of 20 million ounces, or 620 unallocated equivalent tonnes between LBMA members. This does not appear to include additional unallocated tonnages between members and non-members, nor does it include intraday turnover. The London shell game In the interests of understanding the London bullion market, it will be helpful to start with definitions of unallocated and allocated gold accounts. According to the LBMA’s own website,Unallocated accounts

Note that instead of owning gold, the customer only has a general entitlement. Note also that it works like a normal bank currency account. And bear in mind that not only does a customer with an unallocated account not own gold but is just a creditor of the bank. All unallocated gold obligations appear on the bank’s balance sheet. Allocated accounts

This is a completely different type of account, where the bank is a custodian, and holdings do not appear on the bank’s balance sheet. Allocated gold is not at the disposal of the bank and cannot be used for its trading. In practice, banks discourage customers from holding allocated gold through high charges for storage and account maintenance fees. By way of contrast, a customer who maintains an unallocated account is often freed from bank charges entirely. Consequently, the large majority of customer accounts are unallocated. The LBMA/WGC letter leads its readers to assume the only difference between allocated and unallocated gold is the convenience unallocated gold provides for an efficient market. Nowhere is there any mention of the lack of physical gold backing unallocated accounts. And by ignoring the process of bank credit creation, it panders to the naïve assumption that banks are simply pass-through intermediaries with depositors on one side and loans on the other.

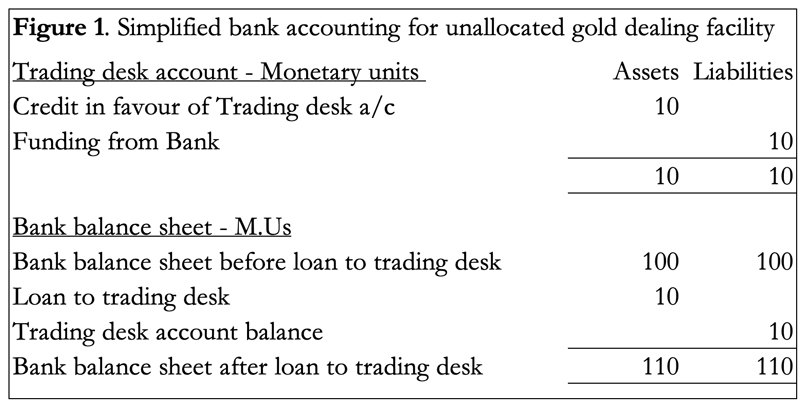

In common with banking regulators, the LBMA and WBC apparently fail to understand that unallocated accounts on bank balance sheets are only created by the process of bank credit expansion and have nothing to do with physical gold. The origin of all unallocated accounts is not the depositing of gold, but credit creation. Figure 1 shows how unallocated gold accounts are created in this way.

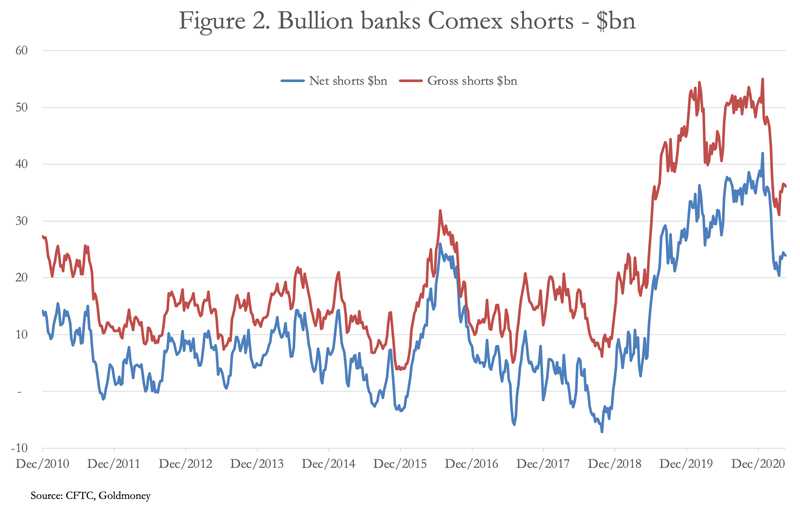

Let us say the trading desk has a facility granted to it by the bank to trade unallocated gold, and its account is credited with this facility by its bank to the extent of 10 monetary units. On its books, the bank records an asset in Monetary Units (normally dollars, or sterling, euros etc. depending on the bank’s accounting currency), reflecting the loan created in favour of its trading desk. At the same time, the bank records an equal liability matching the credit to its trading desk to allow the latter to fund its dealing book. It can now deal with other banks in unallocated gold, all of which will have created the facility to deal in unallocated gold by the same process of credit expansion ever since facilities to trade in unallocated gold evolved into existence. What’s happened is that the dealing desk’s facility has been funded by the expansion of bank credit out of thin air, in the same way that bank credit is expanded by any bank in any other line of banking business. This is standard accounting practice long established by banking law. From it, we derive two important points: the funding of unallocated positions in London is simply through the expansion of credit denominated not in gold, but currency; and with all banks using the same methods no gold is involved at all. Customers of the bank can, of course, request physical delivery, or delivery into an allocated account at the bank, in which case the trading desk acts as a broker, sourcing physical metal. But this function must not be confused with unallocated dealing by banks acting as principals, or on behalf of their customers with unallocated accounts. The LBMA/WGC submission claims that gold is vital collateral for central counterparties, which rely on the LBMA system to manage both it “and the physical delivery of precious metals derivative contracts” (page 3). The wording is misleading, because the delivery of a derivate contract is not the same as delivering the precious metal. The only other reference to collateral is in Annex 1, where the WGC trots out the usual stuff about gold having no counterparty risk and is widely accepted as collateral. That is true of physical gold, but is not relevant to unallocated gold, where counterparty risk is the only consideration and is the exclusive business between LBMA member banks. Unallocated gold is no more than book entries tied to the price of gold, and its origin and continued existence is entirely funded by the creation of bank credit. It is this that Basel 3 recognises. By introducing the net stable funding ratio, Basle III effectively makes standard banking practice unworkable in the case of unallocated precious metals by not permitting a trading book to net off its long and short positions. The regulators at the Basel Committee will not have jumped down on unallocated gold trading unless, in their opinion, they viewed it as a risk to the global banking system which must be offset by proper funding. Plainly, they understand the unallocated shell game for what it is, and that a failure in this market would be a threat to the entire banking system. Almost certainly, Basel III’s banking experts will have examined the risks in considerable detail before making their decision about the rates of both the ASF and RSF to be applied. And when it comes to cooperation from the European Banking Authority, there is also the additional risk that the UK’s PRA could find itself mired in post-Brexit non-cooperation. The impact on physical precious metals Asked to estimate the chances that the LBMA will succeed in stopping the imposition of the NSFR in Europe in six weeks’ time, the answer is it will be as likely as a cat in hell’s chance. While the Swiss proposal would provide some easement, it would effectively shut down their trading desks because of the penalties on uneven books. European and Swiss bank memberships of the LBMA are ten out of a total of forty-three, and most of those are UK incorporated subsidiaries. But it is unlikely that the EBA will accept that by sheltering the banking risks in a wholly owned UK subsidiary they can be simply ignored.A bare quarter of member banks being cut out of unallocated trading may not seem a major disaster for the LBMA. But it is the thin edge of the wedge. From this analysis it seems extremely unlikely that the PRA has any choice but to impose the NSFR calculation method on the London gold market when it adopts the rule, scheduled for 1 January 2022.[iii]This means that all UK subsidiaries and branches of foreign and domestic LBMA member banks must comply by then. In practice, all the non-European member banks are bound to cease running unallocated positions as principals and on behalf of customers in advance of the rule change. The last recorded level of LBMA-member unallocated gold positions was contained in the Bank for International Settlements over the counter derivative statistics for end-June 2020 at $572bn, while at the same time Comex Swap longs and shorts totalled $63bn. Rather like an iceberg, the visible regulated portion on Comex is one ninth of the total hidden derivative mass. If London adopts the Swiss proposal (we don’t yet even know if the EBA will accept it) then banks might be able to continue to run unallocated positions on an even book basis, but without trading income there is little point. Some of the market makers will cease trading and the balance are likely to run smaller books. For all intents, one half of that $500bn+ figure (representing one side of unallocated gold positions at the end of day settlement) will have to close out or be replaced with allocated physical. The regulatory impact on Comex’s futures contracts differs in that the Basel III treatment of regulated markets with central counterparties is a separate topic, beyond the scope of this article. Nevertheless, the end of furious daily trading activity in gold settling at over 600 tonnes a day in London will eliminate hedging activity into Comex futures. It would be too much to assume that such a severe contraction of paper market trading will lead to an automatic shift from paper into physical. But undoubtedly, some bank customers holding unallocated gold deposits at bullion banks will find their accounts closed and seek to replace them with physical gold. The full impact can only be guessed. But in the short-term it would appear that the Swaps category on Comex (bullion bank trading desks) have a separate problem closing their short positions. The most recent position derived from the CFTC’s Commitment of Traders Report is shown in Figure 2.

We don’t know how many of the European banks are short on Comex, which is the immediate problem, but the others with London trading desks (nearly all of them) will shortly find themselves in a similar position, if as expected the PRA follows the EBA by introducing the NSFR calculation from 1 January. Central bank involvement Central banks may find themselves in a difficult position, because of the unknown quantities of gold leased and swapped into the market. While bullion banks have been playing pass-the-parcel in the unallocated market, over the years they have been forced to deliver physical gold to bar hoarders, ETFs, jewellery fabricators and others. In recent decades these demands have exceeded mine and scrap supply by a fair margin, particularly driven by Asian demand. And while the LBMA has been triumphantly proclaiming 9,461 tonnes of gold are stored in LBMA member vaults, 5,616 of that is held at the Bank of England, almost entirely the earmarked property of central banks or their governments. That leaves 3,845 tonnes, of which about 2,500 tonnes are ETF gold, leaving 1,345 tonnes. Of that, an unknown amount is physical bars held by family offices, high net worth individuals and aggregated pooled accounts, probably leaving a balance of physical liquidity of as little as 500 tonnes. We were reminded recently that much of this physical has been supplied by central bank leasing when the GLD ETF briefly showed the Bank of England as a sub-custodian last year.We know this leasing of gold to supply the market has been a major factor since the LBMA got going in its current form. A respected analyst, Frank Veneroso, estimated leasing and lending of official reserves to be at least 10,000 tonnes as far back as 2002.[iv] In those days, gold leasing secured a carry trade as the funding basis for US Treasury bills, so much of it was a rolling total. One suspects some of it was delivered into markets and subsequently had to be replaced out of private sector sales. But clearly, if the derivative trade in unallocated dries up, significant quantities of physical gold leased to the bullion banks might have to be found. Additionally, while Western central banks have been leasing gold into the London market, the central banks and governments which have been adding to their gold reserves are predominently in Asia. In particular, we can be certain that China has substantial physical holdings of gold bullion not declared as gold included in its monetary reserves. The enabling legislation appointing The Peoples Bank sole responsibility for the state’s management of gold and silver bullion dates from June 1983, since when driven by government policy China has become the largest source of mine supply and rigidly controls refining and exports. Between 1983 and 2002, before it was legal for Chinese citizens to own and buy gold, inward capital flows and subsequent export surpluses coupled with a regime of strict exchange controls managed by the PBOC would have permitted the Chinese state to accumulate substantial quantities of bullion at contemporary prices, mostly between $200—$400 per ounce. Only after the state achieved its ownership objectives were citizens then permitted in 2002 to own gold — indeed, encouraged to do so. It is likely that Russia too has undeclared reserves and it is public knowledge she has been replacing US dollar reserves with gold, giving us important evidence of her monetary and strategic approach. China’s gold policy has extended to the wider control of global trade in physical gold, in cooperation with other Asian centres. So far, China’s control over physical markets has been dwarfed by London’s unallocated trading and the Comex futures market. That will change, handing China and Russia ultimate power over fiat currencies as the dollar’s hegemony is undermined and the gold price rises due to ending of paper market price suppression. Conclusion Changes proposed in Basel 3 mark the end of an era for derivative trading, when almost all gold and silver trading has been in unallocated form. The consequences for precious metals markets and prices should not be ignored or underestimated. The implications are understood by the LBMA, and their response to the UK regulator reflects their helplessness in the face of these changes.The joint submission by the LBMA and the WGC is economical with the facts by avoiding an admission that unallocated and allocated gold accounts are completely separate businesses. The origin of the former is through the creation of bank credit. And with all banks operating through credit expansion no physical gold is involved. Dealings are entirely in unallocated notional bullion, with the gold price serving as a valuation reference point. While the creation of unallocated gold through bank credit is one thing, customer demands for settlement in the physical are another, and generally discouraged. But over the years demand for physical has absorbed physical bullion supply and additional leasing of central bank gold, adding a second but entirely different problem for bullion banks. The remaining pool of available physical gold is relatively small when central bank, ETF and privately owned bars are allowed for in vaulting totals. True liquidity is not the headline 9,461 tonnes in London vaults, trumpeted by the LBMA, but is minimal — probably just a few hundred tonnes. It is from this small pool that daily imbalances in unallocated settlements which arise from delivery demands are satisfied. There is never a good time to introduce such radical changes into long-established market practices. But with issuers of fiat currencies debasing them at an accelerating rate, bullion banks face considerable difficulties unwinding their unallocated positions at a time when public demand for physical bullion is increasingly responding to fiat money inflation, spinning out of control.

[i] See The Impact of the NSFR on the Precious Metals Market: https://cdn.lbma.org.uk/downloads/Pages/NSFR-PRA-Letter-final_signed-20210504.pdf

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)