Send this article to a friend:

May

01

2021

|

Send this article to a friend: May |

|

The Fraying of the US Global Currency Reserve System

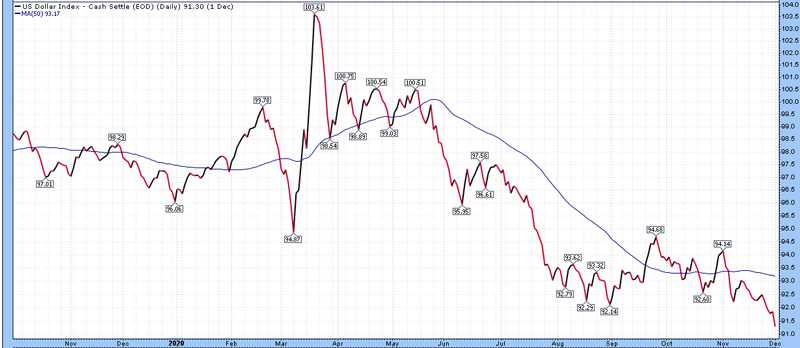

This view began forming when the Federal Reserve cut interest rates in summer 2019, and then the view solidified with a catalyst after an overnight repo rate spike in September 2019 forced the Fed to begin supplying repo liquidity. In my October 2, 2019 article, “The Most Crowded Trade“, I said to look for a weaker dollar in 2020, and also stated that the Fed would likely start expanding its balance sheet by buying Treasuries in 2020 or perhaps as early as that quarter in 2019 due to oversupply. Days later, the Fed indeed announced that they will begin buying Treasuries, and as of this writing well over a year later, they haven’t stopped. Here’s the dollar index since my October article, having fallen from about 99 to 92:

Chart Source: StockCharts.com Going forward over the next 3-5 years, I still expect many currencies including the dollar to continue to devalue vs hard assets, and for the dollar to probably be among the weaker major currencies during that timeframe (with occasional counter-rallies against that trend, as is natural). While it may or may not continue to be, so far this view has been correct. The dollar index is weaker now than it was in October 2019, but it’s still a process playing out. We had a curveball to the outlook from the pandemic in the first half of 2020 that temporarily spiked the dollar, but that merely added massive volatility to the structural forces playing out, rather than changing their direction. I don’t have a firm opinion about the next 3-6 months, because there are plenty of solvency issues between now and when things might start normalizing in the spring or summer of 2021, and dollar shorts are getting crowded at the moment, but as we look into late 2021 and into 2022, I remain with a dollar bearish outlook. Taking my view a step further, evidence shows that the global monetary system as currently structured is gradually re-aligning itself, and this fact will have important ramifications for investments over the long run. This article explores some of those concepts, ranging from the fraying of the existing petrodollar system (for all of its stakeholders, both for US interests and foreign interests), to central bank digital currencies, to a total restructuring of the global monetary system. It’s inherently a challenging subject, because for decades there have been many unsophisticated calls for a “dollar collapse” always right around the corner that never materialize. However, this isn’t one of those calls; it’s a quantitative look at the nearly 50-year history of this current global monetary system as structured since the early 1970’s. This article places an emphasis on where the bottlenecks and problems have been forming in the system, explains why a continued weak dollar over a 3-5 year period remains my base case, and shows why some of these growing pains seem to be leading to a new re-ordering of the global monetary system over this decade. Article Chapters:

The Structure of the Global Monetary System Rather than being a haphazard mess, international trade and exchange rates have a certain structure to them, built and enforced by the hegemonic powers that exist during a given era. In other words, at any given time, an empire or set of powerful countries work together to enforce a rules-based global order on how international trade works, and how it is priced. However, there is inherently an economic entropy within any system, as order gradually frays into disorder. Global monetary systems can be long-lasting, but not permanent. As the global center of power shifts over time, and as bottlenecks and imperfections in the system grow to unsustainable levels resulting in increasing levels of disorder, a system gradually or abruptly gets re-ordered into another system. Ironically, it’s often not an external threat that brings down the existing order; it’s the flaws within the system that, left unchecked, eventually expand enough to bring it down and necessitate a re-ordering, either from the same ruling regime or from a new regime that displaces it. Over the past century, for example, the world went from a gold standard system, to the Bretton Woods system, to the petrodollar system. Each system mostly unraveled from within rather than being brought down externally, and each time one system transitioned to another, a significant and widespread currency devaluation occurred. Gold Standard (pre-1944) For much of human existence, economies were based on trade. Furs for oysters, olive oil for spices, labor for bread, etc. The mining of precious metals like gold and silver made that simpler, and these metals have been considered money for thousands of years. With precious metals, you could turn a specific commodity (like furs) into a universal commodity (like gold and silver, which are rare, long-lasting, and able to be broken into small measurable units), to buy whatever you want at a later date. From there, paper currency and credit was added as a more convenient layer onto gold. Gold itself could be held securely in vaults, and paper slips representing a share of that gold could be used as mediums of exchange. Sometimes they were issued by private banks, and in modern times they were generally issued by sovereign governments. In this sense, governments would issue paper currency that is backed by gold held in central bank vaults. From that point, we saw the rise of global reserve currencies, referring to either paper or precious metal currencies of trading or military empires that were recognized and accepted in many countries outside their own homeland. The Roman Empire was an ancient example. More recently, the Dutch Empire was a notable example, followed by the United Kingdom, and now the United States. In the 1800s and early 1900s, the United Kingdom had the mantle of the most globally recognized currency, although it existed within a system of many currencies being backed by gold. During these centuries, the center of global power mostly rested within Europe with its precise epicenter shifting over time, and wars within Europe played a large role in its eventual replacement. Under this gold standard system, exchange rates between currencies still shifted over time for various reasons, with the balance of payments being a key variable. My article “Why Trade Deficits Matter” goes into detail on why that is the case. The crux of it is that whenever a country began persistently importing more than it was exporting, it risked having gold flow out of the country and risked economic stagnation within the homeland. Ultimately, however, this state would usually be self-correcting because a recession would eventually devalue the currency, which would make their exports more competitive and imports more expensive, and thus re-align their export and import balance. In the later stages of this system, all major nations devalued their currencies sharply and reset or suspended their gold pegs.

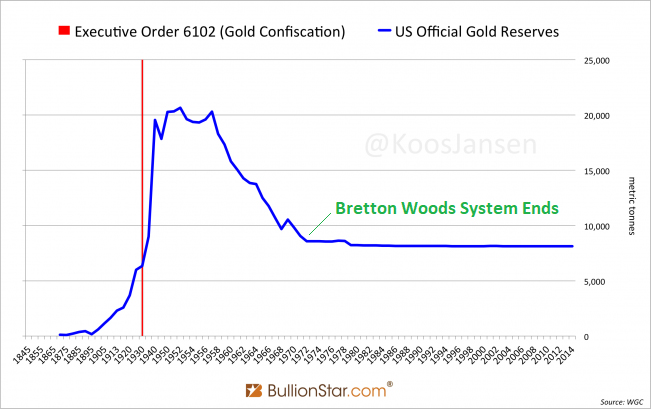

Chart Source: Bridgewater Associates The winners of the world wars devalued their currencies less than the losers, but everyone devalued. This was partly from the wars, but also just as much from the end of the long-term debt cycle. Bretton Woods System (1944-1971) The most recent handover of global reserve currency status gradually began after World War I, and was finalized in the later stages of World War II. As a result of the wars and the rise of the American economy, the center of global power shifted from Europe (and particularly the United Kingdom) to the United States. In the 1930’s, the United States government made gold ownership illegal and forced citizens to sell their gold to the government, which allowed the government to build up huge gold reserves. Then, in order to keep gold safe during the war, many countries shipped their gold to the United States. So, the United States had its own massive gold stockpile, and also served as the global gold custodian for many allies. As World War II unfolded, while Europe and east Asia were devastated by the war, the United States homeland was barely touched, and the US became the world’s largest creditor nation in the process. At that point, the Bretton Woods system was established, whereby the United States backed its dollar by gold, and dozens of other countries pegged their currencies to the dollar, and thus also had a gold standard by association. Many countries held US Treasuries, as a form of reserve collateral that was “good as gold”. The dollar was not redeemable to US citizens for gold, but it was redeemable to foreign governments for gold. During this time, the United States also began laying the groundwork for its alliance with Saudi Arabia, which would come into play with the next system. This period also saw the rise of the “eurodollar market”, referring to the dollar market that exists between banks and other entities outside of the United States and outside of the Federal Reserve’s jurisdiction, primarily centered in Europe but extending throughout the world. With the Bretton Woods system and the following petrodollar system, the United States obtained a near-global lock on the international money system. Previous empire currencies never obtained that complete of a financial lock on the world, and thus were never true “global reserve” currencies but instead were just “widely recognized and dominant” currencies. So the 1944-present status of the dollar as the global reserve currency is not perfectly comparable to pre-1944 periods of other global reserve currencies. This period was rather unique, in other words. It was the first time technology allowed the entire world to be connected together enough for a truly global war to happen, and for a truly global monetary system to come in its wake. However, after only a decade, the Bretton Woods system began to fray. The United States began running large fiscal deficits and experiencing mildly rising inflation levels, first for the late 1960s domestic programs, and then for the Vietnam War. The United States began to see its gold reserves shrink, as other countries began to doubt the backing of the dollar and therefore redeem dollars for gold instead of comfortably holding dollars. This chart shows US gold reserves as measured in metric tonnes:

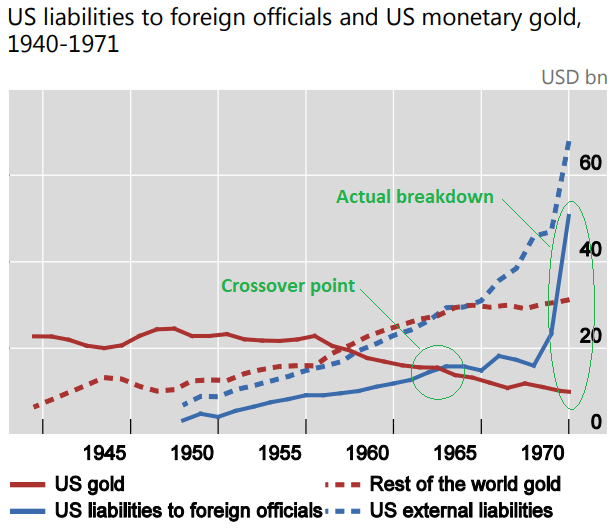

Chart Source: Bullionstar In fact, the numbers show that from inception, it was already on an unstable path. The US began the system with more gold than foreign liabilities, but that gap quickly began closing within the first few years. By the late-1950s, US external liabilities exceeded US gold reserves. By the mid-1960s, the subset of US external liabilities that were owed to foreign officials exceeded US gold reserves, which was the true crossover point where the system became troubled. And by 1971, the system broke down and was defaulted on by the United States.

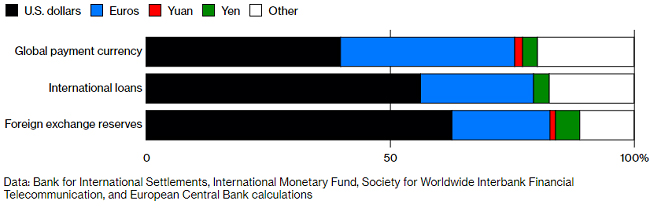

Chart Source: BIS Working Papers No 684 The system had an underlying flaw that when left unaddressed brought the system down. It was never truly sustainable as designed. There was no way that the US could maintain enough gold to back all of its currency for domestic use, and simultaneously back enough currency for expanding global use as well (which was the part that was redeemable). Some economists such as Robert Triffin, explicitly warned about this problem to Congress and the business world in what became known as the Triffin dilemma. It was a foreseeable problem, in other words. The same thing happened to the United Kingdom in the early 1900s, prior to World War I. John Keynes saw the problem ahead of time too, and proposed an alternate system called the Bancor, where an international unit of account based on gold and a basket of major currencies would be used to settle balances of trade and would be held as a central bank reserve asset. This would be an inherently more balanced system, with a neutral settlement mechanism rather than centering everything on the currency of one country. However, politics often wins out over math, at least at first, and the Bretton Woods system won over other ideas. Something like the Bancor idea was enacted on the side by the IMF as well, with units called SDRs that are a basket of major currencies and are still held by central banks, but it never had enough support to catch on in more than a limited way. Eventually in 1971, math came back with a vengeance on the Bretton Woods system, and Richard Nixon ended the convertibility of dollars to gold, and thus ended the Bretton Woods system. The closing of gold convertibility was proposed to be temporary at the time, but it ultimately became permanent. Rather than shifting to another country, though, the United States was able to re-order the global monetary system with itself still in the center, in the next system. Ultimately, all major currencies including the dollar devalued radically vs gold and other hard assets in the 1970’s. This continued the trend of major currency devaluations happening whenever the global monetary system gets re-ordered. Usually the same forces that break the system, also break the currency itself. When that happens, the quantity of broad money supply goes up significantly, and the purchasing power of existing debts gets partially inflated away. Petrodollar System (1974-Present) Beginning in 1971 after the breakdown of the Bretton Woods system, currencies around the world all became fiat currencies, and the global monetary system became less ordered. This was the first time in human history that this happened, where all currencies in the world at the same time were rendered into unbacked paper. A “fiat” is an absolute decree from a person or institution in command. Fiat currency is a monetary system whereby there is nothing of value in the currency itself; it’s just paper, cheap metal coins, or digital bits of information. It has value because the government declares it to have value and that it is legal tender to pay all things including taxes. A country can enforce the usage of a fiat currency as a medium of exchange and unit of account within their country by making all taxes payable only in that currency, or by enacting other laws to add friction to, or in some cases outright ban, other mediums of exchange and units of account. If their currency has a big enough problem, though, as is the case for many emerging markets, a black market will develop for other mediums of exchange, such as foreign currency or hard assets. A fiat currency can face particular problems when trying to be used outside of its home country. Why should businesses and governments in other countries accept pieces of paper, which can be printed endlessly by a foreign government and have no firm backing, as a form of payment for their valuable goods and services? Without a real backing, what is it worth? Why would you sell oil to foreigners for paper? In the early 1970’s, there were a variety of geopolitical conflicts including the Yom Kippur War and the OPEC oil embargo. In 1974, however, the United States and Saudi Arabia reached an agreement, and from there, the world was set on the petrodollar system; a clever way to make a global fiat currency system work decently enough. We think of this as normal now, but this five decade period of global fiat currency is unusual and unique in the historical sense. Imagine trying to architect a way to make an all-fiat currency system work on the global stage for the first time in human history. In doing so, you have to somehow convince or force the whole world to trade valuable things for foreign pieces of paper with no guarantee from the paper-issuing governments that those papers are worth anything in particular, in relation to an amount of gold or other hard assets. With the petrodollar system, Saudi Arabia (and other countries in OPEC) sell their oil exclusively in dollars in exchange for US protection and cooperation. Even if France wants to buy oil from Saudi Arabia, for example, they do so in dollars. Any country that wants oil, needs to be able to get dollars to pay for it, either by earning them or exchanging their currency for them. So, non oil-producing countries also sell many of their exports in dollars, even though the dollar is completely fiat foreign paper, so that they can get dollars for which to buy oil from oil-producing countries. And, all of these countries store excess dollars as foreign-exchange reserves, which they mostly put into US Treasuries to earn some interest. In return, the United States uses its unrivaled blue-water navy to protect global shipping lanes, and preserve the geopolitical status quo with military action or the threat thereof as needed. In addition, the United States basically has to run persistent trade deficits with the rest of the world, to get enough dollars out into the international system. Many of those dollars, however, get recycled into buying US Treasuries and stored as foreign-exchange reserves, meaning that a large portion of US federal deficits are financed by foreign governments compared to other developed nations that mostly rely on domestic financing. This article explains why foreign financing can feel great while it’s happening. The petrodollar system is creative, because it was one of the few ways to make everyone in the world accept foreign paper for tangible goods and services. Oil producers get protection and order in exchange for pricing their oil in dollars and putting their reserves into Treasuries, and non-oil producers need oil, and thus need dollars so they can get that oil. This leads to a disproportionate amount of global trade occurring in dollars relative to the size of the US economy, and in some ways, means that the dollar is backed by oil, without being explicitly pegged to oil at a defined ratio. The system gives the dollar a persistent global demand from around the world, while other fiat currencies are mostly just used internally in their own countries. This chart is two years old, but things haven’t changed much since then. What it shows is that even though the United States represented only about 11% of global trade and 24% of global GDP in early 2018, the dollar’s share of global economic activity was far higher at 40-60% depending on what metric you look at, and this gap represents its status as the global reserve currency, and the key currency for global energy pricing.

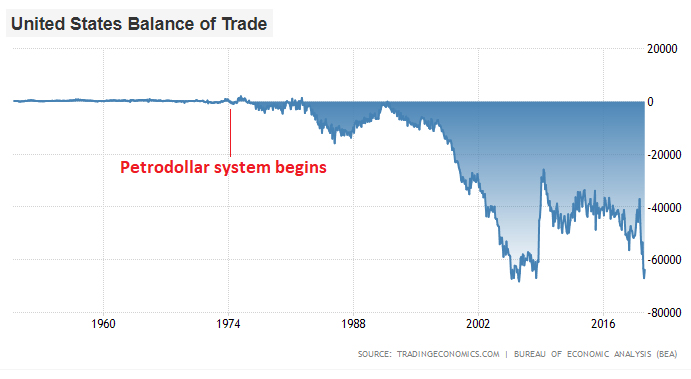

Chart Source: Bloomberg The inherent flaw of the petrodollar system, much like the inherent flaw with the Bretton Woods system, is that as previously mentioned, the United States needs to run persistent trade deficits, and is another version of the Triffin dilemma again. This can work for decades but can’t work forever.

Chart Source: Trading Economics Instead of drawing down our gold reserves, however, we gradually draw down our domestic manufacturing base and it gets replaced piece-by-piece in foreign countries. When most other countries run trade deficits, they eventually have a big enough currency devaluation so that their exports become more competitive and importing becomes more expensive, which usually prevents multi-decade extremes from building up. However, because the petrodollar system creates persistent international demand for the dollar, it means the US trade deficit never is allowed to correct and balance itself out. The trade deficit is held open persistently by the structure of the global monetary system, which creates a permanent imbalance, and is the flaw that eventually, after a long enough timeline, brings the system down. The other flaw in the system is that it incentivizes mercantilism. This means it incentivizes various trade partners to maximize their exports and minimize their imports by manipulating their currencies to weak levels. Since currencies around the world are fiat with floating exchange rates, many countries try to keep their own currencies weak, so that they have a positive trade balance with the United States and other trading partners. They don’t want their own currencies to be so weak that their citizens can’t import things, but they want their currencies to be weak enough so that their exports are very competitive and the importing power is not very strong, so that they can run trade surpluses. This allows a country to rapidly build up industrial production, and accumulate dollars and reserves. As the global reserve currency, the United States is basically excluded from this option, so we’re the ones left holding the bag of persistent trade deficits. Some of us, particularly near the top of the income ladder, directly or indirectly benefit from this system. Americans who work around finance, government, healthcare, and technology get many of the benefits of living in the hegemonic power, without the drawbacks. On the other hand, Americans who make physical products tend not to benefit, because they lost their jobs or had their incomes suppressed, and thus haven’t benefited from the gains. And outside of the United States, exporting countries benefit from the system, while countries that don’t like how the global monetary system is structured don’t have much recourse to do anything about it, unless they get big enough like Russia and China. The Great Petrodollar Bull/Bear Cycle Because exchange rates are free-floating since 1971 within the petrodollar system, the dollar can strengthen or weaken against other currencies significantly, and other currency pairs can strengthen or weaken relative to each other. Whenever the dollar begins to take a dip, we get a host of superficial articles from financial media about the “potential loss of the dollar’s global reserve status”, but that’s not how it works. Conversely, if an analyst such as myself brings up that the dollar may decrease markedly vs other major currencies, one of the comments or pushback they’ll get is “but the US is the global reserve currency.” We need to treat those concepts separately. The dollar indeed has had two huge bear market drawdowns of 40%+ vs a basket of other major currencies within this existing monetary system, without losing global reserve currency status. Being a dollar bear within the existing petrodollar system (and having no opinion about the petrodollar system ending), is not identical to someone who thinks the petrodollar system as currently structured is coming to an end. This chart is the dollar index since the early 1970’s when the petrodollar system began. The chart compares the dollar vs a basket of major currencies, and shows the three major cycles it has gone through (click here for a bigger view):

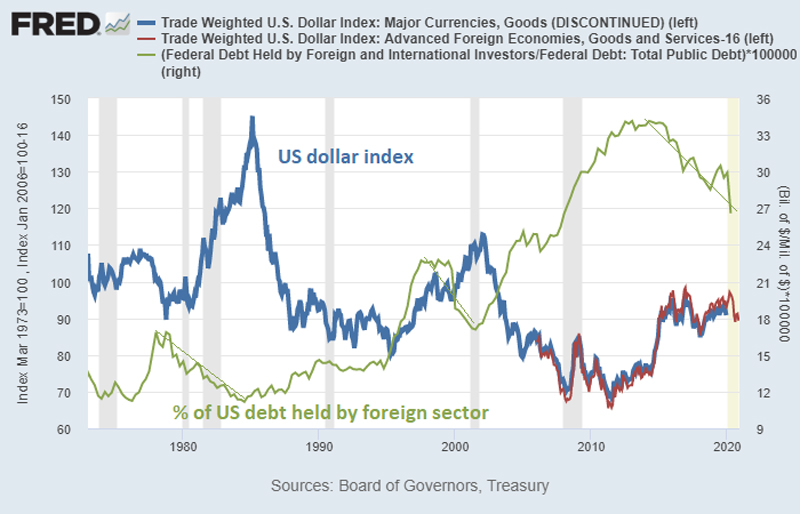

Chart Source: StockCharts.com The dollar index broke below its 50-month moving average this year, and that 50-month moving average itself now has a slight downward tilt. Could it have another one of those dollar down-legs like it had after the previous two major cycle tops? Sure. So, let’s separate being a dollar bear from being someone who thinks the global monetary system will change structurally. The two don’t necessarily go hand in hand, although they can. It’s important to treat those ideas independently, because even though I do hold both of those views over different timeframes, they aren’t the same view. Similarly, the dollar being the world’s reserve currency doesn’t necessarily protect it from major swings relative to other currencies. In fact, the depth to which the dollar is plugged into the global financial system arguably gives it bigger swings than it otherwise would have, both to the upside and downside. Causes for the Cycle The dollar cycle is based on major shifts in monetary and fiscal policy, as well as the resulting capital flows for global money that wants to chase whatever area of the world is doing well. Underlying all of this is the global monetary system as currently structured, i.e. the petrodollar system. As I discussed in my February 2020 article, “The Global Dollar Short Squeeze” and in my April 2020 article, “The $40 Trillion Problem“, governments and companies outside of the United States have a lot of dollar-denominated debt ($13 trillion at a minimum according to the BIS), but also have even more dollar-denominated assets (around $42 trillion according to the IMF and US BEA). These debts and assets were built up over decades due to those countries running trade surpluses with the United States, and from the dollar being used for the majority of global financing deals, especially for emerging markets. That dollar-denominated debt represents a consistent source of demand for dollars to service those debts. So, if recessions happen, or dollar-based global trade slows down, there can become a scramble for dollars which can be in short supply outside of the United States, causing an international dollar spike. This happened in March 2020 as the pandemic sharply diminished global trade, and oil prices collapsed. In that sense, the petrodollar system reinforced itself over time. At first, countries needed dollars so that they could get oil. After decades of that, with so much international financing happening in dollars, now countries need dollars so they can service their dollar-denominated debts. So, the dollar is backed by both oil and dollar-denominated debts, and it’s a very strong self-reinforcing network effect. Importantly, most of those debts aren’t owed to the United States (despite being denominated in dollars), but rather are owed to other countries. For example, China makes many dollar-based loans to developing countries, as do Europe and Japan. When the dollar strengthens relative to emerging market countries’ local currencies, it acts as a sort of quantitative tightening for those countries because their dollar-denominated debts go up in local currency terms relative to their assets and cash flows, which can be particularly brutal during recessions. That’s one of the key reasons why emerging market assets and economies are riskier and more volatile than developed market economies; their dollar-denominated borrowings. On the other hand, a weakening dollar can be like quantitative easing for them, as it eases their debt load relative to their local-currency cash flows and assets. Similarly, dollar-denominated assets, especially ones held by foreign governments and central banks (acquired from years of trade and current account surpluses), represent collateral with which those countries can defend their currencies, or represent assets that they can sell in order to get dollars to support their obligations if need be. During a weak dollar period, there is often a global economic boom, and nations around the world including the United States have a period of growth and prosperity. If nations are smart, they start building up big foreign exchange reserves with their dollar inflows. Within this petrodollar system, that has meant buying US Treasury securities. Countries also often use that period to take out dollar-based loans, which comes back to bite them later. During a strong dollar period, the global economy often slows, and nations get squeezed by dollar-denominated debts. They buy far fewer Treasuries, if any, and might even sell some to get dollars to service dollar-denominated debts or manage their currency. As a result, we see a clear pattern between dollar strength and the percent of US federal debt held by the foreign sector. Whenever the dollar enters one of its big bull runs, foreigners start to get squeezed, global growth slows (including US growth, due to the interconnection of the global economy), and foreigners slow down or stop their purchases of US debt. This chart shows the trade-weighted dollar index in blue (with a newer index in red spliced onto it, due to the fact that the longer-running index discontinued at the start of 2020), and the percent of US federal debt held by the foreign sector in green:

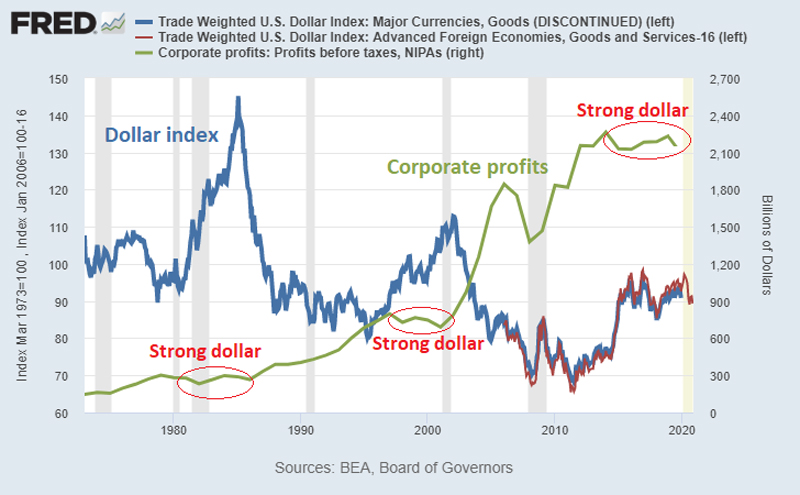

Chart Source: St. Louis Fed As the chart shows, each of the three major dollar index bull runs were accompanied by a sharp reduction in the percentage of US federal debt held by the foreign sector. The United States was still issuing debt, but foreigners weren’t buying much of it. This lack of buying by foreigners forces the US to fund its own federal deficits, meaning either its private sector or increasingly the Federal Reserve itself had to buy Treasuries, and that eventually leads to a dovish shift in US monetary policy, which plays a role in weakening the dollar and starting the cycle anew. For a second chart, we can compare the dollar index to US corporate profits, which shows that corporate profits go flat in dollar terms for a number of years every time there is one of the big dollar bull runs:

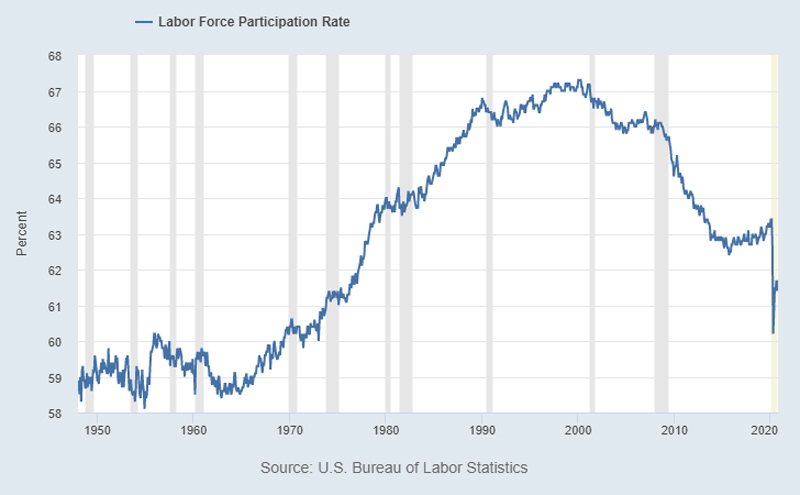

Chart Source: St. Louis Fed In other words, as we all know, the global economy is interconnected. The US usually runs into economic problems when the dollar strengthens, just like certain other parts of the world. In a strong dollar environment, US exports become less competitive, and the overall global trade environment becomes sluggish, resulting in domestic stagnation within the US as well. The 1980s dollar spike occurred in an environment with less global debt, so it required deliberate intervention to reverse. The second and third dollar spikes occurred in environments with more debt in the US and elsewhere, and thus were more self-correcting without global coordination, by unilateral shifts in monetary policy by the US Federal Reserve to protect the US Treasury market and stimulate the domestic economy. 1980s Dollar Cycle The dollar was weak in the 1970’s after going off the gold standard, and the United States and many other countries experienced rapid consumer price inflation. In the early 1980s, the new Fed chairman Paul Volcker jacked up interest rates to quell inflation. At the same time, Ronald Reagan ran large fiscal deficits by cutting taxes and increasing spending, which contributed to an economic boom. This combination of tight monetary policy and loose fiscal policy tends to be strong for a currency while it lasts. The first half of the 1980s saw rapid strengthening in the dollar. This contributed to the Latin American debt crisis; emerging markets in Latin America were unable to pay dollar-denominated debts back, resulting in defaults, recessions, and currency crises. Debts within the United States were very low, so interest rates could be kept high by Volcker for a long time, which added a lot of fuel to the dollar bull run. The dollar eventually reached an apex in 1985, when the United States and four other major countries (Germany, Japan, United Kingdom, and France) agreed to deliberately weaken the dollar in an event called the Plaza Accord so that American and European exports would be more competitive vs Japanese exports, which were dominating global trade at the time. As the dollar fell in the late 1980s and the yen strengthened markedly, money flooded into Japan, which along with their overall strong economy, led to the massive well-known Japanese equity and real estate bubble. 1990s/2000s Dollar Cycle The Soviet Union fell in 1991, leaving the United States as the world’s sole superpower, and led to a period of opening markets and rapid globalization. In the early 1990s, the United States had a recession, and saw a period of declining interest rates, and the dollar was weak overall. Emerging markets had a strong period until the mid-1990s. At that point, the United States’ economy began to do well and raised interest rates, beginning the second dollar bull run. In addition, the US baby boom generation reached its peak working age, resulting in the highest level of labor participation in US history:

Chart Source: St. Louis Fed By the second half of the 1990s, the United States entered a tech boom/bubble period, and the dollar spiked. Several emerging markets encountered serious dollar-denominated debt problems, resulting in the 1997 Asian financial crisis and the 1998 Russian financial crisis. Emerging markets, as a whole, suffered. It mirrored the 1980s Latin American debt crisis, but with its epicenter in southeast Asia. The reason that some emerging markets suffer more than others during a given cycle, has to do with the amount of dollar-denominated debt they have relative to the amount of foreign-exchange reserves they have. The most vulnerable nations for a financial crisis are the emerging markets that have high dollar-denominated debts and low foreign-exchange reserves, while those with the opposite situation of high reserves and low debts are well-fortified. By 2000, the US dotcom equity bubble began to collapse, and the Fed cut interest rates. In the years that followed throughout the 2000s decade, the dollar weakened notably, and emerging markets had a massive boom period. The acronym “BRIC” became popular, referring to the idea that Brazil, Russia, India, and China, due to large populations and massive growth rates, would become increasingly important on the global economic stage. 2010s/2020s Dollar Cycle The dollar remained weak for a while, although it had a brief spike around the 2008/2009 global financial crisis as oil prices fell and a global recession occurred. The Fed, in particular, did three major rounds of quantitative easing, but those ended in late 2014. Between 2014 and 2015, as the Fed shifted to tighter monetary policy by putting an end to QE, the dollar quickly strengthened, resulting in the third major dollar bull run. Several emerging markets subsequently encountered a severe recession from 2014-2016. In 2016, the dollar reached a peak, and there were talks of a secret Shanghai Accord to weaken the dollar, in reference to the well-known Plaza Accord of 1985. The dollar indeed weakened significantly throughout 2017, and the world encountered “global synchronized growth” as it was called, where the United States, Europe, Japan, and emerging markets all did quite well together. In early 2018, the Fed began quantitative tightening (reducing the size of its balance sheet), and the dollar began re-strengthening. From peak to trough, the dollar only had a 12% drawdown from its peak, and never achieved one of those massive 40% dollar declines like the previous two cycles. By mid-2018, global growth began to slow in the US and the rest of the world. The dollar weakness was a fake-out, in other words. It was still a strong dollar period. Argentina and Turkey in particular began experiencing currency crises. They were the vulnerable ones, with lots of dollar-denominated debt and little foreign-exchange reserves. On the other hand, the countries that suffered in the late 1990s dollar bull run, such as Thailand, South Korea, Malaysia, and Russia, learned their lesson from last time around, and came into this cycle with a ton of foreign-exchange reserves and less dollar-denominated debt, which is the opposite of the situation they all had in the 1990s. They were fortified against a strong dollar this time around. By summer 2019, the Fed began cutting interest rates in the face of slowing economic growth. In September 2019, the overnight lending rate in the US banking system spiked, leading the Fed to begin supplying repo liquidity, and then eventually to buying T-bills and expanding its balance sheet, which marked the end of quantitative tightening. This was an example of the system correcting itself, or more specifically, forcing US policymakers to correct it. A strong dollar contributed to slowing global GDP growth, including in the United States, which led the Fed to cut rates. And, with foreigners not buying enough Treasuries for years due to the dollar being so strong, the US domestic balance sheets became increasingly stuffed with Treasuries and couldn’t keep buying more, so the Fed had to shift from quantitively tightening to quantitative easing to begin buying a ton of Treasuries, which floods the system with liquidity. The dollar began weakening again from there, as expected. However, the COVID-19 pandemic hit in early 2020, which halted global trade and contributed (along with a structural oil oversupply issue) to a collapse in oil prices. The dollar quickly spiked, foreigners began outright selling Treasuries and other US assets to get dollars, causing the Treasury market to become very illiquid and “ceasing to function effectively” as the Fed described it. In response to this, the Fed cut rates to zero and performed massive quantitative easing, and the US federal government performed massive fiscal stimulus. The dollar began weakening again, and from there, it remains to be seen what the next chapter will be. The Fraying of the Petrodollar System As I explained before, each global monetary system begins to suffer from a form of entropy, where order falls into disorder as inherent flaws in the system manifest themselves over time. For the Bretton Woods system, the flaw was the persistent reduction in US gold reserves against a growing amount of external liabilities, leading to an eventual inability to maintain the convertibility of dollars into gold. For the petrodollar system, the flaw is the persistent trade deficits that the US has to run with the rest of the world in order to supply the world with dollars that they must use for energy pricing. The US ends up outsourcing large portions of its industrial base, and in the process builds up a massive deficit in its net international investment position as the foreign sector owns an increasing share of US assets. In other words, the flaw in the Bretton Woods system was about the United States’ capital account, whereas the flaw in the petrodollar system is about the United States’ current account. A detailed 2017 paper by the BIS called “Triffin: dilemma or myth?” examines the validity of Triffin’s dilemma from multiple angles, agrees with aspects and disagrees with other aspects, and re-states it and re-applies it in multiple scenarios. In that paper is a good summary of what this updated “current account Triffin dilemma” proposes:

Then in the end, the paper concludes:

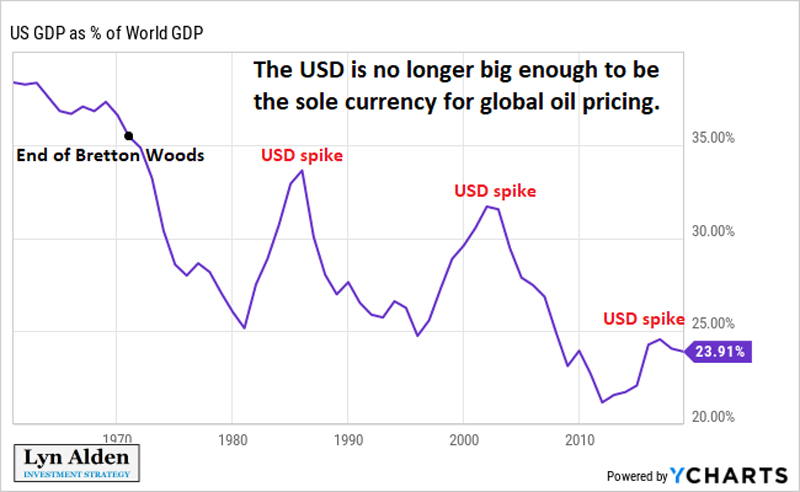

A System Without a Purpose For a while, the petrodollar system made a degree of sense, despite its trade-balance flaws. Unable to maintain gold backing in the previous system, policymakers managed to give order to an all-fiat system. The United States was the biggest economy in the world and the biggest importer of commodities, so our currency was the only one “big enough” to be used for the global oil trade. In addition, as macro analyst Luke Gromen, who in recent years has specialized in analyzing the petrodollar system and the US fiscal situation, has pointed out that the first two decades of the petrodollar system overlapped with the Cold War. So, the system helped strengthen US hegemonic power in a divided world. Love it or hate it, the geopolitical intentions of the system architects were clear. From the 1990s onwards after the Soviet Union fell, as Gromen and others have argued, the system has made less sense, and has resulted in more US military involvement than need be (to put it lightly) as the US indirectly seeks to defend its hegemonic role without a clear direction or identity. In addition, China is now the world’s largest importer of commodities, rather than the United States. It’s challenging to maintain a system of all oil and most commodities being priced worldwide in US dollars if there is a bigger global trade partner and importer of oil and commodities than the United States. The United States still has an unrivaled military reach, but its other justifications for the existing system are diminishing. Shrinking US Share of Global GDP Despite all of this, China can’t replace the United States as the holder of the sole global reserve currency. Not even close. No single country can. And here’s why. In the aftermath of World War II, the United States represented over 40% of global GDP. By the time the Bretton woods system ended and the petrodollar system began, the United States still represented 35% of global GDP. It has since fallen to only 20-25% of global GDP:

And that’s nominal GDP (i.e. priced in dollars), so it is tied in part to dollar strength. If the dollar does have another bear cycle, this would be down to maybe 20%. And based on purchasing power parity (which more closely tracks commodity consumption), the US represents only 15% of global GDP. That’s still pretty good for a country with 4% of the world’s population, but really not enough to maintain the petrodollar system indefinitely. The global energy market, and more broadly international trade, is now too big to be priced primarily in the currency of a country that represents this small of a share of global GDP. Imagine if the entire world tried to price energy exclusively in Swiss francs; there simply wouldn’t be enough of them out there for that to work. The petrodollar situation is not that extreme of course, since the United States is far larger than Switzerland, but the point is, as the US economy represents a smaller and smaller share of global GDP over time, it becomes increasingly unable to supply enough dollars for the world to price all energy in dollars. There’s no country or currency group big enough to do that alone anymore. Not the United States, not China, not the European Union, and not Japan. The United States was uniquely able to do it for decades in the aftermath of World War II as most other nations were decimated and the US share of global GDP became unusually high. However, as the world grows and becomes more multi-polar over time, with no individual country representing a domineering share of global GDP like the US used to, the global monetary system itself also requires more decentralization to work properly. And we’re starting to see that happen. Multi-Currency International Trade As Bloomberg reported this year, exports from Russia to China have quickly de-dollarized over the past few years into a more diverse basket of currencies:

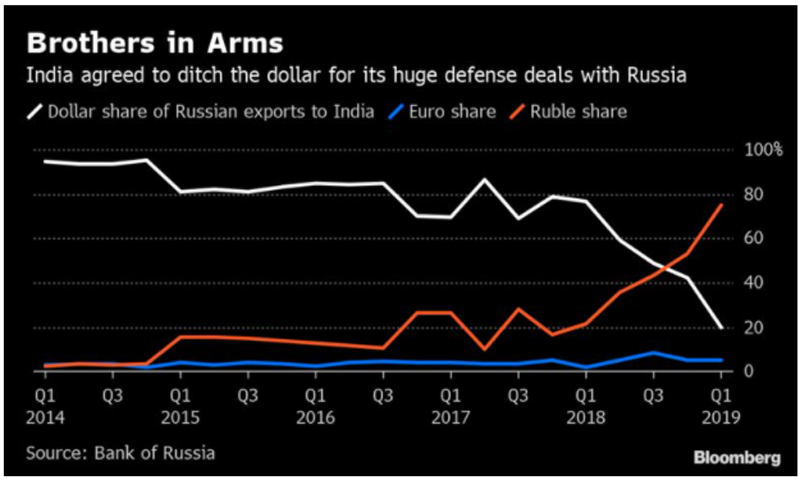

Chart Source: Bloomberg Six years ago, Russian exports to China were over 98% dollar based. As of early 2020, it’s only 33% dollar-based, 50% euro-based, and 17% with their own currencies. And importantly, Russia’s exports are significantly energy-based and commodity-based, which gets to the heart of the petrodollar system. Similarly, the article shows that Russian exports to Europe have become increasingly euro-based as well. Six years ago, Russian exports to Europe were 69% dollar-based and 18% euro-based. Now they’re 44% dollar-based and 43% euro-based. Plus, Bloomberg reported back in 2019 that Russia has been achieving similar results with India as well, with a remarkable drop from nearly 100% of exports to only 20% of exports being priced in dollars:

Chart Source: Bloomberg This isn’t the first time this sort of thing was attempted. Back in 2000, Saddam Hussein began selling oil priced in the newly-created euro. A couple years later, the United States invaded Iraq and removed Hussein from power based on allegations of Iraq possessing weapons of mass destruction. These allegations turned out to be untrue, and Iraq quickly went back to selling oil in dollars. It is disputed to what extent Iraq’s decision to sell oil in euros factored into US decisions to enter the war, but what can be said is this. There is no shortage of malevolent dictators in the world, but that’s the one that we spent 4,500 American soldier lives and $2 trillion in US funds to take out, and that’s without getting into the destruction on the Iraqi side. There is a detailed speech by then-Representative Ron Paul to Congress in 2006 about Iraq and the euro, and broader themes about the petrodollar system as it relates to US foreign policy, including policy towards Venezuela and Iran. Although he’s a controversial political figure, regardless of what side of the political spectrum someone is on, I think that’s a speech worth being familiar with on the historical record. However, when major powers like China, Russia, and India begin pricing things outside of the dollar-based system and using their currencies for trade, including for energy in some cases, the US can’t realistically intervene militarily, and instead can only intervene with sanctions or trade disputes and other forms of geopolitical pressure. The latest hot spot has been multiple rounds and threats of US sanctions for companies involved in the Nord Stream 2 pipeline from Russia to Germany, which if completed would strengthen Russia’s gas supply system to Europe. Both the United States executive branch and legislative branch have been quite fixated on that project. A number of US senators, for example, sent a letter warning of “crushing and potentially fatal legal and economic sanctions” against Germany’s port operator involved with the project. German officials have pushed back, saying such sanctions threaten European sovereignty. Another hotspot has been the US sanctions against Iran. Europe, India, and China all have trade relations with Iran and want to trade with them, and all of them are major energy importers whereas Iran is an energy producer. Europe created INSTEX in 2019, a special purpose vehicle to avoid US sanctions on Iran. The vehicle facilitates trade outside of the SWIFT system and outside of the dollar system more broadly. It has been successfully tested, but barely used. Similarly, India has long had constructive trade with Iran, despite religious/cultural differences that often cause issues between India and its neighbor Pakistan and territorial disputes in Kashmir, but the Iran-India trade partnership has been constrained in 2020 due to a combination of US sanctions and COVID-19. China has a number of strategic energy partnerships and trade agreements with Iran as well, but US sanctions along with COVID-19 also threw a curveball into their trade situation. China is Subverting the Petrodollar System For the past seven years, China has been using the petrodollar system against the United States. The petrodollar system encourages mercantilist nations to run trade surpluses with the United States and recycle those dollars into buying US Treasuries, but after a while of doing this, China started taking their dollar surpluses and investing in other foreign assets instead. This topic has been reported on by petrodollar experts like Luke Gromen and others for quite some time, but is not widely followed in the broad sense. Early on in the days of the petrodollar system, Europe and the Middle East were the biggest trading partners and ran trade surpluses with the United States. They accumulated a lot of dollars, and reinvested those dollars into Treasuries. Then, Japan’s quick rise led them to become the next big trading partner and center of global growth. They took the baton and ran big trade surpluses with the United States, and again, reinvested those dollars into Treasuries. Then, with the stagnation of Japan and the rise of China, China became the biggest trading partner with the United States, ran big trade surpluses with the United States, and reinvested those dollars into Treasuries. All was well, except for the Americans who wanted to make things, or any folks, American or foreign, who were on the wrong side of military adventurism. The wheels of the petrodollar system kept functioning. But then, China broke the wheels. Back in 2013, China declared that it was no longer in their interest to keep accumulating Treasuries. They kept running huge trade surpluses with the United States, and had dollars still coming in, but they would no longer recycle those to fund US fiscal deficits by buying Treasuries. As per the linked Bloomberg article:

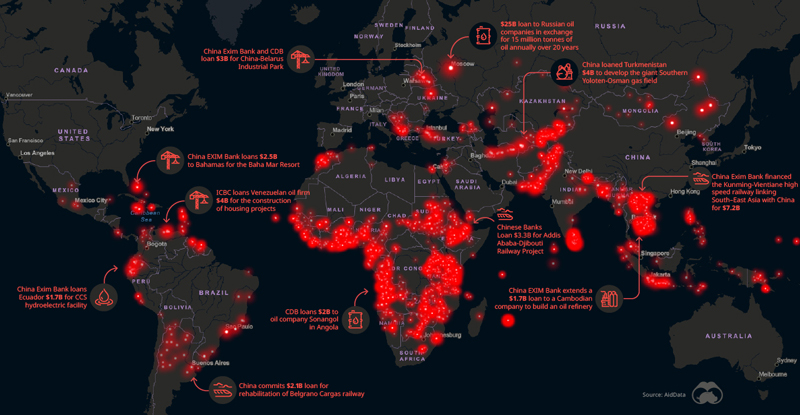

Indeed, China now holds fewer US Treasuries than they did seven years ago, even though they kept increasing their trade surplus with the United States through 2018. Instead, they launched the Belt and Road initiative in 2013. China began aggressively lending dollar-based loans for infrastructure projects to developing countries in Asia, Africa, Latin America, and Eastern Europe, and providing their infrastructure-building capabilities as well, because infrastructure has long been one of China’s technical specialties. Many of those foreign loans, if defaulted on, mean that China gains ownership of the infrastructure. So, whether the loans are successful or not, China gains access to commodity deals, trading partners, and hard assets around the world. Here’s a map of global Chinese funding (and here’s a bigger view).

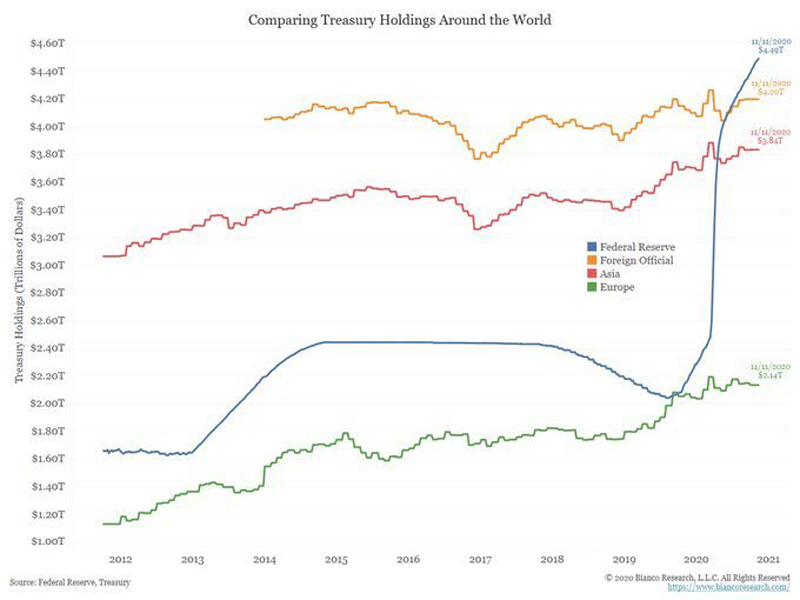

Chart Source: Visual Capitalist So, the US runs big trade deficits with the rest of the world (and especially China), but now rather than funneling those dollar trade surpluses back into financing US fiscal deficits, China uses its incoming dollars to finance hard asset projects around the world, and increase their global reach. At this stage, instead of just blue-collar labor in America being hurt by the system, the geopolitical ambitions of United States hegemony are also subverted. As far as Americans were concerned, for 40+ years the petrodollar system used to work for the top half of the income spectrum but not really the bottom half, and now it neither particularly works for the top half nor the bottom half. It’s now a system without a purpose. There’s an old quote from Charlie Munger that goes, “show me the incentives and I’ll show you the outcome.” As clever as the design of the petrodollar system was in the 1970s, China’s subversion of the fraying petrodollar system was just as clever. The flaws of the system basically ask for it to happen eventually, and it’s mathematics and Triffin’s dilemma coming home to roost. From a geopolitical standpoint, we can see why China would want to do it. The western powers severely damaged China in the 1800s Opium Wars which contributed in part to the next 150 years of Chinese destabilization and stagnation, and now having regained a degree of organization and power, China isn’t playing nice with the global system as structured by those western powers. Chinese officials have said on numerous occasions that their reliance on the dollar system is a security risk for them. Having surpassed the United States as the world’s largest trading partner and world’s biggest importer of commodities, China increasingly has an interest in being able to acquire commodities and perform global trade without dollars, which as we see with trading partners like Russia, or with China’s yuan-based oil futures contract, they’re increasingly able to do with small steps at a time. At the same time, the United States faces increasing populism in its own country, as the persistent trade deficit becomes an increasingly political issue to fix. Plus, US officials have routinely pointed out the security risk of having so much critical supplies made outside of the country, which became even more apparent during COVID-19. The trap solution is for US policymakers to try to narrow the trade deficit by getting other countries to buy more American goods, but that’s like putting a Band-Aid on a gunshot wound. The deeper problem is that the global monetary system as currently structured simply doesn’t work well with that goal; it’s inherently designed at its core to run with persistent trade deficits to get dollars out into the world and enforce dollar-only global energy pricing. Back on March 2, 2018, President Trump tweeted that “trade wars are good and easy to win”. Since then, the US trade deficit increased, rather than decreased. Trade wars are very difficult for the US to win within the petrodollar system as currently structured. The US can close its trade deficit over time, but not without changing the global monetary system from its current structure. So on one hand, US policymakers do what they can with military action or sanctions against those that would sell energy in a currency other than dollars, and try to maintain the dollar lock on global energy markets wherever possible. On the other hand, the US wants to fix its deepening trade deficit, even though that trade deficit is what gets dollars out into the world for use by countries to sell oil in dollars or acquire dollars to buy oil. It’s an incoherent strategy, and it runs deep in US political culture, rather than tied to any one politician. Meanwhile, the entropy of trade deficits chips away at the existing system from within, China uses the system against the system’s owner, populism rises in the US and elsewhere, and countries throughout Eurasia gradually build non-dollar payment channels. Eating Our Own Cooking As of this year, the US Federal Reserve (blue line) now owns more Treasuries than all foreign central banks combined (orange line):

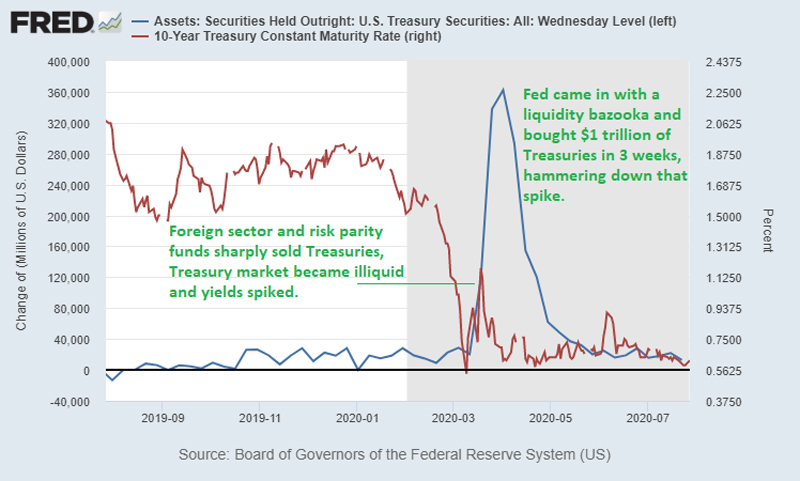

Chart Source: Bianco Research That’s not exactly how the “global reserve” currency is supposed to work. It’s like a restaurant chef eating her own cooking more than her customers do. This is what other non-global-reserve countries look like. Within one year, the Fed went from owning half as much Treasuries as foreign central banks combined, to more than them combined. As previously described, countries can only keep buying Treasuries if global dollar liquidity conditions are good. A strong dollar halts foreign accumulation of Treasuries. In addition, any impact to trade, such as a pandemic and associated economic shutdowns that crater oil demand and import/export volumes, threatens that whole system. And China isn’t recycling dollars into Treasuries for aforementioned strategic reasons. As it relates to the Treasury market, in addition to not buying much Treasuries over the past five years of this strong dollar environment, some countries began rapidly selling Treasuries in March and April of this year at the height of the global shutdown and liquidity crisis. Leading into the pandemic, long-duration Treasuries rallied as investors flocked into them and drove their yields down, but at the worst point in the liquidity crisis as the dollar index spiked to 103, even Treasuries sharply sold off. The Fed described the problem in their emergency March meeting and their subsequent April meeting. Here’s March:

And here are two snippets from April:

And here’s what they did. The red line is 10-year Treasury yields. The blue line is the weekly rate of Treasury security purchases by the Fed.

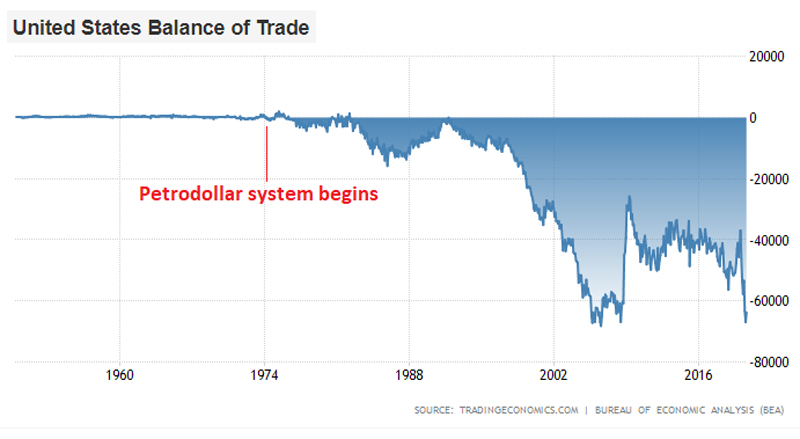

Chart Source: St. Louis Fed More importantly than the yield spike itself in March was the fact that the Treasury market became illiquid, with wide bid/ask spreads. It wasn’t functioning properly, let alone yields going up. Since then, the Fed has gradually tapered their Treasury security buying program from those extreme $75 billion-per-day highs, although they are still buying at a rate that rivals previous instances of QE, at $80 billion worth of Treasuries per month. The Fed remains the biggest buyer of US fiscal deficits, in other words. The dollar weakened from its March highs, but is still at a relatively strong part in the historic cycle, and as such, the foreign sector isn’t recycling many of their dollars into accumulating Treasuries. That’s what happens when there is $13 trillion in dollar-denominated debt in the world, and plenty of dollar-funding needs, while dollars simply aren’t being supplied in sufficient quantity to the world. Foreigners begin selling some of their $42 trillion in dollar-denominated assets to get dollars, and that crashes US markets along with everything else, which forces the Fed to step in, print dollars to buy what they sell, and open dollar swap lines to foreign central banks, until sufficient global dollar liquidity is restored. Triffin’s Dilemma Unfolds Ultimately, this gets back to the question of whether the United States should even want to try to maintain the petrodollar system, if it could. As previously shown, the US trade balance is a mess:

Chart Source: Trading Economics The US net international investment position has absolutely collapsed, with the US having gone from being the world’s largest creditor nation to the world’s largest debtor nation:

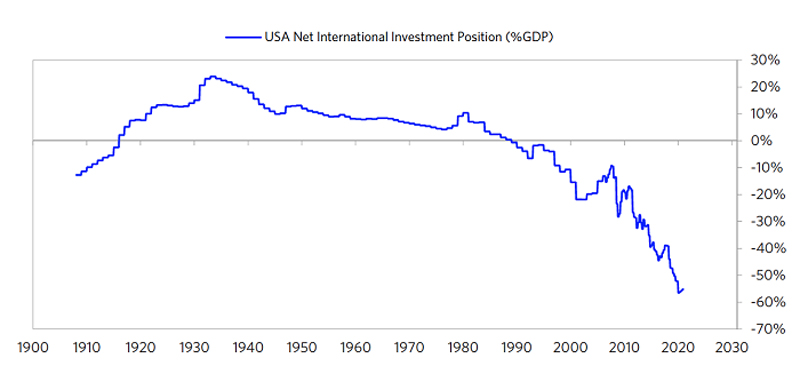

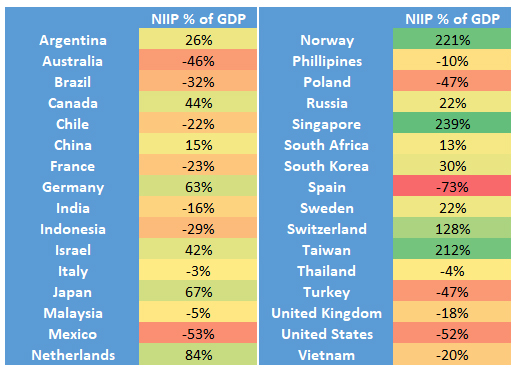

Chart Source: Ray Dalio, The Changing World Order The net international investment position of a country measures how much foreign assets they own, minus how much of their assets that foreigners own, and the chart above shows it as a percentage of GDP. As of this year, the United States owns $29 trillion in foreign assets, while foreigners own $42 trillion in US assets, including US government bonds, corporate bonds, stocks, and real estate. This is a result of accumulated US trade deficits (and on the other side, accumulated trade surpluses by the foreign sector), and now puts the US at one of the weakest positions in the world in terms of this metric. This was as of 2019, and it has gotten worse since then:

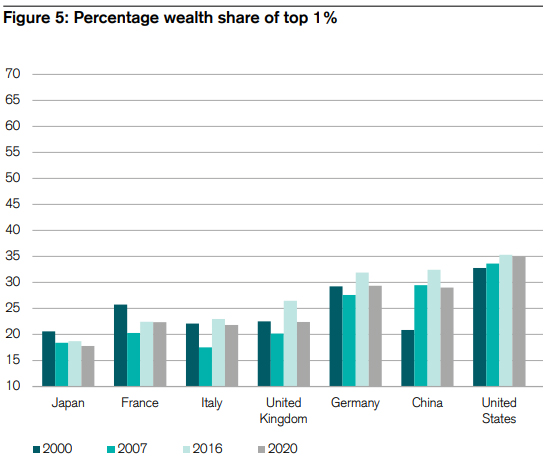

Data Sources: IMF and various central banks Wealth concentration in the US is now higher than just about any other developed nation:

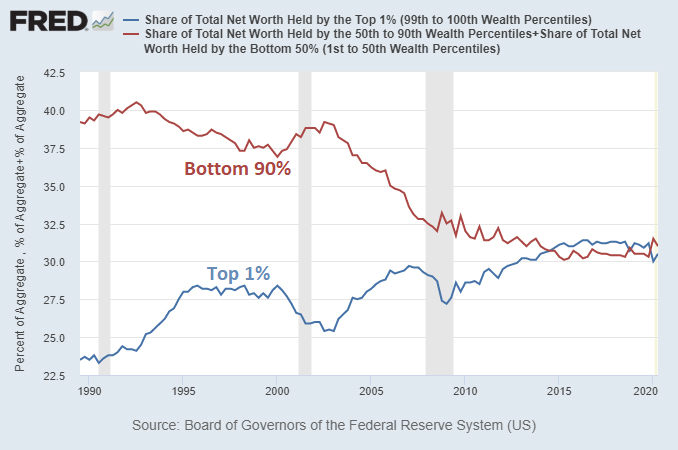

Chart Source: Credit Suisse 2020 Wealth Report The top 1% have as much as the bottom 90%, which is a lot more concentration than 30-40 years ago:

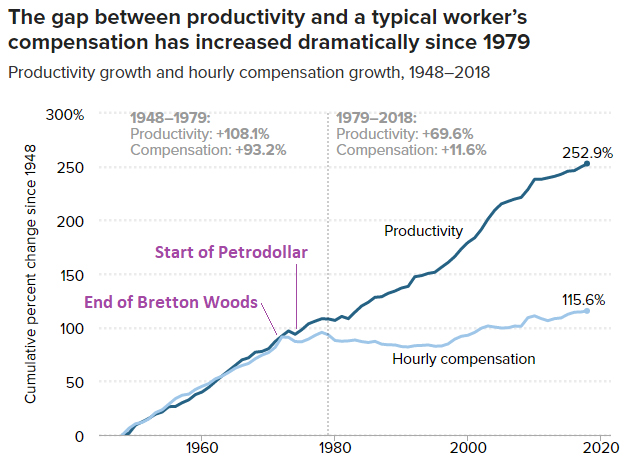

Chart Source: St. Louis Fed The United States is ranked #27 in the world for social mobility, which puts it at the bottom range of developed countries. For Americans, their family of birth dictates their lifetime economic potential more-so than other advanced peers. With a few exceptions, we have to go down into emerging/developing markets to find lower social mobility scores than the United States has. Median American wages decoupled from productivity since the 1970’s, and that gap was arbitraged by those at the top thanks to offshoring/automation:

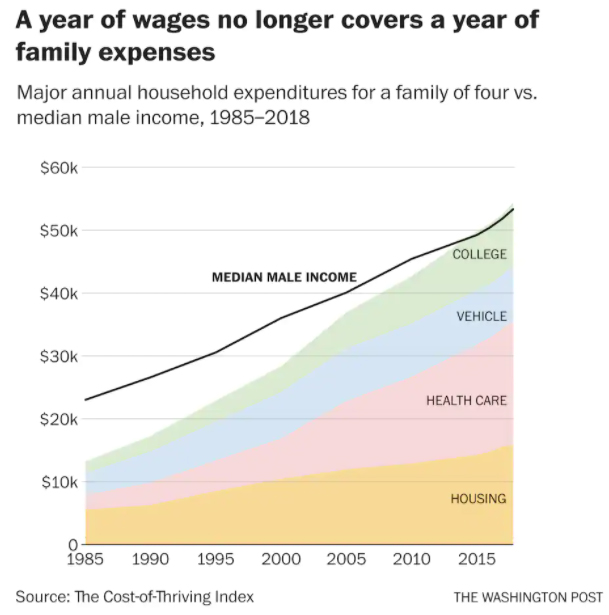

Chart Source: EPI Now, the median American male has trouble affording the expenses for a family that he could easily afford decades ago. Either an above-median income is required, or two incomes are required, because the median income just doesn’t support a family like it used to:

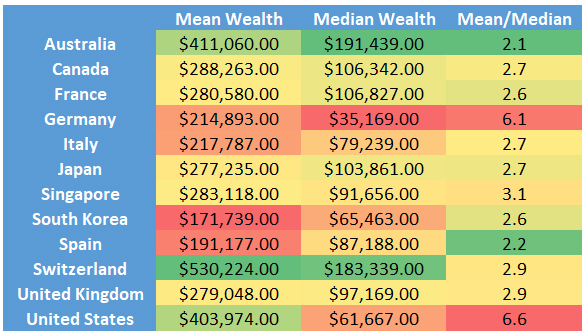

Chart Source: Washington Post, Oren Cass Meanwhile, there has been a rapid increase in CEO pay over the past four decades. CEOs used to make 20x as much as the average worker in 1965, and that ratio moved up to 59x by 1989, 122x by 1995, and in recent decades has been well over 200x as much as the average worker. According to the 2019 Credit Suisse Wealth Report, although the United States is wealthy per capita, because that wealth is so concentrated, the median American net worth (which represents the 50th percentile- the middle person on the spectrum) is actually lower than the median net worth of most other advanced countries. We squeezed our middle and working classes harder than most other countries:

Data Source: Credit Suisse 2019 Wealth Databook It’s no wonder that populism is on the rise, both from the right and the left. Folks sense something isn’t working but differ on what they think the causes and solutions are. Basically, the petrodollar system and the associated fiscal policy is fraying under its own inherent flaws over decades, which again gets back to the Triffin dilemma that to maintain a global reserve currency, you need to export an increasing amount of your valuable assets like gold reserves or your industrial base. That cost inherently makes these sorts of systems long-lasting but not permanent. At first, having the global reserve currency is an exorbitant privilege, because the benefits of hegemonic power outweigh the costs of maintaining the system. Over time, however, the upside benefits stay relatively static, while the costs keep compounding over time, until the costs outweigh the benefits. And from there, the value of the system depends on who you ask. Folks who are often on the higher end of the income spectrum who worked in finance, government, healthcare, or technology benefitted from this system, since they obtained many of the benefits of globalization and none of the drawbacks. Folks who are often on the lower end of the income spectrum, specifically those that make physical things, are the ones that benefitted least and gave the most up, since their jobs were outsourced and automated at a faster rate than other developed countries. But now with China also undermining the structure of the system, even the geopolitical/hegemonic benefits for the political class are subverted as well. As the system frays, it’s easy to point to external nations as the cause of this fraying. When they begin pricing things outside of the dollar-based system, or employing mercantilist currency policies, or building pipelines, or deciding to do something with their dollar surpluses other than reinvest them in US Treasuries, it can seem as though they are undermining an otherwise sound system. In reality, those external actions are a symptom of the more underlying flaws in the system: the fact that the United States is no longer big enough as a share of global GDP to supply enough dollars to fund global energy markets and global trade, the fact that the United States has to run persistent trade deficits to get dollars out into the system, and the fact that an all-fiat global currency system incentivizes mercantilist currency manipulation by many countries to generate trade surpluses against the US wherever possible. The Intermediate-Term Outlook Whether there are major changes to the system or not, I think probabilities lead to a weakening dollar in the years ahead. In other words, another down leg on this dollar chart, even if the overall system structure doesn’t change much:

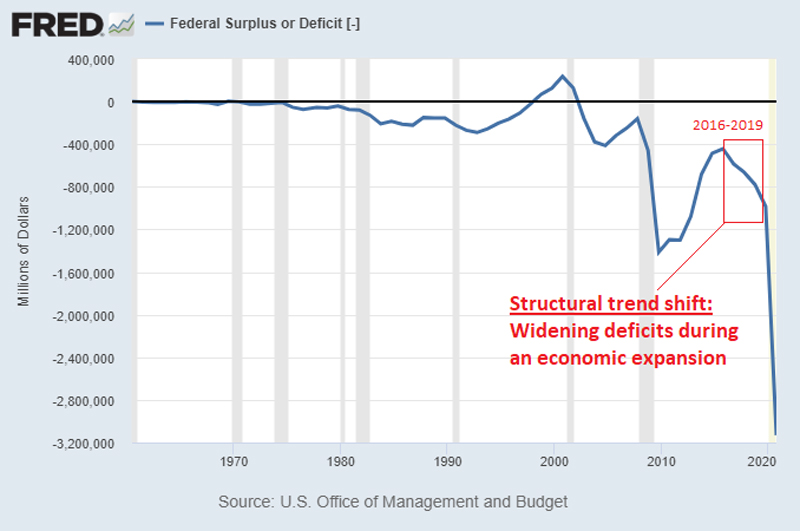

Chart Source: StockCharts.com The Dollar vs Other Currencies Some people ask why would the US dollar weaken more than other major currencies if all of them are printing a lot of money. What causes these big bear markets in the dollar? In other words, just because the US Federal Reserve turns dovish, doing plenty of QE and keeping interest rates at zero, why would the dollar be weak vs the euro, yen, pound, or other countries that are acting similarly dovish? It’s easy to argue that it should weaken against hard assets (and indeed, that’s probably the easier long-term trade), but why should it weaken vs other fiat? The first answer to that question has to do with magnitude. All major countries are acting similarly, but not at the same magnitude. US fiscal deficits as a percentage of GDP were larger than most advanced peers before the pandemic hit, and are larger than most advanced peers during this pandemic as well. Here’s a chart I had in my November 2020 newsletter about the US federal deficit, showing that it’s the first time in modern history where the United States had a rising deficit (both in absolute terms and as a percentage of GDP) during the later years of an economic expansion:

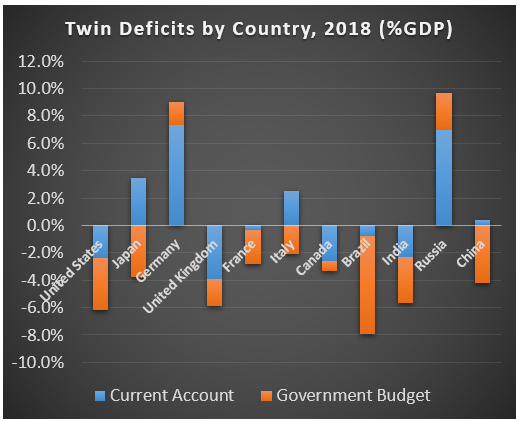

Chart Source: St. Louis Fed In addition, while Japan and Europe and China have positive trade balances and current accounts, the US has the aforementioned Triffin dilemma issue of structural trade and current account deficits. Here’s a chart I put together in 2019 using data from late 2018, showing that pre-pandemic, the US had the biggest twin deficit among major developed nations:

Data Source: Trading Economics, various central banks So, when US monetary policy also turns dovish as it did in 2019, the dollar has plenty of room to decline. The second answer to that question has to do with valuation. Suppose a value stock had a price/earnings ratio of 10x, and you expect 5% earnings growth this year. And suppose a growth stock had a price/earnings ratio of 30x, and you expect 15% earnings growth this year. What happens if, despite expectations, the value stock only grows earnings by 4%, and the growth stock only grows earnings by 7%? Due to high valuation and the bigger relative gap vs what was priced in, the overvalued growth stock has a lot further to fall in that scenario than the value stock. The dollar is specifically propped up in a bullish cycle due to tons of offshore dollar-denominated debts, structural scarcity for dollars outside of the United States to service those debts, and a decade of capital inflows to the United States. Now, in an environment where all countries including the US create massive liquidity and create more currency units, the currency that was specifically overvalued due to scarcity relative to required demand (the dollar) is the one that has the furthest to fall, because that specific scarcity/liquidity problem that was propping it up gets addressed. Trade deficits imply an overvalued currency (too much importing power, uncompetitive export pricing), and trade surpluses imply an undervalued currency (too little importing power, and overly competitive export pricing). Mercantilist countries can manipulate their currency to keep those trade surpluses open for a while, and the global reserve currency can go decades with trade deficits, but when monetary policy stops pushing against these inherent trade forces, exchange rates have a tendency to push back towards the direction of balanced trade. When the US is in a strong dollar cycle, has a big trade deficit, and then cuts interest rates and shifts from quantitative tightening to quantitative easing, the dollar has plenty of room to weaken compared to currencies of developed nations that already have trade surpluses (i.e. undervalued currencies), even though the dollar is the global reserve currency. We saw that happen this year, so the question is whether it will continue. Plus, US stocks are more expensive than many other nations, even when adjusting for sector differences. So, if US equity indices can’t continue their period of outperformance, capital could start flowing elsewhere, which also weakens the currency. Usually, due to equity valuations and shifts in policy, whatever equity region outperformed in one decade tends not to be the same one that outperforms in the next decade.

Chart Source: iShares Risks to this view: Within a multi-year outlook, there will likely be occasional counter-rallies where the dollar outperforms other currencies, or even outperforms gold, despite being within a declining trend. So, maintaining a clarity of time horizon is important. Similar to how the pandemic was a 6-month curveball towards my view of a weaker dollar in the first half of 2020, there are other tail risks that could temporarily derail the outlook as well. An economic slowdown this winter, before the vaccines achieved widespread penetration and change consumer behavior? A sovereign debt or banking crisis in Europe, centered on southern European countries? A famine in China? A currency crisis in a big emerging market like Brazil? Some sort of unexpected military engagement between major powers? Any of those outcomes could cause a temporary spike in the dollar, similar to the spike that occurred in March. An outlook can be firm for structural reasons, but still needs to adapt as data change. That’s why I write newsletters and research reports regularly; things change. In terms of inevitability, the eventual issue with southern European sovereign debt is one that should cause investors a lot of concern in the long run. The euro has structural issues of its own, with a monetary union but no fiscal union, although that’s a subject for another article. The euro has a lot of problems, but being overvalued isn’t one of them. In this strong dollar period, Europe has run persistent trade and current account surpluses:

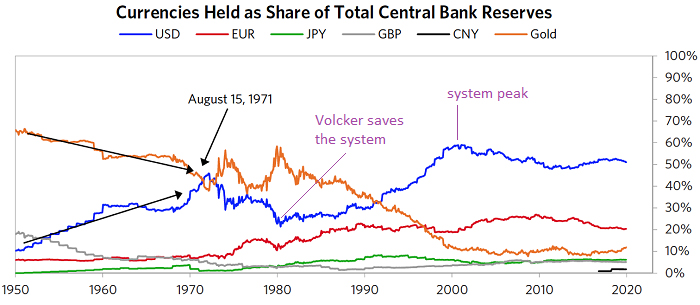

Chart Source: Trading Economics A weaker dollar vs the euro, if it happens, could indeed reduce Europe’s trade surplus with the United States. But the corresponding emerging market boom that would likely come along with a weaker dollar, would open up other trading avenues for them as well. The Long-Term Outlook The further we look out, the more we can think about a structural shift away from the petrodollar system itself rather than just another dollar cycle within the system. The Slow Restructuring Option A structural change could happen gradually, as it already is happening. If an increasing share of global trade, particularly within Eurasia and particularly regarding energy and commodities, keeps shifting towards euros, yuan, and rubles and away from the dollar, then the system can become more decentralized over time. In fact, we could argue that the petrodollar system peaked in 2000, has been in a steady-state for the past 20 years since then, and is now potentially facing decline. This chart shows currencies held as a share of total central bank reserves:

Chart Source: Ray Dalio, The Changing World Order, purple annotations by Lyn Alden Another way of looking at it is that it peaked in 2013 when foreigners owned a record high percentage of US debt, and China declared that it was no longer in their interest to keep accumulating Treasuries. Since then, the percent of Treasuries owned by the foreign sector has diminished. As a base case, I expect this gradual outcome to continue happening, whether the United States participates or not, as various major powers continue to increase their usage of non-dollar payment systems over time, and an increasing percentage of US federal debt becomes owned by the Federal reserve and the US commercial banking system. The new RCEP trade agreement between many Asia Pacific nations, which creates the largest trade bloc in history, could further accelerate that trend, and new technologies including blockchains and domestic government-issued digital currencies, open up novel opportunities for new payment networks as well. The Fast Restructuring Option On the other hand, a structural change could happen with a shock and stepwise change, like the end of the Bretton Woods system. This can happen in a few ways, but becomes more probable if the United States decides to actively promote a change rather than defend the status quo. On the legislative side, the United States could reverse some policies that I described in “The Big Tax Shift” which would make onshore labor more competitive. This would include things like cutting payroll taxes or performing similar measures, and re-arranging other spending and taxing priorities, to emphasize some degree of industrial onshoring. On the Treasury/Fed side, the easiest way would be through foreign-exchange reserves. Countries manage their currencies primarily with their foreign-exchange reserves, which consist of foreign currencies in the form of sovereign bonds, and gold. In some cases they also own foreign equities and other assets. These foreign-exchange reserves held by central banks around the world have multiple purposes:

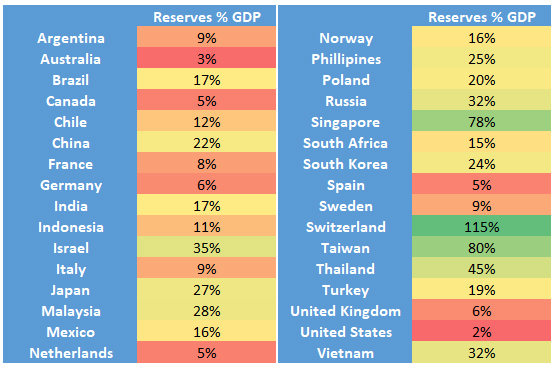

Because the dollar is the axiom of the current global monetary system, Treasuries are the biggest component of most countries’ foreign-exchange reserves. The US itself doesn’t have much foreign exchange reserves. Emerging markets often have the biggest reserves, since they need them the most, but a handful of developed nations also have huge reserves as well, and just about every country has more reserves as a percentage of GDP than the United States. This chart shows foreign-exchange reserves as a percentage of GDP for dozens of countries, as of spring of this year when I assembled it. In terms of comparative magnitude for most countries, it hasn’t changed much since then:

Data Source: TradingEconomics.com, various central bank websites For the United States, this number includes our official gold reserves at this year’s gold prices, and gold indeed represents the vast majority of US reserves. For Eurozone countries, the European Central bank also has another layer of reserves as well in addition to the individual country reserves on the chart, so the numbers on the chart for Eurozone countries mildly understate the total direct and indirect reserves relative to GDP for the euro. The US could devalue the dollar any time it wants by printing dollars to buy foreign assets or gold, and build more sizable foreign-exchange reserves in the process, which would be in line with other peer nations. With a nominal GDP of over $20 trillion, for each 5% of foreign exchange reserves as a % of GDP they want to have, the United States would need to print and spend over $1 trillion. So, adding a 10%-of-GDP reserve would cost over $2 trillion, especially as the dollar devalues in the process of building that reserve. That’s one of the potential endgame scenarios for how the United States could choose to abruptly end this system as currently structured. It could decide to cease being the axiom of the global monetary system and simply move to being the biggest individual player in the system by acquiring foreign-exchange reserves, devaluing its currency in the process, adopt various fiscal changes to promote on-shoring, and begin promoting rather than fighting the trend of energy and other commodities being sold in a handful of major currencies around the world rather than just the dollar. In doing so, it would sacrifice some of its international hegemony in favor of more industrial competitiveness and higher domestic economic vibrancy. The dollar would still be “a” reserve currency, and still the largest individual one, but wouldn’t be “the” reserve currency like it is now. Risks to this view: Big macro shifts have a tendency to take longer to play out than logic would suggest. These sorts of things don’t change easily, so predicting a sharp change to the global monetary system just around the corner is always going to be improbable, even if one day, one of those improbable things happens. I’m focusing on monitoring the slow option: the continued progress or setbacks of non-dollar exports/imports between major powers, particularly regarding energy and other commodities. I prefer “win/win” bets for long time horizons. Scarce assets, particularly industrial commodities, are historically cheap. Plenty of high-quality equities inside and outside of the United States are reasonably-priced. Alternatives like Bitcoin also offer asymmetric outcomes even with small allocations. At this stage in the long-term debt cycle, currency devaluation of some kind or another is likely in the 2020’s decade, both for the dollar and other currencies, so having exposure to scarce assets could do well, regardless of what the global monetary system looks like at any given time based on the decisions of policymakers. What the Next System Looks Like What the next system will look like is an open question. I’ve seen multiple proposals. Whatever form it takes, it’ll be decentralized in the sense that it won’t be completely tied to any one country’s currency, since no country is big enough for that anymore. It’ll be based around neutral reserve assets, and/or a more regional-reserve model based on a handful of key country currencies, with an expanded variety of payment channels. Decentralized Energy Pricing At the heart of all of these systems would be the fact that the dollar would no longer be the world’s only currency for energy pricing. The euro, yuan, and perhaps a few others, or a neutral reserve currency, could be used in trade agreements to buy oil, gas, and various commodities, which unlocks the prospect for more global trade and reserve holdings in those currencies. Even without a major structural change or the formal adoption of a new system, this is already gradually emerging throughout Eurasia, as shown earlier in this article as other large currencies are increasingly used between trading partners including for energy. And as I previously described, the United States, if it felt the current system was no longer in its best interest, could accelerate this shift at any time by building foreign-exchange reserves and/or supporting other non-dollar payment systems for energy and commodities rather than opposing them. In this sense, the world moves from a “global reserve currency” to a handful of “regional reserve currencies”. It doesn’t require new technology or new neutral currency units to do this, but it does require the continued development and usage of non-dollar payment systems. In addition, central banks can hold more gold as a reserve asset (which they already have been doing over the past five years) in this scenario, since it’s a neutral currency. Alongside this trend, countries are increasingly launching or researching digital versions of their own fiat currencies, called central bank digital currencies “CBDCs”. In addition to this base outlook, there are some additional layers that could be added on top, described in the following sections. Digital Global Bancor A number of policymakers have resurrected the idea of the Bancor as a neutral reserve currency for international trade, which already exists in diminished fashion as the IMF SDR. Mark Carney, who was Governor of the Bank of England at the time, made headlines in 2019 when he said at the annual Jackson Hole Symposium (in the United States right in front of US Federal Reserve officials) that the dollar is too dominant, and that a new digital currency could be used for international trade to fix some of the problems in the existing system. Coming from the head of the central bank of one of the United States’ closest allies, this was interesting.

Carney also mentioned the Libra in more positive tones than many other policymakers have. Facebook made headlines earlier that year with the proposal of the Libra; a digital currency that would consist of a basket of multiple currencies. The idea of the Libra is basically a stablecoin Bancor issued by a massive private corporation rather than a supra-government entity. It would ironically be a form of centralized decentralization. In other words, it’s a centralized agreement to create and use a unit of trade that is neutral and not tied to any one country’s currency. The problem with this proposal for a global digital Bancor, like a supra-government version of the Libra rather than a privately-issued one, is that it requires a lot of international cooperation and agreement to use it, something like a new Bretton Woods agreement. So, while certainly possible, something like that appears unlikely in such a fractured geopolitical system. Digital Regional Bancors A less ambitious form of a global digital Bancor idea is one or a set of regional Bancors. In other words, suppose that the 15 nations of Asia Pacific’s new RCEP trade agreement agree to create and use some neutral digital currency between themselves. They’re already in a trading bloc, so organizing something like that is potentially more realistic than organizing something on a global scale. And then maybe a few other nations like Russia would be willing to accept that trading bloc’s Bancor as payment for oil and gas and other commodities like they do for the euro? Russia’s biggest commercial bank, Sberbank, has already experimented with blockchain technology and is an avid investor in tech companies. Blockchain technology creates new options for decentralized international payments, linked to a specific fiat currency or basket of fiat currencies weighted by a specific metric. This is the application of software to the relatively outdated global banking system; potentially a much more liquid medium for trade. This year, the largest commodity companies in the world, BHP, Vale, and Rio Tinto, all completed blockchain sales of iron ore to Chinese firms. Singapore banks were involved with the transactions as well. Singapore also hosted the counterparties that tested blockchain transactions with Sberbank of Russia. Technology can lead to all sorts of new payment channels. Referring to the recent exponential usage of existing private stablecoins on crypto exchanges, Nic Carter, the first crypto analyst at Fidelity, co-founder of blockchain analytics firm Coin Metrics, and who works at a blockchain venture fund, had this to say about stablecoin efficiency: