Send this article to a friend:

May

28

2021

|

Send this article to a friend: May |

|

"Own The Internet" - A Bull Case For Ethereum

What if I told you about a business with strong network effects and 200x YoY revenue growth that was preparing to offer a 25% dividend and implement a permanent share buyback program? Is that something you might be interested in? That’s pretty much Ethereum. It’s one of the most fascinating and compelling assets in the world, but its story is obfuscated by complexity and the specter of crypto. Ethereum is so many things at once, all of which feed off of each other. Ethereum, the blockchain, is a world computer, the backbone of a decentralized internet (web3), and the settlement layer for web3. Its cryptocurrency, Ether (ETH), is a bunch of things, too:

Because Ethereum is so much at once, it’s hard to understand. This post is an attempt to help Ethereum be understood. To a group like us, people interested in technology businesses, finance, and strategy, it’s much more fascinating than bitcoin, but that comes with a tradeoff. It’s much harder to grok than bitcoin, and because of that, it hasn’t gotten the mainstream or institutional attention that bitcoin has. Bitcoin is easy. It’s digital gold. It’s a Store of Value (SoV). It just kind of sits there.

That’s its value prop. It’s immutable and the most decentralized asset in the world. It’s the OG and the hardest to attack. At this point, your bitcoin will not disappear overnight (although this post on Tether is illuminating with regards to ways it, and other cryptos including ETH, can be manipulated nonetheless). As long as other people believe in its value, it will continue to be valuable. Technically, upper-case-B-Bitcoin is the blockchain and lower-case-b-bitcoin is the cryptocurrency, but for all intents and purposes, they’re the same. Bitcoin exists to make and track bitcoin. It’s very good at what it does. Ethereum is so much more than a cryptocurrency. It’s a “world computer,” and the “value layer” of the internet. It lets people build apps and products with money baked into the code. If you believe that web3 is going to continue to grow, then you likely believe that over time, Ethereum will become the settlement layer of a new internet. All sorts of transactions, whether they happen on Ethereum, another blockchain, or even Visa, will turn to Ethereum to exchange funds and keep secure, immutable records. A year ago, I wouldn’t have said that. Until the past year, a lot of Ethereum’s value existed in a theoretical state, in the ideas of what might be possible on a decentralized global internet. Personally, I viewed it as a kind of more interesting thing that was kind of like Bitcoin but smaller and maybe higher upside? As a result, after buying ETH for fun in the 2017 run-up, I sold all 15 of my remaining ETH in June 2020 once I broke even. Lack of understanding = weak hands. As you know, I’m an idiot. Even after the recent drop, those 15 ETH are worth over $30,000. I missed ~10x upside. Not as painful as my $2 million bitcoin mistake, but still dumb. To be fair, though, you shouldn’t invest in this stuff unless you understand it, and I didn’t. I’m starting to. Between then and now, a few things have happened that flipped me from moderately curious to both very curious and very bullish:

Right now, Ethereum is at a narrative inflection point, and narrative reflexivity is more important for blockchains than for almost any other company or asset. I’m increasingly convinced that ETH will be one of the best assets to own over the next five years. Here’s the bull case in a nutshell: Owning ETH is like owning shares in the internet. Demand for ETH will go up with increased web3 adoption, while upcoming changes will decrease the supply of ETH and let more value accrue to holders. It’s like a tech stock, a bond, a ticket to web3, and money, rolled into one. To make the bull case clear, we’ll need to understand why Ethereum will survive and adoption will grow, how it actually makes money, and the differences between ETH and a tech stock. We’ll cover:

For ETH to be worth something, and for the bull case to matter, Ethereum needs to survive and grow. It has faced early challenges and competition from purpose-built blockchains, and this past week was scary. Nothing’s guaranteed. To understand why Ethereum isn’t going to die, let’s start with an analogy. Ethereum is the Excel of Blockchains

If you’re going to be bullish on Ethereum, the first thing you’ll need to believe is that it will be around for a long time, and that more and more people will continue to use it, and that other people also believe those things to be true. You’ll be comforted to know, then, that Ethereum is the Excel of blockchains. That’s not exactly right. The analogy breaks down in places. But for our purposes, it’s good enough. Start by comparing it to Bitcoin. Bitcoin is like a database. That’s what a blockchain is -- a distributed ledger of transactions. The Bitcoin blockchain lets people send each other bitcoin (BTC) and tracks who owns which bitcoin at any given time. It can also reward people for securing the database by giving them BTC for turning electricity into solutions to math problems (Proof of Work or PoW). It does one thing really well: track ownership of bitcoin. Bitcoin is kind of like a spreadsheet, and many people compare blockchains to spreadsheets, but that’s not what I mean when I say that Ethereum is like Excel. I mean that the same elements that have propelled Excel for nearly four decades are present in Ethereum, too. It starts with flexibility. Ethereum is a Turing complete, programmable blockchain that lets anyone build full-blown applications using smart contracts. People can build all sorts of decentralized apps (dApps) on top of Ethereum, plugging into the blockchain and the surrounding ecosystem to provide everything from security to identity to payments. Decentralized Finance (DeFi) apps, NFT marketplaces, Decentralized Autonomous Organizations (DAOs), and games and virtual worlds can all be built on top of Ethereum, all fueled by the native currency, ETH. That flexibility is really hard to do. In Excel Never Dies, Ben Rollert and I wrote about Excel’s staying power in a technology landscape that typically sees new products replace old ones every few years. We wrote:

You could replace “Excel” with “Ethereum” and it works perfectly. Ethereum’s early usability challenges are a function of its flexibility. Ethereum is something of a choose-a-phone, and clearly millions of people do want to compose for it. Beyond the product philosophy, there are some specific similarities between the two:

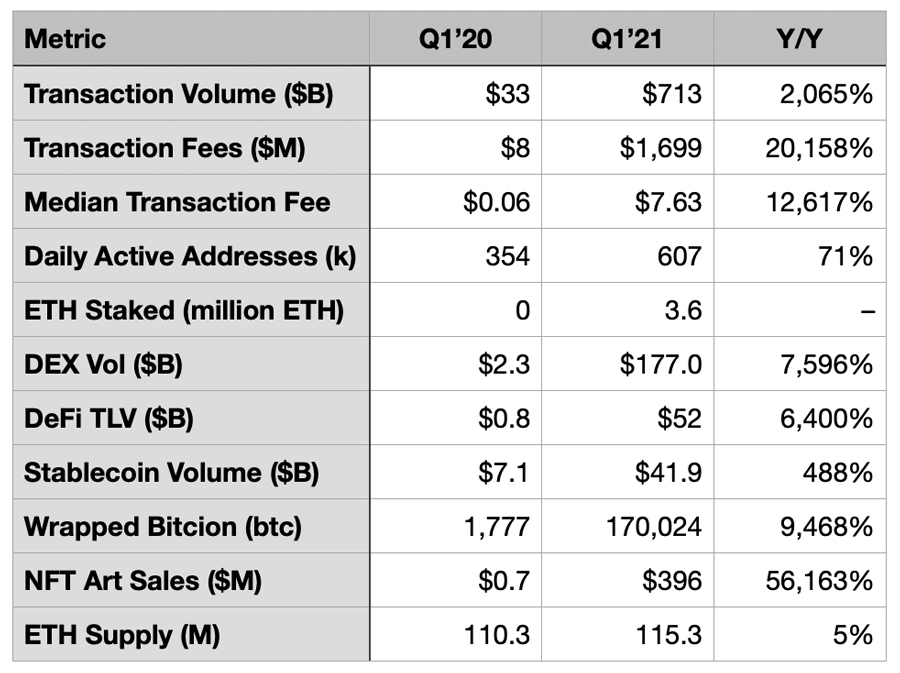

Together, Turing completeness and composability mean that you can build smart contracts to compute anything, and then chain them together to build increasingly complex things, more quickly. It takes time to get the engine revving, but it should move quickly once it’s moving. That’s exactly what’s happening. After years of building in relative obscurity through the crypto winter, facing doubt that there was any actual use for any of this stuff, 2020 and early 2021 saw an explosion of real use cases for the Ethereum ecosystem. In Ethereum Announces First Quarter 2021 Results, James Wang included a Results Table highlighting the year’s progress:

Source: James Wang, Ethereum Announces First Quarter 2021 Results Those are just absolutely massive numbers across a wide range of use cases. This is not one thing. It’s not just “price go up.” It’s a sign of the momentum and composability in the space, where improvements in one area feed directly into improvements in another:

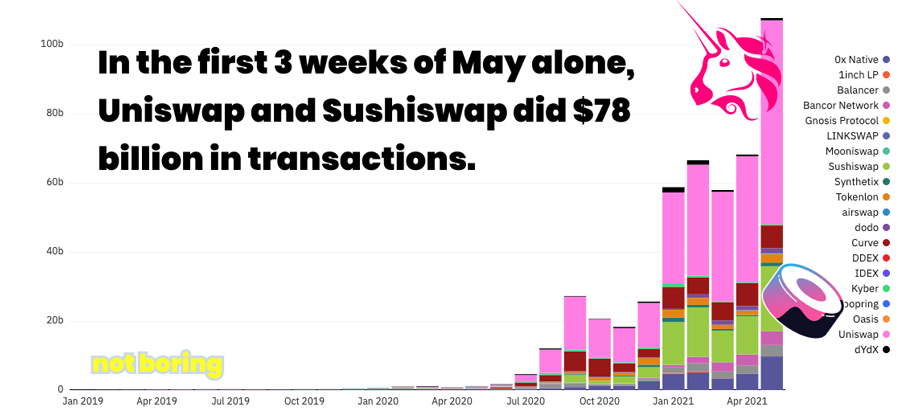

Ethereum usage exploded in Q1, and while NFT sales have slowed, partially as a result of high gas fees and partially because the initial euphoria has died down, DeFi is still going strong:

Source: DeFi Prime From May 1st through May 22nd, just Uniswap and Sushiswap, the two largest Ethereum-based DEXes, handled $78 billion in transaction volume. Q2 will blow Q1 out of the water. Despite the explosion in activity and transaction volume, though, the question remains: what does that mean for ETH? How Ethereum Makes Money I’ve been aware of Ethereum for a long time. I first bought (then sold) ETH in 2017, but it was speculative and I didn’t get it. The big question mark I had with Ethereum was how it made money. How does more activity on top of Ethereum translate into a higher price for ETH? In the near future, the answer will be that more transactions mean higher yields for ETH holders and a decreasing supply of ETH. But that’s not how it works, yet. Let’s start with how it works today, look at the challenges of the current model, the proposed solutions, and what it will look like in the future. (Note: For a more in-depth explanation, listen to Justin Drake on Business Breakdowns) Today Today, when you want to transact on Ethereum, you need to use ETH. There are currently around 116 million ETH, and the price is loosely governed by supply and demand. More transactions on Ethereum means more demand for ETH which means higher price, all else equal. When you transact, say if you send another person ETH, a few things happen:

To keep Ethereum running, it uses a Proof of Work consensus mechanism to trustlessly agree on the state of the blockchain. Bitcoin also uses Proof of Work, that’s where Ethereum got it from, although Bitcoin mining is able to be run on cheaper hardware and has 20x more miners than Ethereum, and is therefore more decentralized. PoW achieves the same thing as your bank account balance going up and someone else’s going down when they send you money, except in the place of a centralized bank, there is a distributed network of miners who agree that these transactions occurred and that all balances are updated. To do it, miners around the world race to solve increasingly difficult cryptographic problems in order to create a new block on the blockchain containing the new transactions. These problems are typically hard to solve -- read: require a lot of energy -- but easy to verify. When a block is entered into the blockchain, the transactions in it officially become part of the record. Miners who successfully create a block are rewarded with 2 freshly-minted ETH (down from 5 in the beginning) and all the transaction fees within the block. Those transaction fees, called gas, are what people pay to submit transactions to be included in the block. When a user sends someone ETH on Ethereum, or mints an NFT, or does any number of things that need to be validated on-chain, they have to pay a gas fee. That gas fee goes towards incentivizing miners to spend the money required, in the form of hardware and electricity, to solve the puzzle and create the block. So currently, the price of Ethereum is based on a combination of supply and demand, and the price it costs miners to secure the blockchain. To participate, you need ETH, and you need to pay the gas. Miners receive ETH in the form of newly-minted supply and your fees. Miners pay for hardware and electricity and taxes, and keep ~5% of their earnings. Today, most of the value accrues to GPU makers, electric utilities, and the government, with the miner’s portion competed down to close to 0. Challenges There are a bunch of challenges with this system.

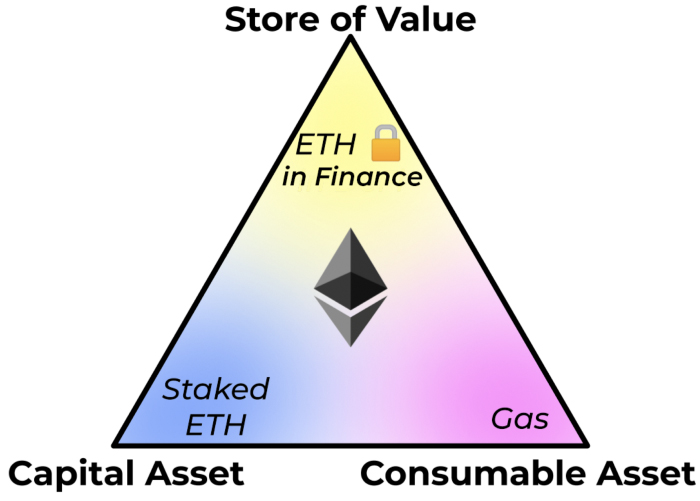

The fact that Ethereum has seen the adoption it has despite all of those challenges is impressive, but they remain real challenges. When I tweeted that ill-fated tweet asking for reasons not to buy ETH, many of the answers centered around one of the above, most commonly the cost of gas and inflation. Plus, increased demand for Ethereum-based dApps -- more DeFi, more NFTs, more DAOs, more games -- means more transaction fees, but those fees don’t really accrue to ETH holders. They leak out of the system to cover miners’ real-world, fiat costs in the Proof of Work process. So today, ETH’s price is based on demand for more ETH, like Bitcoin’s is, and like the dollar’s is. It isn’t tied to revenue, like a company’s is, but it will be soon. Proposed Solutions: EIP 1559 and Eth2One of the things that Bitcoin Maximalists like the most about bitcoin is that you can’t really change it. One of the things they don’t like about Ethereum is that you can change it. It’s not easy, but it’s possible. Two changes are coming to the Ethereum blockchain that aim to fix the challenges mentioned above. EIP-1559 is a proposal that changes how gas fees work by splitting them into two parts -- a base fee and a tip. With EIP 1559, the base fee is burned on each transaction and the miner (and soon validator) keeps the tip. It sounds dull, but it’s huge, because burning will likely make ETH deflationary. Plus, the tip allows people who value better block positions to pay more. That might be important for DeFi participants trying to execute an arbitrage, for example. The proposal was approved in March and will go into effect in July (as part of the London hard fork). Eth2is an upgrade to the Ethereum blockchain itself that will shift consensus from Proof of Work to Proof of Stake and introduce sharding. Eth2 is expected to make Ethereum more scalable, more secure, and more sustainable. The PoS chain, or Beacon Chain, is already live, and is expected to merge with the main chain some time in late 2021 or early 2022. Proof of Stake is a shift in how the network is secured, and who earns rewards. It means that instead of anyone in the world solving math problems to mine blocks, ETH holders can validate block transactions according to how many ETH they hold. Validators secure the network in exchange for yield in the form of tips and newly minted ETH. Ethereum claims that PoS will be more secure because validators will have ETH at stake, which can be destroyed if they try to cheat. Critics claim that staking puts more power into the hands of the people who hold the most ETH, making it less decentralized and therefore less secure. On the scalability side, sharding aims to increase throughput, or transactions per second, by 100x by creating 64 shard chains which validate transactions in parallel. Each shard will only need to validate a fraction of the total chain, instead of every miner needing to validate the entire chain today. Additionally, third-party Layer 2 solutions, like Polygon and Optimism, are already working to speed up transactions and lower fees by essentially batching transactions off-chain and settling on-chain in one transaction instead of many (there are intricacies, but this is close enough). L2 solutions could increase throughput another 100x, and combining Eth2 and L2 solutions could lead to a 10,000x improvement if the theory plays out in practice. Taken together, EIP 1559 and Eth2 could be revolutionary for ETH holders because they improve performance while dramatically altering where value accrues in the Ethereum ecosystem. The Future: Triple-Point, Ultra Sound Money In 2019, David Hoffman wrote an essay called Ether: A New Model for Money. If you want to go deeper, you should read it. In it, he cites a 1997 Journal of Portfolio Management paper by Robert Greer, What is an Asset Class Anyway?, which says that there are three asset superclasses:

Hoffman argues that Ether, as Turing complete programmable money, can be all three once EIP 1559 and Eth2 go through, and further, can be all three at the same time. He calls this triple-point money, referring to the concept in thermodynamics that at the exact right temperature and pressure, a substance can exist as a solid, liquid, and gas at the same time. How they occur simultaneously with Ether is beyond the scope here, what’s important to understand is the three phases in which Ether can exist:

Source: David Hoffman So how does ETH make money? Where does value accrue? There are a lot of ways to earn money on your ETH -- staking, yield farming, liquidity pools, validating, and more -- but let’s look at the simplest, just owning ETH like you’d own a stock. Once EIP-1559 is implemented and the Eth2 merge is complete, value accrues to the people who hold ETH, in a few ways:

We’ll get into the implications of those two things in the bull case, but before we do, we need to understand why Ethereum is defensible. Why can’t another L1 just come in and steal its volume? Legitimacy and Lindy Since Ethereum kind of behaves like a business, with the added benefit of its own currency, we can analyze its strategic position like we would a business. It benefits from brand and network effects. In March, Ethereum co-founder Vitalik Buterin wrote a post titled The Most Important Scarce Resource is Legitimacy, in which he argues that the real value of any crypto asset comes not from actually owning the thing, but from legitimacy. He defines legitimacy like this:

If people believe that other people believe something, it makes more sense for them to believe that thing as well, and act accordingly. On the popular Ethereum podcast Bankless, hosts Ryan Sean Adams and David Hoffman call legitimacy “the theory of everything for crypto.” They listed a series of questions people often ask about the space:

The answer to all of them, according to Adams and Hoffman, is legitimacy. In the post, Vitalik highlights six ways that legitimacy can come about. Two are particularly relevant here:

Performance and continuity create the Lindy Effect, which says that the longer something lasts, the longer it can be expected to last. Something that has been around for a year is expected to be around for another year, but something that has been around for 100 years is expected to be around for another 100 years. This is an observable phenomenon. Amazon is more likely to be around in 30 years than a new startup, our kids are more likely to listen to the Beatles than to Olivia Rodrigo, and our grandkids’ grandkids’ grandkids’ are more likely to read Socrates than Dan Brown. Legitimacy helps explain the Lindy Effect. The longer something has been around, the more people can expect that other people will continue to use it. In the Excel piece, we described a couple more reasons something can be Lindy:

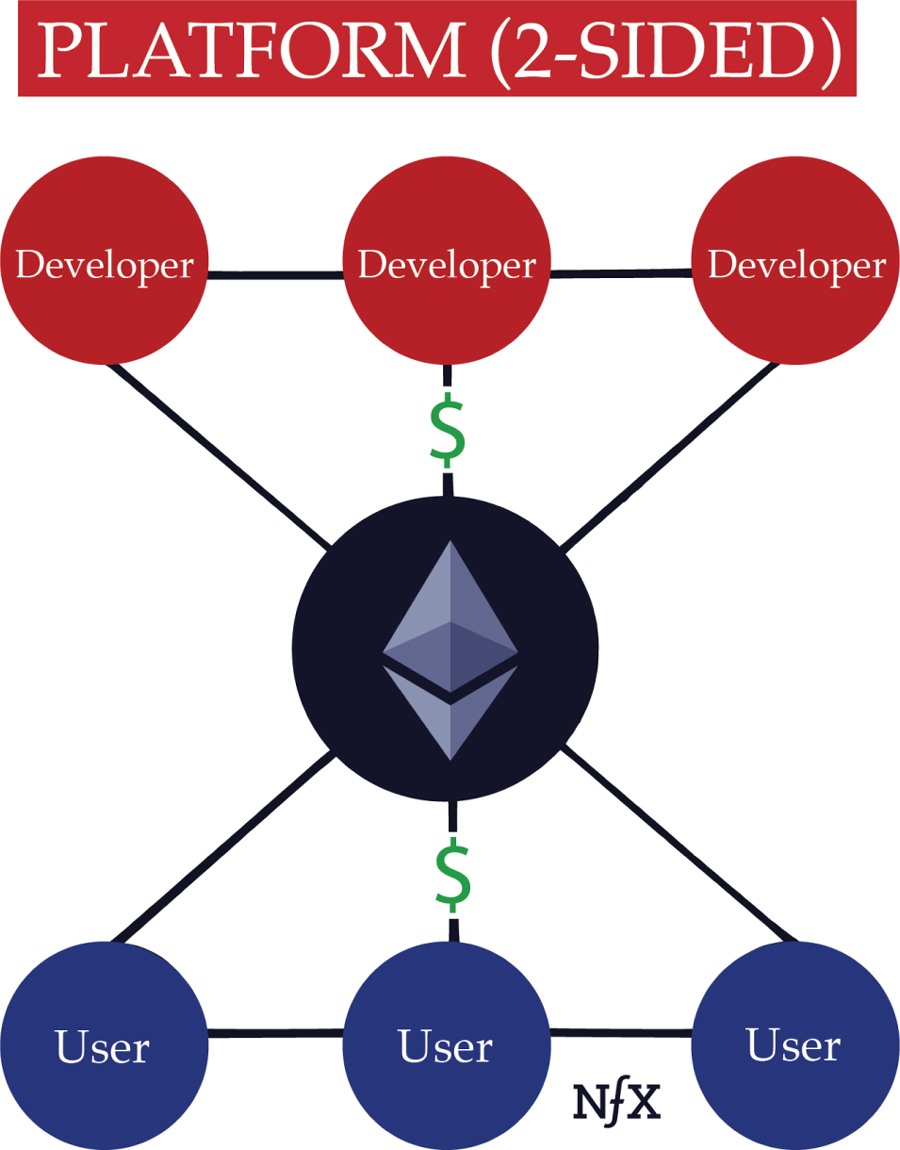

For Excel, the network effect comes from the fact that developers (people building models) know that other people use Excel, so they build their models there, which means that more people need to use Excel, which means that the next person building a model is more likely to use Excel. In Ethereum’s case, more dApps on Ethereum means more users on Ethereum, and more users mean it makes sense for more developers to build dApps.

iOS is an example of Two-Sided Platform Network Effects. The more people who have iPhones, the more likely developers are to make iPhone apps, and the more iPhone apps there are, the more likely someone is to buy an iPhone. In Apple’s case, this network effect is so strong that it takes a 30% cut of all App Store revenues -- whether through the purchase of an app, or through in-app purchases. While they’ve been doing it for years, that model is starting to show cracks. Fortnite-maker Epic Games is battling Apple in the courtroom over the fees, and just this past week, Twitter was atwitter over the fact that Apple will make more from ticketed Twitter Spaces than Twitter itself will. Whether it’s monopolistic or not, Apple’s fees feel extractive. What makes Ethereum’s network effect potentially stronger, and potentially more long-lasting, is that it aligns incentives in a way that traditional software doesn’t. Both users and developers hold ETH -- its the most used token in the Great Online Game -- and benefit from its appreciation. With EIP-1559 and the Eth2 merge, the more ETH is used, the more value accrues to its holders. Additionally, the more ETH is worth, the harder it is to attack. In Ether: A New Model for Money, Hoffman said that fees paid to Ethereum validators act as a wall that protects Ethereum: “The height of the wall is highly correlated with the total fees produced by the network. The height of the wall is the cost of attacking Ethereum.” Solana’sBen Sparango took it a step further when we spoke, explaining to me that it’s in the best interest of everyone involved for the value of the underlying blockchain to exceed the value of all of the dApps built on top of it. If that weren’t the case, bad actors would be incentivized to spend what it takes to attack the blockchain to drain those dApps of their value. The implication is pretty wild: projects that build on top of certain blockchains are actually financially incentivized to support the value of the underlying blockchain in order to secure their project. They don’t pay for AWS or security software; hosting and security is provided by the blockchain. Instead, projects built on Solana may pay out of their Treasury to support the price of SOL, and projects built on Ethereum may pay out of their Treasury to support the price of ETH. That’s a Platform Network Effect unlike any other. It’s hard to imagine an app voluntarily paying to pump up Apple’s stock price. In traditional software, the Bill Gates Line, coined by Ben Thompson, describes what makes something a platform according to Gates:

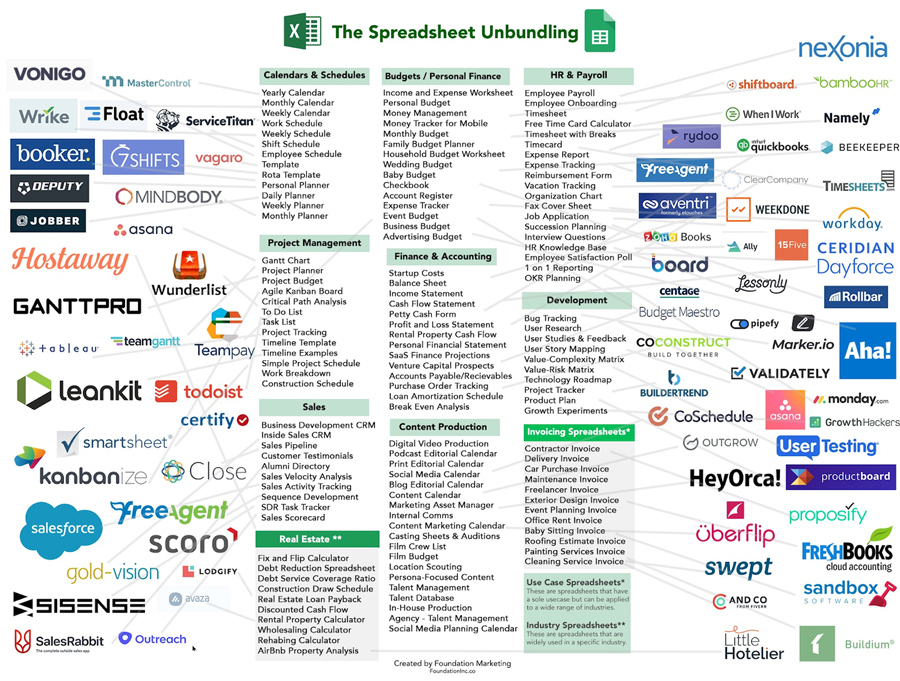

Ethereum has a built-in Bill Gates Line. By owning and using ETH, and making ETH more valuable through usage, the value of everybody that uses Ethereum exceeds the value of Ethereum itself. But they’re also incentivized to make Ethereum more valuable in the process. It blurs the Bill Gates Line by so tightly aligning incentives that the line becomes irrelevant. Importantly, this wall is also why the narrative is so important, and why narrative reflexivity is so powerful in crypto. More demand for ETH doesn’t just increase prices; it shifts some of the burden of security from builders to investors, heightens the wall, makes the network more secure, increases the attractiveness of building on Ethereum, which makes ETH more valuable, heightens the wall further, and so on. It’s a narrative-led flywheel. Definitionally, then, most of the value accrues to Layer 1 and those who hold the Layer 1 tokens. It makes being the Layer 1 on top of which everything is built the prime spot in the value chain. Because of that, and because of Ethereum’s shortcomings to date, a handful of L1 competitors have sprung up that seek to challenge Ethereum’s dominance, or at least pick off some of its use cases. L1 LandscapeWhen I first made the connection between Ethereum and Excel, I didn’t realize just how deep it went. In Excel Never Dies, Ben and I wrote that, “Excel’s flexibility lets businesses build all sorts of work flows and processes in the humble spreadsheet. That creates an emergent product roadmap for the B2B software industry.” The result is the Unbundling of Excel, which has created software companies collectively worth half a trillion dollars.

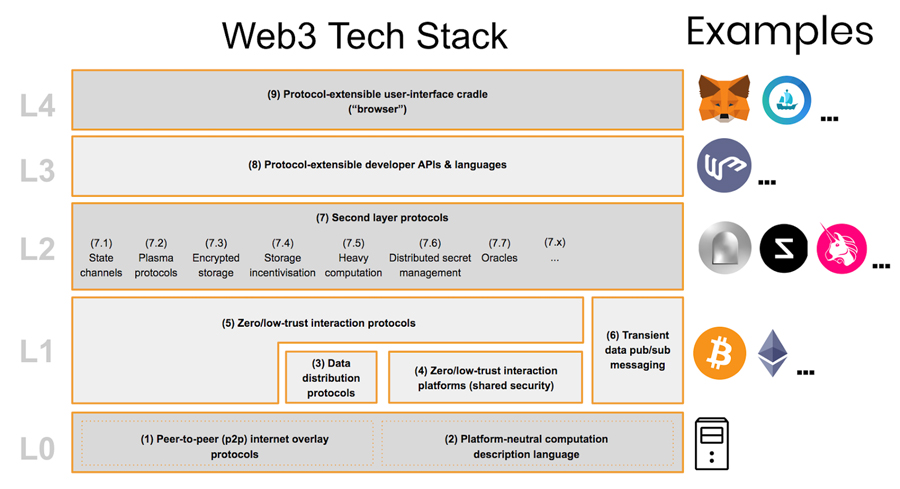

Similarly, a handful of blockchains/L1s are aiming to thrive where Ethereum is weak. As a refresher, Ethereum, Bitcoin, and other blockchains are Layer 1 in the Web3 tech stack. For Bitcoin, pretty much everything, aside from Lightning Network, happens at Layer 1. Hold BTC, send BTC, track BTC. For Ethereum, most of the magic comes in the interaction with Layer 2, the application layer.

Source: readthedocs.io, examples mine The second layer is where builders create Lego blocks of protocols and smart contracts that can be arranged in countless combinations and formations to do anything from mint art to trade crypto, directly, without the need for a third-party. It’s also where L2 scaling solutions like Polygon and Optimism live. When I asked Twitter for compelling reasons not to buy Ethereum, other than Bitcoin Maxis, the most common nonsensical responses came from people shilling other L1s. There are a lot of Something Maxis, people who believe their thing is the one and only solution, but I subscribe to the idea that each successful L1 or L2 will focus on what it does best and interoperate with others who do something else best. I’m a Maximalist Minimalist. To be fair, before digging in, I also would have thought that other L1s were the biggest risk to Ethereum. But in talking to people much smarter in the space, and comparing the situation to Excel, I think the most credible L1s are complementary, and that the ones that are trying to compete directly will lose outright. Chief among the direct competitors is Cardano ($ADA). A lot of people in my replies were shilling Cardano. Then I looked at the website:

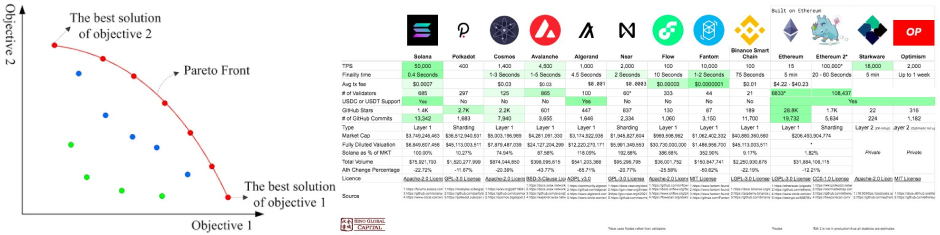

“Cardano is a blockchain platform for changemakers, innovators, and visionaries, with the tools and technologies required to create possibility for the many, as well as the few, and bring about positive global change.” I read and write a lot of words and I have no fucking idea what that means. The whole site has strong Quibi vibes, like seasoned execs heard about the blockchain and tried to make one that woke kids would appreciate. Plus, it’s trying to compete directly with Ethereum via smart contracts and faster speeds, and is somehow based on peer-reviewed research? ngmi. Others, like Avalanche and Hedera seem to be building for the enterprise. It’s an interesting approach, but not a huge threat to what Ethereum is going for. There are others, though, that are more interesting and less directly competitive, aimed at serving use cases that Ethereum doesn’t serve well. If Ethereum sits in the middle of the Pareto Frontier, these others move up or down on the line:

Source: Sino Global Capital, h/t @luxetveritasil They make trade-offs to optimize for certain characteristics, and potentially use Ethereum as a settlement layer, where its greater security will give whales more comfort holding high-value accounts and digital items. Two of the L1s taking this approach that I’m most interested in are Flow and Solana. Flow When Axiom Labs launched the first NFTs, CryptoKitties, they overwhelmed Ethereum with volume and overwhelmed buyers with transaction fees. In response, the team set up Dapper Labs and created the Flow Blockchain. Dapper Labs, and its NBA TopShot, were the darlings of the recent NFT boom. They recently raised a round at a $7.5 billion valuation, led by Coatue, to continue to build out Flow and expand the ecosystem built on top of it. I’ve talked to a few consumer-focused NFT startups in the past few weeks that are building on Flow with funding from Dapper Labs. It’s a win-win for both sides -- startups get funding and support from the company that has had the most success scaling NFTs to non-crypto people, and Dapper gets more usage on, and consumers of, Flow. On Invest Like the Best, a16z partner Chris Dixon explained how Flow and Ethereum might interoperate:

As Flow brings more non-crypto people into Web3, both Flow and Ethereum benefit. SolanaThe L1 that I’m most excited about besides Ethereum is Solana(disclosure: I own some SOL). Solana is likely the fastest and lowest cost blockchain in operation, capable of 50,000 transactions per second (TPS), compared to Ethereum’s current 19 TPS, at a cost of less than one-tenth of one cent. I spoke to Solana founder and CEO Anatoly Yakovenko, and he told me that what Solana is trying to optimize for is instantaneous censorship-resistance over very short periods of time to create fair and open market access to data. He wants to build the execution layer for finance, not necessarily competitive with Ethereum, but with the New York Stock Exchange. Where those transactions settle, and where people hold their coins, doesn’t matter as much to him. Like Eth2, Solana uses a Proof of Stake consensus mechanism, but unlike Eth2 or most of the other scaling solutions, Solana is single-shard. Everything happens on the same chain. They achieve that by using something called Proof of History, which isn’t a consensus mechanism but a source of time, or as Anatoly explained it, “the implementation of the arrow of time in math.” Proof of History uses cryptographic timestamps to sequentially order each transaction that occurs on Solana to provide verifiable ordering without requiring all nodes to agree simultaneously. That has obvious use cases in finance. Just as Ethereum users may be willing to pay a larger tip to move up in the block order, Solana makes money through Miner Extractable Value (or MEV). It sounds evil, but it isn’t. It’s like Payment for Order Flow, but open to anyone in the world with the right hardware instead of just hedge funds. It’s hoping to commoditize and democratize what high-frequency traders are able to do today. There are also non-financial products building on top of Solana.

The Solana Ecosystem Audius, the web3 music streaming platform, builds on both Ethereum and Solana. It issues and manages the $AUDIO token on Ethereum, but it runs upvotes and likes, things that need high speed and low-cost to work as well as a Web2 counterpart, on Solana, powered by the same engine used by some of the most sophisticated finance professionals in the world. That’s one of the most interesting things about blockchain technology -- the ability to build a super high-performance machine that anyone in the world can plug into and use, even if they could never afford to otherwise. Here, too, something that I first thought was competitive with Ethereum is actually a complement. By optimizing for a high-speed trading use case not currently possible on Ethereum, Solana is bringing more financial activity on-chain. By enabling microtransactions like votes and likes, on-chain, and improving the user experience for products that also run on Ethereum, Solana is improving the web3 experience and onboarding more users. Plus, Solana is building compatibility with Ethereum that would allow it to behave like an Ethereum L2, but with the functionality of a L1, including the ability to deposit USD directly at miniscule fees. More on-ramps is net positive for the ecosystem as a whole, and Ethereum sits at the center of the ecosystem. If you come at the king, you best not miss. Just as nothing has killed Excel’s core use case but plenty of multi-billion dollar companies have built businesses by focusing on specific use cases, none of the ETH-killers are going to kill ETH. To the contrary, given the nature of web3 and how early the ecosystem is, more complements bringing more demand is a positive. The Bull Case for Ethereum More demand and less supply leads to higher prices. More fees accrue to fewer coins. I’ve written a lot of words up to here, but the bull case for Ethereum is that simple if you believe a few things.

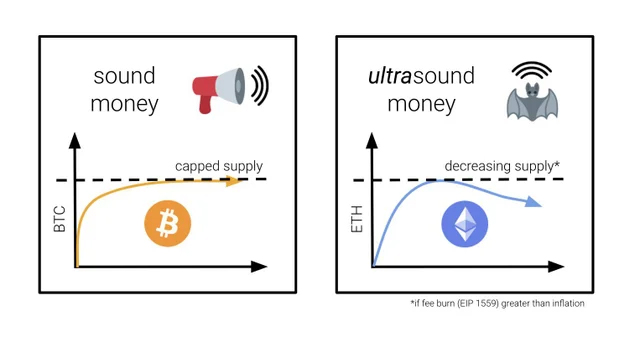

If you believe all of those things, then here’s the bull case. Demand Will Go Up Between Q1 2020 and Q1 2021, there was a massive increase in demand across all categories, from DeFi to NFTs to virtual worlds. Transaction fees increased 200x. All of that happened while usability was rough and fees were exorbitantly high. As my friend Jon Wu (who you should follow to get smarter on all of this) explained it: This past year was as bad as it’s ever going to get for Ethereum. It’s only going to get better from here, for a few reasons. First, assuming everything goes as planned with EIP 1559 and the Eth2 merge, transaction speeds will go up, and gas fees will become both lower and more predictable. It will be easier and cheaper to transact. Lower transaction fees and faster transaction times should lead to more transactions. Second, even if what we just experienced was a bubble, short-term bubbles are long-term useful! They attract money and talent to the space, and money and talent will mix to create new products that attract new users and more demand. I’ve seen dozens of pitches from strong teams leaving traditional startups to build web3 products, many on top of Ethereum, in the past couple of months alone. More products and better experiences will attract more users. ETH is an indexed bet on that growth more than a bet on the success of any one project. Strong trends, lower prices, better experiences, and new products = growing demand. Lower Supply For many ETH bulls, this is the crux of the argument: EIP 1559 means that ETH becomes deflationary. Bitcoin issuance is capped at 21 million. This has been the strongest bull case for BTC. You can’t just print more, like the evil central banks, it’s math, and it’s capped. It’s sound money. The knock against Ethereum is that there is no cap. Theoretically, enough Ethereum users could decide to keep printing ETH and inflating supply. If you’re going to have an inflationary asset, why not just use fiat 🤮 amiright? But EIP 1559 and Eth2 flip that. With Eth2, new issuance to reward validators is expected to drop dramatically versus Proof of Work rewards. With EIP 1559, by burning ETH in every transaction, assuming a conservative amount of daily transaction fees and that 70% of the gas fee is burnt and 30% is sent as a tip, then more ETH will be burnt than issued every day. Together, the supply of ETH will actually begin decreasing after EIP 1559 and the Eth2 merge. It’s better than sound money. It’s Ultra Sound Money. 🦇 🔊

To understand the numbers, check out the models that Justin Drake built on ETH Peak Supply and The Road to 100M ETH. The implications here are enormous. Directly, it means lower supply meeting growing or accelerating demand, which should lead to higher prices. Even wilder, if people and institutions are holding BTC because of its use as a non-inflationary Store of Value, might they switch to Ethereum instead if the Ultra Sound Money thesis plays out? Could Ethereum flip Bitcoin as the most valuable cryptocurrency? But it doesn’t stop there, because ETH isn’t just a store of value. Value Accrues to ETH Holders ETH ownership also grants the right to do work for the Ethereum network as a validator and earn a share of fees. In Proof of Work, miners need to sell the ETH that they earn to cover costs. Today, that creates a daily sell pressure of 22.3k ETH, according to another Justin Drake model. That means that every day, 22.3k newly-created ETH, about $50 million worth, are dumped on the market. With Proof of Stake, the only costs are taxes, which Drake assumes to be 50%, and new issuance drops from 13.5k ETH to 2.1k ETH. That leads to a net sell pressure reduction, from 22.3k ETH per day to 2.6k ETH per day. That’s the equivalent of roughly $40 million per day in new demand. Plus, instead of leaking out of the system, the value accrue to validators. Another Drake model estimates that people who stake their ETH (meaning lock it up to secure the network) can earn a 25% APR including new issuance and tips. In sum:

Risks, More Caveats, and a Conclusion Whenever you’re reading Not Boring, you need to remember a couple things:

Part of the reason I’m so bullish on ETH, the asset, is that the potential of Ethereum, the technology, excites me. ETH is a ticket to web3, but it’s also an excuse to keep going deeper and deeper down the rabbit hole. What I look for in an investment -- returns + participation + education + fun -- might be completely different than what you’re looking for. This past weekend showed just how volatile crypto can be, and how pegged everything still is to bitcoin. If you were in ETH for a quick trade, this weekend could have been nauseating. If you’re in it because you want to learn and explore web3, it was a great opportunity to buy more tokens to play the game at half-off. Despite my overall bullishness, there are real risks ahead for Ethereum, both macro and specific. On the macro side, what happens if Tether blows up? What if governments crack down on crypto generally? What if rates rise ahead of schedule and risk assets tank? What if Elon Musk tweets again? One of the scariest things about this past weekend’s sell-off is that there wasn’t a clear and obvious catalyst. Crypto markets can be wild. Somewhere in between the micro and the macro, there’s a question: what if people outside of the early adopter set just don’t really care about decentralization? What if more centralized solutions like Binance Smart Chain, which comes with a built-in user base of millions of people who trade on Binance, are decentralized enough and more performant? On the micro side, Ethereum faces some real challenges. What if EIP 1559 doesn’t go through as planned? What if the Eth2 merge is delayed? What if sharding doesn’t work as planned, and creates more issues than improvements? One very real possibility is that sharding makes the Legos built on Ethereum less composable, weakening one of the most exciting aspects of the network. Maybe the biggest issue facing ETH is adoption of fragmented Layer 2 scaling solutions. While L2 solutions hold the potential to dramatically improve performance, they present two main challenges, one to Ethereum, and one to ETH:

Admittedly, I don’t know enough to have a strong opinion on the topic. This is an area for more exploration, and maybe a future post. If nothing else, I hope this piece changed the way that you think about Ethereum and makes you want to keep exploring for yourself. That’s the fun here. Normies are getting ETH-pilled, the narrative is changing, and the most bullish thing for Ether is to be understood. * * *

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)