Send this article to a friend:

March

31

2021

|

Send this article to a friend: March |

|

Can Silicon Valley Beat China In Clean Energy Tech?

Yet, Clean tech 1.0 was a disaster, a fact that still lingers like a bruise on the amygdala of investors from a decade and a half ago. According to PwC, of the $25 billion invested by venture capitalists in the clean-tech sector between 2006 and 2011, about half got wiped out. Disappointed by the dismal returns, VCs diverted their attention to app developers, software, and artificial intelligence (AI), which promised bigger returns without demanding huge infusions of capital. In sharp contrast, China has been hugely successful in scaling up solar power and driving huge cost reductions in wind energy and EV batteries. Which makes this year's clean energy selloff all the more seem like déjà vu. After a massive runup over the past two years, the clean energy sector is going through a correction with the sector's most popular benchmark, iShares Global Clean Energy ETF (ICLN), down 20.4% in the year-to-date while its solar peer Invesco Solar Portfolio ETF (TAN) is down 17.1% over the timeframe. But make no mistake about it: Clean tech 2.0 is a one-way street with no chance of turning back. After all, it's got a lot more going for it, including pressing climate goals, much stronger government support, much stronger backing by Silicon Valley, and thousands of useful lessons gleaned from Clean tech 1.0. As Andrew Beebe, managing director at San Francisco-based Obvious Ventures, has succinctly put it:

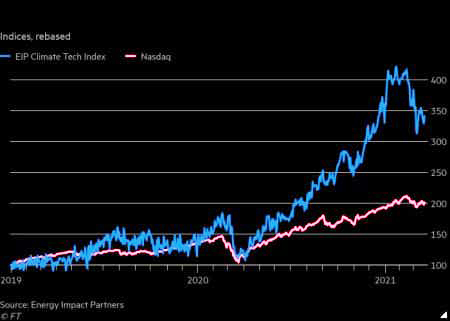

But as this year's correction proves, this is by no means going to be a walk in the park. China's success With Beijing's backing, China's clean energy entrepreneurs were able to scale rapidly with solar energy recording an 80% cost reduction over the past decade. A surge in production in China was responsible for pushing down the price of polysilicon—a key raw material used in solar panels. This lessened the demand for innovative technologies backed by U.S. venture capital evaporated. To make matters worse, U.S. investors shot themselves in the foot thanks to Silicon Valley's "moon shot" approach of hunting for big breakthroughs rather than focusing on smaller, incremental advancements. The result: the majority of the first American solar startups went under because they were unable to compete with China. Almost all the Silicon Valley-backed startups folded, with a handful such as solar startup MiaSolé and battery startup A123 Systems bought by Chinese companies. Learning from China But, finally, Silicon Valley is getting its act together. Whereas Silicon Valley had little to do with solar energy becoming the cheapest form of energy in the world, China's success in scaling up solar power as well as cost reductions in wind energy and EV batteries have provided it with a blueprint, laying the groundwork for a new wave of investment in clean energy startups. First off, Silicon Valley has thrown its full weight behind the sector and the massive ESG boom. The failure of Clean tech 1.0 was not so much due to technical problems but rather a lack of financing options. Luckily, Clean tech 2.0 is enjoying a much greater variety of capital options available, including blank check companies, aka special purpose acquisition companies (SPACs). SPACs act as an alternative to the traditional IPO process. SPAC IPOs have truly exploded over the past few years, with more than 220 SPAC IPOs recorded over the past 12 months with gross proceeds exceeding $74B compared to $13.6B in gross proceeds just a year prior. In fact, we now have a SPAC ETF—SPAC and New Issue ETF (NYSE:SPCX), the first actively managed fund dedicated to the asset class, which was launched last year. Last year saw 40 climate-related companies merging with SPACs, including electric vehicle battery startup QuantumScape, which was backed by Breakthrough Energy Ventures—a $2 billion fund by Silicon Valley tech heavyweights including Microsoft Inc. (NASDAQ:MSFT) and Amazon Inc. (NASDAQ:AMZN) that invests in promising clean energy startups. QuantumScape is currently valued at $21 billion. Part of the appeal is that SPACs not only provide an avenue for early-stage investors to exit their positions but also enables startups to raise more money so they can scale-up production. SPAC-mania is a real thing: Just a month ago, Brazilian iron ore miner Vale S.E. (NYSE: VALE) invested in one of its startups, Boston Metal, a startup that aims to produce low-carbon steel. Further, VCs have become a lot more demanding, with Breakthrough Energy only investing in startups that have the potential to remove 500m tonnes of greenhouse gases a year from the atmosphere—about 1% of the planet's annual output. But ultimately, the biggest reason why everybody wants a piece of clean energy is simple: Returns are higher. Companies supporting decarbonization have clearly been outperforming their more conservative peers.

Source: The Financial Times Government support The renewable energy sector has yet another powerful ally: Governments committing to climate goals. For instance, the U.S. solar sector now has the full backing of the government. A few days ago, the Biden administration set a goal to cut the cost of solar energy by 60% over the next decade. Specifically, the Department of Energy (DoE) wants to lower utility-scale solar energy's current cost of 4.6 cents per kwh to 3 cents by 2025 then to 2 cents by 2030. DoE also aims to have the U.S. power grid to run entirely on clean energy within 15 years, meaning solar energy will need to be installed 5x faster than the current rate. The DoE has committed to spending $128M on technologies including perovskite solar cells and more novel technologies such as cadmium telluride and concentrating solar technologies. Ultimately, developing any technology from the lab into a low-cost, mass-market product with the potential to lower global emissions is not only incredibly hard but frequently requires long lead times. However, Wall Street is saying this time it's different because entrepreneurs have a better understanding of what it takes and are also backed by deep-pocketed corporate investors looking to decarbonize their operations as well as friendly governments. It's a one-way street that investors will have to travel. By Alex Kimani for Oilprice.com

|

Send this article to a friend:

|

|

|

Many investors are already aware of the fact that China is the world's most dominant player in the solar and clean energy sector. 8 out of 10 biggest manufacturers of solar equipment are Chinese with First Solar (NASDAQ:FSLR) and SunPower (NASDAQ:SPWR) the only American representatives among the elite. It's not for lack of trying, though—Silicon Valley pumped tens of billions of dollars in clean energy ventures during the first wave of the renewable energy transition that started halfway through the first decade of the new millennium.

Many investors are already aware of the fact that China is the world's most dominant player in the solar and clean energy sector. 8 out of 10 biggest manufacturers of solar equipment are Chinese with First Solar (NASDAQ:FSLR) and SunPower (NASDAQ:SPWR) the only American representatives among the elite. It's not for lack of trying, though—Silicon Valley pumped tens of billions of dollars in clean energy ventures during the first wave of the renewable energy transition that started halfway through the first decade of the new millennium.

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)