Send this article to a friend:

February

07

2022

|

Send this article to a friend: February |

|

Buckle Up: Virtual Signaling As Financial Implosion Looms

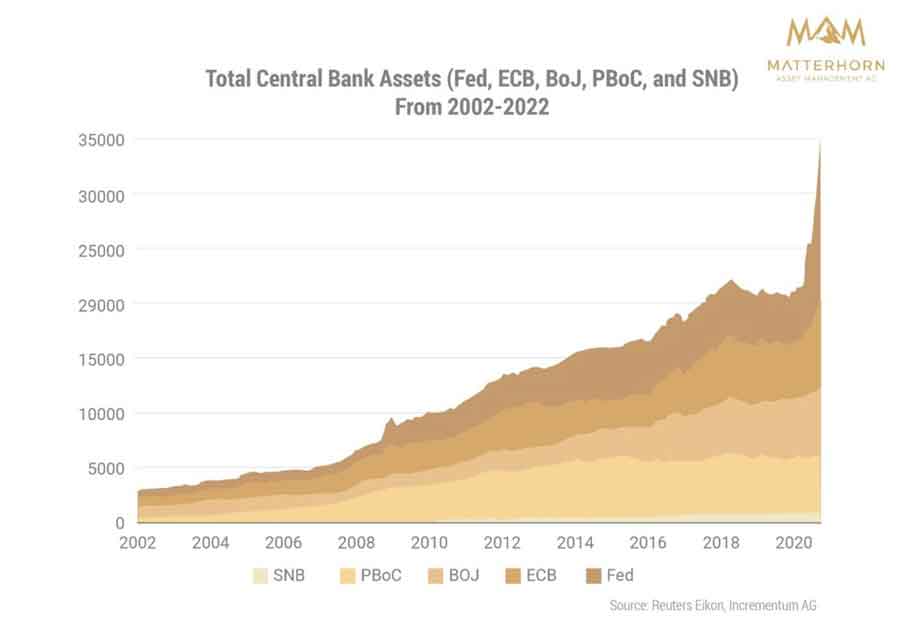

From Virtue Signaling to Elite Tough-Talk In recent years, we’ve seen some admittedly questionable virtue signaling on everything from racial tensions to compliance. I’m thinking of Hollywood’s finest singing John Lennon or Howard Stern and Arnold Schwarzenegger piously criminalizing the. For many of us, watching the subject-matter clueless pretending at wisdom would be almost comical if it wasn’t otherwise so tragic. But for those who track bloated risk assets, cornered central banks, fatal debt levels and incompetent leadership, the sudden rise in tough-guy talk from the skunks in our own financial woodpile is becoming equally tragi-comical. Hawkish Bankers Playing Chicken with Markets As we’ve been warning for over a year, hawkish talk from the Fed regarding a “tapering” of its balance sheet combined with a well-telegraphed rate hike will hardly be good news for debt-saturated securities markets who survive exclusively off of low-rate/cheap borrowing costs. In short: If Fed-engineered low rates gave us this everything bubble, Fed-tapered rising rates will end it. But such examples of the obvious haven’t stopped the 11th-hour experts from suddenly chiming in with some chest-puffing tough-talk of their own as the game of chicken between a central bank and a centralized market continues. Thanks For Nothing Goldman Sachs In a moment of hawkish courage-signaling, Goldman Sachs Group, Inc. President, John Waldron, has been openly critical of Fed independence and rising inflation. Toward that end, he recently declared that “we might need to bring back Paul Volcker” to add some interest-rate-hiking containment and much-needed discipline to our over-heated markets. Now that’s some tough talking. This Goldman mouthpiece of a bank notoriously linked to government bailouts and record-breaking market bubble-creation went on to say that the Fed needs the kind of leadership that does what’s right and steady “without regard for what’s going on in the markets.” Perhaps Waldron had forgotten the not-so “right and steady leadership” from Goldman during its ABS/CDS disaster circa 2006? Ah, the ironies, they do abound… In any case, such tough-talk is pretty rich coming from a bank and banker who knows (and always knew) that the Fed’s covert yet primary mandate has always been the propping of an otherwise rigged-to-fail market, including TBTF banks like his own—just ask former Goldman-CIO-turned-Treasury Secretary Hank Paulson and former Fed Cahir turned market-maker, Ben Bernanke. Waldron knows, moreover, that the parabolic rise in stocks post-March 2020 is directly correlated to the Fed’s doubling of its balance sheet to over $9T in just two years, a move copied by other central banks…

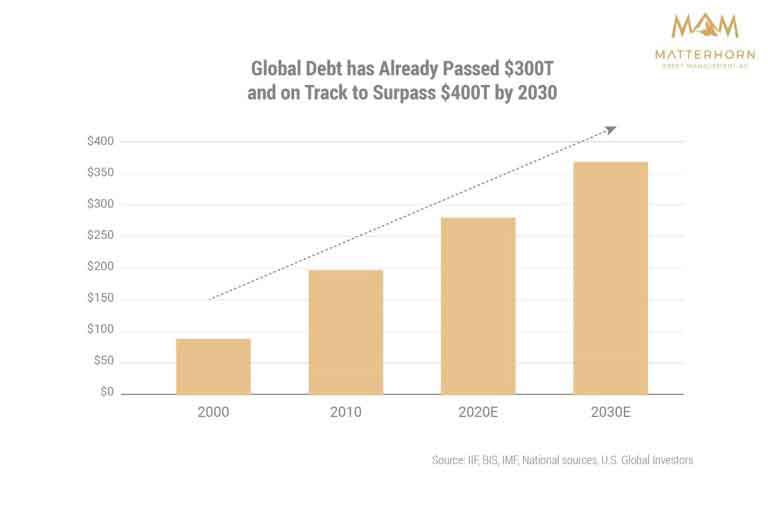

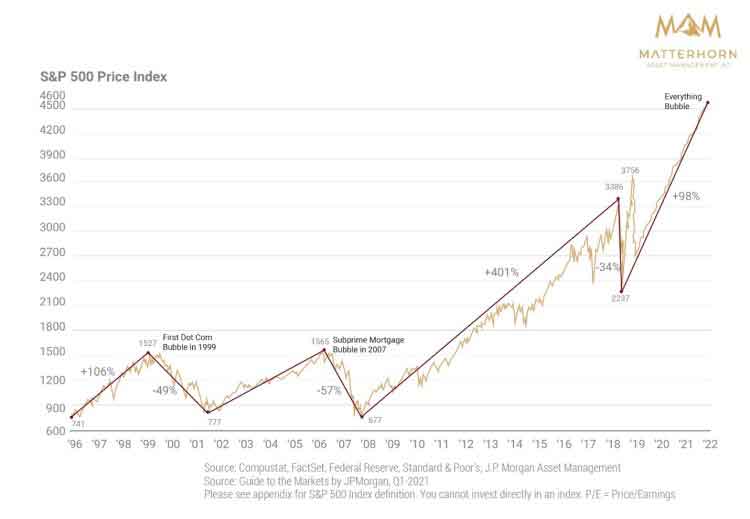

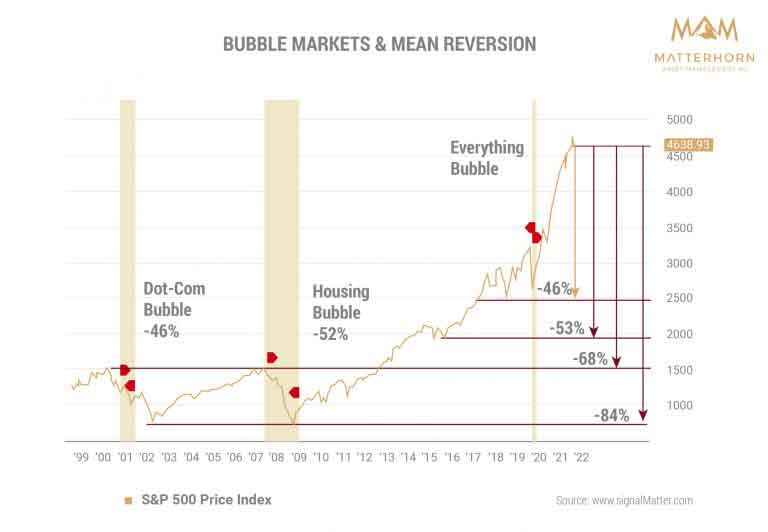

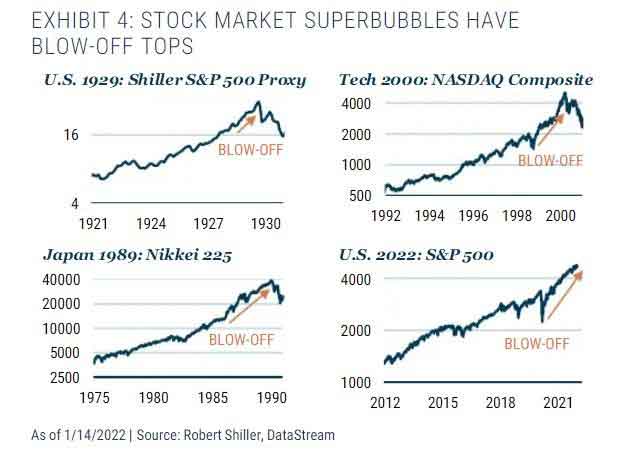

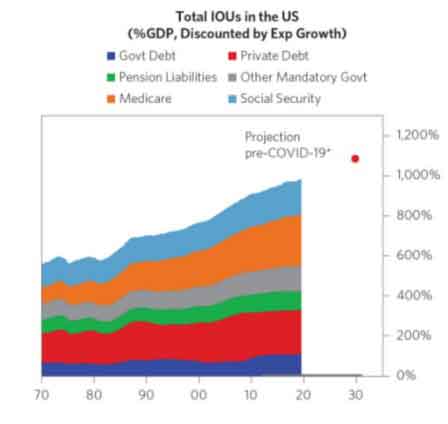

Amazingly, Waldron nevertheless openly criticizes the Fed’s growing lack of independence and credibility over the last 40 years, which is hardly a cutting-edge observation for anyone tracking the open-marriage between the Fed and an entirely Fed-dependent U.S. government. As if suddenly waking from a four-decade nap, is Waldron just now saying the Fed has gone too far with its money printer (see above)? Too Little, Too Late Well, like a soldier deliberately enlisting after the war is already over, Waldron’s signaled courage is a bit too little, too late. Yes, Mr. Waldron, the Fed’s balance sheet is an open embarrassment, but it has been for years. And any significant tapering of Treasury purchases now will mean a significant drop in bond pricing and hence a significant increase in bond yields and hence interest rates. And we all know (except, apparently, Mr. Waldron?) that rising, “Volcker-like” rates are like approaching shark fins to a global market driven by the greatest debt pile in history—a pile Waldron conveniently ignored in his recent public outcry of tough-talk ignoring fatal consequences.  Once that debt (sovereign, corporate and household) becomes too expensive to pay, the entire system implodes. Full stop. Period. And it will implode. So, Mr. Waldron, why did you forget to mention that fun fact in your recent Bloomberg chest-puffing? Thanks For Nothing Mr. Waldron Needless to say, the bigger the bubble, the bigger the “pop” that follows, and Goldman, along with the Fed, has been an open party to the greatest risk asset bubble (see below) in modern capital markets. In short Mr. Waldron: Thanks for nothing. Waldron’s recent ringing of the alarm bell looks a lot like an open (and frankly hypocritical) attempt to position (virtue-signal?) himself (and his bank) for an “I told you so” moment and warning, almost as brazen as Larry Summers warning about debt after having de-regulated the very derivatives market that eventually blew the markets to Hell in 2008. As I’ve written elsewhere: Don’t always trust the experts. Despite Waldron’s brave taper-talk and Fed attacks, he makes zero, and I mean zero mention, of the simply astronomical debt levels in the US and globally. Folks like Waldron (and even geniuses like Jeremy Grantham) keep missing the (sovereign, fiscal and global) debt elephant in the room, for once that debt market collapses under its own weight (and taper-driven rate hikes), securities, currencies and hence economies around the world will spiral. What virtues will banks like Goldman signal when that happens? In the interim, and in order to stem the bleeding to come, more fiat money will likely be mouse-clicked en masse to save an otherwise un-savable and Fed-created debt monster. Such ongoing “emergency measures,” of course, will be fatal to currency purchasing power and likely trigger the not-so-secret “Bretton Woods 2.0 Re-Set” already well-telegraphed by the IMF as early as 2020. Bridgewater Chimes In—More Hawkish Virtue Signaling Meanwhile, over at Bridgewater, similar tough-guy swings at the Fed continued from Greg Jensen, who now, after years of watching (and benefiting from) the embarrassingly grotesque, artificial and unprecedented climb of the S&P, DOW and NASDAQ, is suddenly confessing that a day of tough Fed policy and market reckoning is needed. Again, that’s rich…and comes a little too late Mr. Jensen. Look, for example, at the size of the equity bubble that banks like Goldman and funds like Bridgewater have openly enjoyed during well over a decade of extreme Fed profligacy:  Folks, if the above chart is not evidence enough of a fatal and Fed-driven mega-bubble, I really don’t know what is… As figures as far back as David Hume to Ludwig von Mises (not to mention Thomas Jefferson or Andrew Jackson) have warned, and as history as shown from as far back as ancient Rome or the France of 1790 to the Bear Sterns of 2008 confirm: The bigger the debt-driven party, the more deadly the hangover. As for Jensen, he predicts a stock hangover ahead of at least -20% should the Fed acquire its backbone and get/stay hawkish, as per his “virtuous advice.” Frankly, Mr. Jensen, 20% is optimistic to the point of silly. A Brief Lesson in Mean Reversion I remind Mr. Jensen over at Bridgewater of a simple little market force which I’m sure he and his Connecticut-based colleagues have discussed at the water-cooler, namely: Mean Reversion. Mean reversion, in fact, is one of the most consistent and natural laws of even un-natural/artificial markets like our own. That is, over-bought as well as over-sold securities inevitably and eventually “revert’ to their mean price levels. That is, much like a rubber band stretched up or down from one’s knuckle, the band eventually recoils back with a sting. In case you want to know the potential extent and size of that sting in the current market environment, take a look at the bubbles, graph and mean-reversion implications below…  Again, a 20% “reversion” or fall from these Fed-driven nosebleed levels is being optimistic to say the least. The resistance lines outlined above suggest that the pain (mean reversion) ahead for these bloated markets is far greater than Jensen’s mere 20% and is instead flirting far more dangerously close to at least a -53% to -68% loss. Book Signaling? Of course, banks and hedge funds like to talk their books in the open arena, and one almost wonders if Goldman and/or Bridgewater, in moves all-too-familiar to the ethics-challenged era of Elon Musk, are telegraphing their own short positions (or in Musk’s case, infamous 2018 “funding secured” short-squeeze). Hard to say. It’s Not Gonna Be Fun But one thing is easy to say, namely: Hawkish Fed talk followed by an actual Fed taper will be no fun for stocks and bonds, all well overdue for some serious and mean-reverting “sting.” We all remember, of course, the 2018 Fed attempt to tighten and raise rates into Christmas. Markets puked immediately on a 25 basis-point rate hike. Thereafter, a classic Fed pivot immediately followed into early 2019. In short: The hawks became doves real fast. But as for Jensen, he says the Fed will not “blink” this time. Instead, they will remain disciplined and tough due to current inflation dangers, which, he argues, makes 2022 different than 2018. In other words, emergency (dovish) QE will not follow as per the prior years. I’m not so sure. Debt + Rising Rates Matter Like Jensen, however, I do wonder just who will be buying Uncle Sam’s unloved IOU’s (i.e., Treasury bonds), if the “tapering” Fed is no longer the “expanding” buyer of last resort? Remember: Bond yields (and by extension, interest rates) move inversely to bond price. If Fed demand for bonds “tapers,” bond prices fall and rates (those deadly “shark fins”) rise. Toward this end, the economists over at Bank of America are forecasting seven hawkish rate hikes in 2022 and a 2.75%-3% Fed Funds Rate. Well, that’s tough talk, but what BofA (like Waldron and Jensen) is failing to discuss is that such a rate hike would mean an increased 4% to 5% borrowing cost for Uncle Sam and his staggering $30T bar tab, which at those projected rates boils down to about $1.5T per year in just interest expense alone. Think about that number and read that last line again. Paying that bar tab would require 40% of US tax revenues being earmarked just for interest payments, which is an historical, neon-flashing sign of a nation and financial system on the cliff of an open and self-inflicted debt crisis. Hawks, Chickens and Elephants In short, it seems some of our banking and hedge fund Wunderkinder, proud with their tough talk, are missing the debt elephant in the room as a now hawkish Fed plays chicken with record-high and top-blowing stock markets.  Believe it or not, Uncle Sam’s total debt obligations (i.e., pension debt, govt debt, Medicare, social security etc.) are 1000% of his GDP, which simply means the US will never repay its “elephant-sized” debts. Never.  Meanwhile, the cost of just floating the interest on that total debt is way beyond the incoming revenue from US tax receipts, which in a looming recession, will be going further down not up… In short and in summary, the experts are once again not so expert. Looking (Realistically) Ahead Although no one enjoys such hard, stubborn and depressing facts, it’s time we all speak plainly and realistically about debt rather than just talk tough about an already guilty, discredited and corrupted Fed—thanks to Patient-Zero Greenspan and all the Fed Chairs who followed in his wake. And although it may seem refreshing to see folks at Goldman or Bridgewater taking public swings at this same Fed, as indicated above, it’s far too little and far too late. The warnings they are making today are the very same we’ve been making for years as GS and Bridgewater got fatter and fatter. The debt damage, unleashed by well over a decade QE addiction and Fed drunk-driving, has already been done. Alas, a reckoning is no longer theoretical, but baked into the math (and history) of their own doing. Looking ahead, and assuming the Fed tightens as demanded above by our tough-talking experts, please get your portfolios ready for massive volatility in 2022. In the near-term, a tapering Fed will be a headwind for just about everything but the USD and the VIX. Longer-term, and contrary to Bridgewater’s Jensen, it’s highly likely the Fed will once again pivot from hawk to dove when the coming taper leads to an unprecedented tantrum on the equity tapes. Such a dovish pivot will then be a tailwind to precious metals, BTC, industrials and commodities in general. And the Big Reset? Of course, looming forever above this admittedly ominous, self-inflicted horizon of a cornered Fed and bloated “everything bubble,” is the equally inevitable moment of “uh-oh,” by which markets and currencies will have taken such an historical beating that the global experts will solemnly announce the need for an otherwise well-telegraphed (i.e., pre-packaged) global reset and Bretton Woods II. This will mean more government controls, excuses and distortions the likes of which will surprise even me. Add a (Scape) Goat to the Foxes, Skunks, Chickens, Hens, Hawks, Doves, Sharks and Elephants When, not if, that Re-Set comes, the very foxes who guarded and then raided the global financial hen house which they alone destroyed, will bow their collective heads and innocently point the blame not at their deserving selves, but at the crisis, whose arrival served as a perfectly convenient (perhaps too convenient?) scapegoat for their own sins. Until then, buckle up for a scary ride/taper.

|

Send this article to a friend:

|

|

|

Numerous animal metaphors (hawk, dove to goat) are employed below to make sense of an otherwise imploding financial “barnyard.” Among such squawking beasts, two financial elites from Goldman Sachs and Bridgewater are making the latest noise; but as we soon discover, it’s just that: Noise.

Numerous animal metaphors (hawk, dove to goat) are employed below to make sense of an otherwise imploding financial “barnyard.” Among such squawking beasts, two financial elites from Goldman Sachs and Bridgewater are making the latest noise; but as we soon discover, it’s just that: Noise.

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)