Send this article to a friend:

January

16

2024

|

Send this article to a friend: January |

|

| 2 Undeniable Gold Trends Coming In 2024

Today’s gold market might be closer to 2008 than 1971 Sprott’s Craig Hemke and Technical Traders’ Chris Vermeulen recently discussed whether gold and silver are gearing up for a run like the 2008-2011 surge in gold price. We’ve focused so much on comparisons to 1970s due to interest rate hikes that we’ve almost neglected an equally-important period. Despite gold’s lopsided gains in the decade after Nixon closed the gold window, the 2008-2011 run culminating in the $1,910 peak and a multi-year correction hit closer to home for most. If accurately comparing the current stretch to the 1970s was difficult, doing it to the turbulent financial crisis is next to impossible. That is what the pair keep going back to, wondering if we’re facing similar tailwinds without realizing it based on price action. As they go back and forth on the idea, volatility is perhaps even more of a factor in the discussion than gold itself. Hemke and Vermeulen note that it’s going to be a volatile year, and that the yellow metal could be fully engulfed in its own whiplash as we witness another remarkable bull run. What this means, unfortunately for shaky hands but very fortunate for those looking for dips, are pullbacks. The two remember how gold clearing $1,000 was a massive psychological hurdle, as was the blow when gold’s price fell to $700. With the levels we are seeing now, the comparable targets might be $2,000 and $2,500. $2,500 is definitely a level that the pair see as realistic either this year or next. They remind us that the threat of a near-term pullback is always there to accompany fast gains. We could say that last year’s gradual gains were the kind gold owners prefer. Really, they were anything but. The climb from $1,900 to $2,000 was long and steady, yet the jump from $1,650 to $1,900 was rapid, leaving investors puzzled. We haven’t seen a correction of that jump, so would $2,500 gold necessitate a pullback of equal magnitude? Or leave open more space for the metal to gain? Enticing speculation for the gold owner. Hemke and Vermeulen note that silver has been underperforming compared to gold and failing to follow the historic pattern of outperforming gold during commodities bull markets. Learn more about the gold-to-silver ratio here. While silver’s volatility is often called a benefit, Hemke and Vermeulen say an investment with 30% intraday upside or downside can be a little too much for those seeking a safe haven. Silver’s price moves more like bitcoin than like gold. Gold has performed exceptionally well as a safe haven investment. Its combination of diverse sources of demand, high liquidity and inflation resistance make gold the definition of a safe haven asset, regardless of today’s price. Gold starts 2024 strong, some resistance ahead: World Gold Council In their latest review, the World Gold Council (WGC) noted that gold rose by 15% in 2023. Uniquely, the WGC attempts to quantify the factors behind gold’s annual price increase. In my mind, price comes from just two factors: Supply and demand. But that isn’t good enough for the WGC. According to their proprietary model, gold’s annual performance is the sum of the following:

The central bank demand line item is particularly interesting. WGC analysts state that central bank gold demand made up only 4% of gold’s average annual growth before 2022. In other words, all that’s needed for gold to continue posting all-time highs is for central bank de-dollarization efforts to continue. By all accounts, they’re accelerating. An earlier analysis by the WGC, called the Gold Outlook 2024, outlined gold’s performance in three different possible scenarios that could materialize this year. The so-called soft landing, which seems to be everyone’s favorite guess these days, is supposed to be negative for gold with only central banks doing anything for price action. They outline the consensus scenario as:

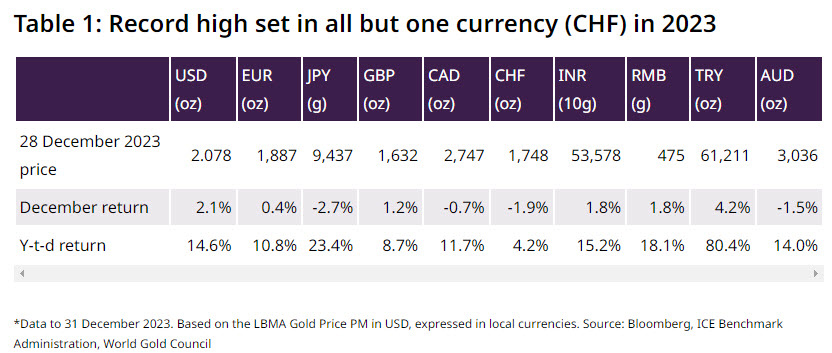

The trouble with entertaining this environment as a negative for gold is that 2023’s performance happened in precisely this environment. The only difference is inflation risks, but does anyone really expect them to simply fade away? We know that rate cuts are being mentioned as a possibility just in the first start of the year, and they are highly inflationary in nature. So the currency will be devalued further whether or not the Fed gives up on the inflation fight. The WGC also reminds us that gold set all-time-high prices in 2023 in every major currency save one (the Swiss franc): Currency debasement was one of the underlying themes in 2023, and it looks like it’s getting swept under the rug so long as the headline CPI is accommodating. But the prices can only wiggle so much before giving way to a crumbling fiat system, as we have seen in the Australian and now the Canadian dollars. Gold’s surprisingly forceful show of strength around the turn of the year might be the result of overlooked factors catching up with a weaker-than-believed U.S. dollar. It’s a reckoning many observers have called for, and one we shouldn’t be surprised to see defy standard metrics of categorization and damage assessment. China’s still making headlines with central bank bullion buying With its latest purchase of 9 tons of gold in December, China has now bought bullion for the 14th consecutive month. This is newsworthy, of course, but not to the extent readers might like. We’ve speculated that China’s newfound interest in revealing gold purchases might need to be interpreted as some kind of signal to the West. To the market watcher hyped up on the prospect of a BRICS behemoth competing with the West with China as its commander, the figures are too lackluster. China’s official stockpile of 2,000-some tons of gold is believed by few. Estimates of the real stockpile, one that was mostly accumulated off the books, place it in the range of 5,000 tons all the way up to 20,000. If we are to entertain any of that, the purchases China is making aren’t particularly relevant to its overall standing. After all, Russia would buy 20-30 tons monthly in 2018 and the like, and it’s supposed to be far worse off economically than China. Since China either wants to diversify almost as much as Russia did, or more so, it wouldn’t be excessive to assume China bought similar amounts during the same time period without reporting it. Which brings us right back to official figures. The 225 tons bought by China in 2023 are a lot, but they’re probably not that in the country’s grand scheme of financial affairs. Let us also remember that China is supposed to be one of the pioneers of the new gold standard, along with Russia. It’s mentioned as a BRICS thing, but these two seem to have the biggest currency aspirations. So who can fault gold investors for wanting something a little more bombastic out of China than reports of 9 tons of gold being bought in December? The “We know you’ve done something” element, or more specifically “know you’re doing something”, is definitely there. With an absence of any official data past what we glean from minutes of various nations, we’ll have to accept these minute announcements even though we feel there’s more. If China announced it’s buying 10 times as much gold, nobody would be surprised and we’d be discussing some kind of financial power play. This way, we’re calling the purchases underwhelming. We struggled to make sense of why China was suddenly announcing PBOC gold purchases and why in such relatively minor amounts before, but it makes sense when framed this way. Choosing to report in this manner appears to have had an intended effect of drying up most analysis and causing all but the most determined pundit to look the other way. All the while, in the background, what is probably gold accumulation on a much larger scale takes place, for reasons not so mysterious.

|

Send this article to a friend:

|

|

|