Send this article to a friend:

January

25

2021

|

Send this article to a friend: January |

|

Inflation Is Spreading Broadly into the Economy. Amid Surging Costs, Companies Raise Prices, and Customers Pay them, Despite Weak Economy,

The signs of inflation building up in the economy are now everywhere. IHS Markit, in its release of the Flash PMI with data from companies in the services and manufacturing sectors, added to that pile of evidence. For companies, inflation happens on two sides: what they are having to pay their suppliers, and what they can get away with charging their own customers, which may be consumers, governments, or other companies. And increasingly, companies are able to pass higher input prices on to their customers – meaning, their customers are not totally balking at paying higher prices and they’re not switching to other sources to dodge those price increases. That’s a mindset that nurtures inflation. This PMI data is based on what executives said about their own companies (names are not disclosed) and the conditions they face in the current month. No quantitative measures or dollar amounts are involved. And this is what they said about their two aspects of inflation, according to Markit: On surging input prices:

Passing on higher input prices via higher selling prices:

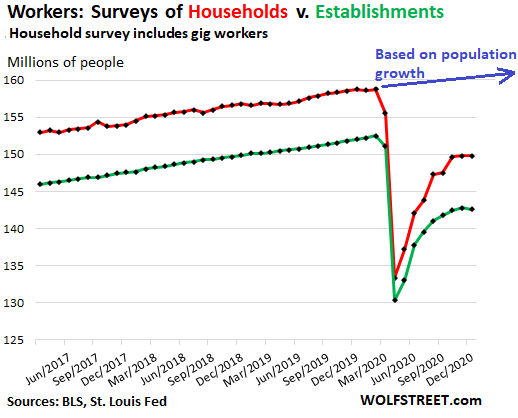

These pricing pressures woke up in June, after the demand collapse in the prior months. Markit reported at the time that “inflationary pressure returned as both input prices and output charges rose for the first time since February, with both increasing at solid rates.” And “firms partially passed on higher supplier prices to clients through greater selling prices. The increase was solid overall and the sharpest for 16 months,” it said. And since then, pricing pressures have risen in much of the economy, with food commodities, steel, and construction materials having seen a huge surge. Food inflation – which the Fed ignores in its core PCE inflation measure – is off to a good start. Prices for wheat, corn, and soybeans have spiked to levels not seen in over six years amid strong export demand from China and low US stockpiles. Rising prices of agricultural commodities raise the input costs for food producers, which are already passing on those costs in form of higher retail prices for consumers. Construction materials too, amid shortages due to the current land rush underway, as high-rise dwellers in some expensive cities are suddenly trying to buy or rent a house in the suburbs or the countryside, and homebuilders have jumped on board. Lumber prices started spiking last June and hit all-time records in August and September, amid huge volatility, and nearly matched that record at the end of December. Though prices have backed off a tad in January, they still exceed all pre-August records. “Lumber shortages are starting to bite: 31% of contractors report a current lumber/wood shortage, up from 11% last quarter,” according to the Q4 2020 US Chamber of Commerce Commercial Construction Index. More broadly, 71% of contractors reported some shortage in building products and materials, up from 54% in Q3, particularly steel, electrical products other than copper wire, and lighting products. Contractors also reported a skilled labor shortage, with 83% reporting “moderate to high levels of difficulty in finding skilled workers.” Inflation pressures despite a weak economy and 10 million missing jobs. It is interesting that these price pressures are happening even as the overall economy is not exactly booming, with GDP down 2.8% in Q3 compared to a year earlier, while 10 million jobs have disappeared, according to the BLS jobs report for December, amid a suddenly weakening employment scenario since late last year:

Price pressures are now being reported across the economy. While lamenting the further deterioration in their business, companies in the service sector – the biggies are finance, insurance, healthcare, information services, and professional services – in the district of the New York Fed also reported rising prices and wages, as the Weirdest Economy Ever is playing out. Read… To Put it Succinctly about Services: Everything Drops, incl. Jobs, but Prices & Wages Rise Enjoy reading WOLF STREET and want to support it? Using ad blockers – I totally get why – but want to support the site? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)