Soothsayers, Naysayers and Ostriches

Darryl Robert Schoon

Someday we’re

going to owe Chicken Little an apology Someday we’re

going to owe Chicken Little an apology

January 2013, US stock markets are at record highs, the volatility

index, the VIX, is as quiet as a dormant caldera and hope the US economy

is recovering is growing again as it has every January since 2010.

Dow, S&P close at five-year highs; VIX

plunges near 12 - CNBC, January 18, 2012

“It’s darkest before the dawn” is a saying often used to rally the

dispirited. The opposite sentiment, “it’s brightest before the night”,

instead cautions that unqualified optimism is just that—unqualified.

Today, hopes the global economy can overcome massive and historic levels

of debt are again on the rise. Those hopes, unfortunately, are as

unfounded as Mitt Romney’s presidential aspirations on November 6th.

|

| John Exter (1910-2006) The Central Banker who made a fortune in Gold |

John Exter after graduating from college in 1932 pursued graduate

studies at Harvard University in economics. Exter wanted to understand

the causes of the Great Depression which had brought economic activity

in the US and around the world to a virtual halt during his youth.

As a banker and economist, Exter was to have a storied career. After

being at MIT during WWII, he joined the Board of Governors at the

Federal Reserve Bank as an economist. In 1950 Exter founded and became

governor of the Central Bank of Ceylon.

In 1953 he was division chief for the Middle East at the World Bank and

in 1954 he returned to the New York Federal Reserve Bank as

Vice-President of International Relations and Precious Metals

Operations. In 1959, Exter left the Federal Reserve to become

Vice-President at First National City Bank (now Citigroup) with special

responsibilities for foreign central banks and governments.

How Exter, an economist, a central banker and investment banker, was to

make a fortune in gold is told by W A Wijewardena, Deputy Governor of

the Central Bank of Ceylon, in John Exter – Central Banker For All Times an article published on

the first anniversary of Exter’s death at 95 on February 28, 2006.

… With a huge fortune made on the gold market by using his own

expertise on the foresight of irresponsible central banking and its

inevitable consequences, Exter took an early retirement in 1972 and

went into private consultancy work.

According to his own admission, the prospect for his fortune on gold

dawned on him after a friendly debate he had in 1962 with his one time

Harvard buddy and Nobel Laureate Paul Samuelson.

In that debate on why the dollar was becoming weak and USA was losing

gold, Exter gave his diagnosis which was based on his experience with

the Federal Reserve System. “Paul, it is very simple. The Fed is

printing too many dollars and they flow out of the country into

foreign central banks who demand gold” Exter is reported to have

said.

But, Paul Samuelson did not accept it and wanted to explain the malady

in terms of productivity differences between USA and other countries,

namely, Europe and Japan. Samuelson’s thesis was that the latter

category of countries had a higher productivity than USA and therefore

the dollar was becoming weaker.

Exter says that he countered Samuelson saying that Japan was in more

trouble than USA, because “the Bank of Japan was running its

printing press even faster than the rest of the central banks around

the world”

Exter had decided then and there that the irresponsible government

expenditure by the Kennedy administration could not keep the dollar

stable in the long run and one day, gold would become the preferred

asset by the world’s nations.

Hence, he says that he converted all his savings into gold based

assets and waited patiently. He was amply compensated in 1971 when the

US government was forced to sever dollar’s link with gold under the

gold exchange standard and allow the gold prices to be determined in

the free market

Overnight, gold prices doubled from $35 per ounce to $70 per

ounce. So did the gold based assets portfolio held by Exter. [At

today’s price of $1690 per ounce, the appreciation of Exter’s gold-based

portfolio would certainly be noteworthy.]

In 1971, Exter had been at the epicenter of US discussions on gold.

President Nixon who closed the gold window in August 1971 was heavily

influenced by the views of Milton Friedman who believed free-market

dynamics would better regulate paper currencies than the rigid

discipline of gold. Friedman was wrong.

Paul Volker, then Under-Secretary of the Treasury under Nixon, had asked

Exter’s advice on the matter. Exter recommended the US raise the price

of gold to accommodate the growing pressure on the US dollar. Volker

said that wasn’t politically possible. Exter then told Volker that

Volker had no choice but to close the gold window. Two weeks later,

Nixon did just that.

Exter later commented on the significance of that act:

The final link between the dollar and gold was broken. The dollar

became nothing more than a fiat currency and the Fed [and especially

the banks] were then free to continue monetary expansion at will. The

result... was a massive explosion of debt.

Gold Wars, Ferdinand Lips, Foundation for the Advancement of Monetary

Education, New York (2001)

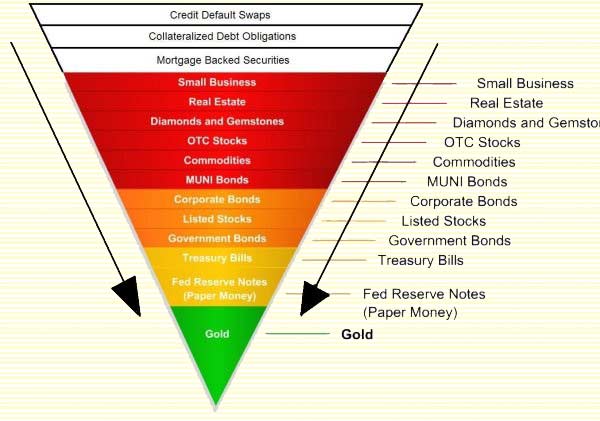

Today, Exter is best known for what is called ‘Exter’s inverse pyramid’,

a model of what will happen during a deflationary collapse when

investors flee increasingly illiquid assets for those offering safety

and liquidity.

Exter's Inverse Pyramid

Ultimately, the fatal flaw in the bankers’ paradigm of paper money is

the hubris of central bankers themselves. Economists had convinced

themselves that by printing money, they could achieve full employment

(Keynes), that without gold, free market forces would stabilize

currencies (Friedman) and that by sufficiently expanding the money

supply a deflationary collapse in demand, i.e. depression, could be

prevented (Friedman) and/or safely offset by increased borrowing

(Keynes).

Both Keynsians on the left and Friedmanites on the right were convinced

that central bank stewardship of paper money was better done without the

constraint of gold. That somehow a house built on sand is preferable to

one built on rock—proving once again that if thought has no bounds

neither does thoughtlessness.

Exter, a friend of Ludwig von Mises, was an adherent of the Austrian

School of Economics, an economic discipline shunned by ‘house’

economists who much preferred the apparent opportunities afforded by

credit and debt. After a discussion of Exter’s Austrian views, Paul

Samuelson told him, “John, you may be right but you’re lonely”.

In a conversation I had with Exter’s daughter, Jane Exter Butler, about

her father, she commented that she wished her father had lived long

enough to see evidence of the economic collapse he had predicted. Exter

had passed away in 2006 two years before the collapse.

I replied that I was certain her father didn’t need any such

evidence. Exter knew with complete certainty he was right—as he still is

today.

John Exter: The Coming Depression and Gold

Exter’s understanding of macro economic factors allowed him to

accurately predict economic events. Exter was certain another depression

was coming and that it would be worse than what had happened in the

1930s. The following is excerpted from a 1981 interview with Exter:

I lived through the great depression. I remember it vividly. I know

what it did to people. I remember the 25% unemployment. So I’m very

unhappy when I have to say this depression is going to be worse.

A time will come when housing prices will weaken so much that many

people who bought houses recently will lose all their equity. Once

they lose their equity, they may say: “Why should I go on paying the

bank? Why don’t I just let them have it?” So I think you’re going to

have defaults on mortgage loans and foreclosures…

More foreclosures, of course, put more pressure on home values. Then

more defaults-and when people start to default on their debts,

troubles multiply. This is one reason why I think we cannot avoid a

banking collapse.

I think people have rather been seeing—in their heart of hearts—that a

depression is coming, or at least some sort of hard times…When your

income shrinks and you have a debt burden, the debt burden becomes

more and more onerous-and you get desperate to borrow…I expect the

government to respond to the deflation by trying desperately to

re-inflate. I expect huge budget deficits. So I expect the dollar

ultimately to become worthless.

The Federal Reserve has already defaulted-gone bust. When I was a

young man, the Fed had to redeem its liabilities in gold at $20.67 per

ounce. As a matter of practice, any of us could go to any bank in the

US and write a $100 check and take out five $20 gold pieces. To

maintain that obligation, the Fed had to avoid borrowing short term

and lending long term. But it didn’t. As a result it had its own

liquidity squeeze and defaulted on its IOUs-the paper dollars

circulating-are not promises to pay anything. They’re IOU nothings.

Paper is worthless as a store of value. The only thing that can give

the US dollar any value is its promise to pay something that is a good

store of value-primarily gold-to the holder. The government now has

welched on that promise, so these paper IOUs are not really worth

anymore than the paper they are printed on.

Sooner or later the public will catch on and the dollar will become

worthless…As the crisis intensifies; as the results of the liquidity

squeeze become apparent and illiquid debtors start to default; as the

depression and deflation set in; gold will once again emerge as the

supreme store of value.

…This is hard for me to say, for I am a banker: On the subject of

income, I’d definitely stay away from banks. Bank deposits are paper

IOUs. A bank owes you Federal Reserve notes. Even Federal Reserve

notes are not good. A bank is even worse because you have the added

risk that it will default on its promise to pay such notes. Remember:

gold never defaults.

"Helicopter Ben" Bernanke and "Kamakazi Shino" Abe are 2013 Co-Sponsors of Exter's Predicted Deflationary Collapse

In October 2011, Jay Taylor, an expert on gold stocks, interviewed

Exter’s son-in-law, Barry Downs. During the interview, Downs discussed

the signs Exter said to watch for, signs which would signal the approach

of the coming economic downturn.

In credit-based economies, aggregate debt levels must constantly grow

and when they don’t, it signals the economy is entering a dangerous

phase; and, if aggregate debt contract, i.e. shrink, that is a far more

dangerous sign. That signals a deflationary depression is beginning; and

in 2008, Downs noted that levels of aggregate debt began to shrink.

Note: Taylor’s interview with Barry Downs begins at the 20 minute mark

and ends at the 30 minute mark, see http://www.voiceamerica.com/episode/56715/pondering-the-possibilities-of-a-greater-deflationary-depression .

This is why the Fed, the Bank of Japan, the Bank of England and the

European Central Bank have thrown caution to the wind in a desperate and

last ditch attempt to save their ponzi-scheme of credit and debt that

has served them so well.

Exter told Barry Downs that once aggregate debt levels began shrinking,

nothing central bankers could do could reverse the process. A tidal wave

of deleveraging debt would sweep aside any and all attempts to inject

enough credit to reverse the process.

QE3 will be no more effective than QE1 nor will QE4 or QE5. No amount of

bond buying, no amount of credit can turn back the tsunami of defaulting

debt that has already begun to gather momentum. The tipping point has

been reached.

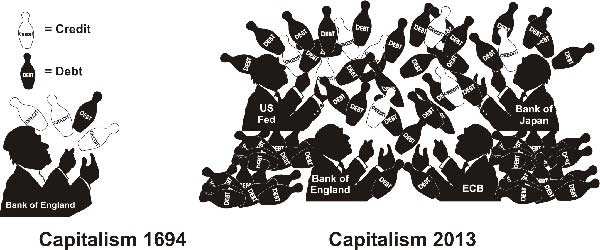

Excessive central bank credit has turned into such levels of debt that

no amount of credit can subsume it. This is why it’s called the end

game. Credit-based capitalism was headed towards this finale in 1694. In

2013, it arrived.

The Japanese central bank said it would aim to achieve a rate of 2

per cent inflation – up from its current goal of 1 per cent – “at the

earliest possible time” by shifting to the kind of limitless stimulus

embraced by the US Federal Reserve and the ECB. - Financial Times, January 21, 2013.

The End Game and the Better Times to Come

Ben Bernanke’s belated attempts to restore US employment levels and

economic growth through even more monetary easing is as futile as Lance

Armstrong’s attempts to salvage his tattered reputation.

No amount of optimism, no amount of denial and no amount of credit can

fix what central bankers themselves broke. Nothing lasts forever. Not

even the dream of bankers who attempted to live off the productivity,

ingenuity and labor of others merely by printing debt-based paper

coupons they could loan to others as money.

Remember: gold never

defaults - John Exter

It might be assumed by readers that my expectation of another depression

is evidence of a pessimistic outlook. Nothing could be farther from the

truth. After the coming collapse, I expect a far better world will

emerge; and, although the process will not be easy, it will be rewarding

beyond our greatest expectations.

John Exter, in his wisdom, firmly believed that when laws fail, human

beings working with moral consciousness could do wonders. - W A Wijewardena, Deputy Governor of the Central Bank of Ceylon

… the vulture feeds neither upon the pastures of the bull nor the stored

up wealth of the bear. The vulture feeds instead upon the blind

ignorance and denial of the ostrich. - Darryl Robert Schoon, Time of the Vulture: How to Survive the Crisis and Prosper in the

Process, 3rd ed. 2012

Buy gold, buy silver, have faith.

My current youtube video, The Cat,

Mouse & the Fiscal Cliff, presents capitalism and America's

fiscal dilemma in a hopefully more understandable context. Best wishes to

all in the coming New Year. The next Mayan long count calendar cycle is

about to begin and it's going to be far, far better than the last cycle.

Buy gold, buy silver, have faith.

Darryl Robert Schoon

www.survivethecrisis.com

www.drschoon.com

www.drschoon.com |