This Is It The party's over The party's over Words by Betty Comden and Adolph Green; Music by Julie Styne; Sung by Nat King Cole

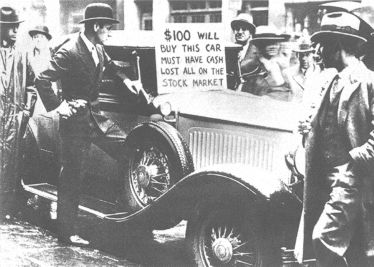

During the roaring 20s (the previous Kondratieff autumn), the large credit expansion and accompanying stock market boom was pretty much an all American affair. The European economies were struggling to recover from the devastation and cost of World War 1. The Europeans, for the most part, were not participants in the credit and speculative bubbles that so captivated their American cousins. However, when these bubbles collapsed following the 1929 stock market peak and October crash, no one, anywhere, could escape the horrendous depression that was its aftermath. This time it is different. As the 4th Kondratieff winter unfolds, most of the world is party to the debt bubble and the congruent speculative mania. The sheer size of this situation is at least 100 times greater than 1920s. Thus, the repercussions are likely to be far more punitive than during the 'dirty 30s'. This huge monetary expansion perpetrated by the Federal Reserve has contributed to the biggest speculation in every conceivable asset category and has been accompanied by unprecedented hubris, greed and outright fraud. This will be punished. The punishment is likely to fit the crime. All cycles are forecasting a major peak not only in stock prices but in the economy as well. This includes, not only the Kondratieff cycle, but also Gann cycles such as the 100 year, the 50 year, the 20 year, the 10 year and the 5 year cycles and according to Gann years ending in 7 are also likely to be bad. So, cycles are predicting a major stock market crash this year. That is right, this year- 2007. Gann wrote that when the time cycle was over there was nothing that anyone could do to alter the inevitable. President Bush, Secretary of the Treasury Paulsen and Federal Reserve Board Chairman Ben Bernanke and anyone else are powerless to control the approaching financial onslaught. Regrettably, many people believe that their leaders can always positively control the future. It is a mistaken belief that always costs them dearly. Every market move is always followed by a reaction. The bigger the up move the bigger the down side. There is no historical comparison with the sheer magnitude of the worldwide investment mania that is currently in force. Thus, the down side threatens to rock the very foundations of capitalism and democracy. As Epicitus put it, "the extreme of any position will ultimately become its opposite." As night follows day, a boom is always followed by a bust; the bigger the boom the bigger the bust. The bust always catches the majority unawares, coming as it does from a zenith of apparent prosperity and speculative excess. At this time, the crowd is imbued with an impetuous fervour encouraged by the affirmations of its leaders. Caution is abandoned. Savings are depleted and copious amounts of debt are assumed. It is the set up. It mirrors the mad dash of the lemmings to the cliffs. In that mad dash the lemmings probably feel the same sense of exhilaration as do the speculators. Both are doomed. Every great credit expansion has always been accompanied by speculative excess. The South Sea Bubble, John law's Mississippi scheme, the great autumn bull markets of the Kondratieff cycle; all are fashioned by massive increases to the supply of fiat money. None of these can compare in sheer magnitude and diversity to the autumn bull market that commenced in August 1982 when the Dow bottomed at 777 points. Everything and anything that could be packaged was sold as an investment. The sub-prime mortgage was just one of these new investment concepts. But the death of this market spells the death of the overall stock market. Confidence has been lost and a contagion of panic will likely ensue. This bull market is now finished and cannot be resurrected as Alan Greenspan was to able breathe new life into the stock market following its peak in the winter of 2000. At that time there was no sub-prime mess to scuttle his efforts. His actions in lowering administered interest rates from 6% to 1% and flooding the banks with money were the very instruments to create the mess in which we now find ourselves. The great Austrian School Economist, Ludwig von Mises wrote, "There is no means of avoiding the final collapse of a boom brought about by credit expansion. The question is only whether the crisis should come sooner as a result of a voluntary abandonment of further credit expansion, or later as a final and total catastrophe of the currency system involved." There has never been any attempt to abandon the credit expansion. Indeed any crisis was simply an excuse to open the monetary spigots. This, then, is the beginning of the total catastrophe of the American dollar, indeed the entire world monetary and financial structure. My deceased friend, Teddy Butler-Henderson, met Alan Greenspan in the 1960's. They apparently discussed the Kondratieff Cycle. According to Teddy, Alan Greenspan confided that he hoped he could be Federal Reserve Chairman at the onset of a Kondratieff winter, because he felt he could defeat winter by substantially increasing the money supply and reducing interest rates to near zero. He had his wish and effected those actions following the 2000 stock market peak. This effectively put winter on hold but massively compounded already excessive credit to the extent that people who should never have had access to loans were willingly given them. Now the credit bubble that Alan Greenspan initiated is beginning to unwind. The process will be horrific and cannot be reversed. Incidentally, Mr. Greenspan told Teddy during that same conversation that if he failed to thwart the Kondratieff winter, it would make what followed 1929 look like a 'Sunday school picnic.' This is what we have to expect. The rapidly advancing monetary crisis centered on the dollar is reminiscent of the previous Kondratieff winter crisis, which was focused on the British Pound. The Pound's collapse in 1931 brought down the world monetary system and caused the abandonment of gold as a backing for money. But in the coming financial and economic chaos that is characteristic of the Kondratieff winter, gold will reassert its traditional role as money. The demand for gold, just as it was in the early 1930's, will be enormous. Since this crisis is much greater than the crisis of the 1930's and international in scope, the rush to own gold is likely to be far more pervasive than it was then.

The unfolding crisis has enveloped the globe. Central banks are pouring money into chartered banks in an effort to stabilize the situation. In the three weeks following the failure of the Bear Stearns funds and other hedge funds, the injection of cash by the world's central banks totaled almost half a trillion dollars. The cash infusions continue.

The son of a British military officer, Ian followed in his father's footsteps and graduated from The Royal Military Academy, Sandhurst. He served as a Platoon Commander in the Cameronians (Scottish Rifles). Four years later in 1967 Ian immigrated to Canada and graduated with a History degree from the University of Manitoba; a decision that has had a profound impact on his career to this day. It was during this period that he began to study the historical trends that ultimately provided the foundation for his Longwave theory. It wasn't until 1983 that Ian entered the financial realm. He worked as a stock broker in Ontario for eight years before working in Management for three more years in Toronto and Vancouver. It was 1998 when Ian determined that the Longwave Theory was too compelling to ignore any longer. He began writing the Longwave Analyst and re-entered the sales side of the business. He accurately predicted the end of the massive equity bull market and also accurately predicted the beginnings of the current gold bull market (1999). By 2003, Ian was the #1 performer at Canaccord Capital (Canada's largest independent brokerage firm) a position he maintained until he left the firm in mid 2005. Ian currently serves as a Vice President of Bolder Investment Partners in Vancouver. This new home affords Ian the flexibility to access institutional investment accounts. The Longwave Theory, in addition to a keen sense of what constitutes a winning deal, has enabled Ian to enjoy meteoric growth over the last 8 years. Today, Ian and his team attend to the needs of their extensive client base and undertake numerous quality junior precious metals financings. ***

|

This is it. The Kondratieff winter is now underway in earnest and nothing can stop it. The huge credit expansion initiated by the Maestro, the past Federal Reserve Chairman, Alan Greenspan, has now reversed. The ensuing credit contraction will be devastating. It will take down creditor and debtor alike and will result in a destructive and frightening deflationary depression.

This is it. The Kondratieff winter is now underway in earnest and nothing can stop it. The huge credit expansion initiated by the Maestro, the past Federal Reserve Chairman, Alan Greenspan, has now reversed. The ensuing credit contraction will be devastating. It will take down creditor and debtor alike and will result in a destructive and frightening deflationary depression. Ian Gordon is a leading financial historian and a top performing retail broker. He is author of the highly acclaimed

Ian Gordon is a leading financial historian and a top performing retail broker. He is author of the highly acclaimed