Pyramids Of Funny Money And Tombs Of Death

A life of private jets and black-tie balls ended with Seth Tobias, a wealthy investment manager and a familiar presence on CNBC, floating face down in the swimming pool of his mansion here. *snip* Along the way, Mr. Tobias collected the trappings of success. He spent days at the Kentucky Derby and nights at Donald Trump's Mar-a-Lago Club. He frequently shuttled by private jet between New York, where he worked in the Seagram Building in Manhattan, and Florida, where he owned two homes. The connection between wealth and death is fascinating. The other day, I read an old National Geographic story about the longest-living, happiest people on earth. Nearly always, they were fairly poor, lived in remote communities where they walked in rough countryside everywhere and ate a frugal diet while sharing everything with extended families. This prudent, restricted, often mountain-oriented lifestyle is the antithesis of the wealthy lifestyle of pampered, spoiled rich people. I have known very rich people who lived frugal life styles yet their children fell into the pit of self-destructive lives due to access to great wealth. Sometimes, the only thing that saved later generations of the extremely wealthy, was to be disinherited. I, for example, was pretty much kicked out of the home at 16 years of age and spent much of my life, fending for myself in difficult circumstances. This was quite bracing. You can't mess around if you are responsible. I know, via knowing people who think this way, the Holy Grail for a number of very rich people is to live as close to 'forever' as humanly possible. The fear of death and the desire to be eternal is very strong in humans. In ancient Egypt, they built up an entire culture based on a futile attempt to live forever. The tombs there are actually time machines rigged to coordinate the dead ruler with the rising and falling of star clusters as well as the planets and the moon. They hoped to escape the darkness of death this way. Great wealth was piled in these supernatural flight machines [which is what they hoped these tombs to be]. But alas, thieves sought out and pulled out of these caves of death, all the wealth. To this day, any tomb hidden in the dark by the families or societies burying the dead with their wealth, are dug up and then used. The artifacts that are dug up are tremendously valuable. There is nothing on earth more valuable than the ancient tombs of the Egyptian pharaohs. The desire to steal from the past as well as plunder the earth and exploit human labor is very strong. The pharaohs who ruled Egypt used the power of the priests and sword to gain their wealth and their hope was to have and hold this forever, even in the afterlife. Rich people today sponsor research in medical advances that could enable them to live forever. There are many curious side issues concerning this. One is our space program: I grew up inside of this culture. I used to talk about interstellar flight and the desire for us to expand beyond our own planet. Namely, this planet and our sun and even our galaxy, are all doomed in the end. The sun has a finite life. Our planet has finite resources. But humans have infinite desires. This is the satanic part of our natures. We are our own gods. And since all things balance out, the yin and the yang, we are also our own demons. And our dreams can also be nightmares. The desire for eternal life runs right next to the urge to commit suicide. When mortal men gain great wealth, the only saving grace for them is to give it away again. If they don't, if they focus on pleasure and indulgences for themselves, they end up dead, but the spiritual death is long before the actual death. This case of a young hell hound going nuts when he got suddenly rich is classic. There are good questions that his wife may have killed him. If so, drowning men like him is ancient. He didn't die and a barrel of Malmsey like one of the Kings named Henry of England. But he may as well have done this. Leona Helmsley was notorious for being a tax cheat and arrogant. She had a fancy tomb built for herself and her husband. The best thing she ever did in her difficult and unhappy life was to disown her grandchildren. This way, they can struggle for life and be productive, pleasant people instead of the opposite. The fact that her miserable dog is unpleasant and annoying is due to it being totally spoiled by this money. People wish it were dead! And this, again, is how death and money are linked. If the dog had no connection with any fortune, it would live a happier life and few people except for maybe some cats, would hate it. All this takes me back to a main theme here: my site doesn't provide easy solutions that means people can escape from the messes made by our pharaohs, our rulers or our economic systems. I want everyone to know that money isn't God nor is danger and striving, bad. The people who live the longest and happiest on earth are seldom living in 'paradise.' Indeed, the lands from which these people arise are often very harsh! The one thing these people who live long have in common is, the love of everyone around them. The elderly are honored and respected. I have seen the elderly abused and mocked by the young. This is very stressful and difficult and depressing. But where they are held in high regard, then the desire to live long is strong. We all want to live long and personally, if a demon were to come to me and offer me great wealth OR long life, I would choose long life even if it means living in a tent [which we did, my son as well, for 10 years!]. I have known a number of people who lived for more than 100 years and were energetic and full of love of life. And virtually none of them were rich. One of them, Mrs. Lake, ran a rooming house next door to me in Brooklyn many years ago. She was always laughing and joking. She had virtually no money. But she had her friends in the local church. She had neighbors who liked her a lot. She shared things unstintingly. She lived in a slum. Yet her days were happy and I enjoyed having her as a neighbor. When I moved away, this wonderful lady actually came over to move furniture! I gave things away that I couldn't move and she wanted to pay me for these things! Money was merely a tool to her. Kisses and hugs were her wealth. My godmother died at 105 years of age. She lived in a big Victorian house. When she was 89 years old, she moved outside and lived in a small pavilion with her wild birds, she was a scientist and wrote books about birds, she did the first study of Californian Condors back before WWI. She lived a very natural and simple life. All I can say is, her gift to me was to teach me how to talk to wild things, how to be a bird. And this is what life is all about: living! And living doesn't mean 'comforts' but rather 'love.' I discuss money a lot because I am struggling to try to explain how 'risky' and 'safety' works and how to avoid the Darkness that lurks in the heart of finances. Now, onto today's news:

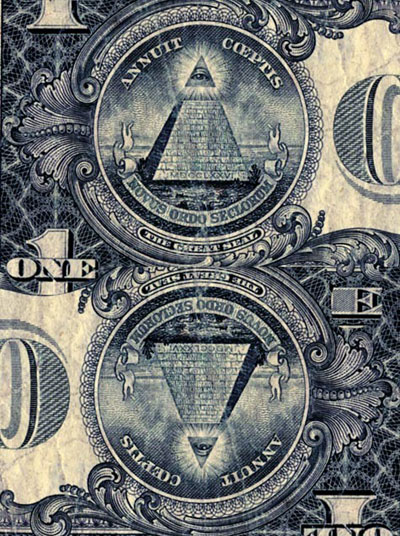

All failed, of course. The pyramids attracted looters like a carcass attracts vultures. Indeed, the thing about our present economic system is, the need for businesses and people to FAIL. This allows vultures to strip out wealth that is buried within enterprises and businesses. In 'Gone With The Wind', Rhett Butler laconically explains to Scarlett when she was raging in hysterics about the death of southern slavery and demanded to know how he got so rich while not having any slaves at all: 'Wealth can be made building a country but EVEN MORE IS MADE BY DESTROYING A COUNTRY.' Minyanville's inverted pyramid shows the huge 'shadow' overhand of derivatives. The educated guess is, the derivatives shadow of the 'real' economy is around $500 TRILLION. This is a vast amount. All the debts held by all nations is only $50 trillion. So how can the derivatives be 'worth' 10X this? The fact is, in the afterlife or rather, hell, debt is wealth. The nature of the Outer Darkness is, all things are mirror opposites of each other. And the co-exist together until some event causes them to switch or merge into one. Example: love can instantly become hate via jealousy. Darkness can become light in a lightning flash. Hard ground can become fluid in a mega-earthquake. The foundation of our wealth, the entire planet's wealth, is this shadow that reflects and amplifies the actual creation of money. Note that NOTHING in this pyramid is 'real'. Slaves, for example, are very real. Their labor is real. But the profits in the form of money is not real. What most slave owners go into debt all too easily and Thomas Jefferson is a prime example of being a nasty nest of opposites, talking about freedom and rights of man while holding slaves! He also was a bankrupt man. George Washington had the nervous fear of the gods sufficient for him to free his slaves upon his death though he didn't have the ability to do this in life, Jefferson's victims were sold at his death to pay for his debts which he accumulated trying to build his Valhalla. The nature of wealth is to generate debts. If this gets out of control, debts grow to infinity. Infinity is where the Gods live, it is where Valhalla rises. And infinity is the vanishing point, too. It is death! And when desire for wealth strives for infinity, for eternal life, it causes all these things to vanish as if they never existed. There are a number of imperial capitals that have vanished and left hardly two stones standing, some, forgotten entirely until the barest outlines are discovered by modern technology! We admire the ruins of these cultures but they were destroyed by humans! And today, we have the infinite ability to destroy all cities. Simultaneously. Humans, when seeking wealth or careless about wealth, can be very destructive. The present pyramid of power and wealth rests upon the US empire. We are the base. We chose to follow the path of infinite debt to gain infinite power and wealth. Our military machine is eating up wealth at a mad rate and it is being paid for via rising debt. And this debt generates other debts! Our exploitation of resources and human labor is causing us to use debt more and more. We have set ALL PARTS of our economic system to run on INCREASING DEBT. This is causing the derivative part of the wealth pyramid to grow to vast proportions, all of this being totally fake, completely false. The rate of growth is set so that all systems MUST run straight upwards...to infinity. Instead of reining in this process and slowing down debt accumulation by spending within our means, spending carefully, trying to live within the means of this planet, we are overspending frantically.

Kass: Ben Stein, Back Off Goldman Sachs By Doug Kass In Sunday's column, the author made a number of allegations that "all started percolating in my fevered brain last week when a frequent correspondent, a gent in Florida who is sure economic disaster lies ahead (and he may be right, but he's not), forwarded a newsletter from a highly placed economist at Goldman Sachs named Jan Hatzius." Since I wrote about Stein's article, I thought it interesting that this man is the one referred to by Stein as an anonymous emailer. Obviously, Stein had to cover up who he was talking about. This way, the NYT didn't have to give Mr. Kass the courtesy of a reply which is typical of the NYT, by the way. But this Kass article shows how poorly many participants in our system understand what is going on. Neither Stein NOR Kass understand the more complex underpinnings of the system. Stein thinks we can go into debt forever and Kass thinks that if a con man says, 'Don't trust me but trust me,' then he has given fair warning when tempting people with goodies. Both men don't understand how we conned ourselves into a financial trap.

Interesting that Kass notices the graveyard and the religious underpinnings to wealth. But his 'buyer beware' is pure silliness. Sellers of 'bonds' are selling...BONDAGE. Yes, this is very much connected with slavery in olden times. When a king made a 'bond' with his knights, this was called 'fee' or 'feudalism'. And this 'bond' meant the knights would have to DIE for the king in battle. The Magna Carta was these bondsmen attempting to control the conditions of their bondage. Indeed, all peasants were held in 'bondage.' This system of reciprocal relations was the basis for society and was IN LIEU OF MONEY. Now, we pay taxes rather than swear fealty on our bond to a king! So when Goldman Sachs comes slithering into the room, suggesting I put my wealth into BONDAGE supporting some certificates that will be repaid in the future, I am giving them my TRUST if I buy these things.

Note the word 'trust' I used earlier. Indeed, the vehicles used to do this are often called 'TRUST FUNDS' for a reason: the sellers [Goldman Sachs and their ilk] are asking us to TRUST THEM. The fact that Kass thinks they can be UNTRUSTWORTHY and this is OK is why our system is collapsing. Excusing fraud is a sign, a system is corrupt. Snearing that we should beware of the guys running our financial system is OK if we extend this to saying, why not arrest these frauds we can't trust? EH? If I lie about things, I get in trouble. So why is it OK for guys who lied to us in the past, hoping to get rich by both selling bonds that are bad AND betting against these same bonds, hoping they fail and the seller [Goldman Sachs] gets richer due to this failure of the bonds they sold? ARGH. Fools! Kass is a #1 fool. Poor Mr. Stein suddenly noticed a major financial fraud and correctly called for an investigation [I mis-typed 'infestation'-hahaha]. His emotions are correct in this instance even if his analysis is totally stupid. Mr, Kass, on the other hand, is an enabler of criminals. Just because the weasels in one division of GS didn't talk to the demons in the other section doesn't matter. The fact that Goldman Sachs was working as an 'honest broker' while the other hand of that SAME entity was PICKING POCKETS doesn't excuse things. It makes it MUCH WORSE. This shows criminal intent on the part of Paulson and the other overlords in this organization! And if Kass is so infantile to think that Paulson and the host of other creeps from Gollum Sachs are not still serving GS, he is too childish to take seriously as a commentator on financial or political matters.

The news is bad, of course. California is overdue for a major earthquake. Like other system 'resets', this looming and inevitable event will shatter the housing market further. Right now, with only massive fires and other messes, the housing business stumbles along, going downhill. This is due to the obvious fact that people accumulated too much PRINCIPAL debt. They were reduced to paying only interest rates and now, they can't pay even that. The system of trust and signing contracts is falling apart rapidly and all fixes are actually making things worse since they are based on ignoring inflation and economic reality. The sole function is to keep housing values higher than they really should be, based on our incomes and ability to pay back any debts.

I am happy that I am not the only person who is against this rescue plan. Goldman Sachs, the deceitful seller of these bonds, is sweating bullets that they may be in legal trouble due to this. So they and the other five big financial houses are anxious to paper over their messes. But on the other side of this ledger is the huge derivative triangle we saw above: the $500 trillion in shadow wealth. This system is losing money rapidly and by freezing rates, it actually makes things worse which is paradoxical. The foolish home owners who played cynical interest rate games with mortgage brokers who were playing with bond sellers at the 5 big banking/investment houses, created this mess. They sold all this to investors, many of whom are hell hounds living on Queen Elizabeth's pirate coves. They are glaring with deadly eyes at all this and might let the system collapse, or rather, cannot stop it from collapsing. For it needs carcasses and dead meat! Death. It needs to feed off of the bankrupts! Far from fearing bankruptcy, they need it! Letting people borrow money for less return is death to these investors. They need greater, not lesser, returns. This is a paradox and of course, life is one long paradox!

Note how Paulson must pet the three headed hell hounds. But they want bones. On top of all this, the relaxation of lending rules troubles them. And it troubles me. Why bother with contracts? The Californian attitude of 'tomorrow is another day,' is pure Scarlett O'Hara. The desire for iron-bound bonds to suddenly become 'whatever' is strong. If only we can change terms within a few months of signing contracts! Heh. Fun, no? Indeed, the people signing these things were hoping for PROFITS. They thought the market would go up and up and their gamble would pay off in less than two years. When it didn't, they defaulted, fast. The only way to fix this is to speed up defaults as much as possible, drop the prices to pre-balloon prices and then deal with the collapse of the shadow economy of derivatives by passing draconian banking laws re-establishing the old banking rules that were increasingly suspended or toyed with ever since the US currency collapse of 1974.

Merkel was elected because she was supposed to be 'law and order' only she wasn't. And she was supposed to draw Germany closer to the US so they could run trade surpluses with the US, of course. But this is all turning to dust and ashes as the German love of a solid, strong currency has been exploited by Asia and the US.

Inflation is the flail that is striking the planet's economic systems. It is a cruel sort of inflation. All things people need are inflating, all things people want for the fun of it, are deflating. Since we can put off buying things we don't absolutely need, the deflation in these goods is meaningless. But inflation of necessities is very vile and very powerful. We cannot stop needing things we need to stay alive! Or keep things running! So when this inflates, far from being 'unimportant', it is strikingly, solid proof of financial inflation! So the inflation scales should be REVERSED. Instead of all nations ignoring or eliminating the price of energy and food, these should be the MAIN data for calculating inflation. That, and taxes, of course. The yen and the yuan both went down yesterday against the dollar. Is this a sign that Japan has a secret accord, a gentleman's agreement to let both drop? It would not surprise me. Both want to have the dollar grow stronger. China pushed the yuan up and up and was rewarded by being struck at hard by the US. So they won't do this anymore, I assume. -Construction starts have been falling steeply, with the total floor area of houses, buildings and other structures on which work has started standing at less than 80% of the year-earlier level in July and under 60% in August and September. *snip* Construction starts have decreased sharply due to confusion over applications for building certification caused by toughened screening criteria under the revised Building Standard Law, which took effect on June 20. Japan is sharply reducing business at home to maintain its depression. Note that this reduction is inspired by the goverment itself. Just like the government raising sales taxes while complaining about deflation! Their 0% system at home is working fine. While their exterior markets grow rapidly. OECD advises Fed,ECB,BoJ to hold rates through '08 PARIS (Reuters) - The OECD advised the central banks of the United States, Japan and the euro zone to leave interest rates on hold for more than a year in a report on Thursday which said more rate cuts by the U.S. Federal Reserve were not needed. *snip* It assumed the European Central Bank, which was meeting on Thursday, would keep official rates on hold at 4.0 percent in the 13-country euro currency zone "over the next couple of years" as a strong euro and fading oil and commodity prices contained inflation. The OECD wants the status quo. Indeed, the forces demanding the status quo are very powerful. Humans like risk and change but they love statis more. So we have a risky static status quo! It is utterly contradictory. And is a prime example of how the Darkness works: in that realm, all things balance out suddenly and quite violently. All things must reverse or merge! And it is not possible to keep the present status quo going for much longer, is it? I am betting the top game players here will use every trick, every magical incantation, to keep it going for as long as possible. Maybe even five years! Even the Chinese want this to run for 5 more years. And the 5 year plan of the Fed, cooked up by a consortium of 'buyer beware' Goldman Sachs goons, just might make it to that point in time! But by then, the derivative part of the pyramid will be much bigger, maybe even over $1000 trillion which is approaching a horizon populated with an awful lot of zeros. Culture of Life News Main Page ***

|

Yet another meditation on the topic of death, money and eternal life. Right now, the people who set up and designed and then profited from the present mal-adjusted financial systems are struggling to keep it going for just a little bit longer. This is not working, of course. But hope springs ever eternal and we see this in the stock market that shoots up like a rocket every time it seems as if the status quo that is destroying America and world trade, will continue. There is no way this mess will trigger good reforms unless it totally crashes. Why we can't reform prior to a crash is simple: too many powerful people make too much money off of crummy, deceitful systems so they want to keep these con games going for as long as possible, sometimes for over 100 years.

Yet another meditation on the topic of death, money and eternal life. Right now, the people who set up and designed and then profited from the present mal-adjusted financial systems are struggling to keep it going for just a little bit longer. This is not working, of course. But hope springs ever eternal and we see this in the stock market that shoots up like a rocket every time it seems as if the status quo that is destroying America and world trade, will continue. There is no way this mess will trigger good reforms unless it totally crashes. Why we can't reform prior to a crash is simple: too many powerful people make too much money off of crummy, deceitful systems so they want to keep these con games going for as long as possible, sometimes for over 100 years.

{kind=link}