|

|

The Investment / Savings Trap (Editor's note: As most of you might have noticed, we frequently post articles in "the War" forum that are concerned with domestic, rather than international issues. I believe that we should consider ourselves at war with anything, anyone, or any group that threatens our survival. I would say the following might be considered a domestic issue. "The Investment / Savings Trap" is the sixth chapter of a book by Mr. Pugsley entitled "The Alpha Strategy", written twenty-eight years ago. We intend to post a chapter each week. -JSB)

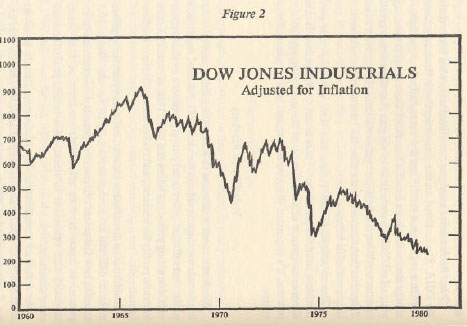

If you are an average saver and investor, you have lost, are losing, and will continue to lose a major part of all your stored wealth to the combined forces mentioned above. You may be among those who have been only vaguely aware that things are not right, and, indeed, even as your purchasing power has been dwindling, may have thought that you were ahead. Even if you could see your losses happening, you may have been unable to figure out how to protect yourself. It's time now to take a hard look at some of the fallacies supporting the savings and investment industries, in order that you can better understand why your only realistic defense is the Alpha Strategy. Storing Wealth - The Three Alternatives Your choices of what to do with your money can be divided into three broad categories. You can lend it to someone, as you do when you make a deposit in a savings account, or buy a bond; you can invest it in a business, or in the shares of a business' stock; or you can buy something tangible, like a piece of real estate, some gold, or a pair of shoes. Of these three categories - lending, investing, and buying - lending and investing are by far the most popular methods used to save for the future. Regardless of the publicity that gold, silver, and collectibles have received over the past few years, the great majority rely on savings accounts, bonds, stocks, and a little real estate as the foundation for their investment programs. Unfortunately, both lending and investing are fraught with traps for the unwary investor, traps that are so broad it is nearly impossible to avoid them, and that are totally camouflaged by a series of false premises promoted by the investment industry. To understand the traps, we must first deal with the false premises. The Illusion of High Returns The first false premise is that high or even modest rates of return are easily attained by the majority of investors. The savings and investment industries survive only by convincing savers and investors that it is possible to earn substantial returns in savings accounts, bonds and stocks. A regular 10 percent annum compound return has long been advertised as attainable and conservative. This seemingly simple objective, 10 percent compound interest, is not only more difficult than it appears, in the long run it is actually impossible. While a few adroit or lucky investors might accomplish a 10 percent return over short periods, the majority are doomed to failure. Let me demonstrate the impossibility of high returns over long periods of time. Peter Minuit bought Manhattan Island from the Indians in 1626. Supposedly, he paid them in beads and trinkets worth about $24. We all figure Mr. Minuit was pretty shrewd, and had the best of the bargain. Well, smart as he was, he wasn't smart enough to get a 10 percent return on his money. Had Peter taken that same $24 and invested it at 10 percent, today, instead of having just the real estate we now think of as New York City, his fortune would amount to some $34,000,000,000,000,000! That is $34 quadrillion, or approximately the value of the total output of goods and services of the United States over the next 17,000 years! Assuming a constant GNP, of course. In short, not one dollar of capital that existed in 1626 has compounded itself at 10 percent in the intervening period. Not one dollar. If it had, today it would be worth over $1 quadrillion, an amount greater than the value of all the man-made wealth in the world. No capital has ever compounded itself at 10 percent for more than a few decades. Why can't wealth grow at 10 percent annually? Because it is not being created that fast. As we noted in the first chapter, wealth is the real things that man creates from nature's raw materials. The growth of real wealth is limited by man's ability to produce, and is reduced by his consumption. Real growth is the amount left over at the end of each year that is added to his stockpile of real goods. Man cannot increase wealth fast enough to meet his consumption needs and have 10 percent left over each year. Suppose man can get his real wealth to increase at 3 percent per year (which is probably still beyond his abilities). That 3 percent real growth will not belong solely to the person who made the capital investment. It will be divided among the product's producers (the business entrepreneurs and managers), and the investors. The entrepreneurs and managers will always get the lion's share, while the passive investor, the little saver who puts up his money and nothing else, will get what is left. In an ideal world, one without inflation, business cycles, and extensive legalized plunder, the passive investor would probably find that his savings, when loaned out, would yield him about 1 percent per year. But, in our economy, the entrepreneurs and investors are not the only people dividing up the spoils. All the plunderers that we exposed in the first five chapters are there first, helping themselves to the rewards of production, eating away at the entrepreneurs' and investors' returns. After the world's production is plundered through taxes, inflation, and regulation, after the business cycle takes its toll, and after the entrepreneur takes his, there is nothing at all left for the investor. In fact, it is worse than that. The investor not only gets no real return, he subsidizes the others. Every year, the total capital invested by savers and investors depreciates. Only the mistaken belief that he is really earning a positive return keeps the investor in the game. Before going further, be aware that there are two types of return: there is the advertised return, and the real, after-tax, after-inflation return. You are not concerned with the returns that are advertised, but only in the return that actually adds to your overall purchasing power. The masses of savers and investors have lost hundreds of billions of dollars of real purchasing power in the financial marketplace simply because they failed to differentiate between the quantity of dollars they hold versus the quantity of purchasing power. How Lenders Lose Simple arithmetic will clarify this point. Let's assume you decide to save money in either a savings account, a bond, a cash value life insurance policy, or by carrying a mortgage or deed of trust. In all these cases you are lending your money. In exchange you receive a promise of repayment at a given time in the future, and some rate of interest to compensate you for the use of your money. The promissory notes you receive when you lend money are debt securities; they might be thought of as claim checks on money. In early 1980, life insurance policies were yielding 3 to 4 percent on the cash value of the policy, savings accounts 5 to 12 percent, and bonds from 6 to 14 percent. First, he must pay income taxes on this return, which might be as high as 70 percent of the interest. Even the small saver who has a modest income will still pay 30 percent to 40 percent of his interest income in taxes. This means the interest retained by the T-bill owner will be between 4 to 10 percent, depending on his tax bracket. meanwhile, during the same period prices were rising at the rate of 18 percent per year, so the value of the saver's principal was falling. Thus, anyone who loaned money to the federal government and received a T-bill in return had to lose between 4 percent and 9 percent of his savings per year, even though he is receiving the highest interest rate in history. Even if the yield was tax-free, the saver still lost 4 percent per year on his capital. Further, most people are not buying T-bills. You are probably saving your money in cash value life insurance policies or bank savings accounts where the yields are much lower than Treasury bills. Your loss for 1980 will probably be 10 percent to 15 percent. Lest you feel alone, during 1979 American savers were lending money at a record pace: they had on deposit over $550 billion in savings accounts, $410 billion in cash value life insurance, and $450 billion in long term bonds. And in every case the real yield, after inflation and taxes, was negative. In today's world, you are a certain loser if you lend out your money. Common Stocks Stock brokers will argue that the answer is to invest in stocks, and will suggest that after-inflation, after-tax yields of 10 percent or more are relatively easy to attain. Are they? Over the last decade the stock market certainly hasn't offered a hedge against the inflation that threatens the bond holder. The Dow Jones Industrials Average went over 1,000 in 1966. By the end of 1980 it was just below that 1966 high. Adjusted for inflation, however, the picture is much worse. Figure 2 shows the value of the stocks in the DJIA between 1960 and 1980, adjusted for the falling value of the dollar. Inflation-adjusted, the average stands below 300. In other words, investors who bet on the thirty largest companies in the country have lost over half of their purchasing power during the last twenty years. Dividends helped to cushion this loss, but after taxes, that help was not enough.

Other stock market averages have fared somewhat better than the DJIA. Stocks listed on the American Stock Exchange have been in a bull market for the last few years, led, of course, by the energy stocks that have benefited so much from the skyrocketing price of oil. Still, there is little to suggest that the average small investor could hope to be in the right stock at the right time, or even if he were, that, on average, the after-tax returns from stocks would keep pace with inflation. The volatility of stock prices, and their generally poor performance over the past fifteen years is not an aberration. It is a direct consequence of the inflation of the money supply. As an investor, it's important that you understand how inflation affects values. Volatility of Markets Stock values are a function of business earnings, and over the last decade earnings have been the victim of inflation. I mentioned earlier that inflation of the money supply causes a business cycle with alternating periods of boom and bust. This, of course, results in erratic profits for business, and makes for erratic stock markets as well. In addition to the inflation-induced business cycle, rising prices make it difficult for businessmen to plan for the future. Not knowing how fast prices will rise next year, businessmen are hard-pressed to know how to price their products or how much inventory and equipment to stock. As a result, profits become more uncertain. As a further complication, the businessman tends to count inflationary gains on inventories as profit, when in reality they are not. I was reminded of this recently when, while on vacation, I went into a health food store to buy some honey. The jar on the shelf was priced at $1.00. As I was paying for it, the proprietress and I began to talk about rising prices. She noted how lucky she was to have bought a large supply of honey two years earlier when prices were much lower. The jar I held in my hand cost her only fifty cents, she noted, while now the same jar would cost her $1.10 at wholesale. Many other items in her inventory had risen proportionately. She then made the comment that she was thinking of expanding her little store, as profits had been good. She assumed that because she had purchased the honey for fifty cents and sold it to me for $1.00, that she was making a fifty-cent profit. I was a bit embarrassed to point out to her that she had not made a profit at all. She would have been better off not to have sold the honey to me, since now she had to take the dollar I gave her, plus a dime from her cash drawer, just to replace the jar on her shelf. She was going to lose a dime the moment she replenished her inventory. To bring her mistake vividly home to her, I suggested that she would be smart to immediately buy the honey back from me at $1.05, since that was five cents less than she could buy it for at the wholesaler. By her way of thinking, she would have bought all the jars on her shelves herself, made a fifty-cent profit, and then turned around and sold them back to herself at $1.10, and made another dime. Like many business owners, she did not understand that a profit is not the difference between original cost and selling price, but the difference between replacement cost and selling price. This error of counting inflationary gains as profits is widespread, and applies not only to inventory, but to costs of plant and equipment as well. Just as a businessman will under-price his merchandise because he uses original cost rather than replacement cost in figuring profit, he will also fail to allocate enough of his income to the replacement of plant and equipment. He may use the fastest depreciation schedule the government allows, but if the depreciation he deducts is a percentage of original cost, he will understate his true cost. The idea of depreciation is to set aside a portion of the equipment's cost as the equipment is being used, so there will be a reserve to replace it when it is worn out. If he does not set aside enough, then he must raise fresh capital to buy new machines when the old ones are gone. By failing to set aside enough, the businessman consumes his capital investment, thinking it is profit. In a world of stable prices, businessmen do not have to worry about the difference between original cost and replacement cost, as it is the same. Under rampant inflation, however, the error is so large that businesses fail because of it. The United States is only beginning to experience high rates of inflation, and it will take businessmen some time before they recognize the importance of this problem. The business cycle and inflation make it difficult, if not impossible, for a businessman to accurately calculate profits, and this leads to erratic planning, which in turn leads to uneven and unpredictable corporate earnings. Investors, of course, are even less able to understand what the true profitability of a business is than are its managers: consequently stock prices become more volatile than profits. Volatile stock markets are not solely a result of the fact that the business cycle and inflation disrupt our ability to calculate profits. That is only part of it. An even greater effect of inflation is produced by the attitudes of savers and investors. As inflation and the business cycle begin to cause fluctuations in markets, savers find that just putting money away in savings accounts and bonds does not keep them even with inflation. Simultaneously, they hear accounts of tremendous profits made by others who are speculating in the now-volatile stocks and commodities. As a consequence, they turn away from conservative savings plans and toward get-rich-quick speculation. People who have no knowledge of investments are found aggressively trading stocks, commodities, gold and all manner of esoteric assets, encouraged by their neighbors, stories in newspapers and popular magazines, and a brokerage industry that capitalizes on the speculative fever. Lest you think that the phenomena I am describing are something new, and unique to our own times, you need only to study history to see the parallels. During the American Revolution, the colonies and the Continental Congress printed huge quantities of notes to finance the war. Soon the notes began to depreciate in value, prices rose, and runaway inflation ensued. One historian noted: The effect of the ever varying currency was bad upon the community...It produced a rage for speculation which infected all classes; all ties of honor and honesty were dissolved. 1 In 1789-1795 France underwent a wild monetary inflation as the government tried to solve the economic problems generated by the French Revolution. Andrew Dickson White, in his book Fiat Money Inflation in France, described what happened to the investment markets. With the plethora of paper currency in 1791 appeared the first evidence of that cancerous disease which always follows large issues of irredeemable currency - a disease more permanently injurious to a nation than war, pestilence or famine. For at the great metropolitan centers grew a luxurious, speculative, stock gambling body, which like a malignant tumor, absorbed into itself the strength of the nation and sent out its cancerous fibres to the remotest hamlets. At these city centers abundant wealth seemed to be piled up; in the country at large there grew a dislike of steady labor and contempt for moderate gains and simple living. 2 You may have heard stories about the hyperinflation that occurred in Germany just after World War I. Money was created in incredible quantities, causing prices to multiply millions of times in a matter of months. Again, investors and markets reacted with predictable abandon. It was observed in Germany (during the inflation) that the circle of speculators was greatly enlarged. Shares were held by speculators in a much larger measure than formerly, when they for the most part had been held longer by investors, who considered them as permanent investments. But in 1920 and 1921 shares passed rapidly from hand to hand, and oscillations of their prices were much more frequent and more violent than formerly ... Business on the German Bourse reached such a condition as to put in the shade even the classical examples of the most violent speculation. 3 Today's volatile investment markets merely reflect the natural tendencies of individuals as they react to the complicated effects of monetary inflation. The values of investments fluctuate wildly as one by one individuals learn that savings accounts and bonds no longer provide security, and as they hear stories of the fortunes being made by speculators in stocks and commodities. There is no certain way to profit in such times, for although there may be a feeling that new wealth is being generated, in reality there is merely a constant transfer of wealth from one group of speculators to another. It is like a giant poker game, with players betting against one another, and with the taxmen and brokers raking a large percentage out of each pot. As inflation gets worse, markets will become even more erratic. Some people will become wealthy, but the great majority will be poorer. Even as you watch the price of some assets skyrocket, and you realize that you could have taken your small nest egg and become wealthy almost overnight, recognize that other assets have fallen, and soon yours may, too. Before getting caught in the speculative mania, soberly reflect on the lessons of history. Prices go in both directions. Most speculators lose in the end. The novice investor who falls for the idea that he can easily take his few dollars and parlay it into a fortune in the stock or commodity market is simply a fool. And you know what they say about a fool and his money. Can You Beat the Averages? Brokers are the first beneficiaries of volatile stock prices, and as the market begins to fluctuate your broker's consistent story will be that he can outperform the averages by aggressively trading. The brokerage industry relies on being able to convince the naive investor that he can beat the other players, an idea that seems believable because it rests on the second great fallacy of the investment industry: that short-term changes in the values of investment assets can be predicted. To expose this fallacy for what it is, let us examine the systems your broker might use to foretell these short-term fluctuations in the values of stocks or commodities. The two most popular systems for selecting stocks are fundamental analysis and technical analysis. Fundamental analysis rests on the assumption that by studying a company carefully, you can estimate future earnings and growth prospects and thereby establish a value for a share of stock of that company. In the commodity market, the fundamental analyst studies supply and demand, and tries to foresee changes that would affect value. Technical analysis, on the other hand, rests on the assumption that past prices form patterns on a chart that indicate what future action is likely to be. The technician does not concern himself with the study of the fundamentals affecting earnings, but looks at the price history of a stock or commodity and attempts to predict future prices, based on the patterns formed by past prices. If you are an investor, the odds are very high that you have relied, directly or indirectly, on fundamental or technical analysis. Investors who follow the strategy of fundamental analysis are accepting the premise that it is possible to forecast earnings accurately enough to make their price prediction valid. Likewise, investors who follow the strategy of technical analysis are accepting a different basic premise: that the past prices of a stock or commodity bear some predictable relationship to future prices. Few investors ever question the validity of these premises. This is a fatal mistake. Technical Analysis The basic premise in all forms of technical analysis is that stock prices, when plotted on a graph, form certain patterns that can foretell future prices. Technicians claim that they can identify all sorts of formations that yield clues to the future, calling them by names such as primary and secondary waves, headand- shoulders, deformed heads, double-tops and double-bottoms, wedges, gaps, fans, and flags. These patterns then tell them when to buy and sell. Some systems, such as the Kondratieff Wave Theory, merely plot the prices and measure the period between highs and lows, then assume that that period will be repeated. Others integrate a variety of information on and beyond just the stock price itself - moving averages are calculated, as are measures of the volume of shares traded, the number of issues advancing or declining, etc. The Dow Theory, for example, contends that there are primary trends in stock prices, in which prices are moving either upward or downward. In the upward trend, each new high is above the old high, and in the downward trend, each new low is below the previous low. Thus, the investor who follows the theory would buy during up-trends and sell whenever prices broke below a trendline, and vice versa. Whenever you see an analyst draw a straight line that touches the tops or bottoms of the prices on a chart, and then intersect it with another straight line when the prices break above or below the first line, you can bet that he is, consciously or unconsciously, following some variation of the Dow Theory. The task of the technician (or chartist, as he is often called) is to recognize those chart formations that indicate price changes are about to occur. While the question the investor usually asks is which technician should he believe (all technicians interpret patterns differently), the question he ought to be asking is whether past prices bear any relationship to future prices at all. David Dreman, an experienced securities analyst and investment adviser, is the author of Contrarian Investment Strategy, a book that must be terribly disturbing to technical analysts. In it, Dreman cites a number of careful studies done using probability theory on the relationship between past and future prices. The first study he mentions is a doctoral dissertation by Louis Bachelier, a brilliant French mathematics student. Written around the turn of the century under the supervision of the internationally famous mathematician Jules Henri Poincare, Bachelier's work demonstrated conclusively that past price movements were useless in predicting future changes. Another early study revealed that a randomly chosen series of numbers, when plotted on a graph in the manner of stock prices, closely resembled actual patterns formed by stock-price actions. A third pointed to the parallels between price patterns and patterns formed by Brownian motion, that random movement of molecules in solution. Some tongue-in-cheek rogues have gone so far as to make up charts from randomly selected numbers and have presented them to technical analysts under the ruse that they were stock prices. They have been rewarded by watching the technicians discover conclusive buy and sell signals in these phony "price" patterns. With the advent of the computer and other new mathematical tools, the relationship between past and future stock prices continued to be tested. Dreman cites a study done in 1963 in which two researchers used advanced spectral analysis on a data base that included seven hundred weeks of price information for various industries in the 1939-1961 period, as well as the Standard and Poor's and Dow Jones' averages for intervals of one to fourteen days over a five-year period. Dreman comments: "All the studies demonstrated that future price movements cannot be predicted from past changes. Without exception, the findings indicated randomness in price - day to day, week to week, even month to month." 4 Over and over again, graduate mathematics students at the world's leading universities, fascinated by the idea of scientifically beating the investment markets, have combed the field of technical analysis for some method that would work. The answer was always the same. Past prices bear no relationship to future prices. Under merciless computer examination, even the Maginot Line of technical analysis, the Dow Theory, crumbled. Again, quoting Dreman, "The size of neither price nor volume changes appeared to influence the direction of future price movements .... One ambitious project analyzed 540 stocks trading on the New York Stock Exchange (NYSE) over a five-year period .... The computers were programmed to recognize 321 of the most commonly used patterns, including head-and-shoulder formations and double and triple tops and bottoms .... When the results were measured, no correlation was found between the buy and sell signals and subsequent price movements." 5 Out of these studies came the Random Walk hypothesis, an idea which captured a few of the clearerheaded analysts after the release of Burton Malkiel's popular book, A Random Walk Down Wall Street, in 1973. This hypothesis maintains that past price and volume statistics do not contain any information by themselves that allow an investor to obtain results superior to those he would achieve by simply buying and holding securities. The hypothesis thus concludes that charting is a worthless forecasting method. Dreman concurs: "No matter how convinced the technician is about the market's or the stock's next move, he has no more chance of being right than he would have tossing a coin." 6 In the face of such overwhelming statistical evidence and the complete lack of any theoretical foundation for the importance of patterns, why does the investment community continue to base so much of its work on technical analysis? There is an overwhelming pressure from investors for some system that can predict short-term price changes. Investors desperately want to believe that they can get rich through speculation. The demand for systems that predict prices is so great that systems are supplied, even though they don't work. Unfortunately, the same law of probability that proves these systems don't work also says that occasionally some system or other is going to appear to work over a short period. If you flip a coin and call it in the air, the laws of probability say that you will call it correctly 50 percent of the time. Repeat the action enough times and there will be sequences where you will be right five, ten or even twenty times in a row. But this does not mean you have the ability to foretell the future, for by the same laws of probability there will be sequences where you will be wrong five, ten, or twenty times in a row. Advisers using these worthless systems are often able to point to short-term results that appear to indicate success, but any person familiar with probability theory will recognize that their "success" is due to nothing more than chance. Our minds play tricks on us. When we really want to believe something, we overlook contradictory evidence, and remember only the signs that support our convictions. So subtle is this potential bias that researchers long ago learned to use double-blind testing techniques in order to prevent test subjects from inadvertently biasing test results. The tendency to misread data is enormous when the analyst's livelihood depends on his ability to convince people that he has a method of beating the market. On the other side, the investor so wants to believe the market can be beaten that when a system fails, he doesn't question the principle, but merely searches for another, smarter technician. All the evidence seems to indicate that technical analysis is no better than flipping a coin as a method of choosing stocks. It would appear that those advisers who use these methods, including those "experts" who write the books, newsletters, and offer high-priced consultations, are nothing more than quacks, charlatans or both. A multibillion-dollar industry has been built around superstition and mysticism. Incredible as it may seem, billions and billions of dollars are being shuttled through investment markets, guided by technicians who are little more than soothsayers and fortunetellers. Fundamental Analysis The fundamentalist studies sales, earnings, dividends, financial strength, competitive position, and other related measures. He believes that stock prices will often diverge sharply from intrinsic value, and his methods allow him to find and buy solid companies that are undervalued and to sell those that are overvalued. The market, he thinks, must eventually recognize the errors of its ways and correct them. Research has demonstrated that earnings and dividends are the most important determinants of stock prices over time. In other words, the value of owning a business (or a share of stock in one) is to enjoy the profits that that business generates. One study of the fifty best and fifty worst performing stocks on the NYSE concluded that " ... stock prices are strongly dependent on earnings changes, both absolute and relative to analyst’s' estimates.... It is clear that an accurate earnings estimate is of enormous value in stock selection." 7 The core of fundamental analysis is thus the development of techniques that will accurately estimate these earnings. Dreman cites numerous studies relating to the ability of analysts using the latest techniques to predict future earnings. the only consistent conclusion that emerges from these studies is that it is difficult to anticipate future earnings within a useful degree of accuracy. Most investors consider earnings increases of 7 to 8 percent normal - and 10 to 15 percent in the above-average growth category. Studies showed that when estimates of future earnings were made by corporate executives, their average error in predicting next year's earnings was 14.5 percent while the estimates of securities analysts were far worse. since forecasting errors of 10 to 20 percent make it impossible for the investor relying on them to distinguish the growth stock from the also-ran, it would appear that fundamental analysis is severely limited. If fundamental analysis requires an accurate forecast of earnings, and earnings can't be accurately forecast, we are back to square one. The inability to forecast earnings is not the only problem blocking an investor from stock market profits. The analyst and investor face a second, perhaps more formidable hurdle. The information that affects present and future earnings of public corporations is available to millions of investors. The prices that the marketplace sets on stocks is the cumulative decision of all of these individuals, each of whom has reached his decision after carefully studying all the available data. This has led many researchers to conclude that the current price of any stock at any time is probably close to an accurate estimate of its real value, given all the existing data. This idea is called the Efficient Market Hypothesis (EMH), and it seems to be borne out by all statistical studies of stock price movements. If a stock price moves up or down, according to the EMH, it merely means that new data was introduced to the market that was not available earlier. Lest you still believe that sophisticated systems of analysis are available to give you an edge in the stock market, you should at least study the performance records, which are public, of the thousands of professional money managers who direct the investments of the big bank trusts, mutual funds, and pension trusts. Not only have these elite professionals with all their sophisticated, computerized analytical tools been unable to outperform the market averages over long periods of time, they have dramatically proven the point by consistently doing worse than the averages. Dreman uses their remarkably poor performance record both to substantiate the basic premise that fundamental and technical analysis are worthless, and to develop a new system that capitalizes on most investors' belief in these fallacious systems. Certainly, in a world in which the majority of investors are following false prophets, the most rational course is to follow a system of contrary opinion. In summary, the stock market will prove a treacherous friend to most small savers and investors. Although there will be periods of rising prices as well as periods of decline, the essential characteristic of stock prices will be their volatility. No matter how badly we would like to believe that a stock trader can beat the market averages, the sad fact is that over the short term stock prices move randomly. Tomorrow's prices have an almost equal probability of being higher or lower. After taking out the broker's commission, the trader has the odds stacked against him just as surely as does the roulette player in Las Vegas. The longterm investor faces a different set of problems. By holding stocks, he avoids the commission drain, but must hope that the broad economic effects of government intervention in the economy will not erode the profits of industry. The odds seem to be against him here, too. In a stable world, which we do not have, investment in the profits of business enterprise will be the best investment of all. In a world of legalized plunder that is rife with charlatans and quacks, the small saver and investor should look to other havens for the preservation of his wealth. Real Estate For two decades hardly a voice has been heard in opposition to the idea that real estate is the road to riches for any prudent small investor, and, indeed, it has seemed to be true. Prices on single family residences have exceeded the general inflation rate by 5 percent per year since 1948; farmland exceeded the general inflation rate by 2.6 percent per year from 1942 to 1972, and by almost 9 percent per year from 1972 to 1977; apartments and business real estate have had less dramatic growth, but have also shown above average price increases. Most homeowners saw the equity in their homes soar during the 1970s. Having bought with 10 percent to 20 percent down, and with prices doubling or tripling on single family homes, the homeowner has multiplied his initial capital by five to twenty times, and all this while enjoying occupancy of the house. This explosion in value has presented many middle-class Americans with the first substantial wealth they have ever had. Residential real estate has been rising so steadily, for so long, that many Americans, especially those under forty, have never experienced a period of declining real estate values, and even most older citizens cannot remember when real estate was not going up. Looking back over the post-World War II era, real estate appears to have been the most stable and profitable of all investments. Since real estate has been rising steadily in value, we tend to accept the idea that it will continue to do so. When we are given reasons for continued price increases like the limited amount of land, population growth, the ability to leverage, and the tangible nature of real estate, we tend to accept them without critical examination. Before you blindly follow the pack and swallow real estate as a panacea for your investment problems, allow me to expose some of the less advertised economic facts behind the value of land and buildings. Real estate achieves its underlying value because it offers us a place to live, grow our food, work, and play. It is one of the goods we use that brings us happiness. But it is only one of our needs, and we are always weighing our desire for all the other goods we enjoy. As mentioned earlier, each of us has limited resources, and we can't have everything. Buying one thing means we forgo another. Our individual desire to own real estate is elastic. If it is cheap enough, we will own a great deal; if it is dear, we may own none. The demand for real estate, then, is dependent on its cost relative to other things. The demand for holding it could fall dramatically under the right set of conditions. There are two potential buyers of real estate: individuals who want to hold the land for use, and individuals who want to hold the land for investment or speculation. As the population increases, more land will be occupied. As the population becomes more wealthy, each individual may decide to own more real estate for his own use. These things put upward pressure on real estate prices. Rising prices, in turn, contribute to the demand for real estate as an investment. The more than people believe real estate is going to rise in value, the more they will buy for investment or speculation, and thus demand, and price, will rise. The proponents of real estate argue that real estate is a good investment because it has a steady history of price appreciation. Since an unusually high rate of appreciation in the past is a danger signal in any investment area, we must ask ourselves what has caused real estate prices to rise so steadily. First, have the earnings from real estate been rising, thus adding to real estate's value as an investment? Second, is the demand for real estate really caused by population growth, limited supply, etc., or is there some other reason? The value of anything is tied to the use people can get from it. Stocks get their value from corporate earnings, and real estate from its crop yields or rent. For real estate to go up endlessly, people would have to be able to get ever-increasing use or profit from it. The value of farmland, for example, is a function of the earnings possible from the crops grown on the land. A speculator may buy land to hold for appreciation, but the appreciation will, in the end, depend on an increased yield from that land. A study of farmland prices relative to farm earnings is revealing. During the period from 1950 to 1971, the price of farm assets averaged 26 times farm earnings. At the end of 1979, that ratio had climbed close to 40 times earnings. What will happen if earnings remain even with the inflation rate, but farmland continues to increase in price at 9 percent per year higher than the inflation rate? In twenty years, farm assets would be priced at 172 times earnings! Do you recall the absurd price-earnings ratios enjoyed by some of the glamour stocks in the late 1920s, as well as the late 1960s? Looking back, everyone sees that the profits of those companies could not have grown fast enough to justify those ratios, yet at the time few people were disturbed. Who cared what the P/E ratio was if the stock was going to double again in a month? Isn't it clear that the same fallacy is present in the case of farmland? The value of a house is no different than the value of stock or farmland: it is a function of the earning power of the house over its lifetime. Traditionally, houses have rented at 1 percent of their value per month. Today that ratio has fallen, and is probably close to 0.7 percent per month. If rents continue to appreciate at the rate of inflation, but houses rise at inflation plus 5 percent, by the year 2000 the average house will rent for less than 0.3 percent of its price, per month. At that point, rental income will barely cover property taxes and maintenance, leaving nothing for debt service or investment return. Already, much residential real estate must be subsidized by its investor-owners, since rents do not cover costs. At some point in the future, either rents will have to rise dramatically, or the value of properties must drop. Investors today have bid the price of real estate up because they firmly believe the price rises of the past will continue. This may be a costly mistake. Also, you can forget about the idea that real estate always goes up in value. It doesn't Real estate prices have fallen many times in the past. Farm real estate fell steadily and dramatically from 1915 to 1942, losing 50 percent of its value. House values lagged behind consumer prices for most of the period between 1910 and 1948. Furthermore, there have been numerous speculative booms in real estate in the past in which prices have plummeted dramatically after a few years of explosive price increases. History records booms and busts in Chicago in the 1830s, Southern California in the 1880s, and Florida in the 1920s. In all these cases, the same elements were present: a period of mild growth followed by a burgeoning belief that the demand for property must continue to increase, and accumulations of unfounded growth assumptions feeding on themselves that created a rush by the masses to get in before it was too late. Do any of these conditions fit today? No one contemplating investing in real estate can afford to ignore the role that government plays in the support of prices. There is a complex web of special interest groups constantly pressuring politicians to favor real estate. Producers of raw materials from lumber to glass to copper depend on real estate construction. Hundreds of thousands of contractors and laborers earn their total livings in real estate construction and development. Thousands of banks hold billions of dollars of real estate as collateral for loans. Millions of investors are involved. Tens of millions of homeowners and tenants are affected. All of these individuals combine to form one of the most powerful political lobbies in the nation. Politicians and bureaucrats have an enormous political stake in supporting real estate prices. How does the government carry out its mandate? The most direct influence is through the mortgage credit market. We already know that the demand for any product depends upon the amount of money individuals have available to purchase it, and thus credit plays a crucial role. whenever the Federal Reserve increases bank reserves, one of the first beneficiaries is the real estate loan market. In addition to the benefits real estate receives from general credit expansion, the government has established a variety of federal agencies to supply credit specifically to this market. The Federal Housing Administration (FHA) guarantees certain mortgages, thus encouraging lenders to offer more favorable loans on real estate. The Veteran's Administration guarantees real estate loans for veterans, again shifting funds toward real estate. Under both FHA and VA programs, government agency guarantees expand the demand for real estate by helping people qualify for loans who would otherwise be ineligible. The Federal National Mortgage Association (FNMA or Fanny Mae) is a congressionally chartered private corporation that was created to invest in and aid the mortgage market. Investors place money with the FNMA, and the money is used to purchase mortgages from banks and savings and loans, thus replenishing their mortgage funds. By structuring favorable programs for certain kinds of real estate, FNMA is able to funnel demand into any real estate sector it cares to bolster. In 1978, it began a two-to-four unit program which provides favorable loans for individuals who want to buy duplexes, triplexes, and fourplexes. Currently, FNMA holds some $40 billion in mortgages. This much capital directed into the real estate market has been a significant factor in the rising prices of real estate. The Government national Mortgage Association (GNMA or Ginnie Mae) is a federal corporation within the Department of Housing and Urban Development that guarantees bonds issued by financial institutions holding FHA and VA mortgages. The government guarantee of payment added to the guarantees made by the FHA and VA makes the bonds very attractive, thus siphoning capital into the mortgage market that might otherwise go somewhere else. In the last decade, GNMA has attracted $50 billion into the real estate mortgage market - again, a very significant factor in the rising prices of real estate. Alan Greenspan, formerly Chairman of the President's Council of Economic Advisers, pinpointed the expansion of mortgage credit as a dominant factor in the U.S. during the last few years. He noted that up until about 1973, mortgage credit rarely grew by more than $15 billion per year. In the past two years, the rate of increase has approached $100 billion annually. Is it any wonder real estate prices have soared? Nor is credit expansion the only way government chooses to favor the real estate lobby. Farm subsidy programs pay farmers for not growing crops, thus encouraging farmers to hold more land that they would otherwise. Price support payments inflate the earnings from farmland, and thus increase land demand and prices. Federal, state, and local governments own incredible amounts of land, all of it removed from the supply available to individuals, and this causes the remaining land to rise in value. Zoning laws restrict use of land, thus effectively increasing prices on unrestricted parcels. Environmental restrictions remove land from use, thus causing price increases on remaining land. What we are talking about is "the sting" in action. All of these government programs are the indirect efforts of individuals to benefit themselves at the expense of others. The result has been an enormous shift of wealth into real estate and away from other markets. Obviously, it has been incredibly effective, but what should be seen is that the rising values of real estate are not a natural market phenomenon of individuals readjusting their value scales because of any growth in the intrinsic value of real estate; rather, prices have risen as a result of a contrived, artificial demand created by government interference. Whenever the government uses force to direct funds toward any market, capital is being misallocated. The steadily rising prices of the past decade cannot continue unless the government can find ways to pump more and more money into this market at ever-increasing speeds. it appears that they may have reached the end of their ability to do so. In summary, real estate prices in general, by any measure, are too high. There is no law of nature that says they cannot continue up for awhile longer, but eventually they must come into line with the values of other assets. The small investor who uses his savings as a down payment on real estate at today's prices is not an investor, but a speculator. This is a role he is poorly equipped to fill. Conclusion Government interference, inflation, taxation, unsound investment strategies, and ignorant or unscrupulous brokers have created the most speculative and dangerous investment markets in the history of the country. Bonds, stocks, and real estate are not the secure havens they appear. They are games in which the odds are as clearly against the small investor as are the odds in any game of chance. On the average, the small investor who participates in these markets probably loses 5 percent to 10 percent of his real wealth every year, and if the economic situation in the country deteriorates, which it certainly will, those losses could become much worse. In this investment game you must ask yourself if you have some special quality that makes you smarter or luckier than the millions of other investors against whom you're playing, many of whom have sizable fortunes and rich sources of information. If you entered a poker game with the very best poker players in the world, assuming you are just an average amateur, what would be your chances of coming away a winner over hundreds of hands? In the poker game of the savings and investment markets, you have an even worse situation, as inflation, taxes, and brokers act like a greedy dealer who rakes in 10 percent to 20 percent of every pot. You may go into the savings, stock, or real estate markets and come away with returns that beat both inflation and taxes, in the same way that you may, through sheer luck, beat superior poker players, or beat the roulette wheel in Las Vegas. But why gamble when the odds are so clearly stacked against you? You do not need to gamble. There is a savings plan that eliminates all the risks and problems. It is part of the Alpha Strategy.

|

|

|

In the past five chapters we explored the numerous ways in which you are being secretly and openly robbed of your earnings. Others are using the guns of the law to steal a major part of everything you produce. If you're frugal, however, even after these confidence men have taken their toll, you may still have accumulated some savings and investments. Assuming you have, you now face the second assault. You face inflation as it waits to sap the purchasing power of your savings; the taxmen who would steal part of your earnings from your savings and give it to the swindlers; the investment salesmen and brokers who make their living off your lack of expertise; the managers who manage the things in which you invest; the occasional schemer who would take your money through fraud; and finally, the convulsions of speculation that grip all investment markets in the aftermath of inflation.

In the past five chapters we explored the numerous ways in which you are being secretly and openly robbed of your earnings. Others are using the guns of the law to steal a major part of everything you produce. If you're frugal, however, even after these confidence men have taken their toll, you may still have accumulated some savings and investments. Assuming you have, you now face the second assault. You face inflation as it waits to sap the purchasing power of your savings; the taxmen who would steal part of your earnings from your savings and give it to the swindlers; the investment salesmen and brokers who make their living off your lack of expertise; the managers who manage the things in which you invest; the occasional schemer who would take your money through fraud; and finally, the convulsions of speculation that grip all investment markets in the aftermath of inflation.

John Pugsley is chairman of

John Pugsley is chairman of