Send this article to a friend:

December

03

2018

|

Send this article to a friend: December |

|

Caved

Home sales are dropping hard. Global growth is slowing hard. Financial conditions are tightening. Stock have been dropping. Never mind all the Fed Crying or Trump expressing his displeasure. Real rates are still negative and the Fed’s tough talk on raising rates came to a sudden halt: Fed’s Powell, in dovish shift, says rates near neutral: “Federal Reserve Chair Jerome Powell on Wednesday appeared to signal the U.S. central bank is nearing an end to its interest-rate hikes, saying the Fed’s policy rate is now “just below” a level that neither brakes nor boosts a healthy economy.

The signs were all over the place in the past 24 hours.

Today before the speech: Fed warns that a ‘particularly large’ plunge in market prices is possible if risks materialize:

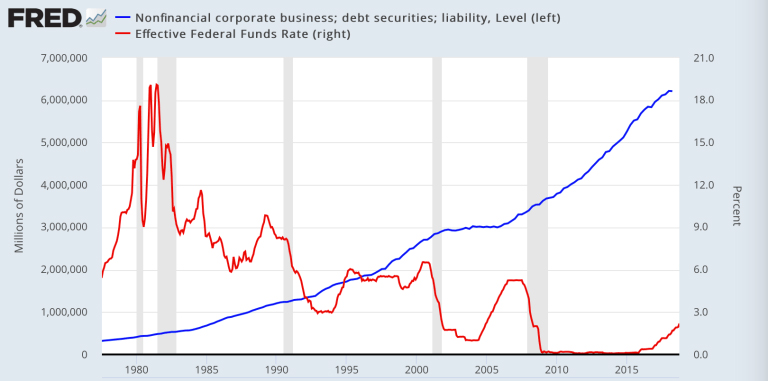

That’s Fed speak for “we’re covering our collective butts”. It gets better: The Fed is now worried about corporate debt: Fed flags concerns over corporate debt in first-ever financial stability report

That’s rich coming from the enablers themselves:

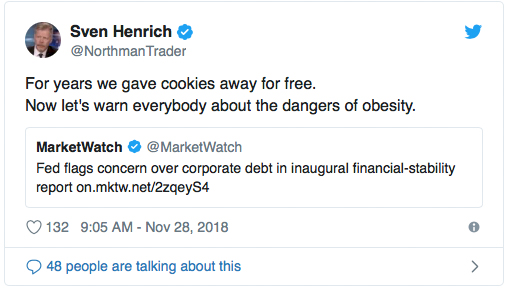

Thats the best analogy I could come with:

And, oh, one has to admire the timing of it all. After all stocks were once again close to breaking their 2009 bull market trend in November:

What better way to avoid all that but with a dovish turn 3 days before month end sending stocks screaming higher. It’s almost as if this was a Bear Trap. No, make no mistake, this was all well crafted, timed and executed. And while the Fed turning dovish again is bullish now is it in the longer term? The Fed just warned about massive downside risks and has admitted what bears have been saying along: They can’t normalize rates, the debt lading global construct can’t handle it. And now they’re stuck and at risk of bringing about the next recession if they were to raise rates further into 2019. And at a point with historically little ammunition to react if things turn sour. Cut rates again? QE coming back? You better believe it. Just a matter of time. But first let’s see how far this dovish turn will take us. Jerome Powell: The Wall Streeters, until today condemned to not get Christmas bonuses this year, salute you. For the latest public analysis please visit NorthmanTrader. To subscribe to our market products please visit Services. All content is provided as information only and should not be taken as investment or trading advice. Any investments, trades, and/or speculations made in light of the ideas, opinions, and/or forecasts, expressed or implied herein, are committed at your own risk, financial or otherwise. For further details please refer to the disclaimer.

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/silver/t24_ag_en_usoz_2.gif)