Send this article to a friend:

November

24

2017

|

Send this article to a friend: November |

|

The Mother Of All Irrational Exuberance

But eventually the mania lost all touch with reality; it succumbed to an upwelling of madness that at length made even Alan Greenspan look like a complete fool, as we document below. So doing, the great tech bubble and crash of 2000 marked a crucial turning point in modern financial history: It reflected the fact that the normal mechanisms of honest price discovery in the stock market had been disabled by heavy-handed central bankers and that the natural balancing and disciplining mechanisms of two-way markets had been destroyed. Accordingly, the stock market had become a ward of the central bank and a casino-like gambling house, which could no longer self-correct. Now it would relentlessly rise on pure speculative momentum---- until it reached an asymptotic top, and would then collapse in a fiery crash on its own weight. That's what subsequently happened in April 2000 when the hottest precincts of the stock market---the NASDAQ 100 stocks----began a perilous 80% dive; and it's also what happened in the broader markets-----including the S&P 500---in 2008-2009, when a thundering 60%plunge unfolded in a hardly a year's time. So with the market raging in self-fueling momentum at the 2600 mark on the S&P 500, we reflect back to the great dotcom crash for vivid reminders of what happens next. That earlier meltdown is especially pertinent because in many ways today's stock market mania is far less justified than the one back then. Moreover, the dotcom version was also the first great central bank fueled bubble of modern times---a creature that market participants understandably did not fully grasp. Yet to its everlasting blame, the Fed's subsequent experiments in reflationary bailouts of the casino gamblers has only caused Wall Street's muscle memory to atrophy further. Indeed, after 30 years of Greenspan-style Bubble Finance and two devastating crashes, Wall Street is even more credulous today than it was on the eve of the tech crash. Back then, in fact, there was a considerable phalanx of Wall Street old-timers who warned about the dotcom insanity. Now almost no one sees this one coming. Indeed, today's nutty forecast by Goldman Sachs that the S&P 500 will hit 3,100 by the end of 2020 makes Greenspan's earlier bubble blindness look clairvoyant by comparison. In hindsight, Alan Greenspan did see it coming early on--- when he broached the "irrational exuberance" topic in passing during a speech in December 1996. Unfortunately, he has mostly been dinged for being allegedly way too early in making the call. In fact, we don't think he was making much of a call at all---he's was just musing out loud with no intention of reining-in the then rampaging bull. What he actually did was to conduct several gumming fests at subsequent Fed meetings and then diffidently raised interest rates a single time by a pinprick 25 basis point in April 1997. After that the Maestro (so-called) apparently forgot all about "irrational exuberance" even as that very thing soon began infecting the entire warp and woof of the financial system. In fact, Greenspan's fatuous amnesia became so pronounced that by the very eve of the dotcom crash in April 2000, he proved himself blind as a bat when it comes to central bank created bubbles. Said the Maestro to a Senate committee on April 8 when asked whether an interest rate increase might prick the stock market bubble:

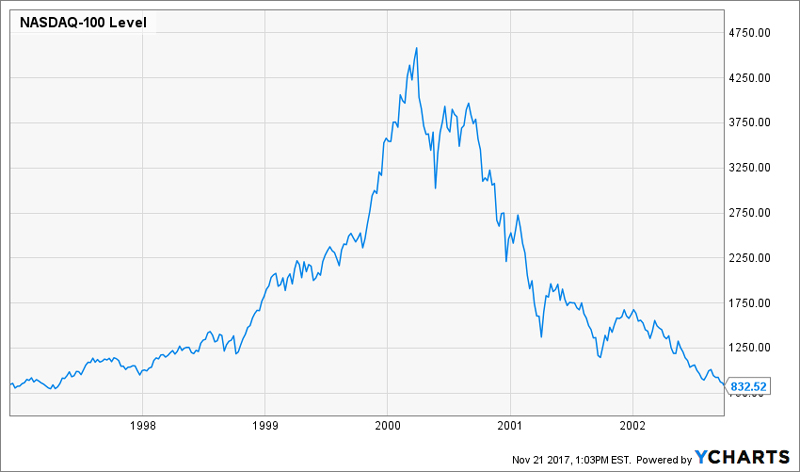

At least he got the latter part right. After the NASDAQ had risen from 835 in December 1996 to 4585 on March 28, 2000---or to an out-of-this-world 5.5X gain in 40 months----Greenspan wasn't even sure he was seeing a bubble! Accordingly, he apparently didn't have that capacity to predict an imminent decline---although the 51% crash to 2250 by the end of the year would seem to have been exactly that. Indeed, after unloading the above tommyrot at the tippy-top of the NASDAQ-100 bubble, Greenspan proved himself a clueless, pitiable fool when this giant bubble deflated by81% over the next two years. In fact, the index ended up in September 2002 almost exactly where it had been when Greenspan spoke the words "irrational exuberance" and then moved along with the Fed's printing press at full speed---claiming there was nothing to see.

Still, back then you could almost have made a (lame) excuse for the Fed chairman's bubble blindness. The Maestro was operating in the early days of monetary central planning and wealth effects management, and its potent capacity to unleash rampant speculation in the financial system was not yet fully understood----even if the underlying monetary theory defied all the canons of sound finance. Moreover, in addition to rampant bubbles in the financial market, the Fed's money pumping during the 1990s did also seem to be producing some seemingly robust real world effects on main street and in the booming new tech part of the economy. And, in turn, these positive macroeconomic developments were unfolding in a global political/strategic environment that had suddenly become more benign that at any time since June 1914. Indeed, the outside world fairly buzzed with positive developments. These included the fact that the internet/tech revolution still exuded adolescent vigor, the government's fiscal accounts were nearing balance for the first time in two decades, the vast market of China was convincingly rising from its Maoist slumber and the Committee To Save the World (Greenspan, Summers and Rubin) had just rescued Wall Street with alacrity from the Long-Term Capital Management (LTCM) meltdown. Likewise, Europe was launching the single currency and expanding the single market. In place of the Soviet Union, which had disappeared from the pages of history in 1991, Russia, its breakaway republics and the former Warsaw Pact (captive) nations were all bursting out of their statist chains and experimenting with home grown capitalism and reaching out to the west via rising trade and capital flows. In the US, the combination of the end of the cold war and the internet revolution contributed a doubly whammy to growth and prosperity. When defense spending fell from 7% of GDP on the eve of the Soviet collapse to under 4% by the year 2000, substantial domestic resources were released for private investment and a resulting substantial productivity uplift. In fact, real private nonresidential investment grew at 7.3% per year from the 1990 pre-recession peak through 2000. That was more than double the still respectable 3.4% rate recorded between 1967 and 1990; and causes the anemic 1.4% real growth of fixed investment between the pre-crisis peak (2007) and 2016 to pale into insignificance.

Notwithstanding all of these positives, however, the great bull stock market of the late 1990s ended-up getting way ahead of itself. That was especially the case during the next 18 months after the Fed's heavy-handed and somewhat panicked bailout of LTCM in September 1998 had confirmed to the newly energized casino gamblers that the Greenspan Put was most definitely operative. In the Great Deformation we tracked 12 of the highest-flying big cap stocks ("Delirious Dozen") during the period between Greenspan's December 1996 speech and the April 2000 dotcom bust. During this 40-month period, the combined market cap of these 12 leading momo stocks---including Microsoft, Cisco, Dell, Intel, Juniper Networks, Lucent, AIG, GE and four others---soared from $600 billion to $3.8 trillion. That eruption did indeed give the notion of trees which grow to the sky an altogether new definition. To wit, the total market cap of the Delirious Dozen grew by 75% per annum for nearly 4 years running; and the future outlook was claimed to be even more fantastic. For instance, as of mid-2000 Intel was valued at $500 billion and traded at 53X its $9.4 billion of LTM earnings. Yet it was argued that this nosebleed multiple was more than warranted because the company had grown its net income from $1 billion to $9.4 billion during the previous decade, and that there was nothing but blue sky ahead. Here's the thing, however. Intel was and is a great company that, in fact, has never stopped growing. But during the 17 years since mid-2000, its net income growth rate has sharply slowed to just 1.79% per annum; and its $12.7 billion of LTM net income for September 2017 is valued at only 15.7X or $210 billion. In short, at the peak of the tech bubble Intel's market cap had vastly outrun its long run-earnings capacity. Even today it has only earned back 40% of its bubble peak valuation. Likewise, Cisco was valued at $500 billion in July 200 and sported a 185X PE multiple on its $2.7 billion of LTM net income. And it, too, has continued to grow, posting LTM net income of $9.7 billion for September 2017. Yet today's earnings are accorded only a 19X multiple after 17 years of 2.4% per annum growth; Cisco's current $181 billion market cap, in fact, sits at just 36% of its bubble peak. Even the mighty Mr. Softie has experienced pretty much the same fate. Back in mid-2000, it posted $8.3 billion of LTM net income and was valued at $600 billion or 72X. Today its net income has tripled to $23.1 billion, but its PE multiple has receded to just 29X. Stated differently, Microsoft's net income has grown at 6.1% per annum since the company vastly outran it true value back in early 2000. Accordingly, its market cap gained just 0.4% per annum during the last 17 years. That is, it has taken one of the greatest tech companies of all time upwards of two decadesto earn back its peak dotcom era bubble valuation. And when it comes to the industrial and financial conglomerate empire that Jack (Welch) built, the story is even more dramatic. GE's mid-2000 market cap of $500 billion stands at just $155 billion today; and its PE multiple of 60X has shrunk to just 22X. In short, that was irrational exuberance back then, and it did not take long for the vast quantities of bottled air in the market cap of the Delirious Dozen to come rushing out. By the bottom in September 2002, four of these companies had vanished into bankruptcy and the market cap of the survivors had imploded to just $1.1 trillion. That's a fact and you can look it up in the papers. In less than 30 months, $2.7 trillion of market cap had literally ionized. And these were the leading companies of the era. None of them, it might be noted, were valued at 280X shrinking net income, as is Amazon today; or at infinite PE multiples like much of the biotech sector and momo hobby horses like Tesla. More importantly, the promising macro-economic situation at the turn of the century has given way to a world precariously balanced on $225 trillion of debt and the tottering $40 trillion Red Ponzi of China. Likewise, the benign geo-strategic environment of that era has long since disappeared into the madness of RussiaGate, endless wars in the middle east and Africa and the incendiary confrontation between the Fat Boy and the Donald on the Korean peninsula. Finally, after 30 years of rampant monetary expansion the central banks of the world have been forced to reverse direction and begin to normalize interest rates and balance sheets. And that now incepting and unprecedented experiment in massive demonetization of public debts is coming at a time when----after 8 years of business cycle expansion---the US, Japan and most of Europe are running monumental "full-employment" budget deficits. Even then, these reckless fiscal policies are happening in the teeth of a demographically driven tsunami of pension, medical and welfare spending. For the period just ended, the S&P 500 companies earned $107 per share on an LTM basis---or just 2% more than the $105 per share posted back in September 2014; and also only modestly more than the $85 per share recorded way back at the June 2007 pre-crisis peak. Stated differently, on a trend basis S&P 500 companies have grown their earnings at 2.33%per annum over the last decade. How that merits a 24.3X PE multiple on today's 2600index price is hard to fathom---let alone Goldman's 3100 target for 2020. Indeed, just to retain today's absurd PE multiple would require $130 per share of GAAP earnings by 2020 at the Goldman target price. That's right. By the end of 202o we would be implicitly in the longest business expansion in recorded history at 140 months (compared to 118 months in the 1990s), Furthermore, the term structure of interest rates will be 200-300 basis points higher according to the Fed's current policies, while the US treasury will be running $1 trillion plus annual deficits and experiencing recurring debt ceiling and financial crises. Even then you would need 7% annual earnings growth to hold onto today's 24.2X PE multiple at the Goldman S&P 500 target. As we said, relative to today's casino madness and the Goldman fairy tale hockey stick, Alan Greenspan circa April 2000 looks like a model of sobriety by comparison. So if that was Irrational Exuberance back in April 2000, what we have now is surely the mother thereof.

davidstockmanscontracorner.com

|

Send this article to a friend:

|

|

|

You could almost understand the irrational exuberance of 1999-2000. That's because everything was seemingly coming up roses, meaning that cap rates arguably had rational room to rise.

You could almost understand the irrational exuberance of 1999-2000. That's because everything was seemingly coming up roses, meaning that cap rates arguably had rational room to rise.

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/silver/t24_ag_en_usoz_2.gif)