Send this article to a friend:

November

26

2014

|

Send this article to a friend: November |

|

Brent Plunge To $60 If OPEC Fails To Cut, Junk Bond Rout, Default Cycle, "Profit Recession" To Follow

By way of background, the key reason OPEC is struggling to remain relevant is because, as the FT reported over the weekend, "US imports of crude oil from Opec nations are at their lowest level in almost 30 years, underlining the impact of the shale revolution on global trade flows. The lower dependence on imports from the cartel, which pumps a third of the world's crude, comes amid advances in hydraulic fracturing that has propelled domestic US production to about 9m barrels a day – the highest level since the mid-1980s." The US "shale miracle" is best seen on the following chart showing the total output of the US compared to perennial crude powerhouse, Saudi Arabia:

It is this shale threat that has become the dominant concern for OPEC, far beyond whatever current US national interest are vis-a-vis Ukraine, and Russia's sovereign oil revenues, and as reported previously, Brent has to drop below to $75 or lower for US shale player to one by one start going offline.

Unfortunately, it may bee too little too late for the splintered cartel. As Bloomberg reports, "the days when OPEC members could all but guarantee consensus when deciding production levels for oil are long gone, according to a veteran of almost two decades of the group's meetings."

So if OPEC is unable to reach an agreement, what is the worst case? Back to Reuters, which says that "The market would question the credibility of OPEC and its influence on global oil markets if there was no cut," said Daniel Bathe, of Lupus alpha Commodity Invest Fund.

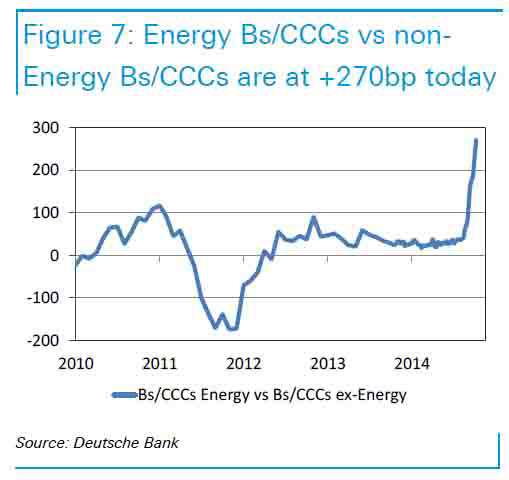

It's not all downside: there is a chance that OPEC will agree on a 1 million barrel or more cut, which would actually send prices higher: "The market really wants to see that OPEC is still functioning ... if there is a small cut, with an accompanying statement of coherence from OPEC that presents a united front, and talks about seeing demand recovery, and some moderation of supply growth, then Brent could move up to $80-$90." "Prices below $80 are putting significant strain on the cartel's weakest members such as Venezuela," said Nicolas Robin, a commodities fund manager at Threadneedle. He said a bigger cut -- of 1 million bpd or more -- was an "outlier scenario", but such a move would rapidly push prices above $85. Then again, even thay may be insufficient if the market prices in an ongoing deterioration in global end-demand: "Doug King, chief investment officer of RCMA Capital, sees Brent falling to $70, even with a cut of 1 million bpd." So in a worst case scenario, where Brent does indeed tumble to $60, what happens? We already know the answer, as it was presented in "If WTI Drops To $60, It Will "Trigger A Broader HY Market Default Cycle", Says Deutsche":

This explains why the HY space has been far less exuberant in recent weeks, and the correlation between HY and the S&P 500 has completely broken down.

Finally it is not just the junk bond sector that is poised for a rout should there be no meaningful supply cuts later this week: recall that in another note over the weekend, DB said that should crude prices take another leg lower, then the most likely next outcome is a Profit recession, which while left unsaid, will almost certainly assure a full-blown, economic one as well.

So keep an eye on Vienna this Thanksgiving: the black swan may just be coated with an layer of crude oil this year.

|

|---|

Send this article to a friend:

|

|

|