|

|

Alert: QE II Has Lit the Fuse

For a very long time, I have been calling for, expecting, and otherwise anticipating the day that the Federal Reserve would begin openly monetizing government debt. Intellectually knew the day would come, but in my heart I hoped it wouldn't. But with the Fed's recent decision to directly monetize the next eight months of federal deficit spending, that day has finally arrived. I have to confess, while my prediction has proven accurate, I'm still stunned the Fed actually did it. In this report I examine the risks that this new path presents, what match(es) may finally ignite the decades-old pile of dry fuel, what the outcomes are likely to be, and what we can and should be doing in preparation. How is this Quantitative Easing (QE) different from the prior QE?There are two main points of departure between the two QE programs:

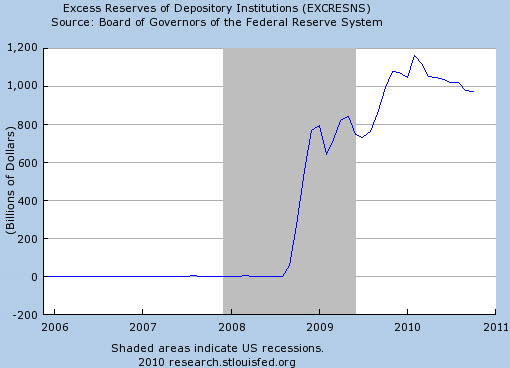

Let's take the second point first. QE I consisted of all sorts of liquidity efforts that went by various acronyms, but the main act was the accumulation of some $1.25 trillion in MBS and agency debt. Some might note that taking MBS paper off the hands of financial institutions, which then bought Treasuries with the cash, is little different than the recently announced QE II program, because at the end of the day, money was printed and Treasuries were bought. In this regard, they're right. But let's be clear about something: The first QE effort had the specific aim of repairing damaged bank balance sheets. That is, banks and other financial institutions had made some colossally poor and risky financial moves that didn't work out for them. They needed some help, and the Fed was more than happy to oblige by handing them free money to patch up their losses. Of course they didn't do this outright by saying, "Here take this money!" -- they did it somewhat sneakily. But when the Fed hands you huge piles of money (for your dodgy debt) and then lets you park that very same money in an interest-bearing account at the Fed, there's really no difference between that and just handing you free money. No difference at all. If the Fed ever offers you free money that you can then park in an interest-bearing account with the Fed, you should take them up on it, and you should do it as much as they will allow. Indeed, that's exactly what happened. These parked funds are called "excess reserves," and this chart clearly displays the massive program undertaken by the banks and the Fed:

So QE I (and the 'Stealth QE' program) was directly aimed at banks to help them repair their balance sheets and make them whole after their terrible decisions and losses. It turned out, though, that fixing the banks did absolutely nothing for Main Street. The rest of the economy remained mired in a rut, with banks either unable or unwilling to make additional loans. They kept their QE lotto winnings and parked them with the Fed. QE II, then is about getting thin-air money to the government which, the Fed rightly assumes, will immediately spend and push out into the economy. Here's how the head of the Dallas Fed, Richard Fisher put it in a recent talk he gave:

There it is in black and white. You might want to read it a couple of times to let it sink in. The Fed is directly monetizing the next eight months of excess(ive) spending by the federal government and is doing it despite being perfectly aware of the extent to which history is littered with the remains of those who have traveled this path before. Presumably, we are supposed to console ourselves with the idea that the Fed will be successful where others have failed, and sometimes failed miserably. Yes, we are talking about the same Fed that fueled that last two destructive bubbles by keeping interest rates too low for too long; failed to see the housing bubble for what it was as late as 2007, and apparently entirely lacked the capability to foresee any of the current mess. That Fed. The one run by the gentleman who said this to the House Budget Committee on June 3, 2009,

In summary, the difference between QE I and QE II is that QE I went primarily to the banks and QE II is going directly to the government. While this may be something of a semantic difference, it shows that the Fed is changing its strategy again. We might ask: Why this shift, and why now? How is QE II Being Viewed Outside of the US?In a word, poorly. The German finance minster called the Fed's application of US monetary policy "clueless" and argued that the Fed decision would "increase the insecurity in the world economy." China was predictably unhappy too, but initially used more diplomatic language:

All of the above is loosely coded diplomatic speak for "The US really bummed us out here; it should have stuck to the agreements we thought we had after the Pittsburg meeting. Going off-script like this was really not appreciated. We think an intervention is needed here." Later, an advisor to the Chinese central bank went further and called the US actions "absurd."

Here are a few other selected expressions of dismay from around the world:

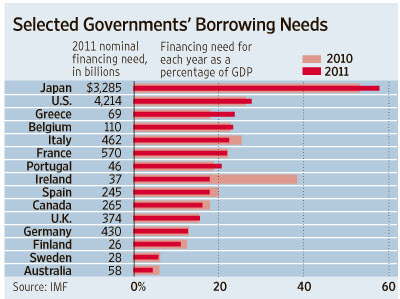

In summary, QE II has been described by several major trading partners as "clueless," "abusive," "absurd," and even resulted in a lecture from Greece on the subject of printing. By the time you are getting lectured by Greece on monetary actions, it might be time for a bit of self-reflection. It is not too strong to suggest that something of a tipping point has been reached in regards to how the US is perceived as a leader on financial and monetary matters. Why this is importantOkay, so the US's international friends are a little upset with it for deciding to print up the better part of a trillion dollars out of thin air. What's the big deal? The big deal here is that the OECD countries have a monster borrowing bill set for next year. There needs to be some level of cooperation, and fair play is going to be required in order to pull this off:

Having the perception out there that the US is being run by clueless (or 'abusive') individuals is not going to help the situation much. In order for the requisite levels of borrowing to be pulled off in a smooth and uninterrupted fashion, there can't be any hits to confidence and no major disruptions can happen. Everything has to run with clockwork precision. It is against this backdrop that I view the profoundly undiplomatic statements directed at the US as quite a bit more serious than some other observers. ConclusionBy choosing the path of money printing (instead of austerity like the UK), the Fed has decidedly placed the US on a very risky course. I see the outcomes as almost binary: Either this works, or it doesn't. If this gamble works, business will pick up, unemployment will drop, tax revenues will flow again to the states and federal government, the sun will continue to rise in the east, and roses will bloom in the spring. If the gamble fails? Then we can envision an enormous devaluation event for the US dollar, with the Fed having to choose between defending the dollar (via rising interest rates) or preventing the federal government from a fiscal emergency brought about as a consequence of rising interest rates. And by "fiscal emergency" I mean being forced to slash expenditures by as much as 50% in order to service rapidly escalating interest-carrying costs on the short-term portion of the fiscal debt load. But that's a death spiral, because cutting government spending is the same as cutting GDP (it's practically 1:1), and every cut to GDP leads to lower revenues, which will necessitate more expenditure cutting, et cetera and so on, until 'the bottom' is reached. I wish there was some sort of middle ground on this one, but I can't quite see it. Either the Fed's efforts work or they don't. Let's hope for success. In truth, I've long predicted that the day would arrive when the Fed would monetize government debt, but I hoped that it would never come. Because hope alone is a terrible investment strategy, I prepared for this event years ago by accumulating gold and silver as the core of my portfolio. But now the rules have changed again, we are on a slippery slope, and gold and silver were always meant to be my "transition elements" put there to help shepherd my wealth through the transition period as the world's fascination shifted from "paper" to "things." Now that we're "almost there" in terms of the required shift in perception necessary to call an end to one period (the "king dollar" period) and mark the beginning of another, it's time to begin considering the places, timing, and ways that these transition elements can be redeployed to take advantage of the second part of this story. In particular, concerned minds are looking for answers to questions about what might happen next and how to insulate oneself from monetary madness. These questions are explored in detail in Part 2 of this article (free executive summary; paid enrollment required to access).

I think it’s important that you understand who I am, how I have arrived at my conclusions and opinions, and why I’ve dedicated my life to communicating the to you. First of all, I am not an economist. I am trained as a scientist, having completed both a PhD and a post-doctoral program at Duke University, where I specialized in neurotoxicology. I tell you this because my extensive training as a scientist informs and guides how I think. I gather data, I develop hypotheses, and I continually seek to accept or reject my hypotheses based on the evidence at hand. I let the data tell me the story. It is also important for you to know that I entered the profession of science with the intention of teaching at the college level. I love teaching, and I especially enjoy the challenge of explaining difficult or complicated subjects to people with limited or no background in those subjects. Over the years I’ve gotten pretty good at it. Once I figured out that most of the (so-called) better colleges place "effective teacher" pretty much near the bottom of their list of characteristics that factor into tenure review, I switched gears, obtained an MBA from Cornell (in Finance), and spent the next ten years working my way through positions in both corporate finance and strategic consulting. From these experiences I gather my comfort with numbers and finance. So much for the credentials. The most important thing for you to know is the impact that the information that I’ve now placed on this site had on me. Let’s do this as a Before and After. Before: I am a 40-year-old professional who has worked his way up to Vice President of a large, international Fortune 300 company and is living in a waterfront, 5 bathroom house in Mystic, CT, which is mostly paid off. My three young children are either in or about to enter public school, and my portfolio of investments is being managed by a broker at a large institution. I do not really know any of my neighbors, and many of my local connections are superficial at best. After: I am a 45-year-old who has willingly terminated his former high-paying, high-status position because it seemed like an unnecessary diversion from the real tasks at hand. My children are now homeschooled, and the big house in Mystic was sold in July of 2003 in preference for a 1.5 bathroom rental in rural western Massachusetts. In 2002, I discovered that my broker was unable to navigate a bear market, and I’ve been managing our investments ever since. Since that time, my portfolio has gained 166%, which works out to a compounded yearly gain of 27.8% for five years running (whereas my broker, by keeping me in the usual assortment of stocks, would have scored me a 38% return, or 8.39%/yr). I grow a garden every year; preserve food, know how to brew beer & wine, and raise chickens. I’ve carefully examined each support system (food, energy, security, etc), and for each of them I've figured out either a means of being more self-sufficient or a way to do without. But, most importantly, I now know that the most important descriptor of wealth is not my dollar holdings, but the depth and richness of my community. I hope you find what I have to offer here useful. All the best, Chris Martenson |

|

|

Now, it's also true that the Fed does not pay a lot of interest on this money, just 0.25%, but on a trillion dollars that pencils out to some $2.5 billion a year, handed straight over to the banks. I call this program "Stealth QE" because it is nothing more than printing money and handing it over to the banks, with a slight bit of complexity thrown in just to put the dogs off the scent. A couple of billion may not sound like much these days, but I raise it to illustrate the many and creative ways that QE I was about getting the banks back to health, and not much else.

Now, it's also true that the Fed does not pay a lot of interest on this money, just 0.25%, but on a trillion dollars that pencils out to some $2.5 billion a year, handed straight over to the banks. I call this program "Stealth QE" because it is nothing more than printing money and handing it over to the banks, with a slight bit of complexity thrown in just to put the dogs off the scent. A couple of billion may not sound like much these days, but I raise it to illustrate the many and creative ways that QE I was about getting the banks back to health, and not much else. Just ponder those numbers for a bit. The average borrowing across 15 major developed countries is 27 percent of GDP(!) Ask yourself how dependent the entire OECD world is on a smoothly operating financial system in order to merely function next year.

Just ponder those numbers for a bit. The average borrowing across 15 major developed countries is 27 percent of GDP(!) Ask yourself how dependent the entire OECD world is on a smoothly operating financial system in order to merely function next year.  Executive summary: Father of three young children; author; obsessive financial observer; trained as a scientist; experienced in business; has made profound changes in his lifestyle because of what he sees coming.

Executive summary: Father of three young children; author; obsessive financial observer; trained as a scientist; experienced in business; has made profound changes in his lifestyle because of what he sees coming.