Send this article to a friend:

October

27

2020

|

Send this article to a friend: October |

|

Creditors Finally Wake Up To An Apocalyptic Reality: Bond Losses As High As 99%

Fast forward to today when Bloomberg picks up on what we said almost five years ago an in "Bond Defaults Deliver 99% Losses in New Era of U.S. Bankruptcies" writes that more and more, bondholders are fighting over recoveries as low as 1 cent. The story should be familiar as we have discussed in constantly in recent months: in a post-covid world, where bankruptcy filings are surging, many lenders are coming to the realization that their claims are almost completely worthless, just as we warned would happen in 2016.

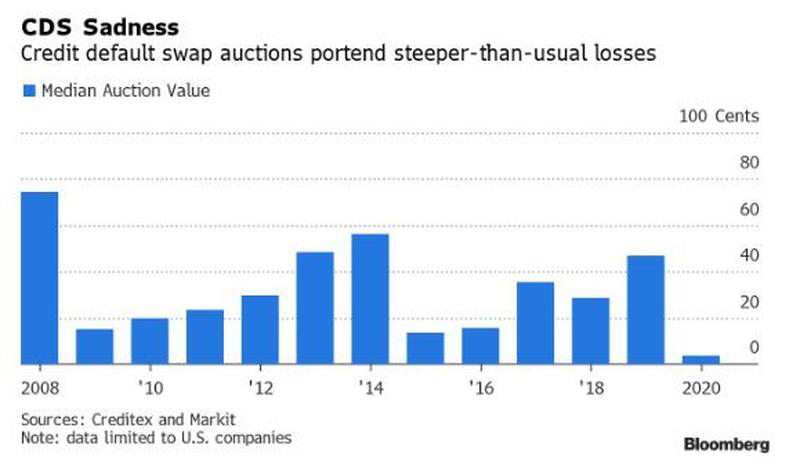

Several stark examples of this epic collapse in recoveries is the current price of a handful of retailers' bonds. Men’s Wearhouse, which filed in August, traded this month for less than 2 cents on the dollar. When J.C. Penney Co. went bankrupt, an auction held for holders of default protection found the retailer’s lowest-priced debt was worth just 0.125 cents on the dollar. For Neiman Marcus that figure was 3 cents. Indeed, as the following chart of median CDS auctions finds record low recoveries for bondholders (which of course is great news for all those who bought the CDS).

According to Barclays, the median value for companies’ cheapest debt in credit derivatives auctions this year is just 3.5 cents on the dollar, a record low and far below the 23.4 cent median for 2005 through 2019. It also confirms our warning that record low recoveries for bondholders are now the norm. Bloomberg then focuses on the underlying reasons which as regular readers will note, we correctly predicted years ago. It's probably why Bloomberg notes that "while few could have foreseen the pandemic’s toll on the economy, the depth of investors’ pain from corporate distress was all too predictable" although they clearly were not "predictable" to all those bondholders and yield-starved managers of other people's money who are now fighting for any recoveries, in many cases just years after buying the debt at par. Here is how Bloomberg lays it out:

If that sounds familiar, it's because it's verbatim what we said in 2016. And yes, even Bloomberg blames the Fed:

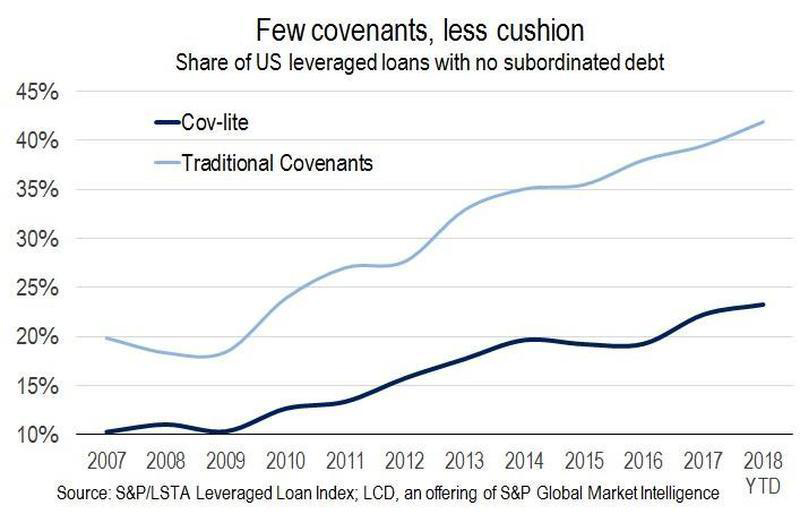

This reminds us of something else we wrote back in 2018, when we discussed the surge in covenant-lite deals:

Back then, we quoted Derek Gluckman, Senior Covenant Officer at Moody's who said that "while the rate of deterioration in covenant quality has slowed, protections remain distressingly weak on average. Investors should remain wary given the risks presented by most loan documents and the likelihood that any steadying of covenant protections is temporary." Gluckman added that collateral remains a key concern for investors, and warned that the loosening of covenant protections raises the risk that the collateral securing loans will be unavailable to support recoveries in a bankruptcy scenario. Separately, an analysis by LCD looked at the debt cushion of outstanding loans – the amount of debt in a borrower’s capital structure that is subordinated to the senior loan – and found that, increasingly, today’s cov-lite deals have little or no debt cushion beneath them. This, as we warned "is important because the lack of a debt cushion significantly lessens what an investor will recover on a loan, if that credit defaults." This, too, proved prophetic because as Bloomberg today writes, "the loose lending terms that investors have agreed to mean that by the time corporations file for bankruptcy now, they’ve often exhausted their options for fixing their debt loads out of court."

Of course, the one thing that was missing back in 2016 or 2018 was a catalyst triggering a wave of defaults. We now have that, however, the covid-linked lockdowns have added an additional twist of complexity: the pandemic has upended industries like retail and energy, "making it unclear how much assets like stores and oil wells will be worth in the future" further depressing already dismal recovries. But covid aside, the core problem for most companies is one that accumulated, literally, over the past decade with the explicit encouragement of the Fed: they have astronomical levels of debt after borrowing with abandon over the previous decade, then topping up with more to get them through the pandemic. Bloomberg then echoes our other warning: the record amount of secured debt means zero recovery cushion for unsecured debt lower in the cap structure:

"We’ll see companies gradually hitting the wall -- it’s just a question of when and how fast," said Dan Zwirn, founder of Arena Investors, a $1.7 billion investment firm with an emphasis on credit. “There’s just going to be way more downside.” Ultimately, the question when determining recoveries is what is the value of the enterprise post-bankruptcy, and it is here that a new set of investors are finding that they, too, are exposed. While unsecured creditors likely anticipated (or should have anticipated) catastrophic recoveries in a default cycle, secured lenders were hoping that their collateral coverage likely ensured a par recovery in a worst case scenario. Only that's no longer the case, as valuations collapse so much and asset values are so depressed, even secured debt faces dramatic impairments. According to Barcalys, loan investors could find themselves losing 40 to 45 cents on the dollar, compared with historical averages of 30 to 35 cents, according to Barclays. This is an optimistic take by Barclays, especially if the covid crisis drags on. Here, too, the preponderance of covenant-lite deals means that creditors are about to experienced unprecedented pain:

This, too, is something we warned about years ago, when we said that a cov-lite "secured" loan is effectively an unsecured bond. With a modest delay, others now agree: "Covenant-lite paper usually means by the time you get back to the table with the borrower, the house is on fire,” said Sanjeev Khemlani, a senior managing director at FTI Consulting. "All of that extra time you had before, that’s just gone away." To be sure, it wasn't just us who warned all this would happen: some investors predicted this outcome early and are now reaping profits. One such investor was Third Point's Dan Loeb, who in July 2019 correctly said that "covenant-lite loans will lower the overall default rate but result in higher loan loss severities in a stressed credit environment." It's why Loeb continues to generate alpha while most of his peers even as the hedge fund industry slowly sinks into oblivion. Here are a few more examples illustrating the collapse in "secured" recoveries: as Bloomberg writes, investors who bought a J. Crew Group Inc. term loan at par back in 2014 may have thought they were making a relatively safe bet, since it was secured debt. When the company started struggling a few years later, it moved intellectual property including its brand name into a new entity, a move enabled by relatively loose covenants. The company then exchanged some of its existing bonds for new notes secured by the intellectual property as well as preferred stock and equity in its parent company, as part of a broad restructuring. Loan investors ended up suffering: after the company filed for bankruptcy in May, the 2014 obligation was worth less than 50 cents on the dollar, according to Bloomberg loan valuation estimates. (J. Crew exited bankruptcy in September.) Sadly for creditors the pain is only just starting because they are only now about to learn what 10 years of cov-lite deals means in terms of their "modeled" recoveries:

The biggest irony of all this? Instead of encouraging corporations (which for years used debt proceeds to repurchase stock, pushing stock prices and equity-linked management comp to record highs) to prudently ease back on debt issuance, the Fed instead was instrumental in unleashing a truly unprecedented corporate debt issuance tsunami after the covid crisis, when it backstopped the corporate bond market for the first time ever and started buying investment grade and fallen angel bonds and junk ETFs. In doing so, it has terminally disconnected the link between prices and fundamentals. It also means that when the default cycle kicks up further over the next 6-12 months, recoveries will be even lower, and the losses for creditors will be even greater. It also means that as creditors start to model in far lower recoveries in the future, they will demand far more in terms of yield/current income which in turns will only be possible with ever more Fed intervention. In short, it means that by having gone all in on preventing the corporate bubble from bursting in March of this year, the Fed has made the situation far, far worse than if it had let the chips fall during the March crash. And since the Fed will never allow unmanipulated prices to clear without its intervention, the current default crisis only means that the fateful moment when the Fed openly starts buying stocks to prevent an all-out collapse of western capital markets is that much closer.

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)