Send this article to a friend:

October

14

2019

|

Send this article to a friend: October |

|

Will Social Security Be There for You? Status of the Social Security Trust Fund

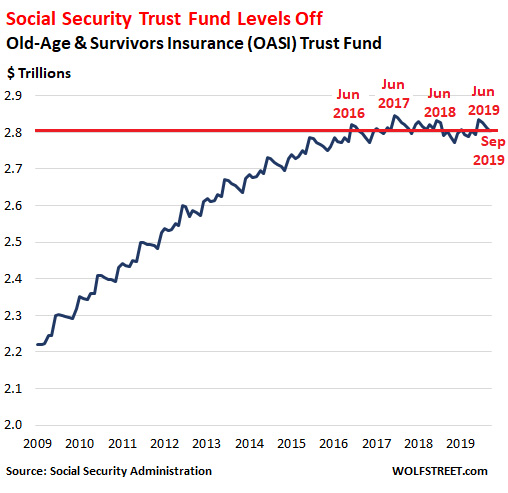

The Old-Age and Survivors Insurance (OASI) Trust Fund – does not include the Disability Insurance (DI) Trust Fund – which closed the fiscal year 2019 at the end of September with a balance of $2.80 trillion, according to figures released by the Social Security Administration. This balance was up by $3 billion from September last year, but was down $16 billion from September 2017. The balance tends to hit annual peaks in June. The all-time peak was in June 2017, at $2.846 trillion. In June 2018, the balance was down by $13 billion. In June 2019, the balance, at $2.834 trillion, was up $1 billion from a year earlier, but was still down $12 billion from the peak in June 2017. You get the drift: 2017 was a record year, 2018 was an alarming down-year, and 2019 has reversed the down-trend, but not by much:

The Social Security Trust Fund is benefiting from the increase of workers – particularly millennials, the largest generation ever – and from rising wages that trigger higher Social Security deductions. And the date when the trust fund is depleted keeps getting moved out further, currently estimated to occur in 2034. Depletion of the Trust Fund doesn’t mean that Social Security will collapse or whatever. It means either that workers will have to pay in a little more, or benefits will get cut, or a little of both. Social Security has been fixed before. Raising the maximum amount of earning subject to Social Security tax would be one way of doing it. Over 63 million retirees are drawing Social Security benefits (in addition, 8 million people are drawing SSI disability benefits). Back when I was a senior in high school, the dad of my sweetheart told me that Social Security was a “scam” and that it wouldn’t be around for him to use when he’d retire. He was a CPA and had his own business, an accounting and tax firm. He ended up retiring and collecting Social Security, which was still around. And a few years ago, he passed away, and his wife began collecting survivor benefits. Social security, which has been around for 84 years, has outlived him, and it’s going to outlive me too. But he gave me a piece of wise and correct advice – for the wrong reason: “Don’t rely on Social Security.” It’s tough to live off Social Security benefits, and it gets much tougher as you get older, as we’ll see in a moment. Of the SS Trust Fund’s assets, almost all, $2.79 trillion, were invested in in long-term US Treasury bonds at the end of September, with a weighted average maturity of 7.8 years. The remaining $12 billion (less than half of 1% of the total) were invested in short-term “certificates of indebtedness,” similar to Treasury bills. US Treasury securities are considered among the most conservative assets. The fund’s investment in Treasuries is very similar to a bond fund’s or a regular pension fund’s investment in Treasuries. The funds receive interest payments and are paid face value by the Treasury Department when the security matures. But there is one difference: Bond funds, pension funds, and other investors buy “marketable” Treasury securities that can be traded in the bond market. The SS Trust Fund buys nonmarketable Treasuries that cannot be traded, which has an advantage: Since they cannot be traded, their value doesn’t change on a daily basis. The Trust Fund accounts for them at face value, and face value is what the Trust Fund gets paid when the securities mature.

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](../09.19/images/t24_ag_en_usoz_2.jpg)