Send this article to a friend:

October

01

2018

|

Send this article to a friend: October |

|

Ignore The Hype – Oil Prices Aren’t Going Back To $100

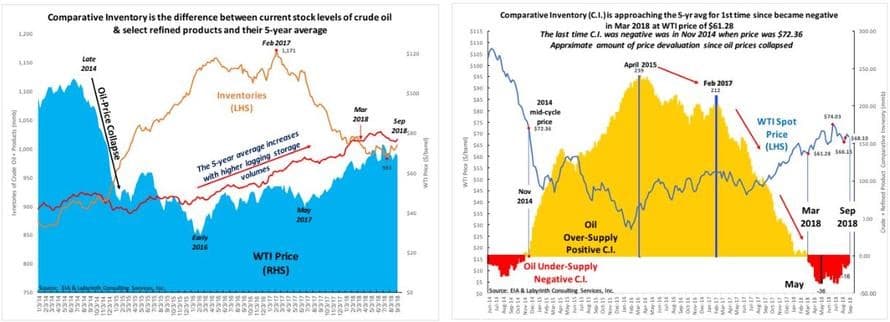

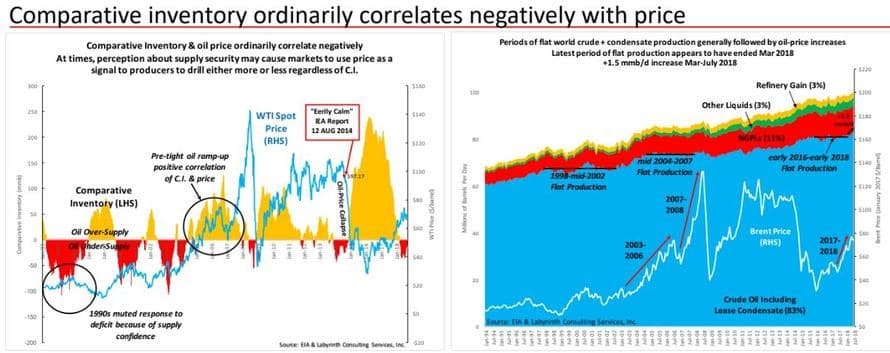

But to hear respected petroleum geologist and oil analyst Art Berman tell it, Trump should relax. That's because supply fundamentals in the U.S. market suggest that the recent breakout in prices will be largely ephemeral, and that crude supplies will soon move back into a surplus. Indeed, a close analysis of supply trends suggests that the secular deflationary trend in oil prices remains very much intact. And in an interview with MacroVoices, Berman laid out his argument using a handy chart deck to illustrate his findings (some of these charts are excerpted below). As the bedrock for his argument, Berman uses a metric that he calls comparative petroleum inventories. Instead of just looking at EIA inventory data, Berman adjusts these figures by comparing them to the five year average for any given week. This smooths out purely seasonal changes. And as he shows in the following chart, changes in comparative inventory levels have precipitated most of the shifts in oil prices since the early 1990s, Berman explains. As the charts below illustrate, once reported inventories for U.S. crude oil and refined petroleum products crosses into a deficit relative to comparative inventories, the price of WTI climbs; when they cross into a surplus, WTI falls.

Looking back to March of this year, when the rally in WTI started to accelerate, we can on the left-hand chart above how inventories crossed below their historical average, which Berman claims prompted the most recent run up in prices. Related: The Future Of Global LNG Is Here Comparative inventories typically correlate negatively to the price of WTI. But occasionally, perceptions of supply security may prompt producers to either ramp up - or cut back - production. One example of this preceded the ramp of prices that started in 2010 when markets drove prices higher despite supplies being above their historical average. The ramp continued, even as supplies increased, largely due to fears about stagnant global growth in the early recovery period following the financial crisis.

The most rally that started around July 2017 correlated with a period of flat production between early 2016 and early 2018. Meanwhile, speculators have been unwinding their long positions. Between mid-June 2017 and January 2018, net long positions increased +615 mmb for WTI crude + products, and +776 for WTI and Brent combined. Since then, combined Brent and WTI net longs have fallen -335 mmb, while WTI crude + refined product net long positions have fallen -225 mmb since January 2018 and -104 mmb since the week ending July 10. This shows that, despite high frequency price fluctuation, the overall trend in positioning is down.

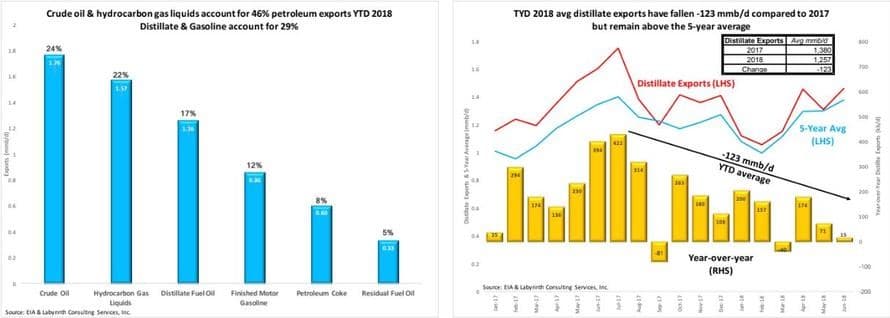

And as longs have been unwinding, data show that the U.S. export party has been slowing, as distillate exports, which have been the cash cow driving U.S. refined product exports, have declined. Though they remain strong relative to the 5-year average, they have fallen relative to last year. This has accompanied refinery expansions in Mexico and Brazil.

Meanwhile, distillate and gasoline inventories have been building.

Meanwhile, U.S. exports of crude have remained below the 2018 average in recent weeks, even as prices have continued to climb.

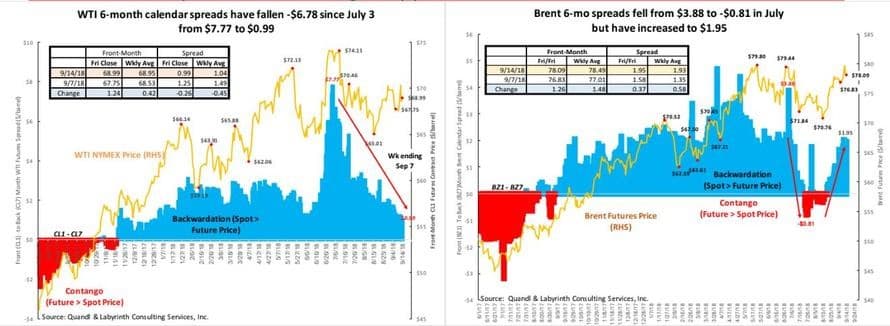

This could reflect supply fears in the global markets. The blowout in WTI-Brent spreads would seem to confirm this. However, foreign refineries recognize that there are limitations when it comes to processing U.S. crude (hence the slumping demand for exports).

In recent weeks, markets have been sensitive to supply concerns thanks to falling production in Venezuela and worries about what will happen with Iranian crude exports after U.S. sanctions kick in in November.

But supply forecasts for the U.S. are telling a different story than supply forecasts for OPEC. In the U.S., markets will likely remain in equilibrium for the rest of the year, until a state of oversupply returns in 2019. But OPEC production will likely continue to constrict, returning to a deficit in 2019.

Bottom line: According to Berman, the trend of secular deflation in oil prices remains very much intact. While Berman expects prices to remain rangebound for the duration of 2018 - at least in the U.S. - it's likely markets will turn to a supply surplus next year, sending prices lower once again. By Art Berman via Zerohedge

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/silver/t24_ag_en_usoz_2.gif)