"The End Of The QE Trade": Why Bank of America Expects

An Imminent Market Correction

Tyler Durden

Last Friday, when looking at the historic, record lows in September volatility and the daily highs in US and global equity markets, BofA's chief investment strategist Michael Hartnett said that the "best reason to be bearish in Q4 is there is no reason to be bearish." Last Friday, when looking at the historic, record lows in September volatility and the daily highs in US and global equity markets, BofA's chief investment strategist Michael Hartnett said that the "best reason to be bearish in Q4 is there is no reason to be bearish."

That prompted quite a few responses from traders, some snyde, a handful delighted (some bears still do exist), but most confused: after all what does investors (or algo) sentiment have to do with a "market" in which as Hartnett himself admits over $2 trillion in central bank liquidity has been injected in recent years to prop up risk assets.

To explain what he meant, overnight Hartnett followed up with an explainer note looking at the "Great Rotation vs the Great DIsruption", in which he first reverted to his favorite topic, the blow-off market top he dubbed the "Icarus Rally", which he defined initially nearly a year ago, and in which he notes that "big asset returns in 2017 have been driven by big global QE & big global EPS."

But mostly "big global QE."

And with global QE continuing, Hartnett, who two months ago predicted a volatile fall (and winter), now sees that Icarus “long risk” trade extended into autumn "by low inflation, big liquidity ($2.0tn central bank buying), high EPS, and promise of US tax reform."

As a result, Hartnett's "blow off top", or Icarus, targets for Q4 are: S&P 2630, Nasdaq 6666, 10-year Treasury 2.85%, EUR 1.15. At this rate, the S&P could hit BofA's target in about 3-4 weeks, and thus Hartnett lays out the following 11th hour trade recos for Q4

- long US$ vs EM FX,

- long oil,

- long barbell of uber-growth (IBOTZ, DJECOM) & uber-value (BKX) = Icarus trade;

- further unwind of extended “long disruptor, short disrupted” trade likely (i.e. death of old Retail, Media, Autos, Advertising by Tech Disruptors);

- rotational outperformance of oil>credit, EAFE>EM,

- value/growth

But if Hartnett's "Icarus" is here, then the just as popular "Humpty Dumpty" must be set to follow, and sure enough Hartnett goes back to square one, and his contention that since there is "nothing to be bearish about", it's time to take profits. Below are the various reasons why the BofA strategist expects the long-overdue market top is just around the corner.

- Global stock market cap up a massive $18.5tn (= US GDP) since Feb’16 lows

- 3P’s (Positioning, Profits, Policy) thus closer to peak than trough: BofAML Bull & Bear Indicator was 0 in Feb’16, now 6.9; global EPS growth was -6% YoY in early- 2016, now 14% YoY; $2.0tn of asset purchases by central banks YTD but Fed & ECB will taper next 6 months

- Q4 “top” in equities and credit driven by:

- a. pricing-in of US tax reform (= peak Policy),

- b. rise in MOVE index (= peak Positioning),

- c. rally in oil + trough in Chinese RMB + upgrades to global GDP (= peak Profits)

- Tax reform = “peak policy” = buy rumor, sell fact; passage of reform or cuts = quicker Fed balance sheet reduction + less share buybacks as capex accelerates; US equities lose 2 big tailwinds next year (since 2009 lows S&P equity market cap up $15.3tn, Fed’s balance sheet up $4.5tn, share buybacks up $3.5tn)

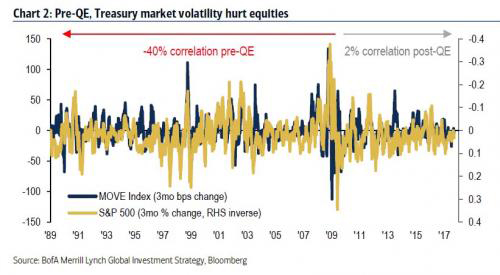

- Big jump in the MOVE index of US Treasury market volatility (i.e. “bond shock”) catalyst for cross-asset volatility (QE has neutered impact of bond volatility on equity prices but the negative correlation will return as monetary policy normalizes)

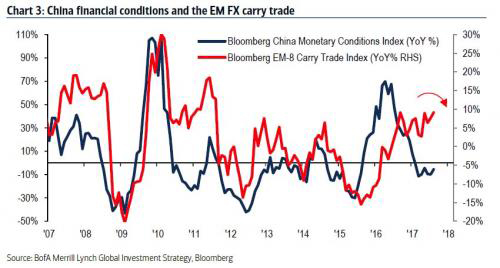

Lastly, BofA reminds us not to ignore China, where financial conditions have tightened of late (explcining this weekend's targeted RRR-cut), and a further leg higher in US bond yields will mean an unwind of EM “carry-trade” another source of Q4 cross-asset vol (Chart 3); note CNY has troughed.

Summarizing BofA's thesis:

In short, correction late-17 driven by “as good as it gets” narrative; magnitude dependent on CNY, MOVE, tax reform & degree of “forced selling” by ETFs & quant (7 ETFs accounted for 41% of volume of the top 20 most actively traded US issues in 2017; quant hedge funds & CTAs = $1.3tn AUM = 40% of industry total); right now feels more likely single- than double-digit.

It's not just the imminent correction, however. Hartnett also takes a longer look, and specifically what "the end of the QE trade" will look like. Here are his thoughts:

- Tech disruption & central bank liquidity have been the most important themes past 10 years; CBs have caused Wall St asset prices to boom, technology has constrained wages on Main St

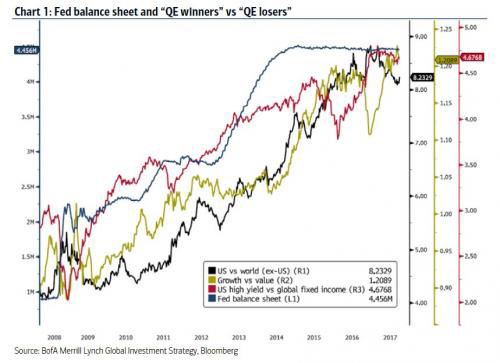

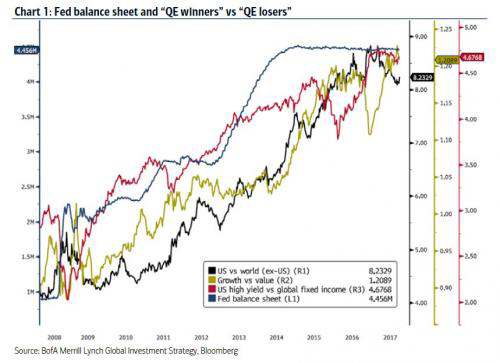

- Relative asset price performance next year will be highly dependent on speed & magnitude of liquidity withdrawal; since Bear Stearns event, expanding Fed balance sheet has led the outperformance of High Yield versus Treasuries, of Growth versus Value, of US equities versus RoW equities and so on.

- Table of QE winners & losers below illustrates the excess returns from 2 secular themes of “growth” & “yield”; low economic growth has boosted “growth” stocks, e.g. biotech, tech; low interest rates have boosted “high yielding” assets such as high yield bonds.

- Fed balance sheet about to reverse and global balance sheet same in 2018; and the massive outperformance of “QE winners” versus “QE losers” had frayed in recent months (e.g. growth>value) & quarters (e.g. US>RoW)

- The strong Q4 tactical case for asset/regional/style rotations ultimately dependent on inflation & interest rates rising (e.g. 10-year Treasury yield moves toward 3%) as low unemployment rates in the US, UK, Germany, Japan finally cause wages to accelerate and the Fed & ECB to tighten more aggressively in 2018; we strongly doubt this is the secular base case, however.

- Thus we fear Disruption, Demographics, Debt continue to prove deflationary, tying the hands of the central banks & keeping rates low (e.g. 10-year Treasury hugs 2%); if so, speculative bubbles in the bull market leadership of Tech, EM debt, High Yield are likely to occur.

our mission:

to widen the scope of financial, economic and political information available to the professional investing public.

to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become.

to liberate oppressed knowledge.

to provide analysis uninhibited by political constraint.

to facilitate information's unending quest for freedom.

our method: pseudonymous speech...

Anonymity is a shield from the tyranny of the majority. it thus exemplifies the purpose behind the bill of rights, and of the first amendment in particular: to protect unpopular individuals from retaliation-- and their ideas from suppression-- at the hand of an intolerant society.

...responsibly used.

The right to remain anonymous may be abused when it shields fraudulent conduct. but political speech by its nature will sometimes have unpalatable consequences, and, in general, our society accords greater weight to the value of free speech than to the dangers of its misuse.

Though often maligned (typically by those frustrated by an inability to engage in ad hominem attacks) anonymous speech has a long and storied history in the united states. used by the likes of mark twain (aka samuel langhorne clemens) to criticize common ignorance, and perhaps most famously by alexander hamilton, james madison and john jay (aka publius) to write the federalist papers, we think ourselves in good company in using one or another nom de plume. particularly in light of an emerging trend against vocalizing public dissent in the united states, we believe in the critical importance of anonymity and its role in dissident speech. like the economist magazine, we also believe that keeping authorship anonymous moves the focus of discussion to the content of speech and away from the speaker- as it should be. we believe not only that you should be comfortable with anonymous speech in such an environment, but that you should be suspicious of any speech that isn't.

www.zerohedge.com

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/silver/t24_ag_en_usoz_2.gif)