|

US Monetary Policy - Disharmony and An Unbroken Will to Plan

Antipodes Speak Out - Lacker and Evans Over the past two weeks we have heard several regional Fed presidents speak their mind, some of whom oppose the central bank's current easy money policies and some of whom think it should ease even more. Members of the Fed's board of governors in Washington and chairman Bernanke were also heard from - this group seems to be united in wanting to pursue an extremely easy monetary policy. We will look at some of the speeches that were delivered, with special emphasis on Charles Evans, as his viewpoint seems to be gaining ground lately. First we got to hear from 'hawk' Jeffrey Lacker again, the president of the Richmond Fed, who spoke to a group of businessmen in Salisbury, essentially repeating what he had said a week earlier already. Lacker once again stressed that he doesn't believe that 'Operation Twist' will do anything to revive economic growth, but that it may well lead to rising prices. However, he also mentioned a new and interesting aspect raising what in our opinion is quite an important point:

(emphasis added) Lacker is absolutely correct on the point highlighted above. By directing credit to a specific sector of the economy, the Fed without a doubt deprives other sectors of the economy. In this particular case the mistake is compounded by the fact that the Fed is directing more credit to a sector of the economy that is in urgent need of further liquidation and redirection of malinvested capital and needs to be allowed reach a market clearing level if its health is to be restored. All additional resources that are artificially directed toward this sector will only serve to delay the necessary readjustments and waste more scarce capital in the process. Note here to Lacker's point that the pool of real savings in the economy is limited, so when the Fed showers new money created from thin air on a specific sector, the sector's ability to bid for resources increases relative to that of other branches. The extent to which this redirection of scarce resources occurs is precisely the extent to which alternative employments of the same resources can not be undertaken by others. Wealth generation will be hampered. We should add to this that even if the Fed did not explicitly direct credit toward a specific sector of the economy but instead - as it normally does - were to merely accommodate credit expansion by the commercial banks passively, i.e., by supplying reserves so as to sustain an interest rate target below the natural level, very similar effects would be observed. Credit expansion by commercial banks does not happen in a vacuum after all. Which sectors of the economy will be the first recipients of newly created credit and money depends on the specific market data of each historical case, but when interest rates are kept below the natural rate, the bulk of investments will generally take place in higher order (capital) goods production or other long-duration investments (the housing sector is similar to capital goods from an analytical point of view, due to the long duration of services rendered by real estate). Credit creation in each specific case will anyway always end up favoring certain industries over others. However, it is still better to leave the decision to the private sector than leaving it entirely to the central bank. Currently the private sector has pulled back from pumping more credit into the real estate sector (this is not only due to the fundamental economic reason that the sector needs to liquidate malinvested capital and the housing market has yet to 'clear'. It is inter alia also due to the string of government interventions in the mortgage credit market over the past three years, which have made life extremely difficult for private sector mortgage lenders. This point has been discussed in more detail in Ramsey Su's articles). The Fed intends to create a fresh impetus for more credit creation in the mortgage sector, but as we noted above, this is a serious mistake. What should be implemented instead is a credible plan to wind down the operations of the GSE's (this is not the province of the Fed of course, but it certainly helps to perpetuate these interventionist entities by buying up their debt). The Evans GambitAnother regional Fed president who was heard from again was Charles Evans of the Chicago Fed - currently one of the most 'dovish' Fed members, whose idea we have named the 'Evans gambit' in allusion to a famous chess opening (named after the Welsh sea captain William Davies Evans who introduced the gambit in 1827. It goes: 1. e4 - e5; 2. Nf3 - Nc6; 3. Bc4 - Bc5; and now: 4. b4 - the 'gambit pawn' that the leader of the white pieces offers as a sacrifice in order to achieve a positional advantage). Evans delivered a speech entitled 'The Fed’s Dual Mandate Responsibilities: Maintaining Credibility during a Time of Immense Economic Challenges' to the Michigan Council on Economic Education. First Evans launches into a description of the 'enormity of the economic problem' we face, naming 'Paul Krugman, Mike Woodford and other economists' like them as the ones he 'largely agrees with', and citing the Keynesian shibboleth of the 'liquidity trap' as the primary economic problem. There is a lot of nonsense that just won't die, and this particular one serves as a very convenient excuse for supporting inflationism and deficit spending as the best 'cures' for economic recession. So far it's not working, but such facts curiously never intrude very much on the convictions of Evans and the economists he names. Even those who are convinced that Evans is correct in his diagnosis will have to admit that he omits an important point: he doesn't explain how it was possible for us to even arrive in this dreadful situation. Given his conviction, further stressed in the remainder of his speech, that the Fed's central economic planning is beneficial, such an 'immense economic challenge' should never have arisen. After all, the Fed's polices were a crucial factor influencing economic development before the bust as well. Further along in the speech Evans addresses some of the concerns that have inter alia been frequently mentioned by his more hawkish colleagues (he refers to them as the 'Fed's critics', without letting on that several of these critics are actually members of the Fed):

What is immediately clear from the above is that Evans is convinced that it is appropriate for the market economy to be lorded over by what is in effect a socialistic central economic planning agency that - in his words - needs to 'influence the trajectory of the economy'. It is probably not a big surprise that a Fed official would make this assertion, but it most definitely should be questioned. How can it even be considered possible that a handful of bureaucrats will know better which 'trajectory' the economy should take than the market economy itself? Why should it be held that such a state of affairs is even remotely desirable? This sudden obsession with 'credibility' must be brought into context. Numerous protest movements have sprung up in the US, from the 'Tea Party' to the 'Occupy Wall Street' demonstrations, and although many of the protesters likely don't know precisely how the modern monetary system works, they do know that something has gone wrong. Institutions such as the Fed that took credit, or were credited by others, for the boom can not escape becoming a focus of criticism during the bust. In addition, as Bob Prechter has pointed out in his most recent issue of the 'Elliott Wave Theorist' (more on this further below), 'the Fed not only suffers from an internal split, it has never had fewer friends in Washington than it has now'. A recent editorial by Ron Paul (recommended reading) excoriating the Fed that appeared in the Wall Street Journal has provoked an unusually large number of reader comments - the vast bulk of which seem to be in agreement with Paul's analysis. So yes, the Fed has a credibility problem, but it is no longer merely confined to the 'price stability' and 'inflation expectations' question (which seems to be the major concern of the 'hawks'). Evans then launches into a description of the 'monetary policy deliberation process' the Fed engages in before setting sail on a specific course. He unwittingly admits that socialist central planning is in fact an impossibility - in the sense that it can not deliver what its proponents insist it can: smooth economic development. Consider what he says below - we intersperse a few brief comments [bold and in brackets].

Evans then returns to the credibility question, noting that there have been times when the Fed's credibility suffered and times when it was comparatively high. He cites specifically the 1930's and 1970's as examples. We would put it as follows: whenever the stock market goes up, their policies seem to 'work'. When it goes down, they don't seem to work.

You don't say. Here we should perhaps point out that there exists a process that is clearly superior to 'policymaking' with its many flaws: the unhampered free market economy. We should try it sometime. Evans continues:

What he is in fact telling us is that as long as a boom continues, people are prepared to believe the most preposterous stories, including the one that the seeming health of the economy can be credited to 'economic policy' implemented by central economic planning institutions such as the Fed. In reality the boom eventually always leads to a condition deemed rather unsatisfactory, namely a bust. The bust is the economy's attempt to heal itself; to purge the distortions of the boom and rearrange its structure of production to correspond to the realities of consumer demand. The bust reveals the mistakes of the boom - and as such it naturally implicates policy makers that indeed must take responsibility for having fanned and rationalized the boom. Every time this happens, the preposterous stories people were eager to believe during the boom naturally meet with more and more incredulity. That's actually a good thing. Evans continues and begins to fantasize a bit:

Alas, as one would expect, for Evans the failure of the Fed's policies in the course of the bust to date are not a reason to rethink or abandon them; he thinks they should be intensified.

And while it is correct that the Fed made a string of mistakes in the 1930's, this is the wrong thing to focus on. The biggest mistakes occurred during the boom of the 1920's. In the 1930's a lot of effort was expended on redoubling the same mistakes, which is why what might have been a sharp and short recession turned into a long lasting depression. It would be entirely wrong to say that the Fed was 'sitting on its hands' during the bust that began in 1929. On the contrary, its policy recipes were not substantially different from today's. The Fed's credibility didn't suffer because it made no effort to pump in the 1930's - it suffered because the structural damage the economy had suffered during the boom was so great that it became glaringly obvious that the policy didn't work and in fact made matters worse. In his description of the historical data surrounding the episodes of the 1970's and 1930's contraction, Evans implies that Federal Reserve officials of both eras misinterpreted the economic data, and hence reacted 'wrongly' by pumping too much in the 1970's and not enough in the 1930's. Allow us to point out here that the Fed in both periods did what it always does when a bust strikes: it pumped. It doesn't have any other 'policy lever' than creating more money from thin air by various methods. Naturally Evans then dismisses the critics of today's unprecedented monetary pumping efforts by noting that he thinks we're in a replay of the period when the Fed allegedly didn't pump enough (in short, all roads lead to more money printing):

The blind faith that a mathematical construct can actually be used to determine how much monetary pumping there should be is entirely misguided. How does Evans know that - given the lack of a crystal ball which he admitted to earlier in his speech - he actually interprets the economic situation correctly? Even if he did so, it would not follow from this that more monetary pumping can 'fix' the economy. Since money printing can not create any wealth, it can only lead to a shifting around of existing wealth - the redistributive effect Lacker mentioned. It as a hindrance to the necessary economic adjustments the bust attempts to achieve. To be sure, the short run effects of a strong dose of monetary pumping usually make it appear as though the policy had a positive effect: asset and commodities prices rise, alleviating the pressure on bank balance sheets and creating speculative profits. Economic activities spring up that would not be pursued absent the artificial demand monetary pumping introduces. At the same time though all of this make the lives of most producers and wealth generators more difficult, as they have to contend with rising input costs. Consumers never get to see the falling consumer prices that would make their incomes stretch further - real incomes in fact tend to decline. Within the Fed, only Thomas Hoenig, the now retired former president of the Kansas Fed, clearly identified artificially low interest rates and money printing as causing the central problem of resource misallocation and malinvestment. Evans then goes on to describe the current dilemma as one consisting of a trade-off between 'inflation' (i.e., the effects of the inflationary policy on the 'general price level') and unemployment. He diagnoses that the reason that the economy isn't improving is that the public expects the Fed to soon tighten monetary policy again (in other words, he doesn't realize that the worsening of economic conditions is a long run effect of monetary pumping).

In short: the money supply must be increased further. Evans doesn't stop to ask how it is possible that a time period which has seen more money supply growth than occurred in all of preceding history (since the end of 2000, the US true money supply has increased by 165%) was concurrently the period that produced the worst economic performance since the end of WW2 and the worst stock market performance ever. It remains a mystery why neither he nor most of his colleagues at the Fed stop to question this fact.

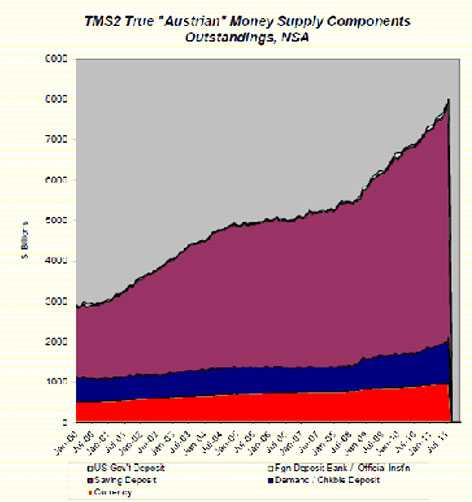

True money supply components since 2000 (legal categorization), via Michael Pollaro; at end 2000 the total stood at $3.017 trillion. At end of September 2011 it had grown to $8.003 trillion, an increase of 165%

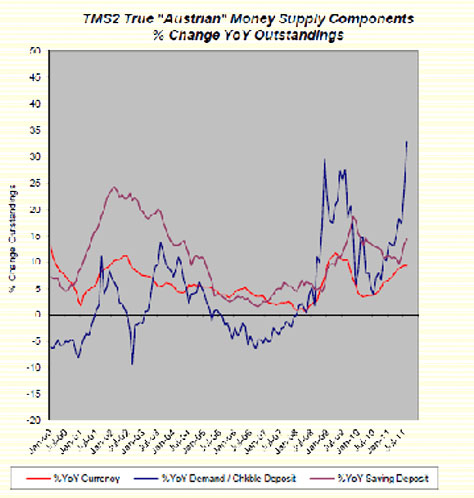

Year-on-year growth of the main components of TMS-2 since 2000; as an aside, the most recent growth spurt was egged on by dollar deposits fleeing Europe.

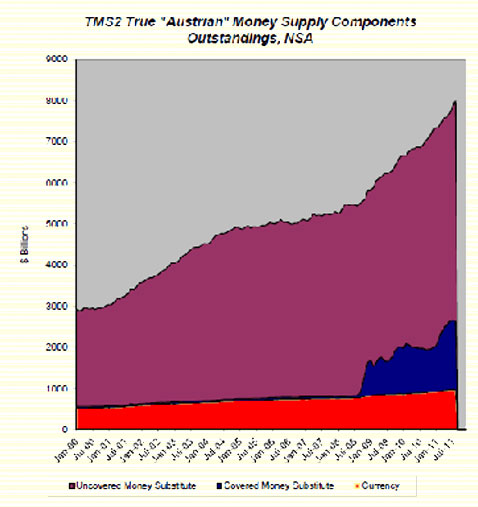

TMS-2 components by economic categorization. The periods when money supply growth accelerated the most coincided with economic downturns, while a slowdown in money supply growth preceded said downturns. Note that the big increase in covered money substitutes is due to the Fed's QE programs, which inter alia create massive amounts of free bank reserves. Considering the above charts, it seems clear that whenever money supply growth slowed down (in the year 2000 and the years 2005-2007), the effects of the previous inflationary period dissipated and the economy fell into recession, as uneconomic activities depending on easy money were unmasked and began to be liquidated. This does not mean that recession can be averted forever by the expedient of growing the money supply. Eventually, a crack-up boom and catastrophic collapse of the currency system would occur. Given the evidence it is curious why Evans and others at the Fed believe that more of the same will be a good thing. Internal Critics and SupportersAmong the current crops of dissenters in the Fed, Richard Fisher recently remarked:

This is obviously quite different from Evans' idea that businesses will expand if only they can be assured that no monetary policy tightening is imminent. Fisher is of course quite correct as to who profited the most from the recent Fed efforts. Regarding economic forecasts, Fisher had this to say:

(emphasis added) Nonetheless, Fisher is not doubting the value of the Fed's activities as such, in spite of practically admitting that they are flying blind. This contradiction is impossible to explain. Charles Plosser likewise expressed his doubts, saying that while he doesn't fear a large increase in 'inflation' (rising prices) in the near term, he believes that the excess reserves held by banks represent the fuel for same in the future. In an interview with the German paper 'Handelsblatt' he noted:

'Fiscal discipline' is something the Fed various members are also not really of one mind about. Similar to low 'inflation', many think it should only be a 'medium or long term goal'. Let's have fiscal discipline, but not just yet. Late last week more voices in support of additional easing measures were heard - which no doubt helped with goosing the stock market a bit. First Daniel Tarullo (a member of the board of governors in Washington), who normally doesn't engage much in public opining on monetary policy, pleaded for additional easing via monetization of more mortgage backed securities. One of the objectives of this plan - so Tarullo - is to induce investors to buy more risky securities - in other words, the objective is to blow another bubble. Tarullo considers a 'shortfall in aggregate demand' the economy's most pressing problem. However, demand is never really an 'economic problem'. It can not be, until the day arrives when all wants are satisfied. This and similar underconsumption theories were unmasked as fallacies long ago, but remain highly popular. The scarcity of resources and their optimal allocation to best satisfy the wants of consumers represents the central economic problem - and this is not something that can be improved by the intercession of planners. Lastly Janet Yellen, vice-chair of the Fed, announced her support for both Evans' idea of announcing specific thresholds for the eventual tightening of policy and the idea of embarking on yet another large scale asset purchase program - as Bloomberg reports:

Yellen's entire speech can be found here. Shortly before these two speeches were delivered, Ben Bernanke let loose on the technicalities and evolving philosophy of central banking, also proving that he remains the consummate planner. He inter alia announced that central banks will henceforth be 'better' at manipulating the economy because the financial crisis has taught them so many valuable new things. Seriously. The precise wording of that astonishing conclusion reads as though a sketch writer for a stand-up comedian had a hand in formulating it:

This is an enormous mouthful of utterly meaningless gibberish (as is the rest of the speech). If someone were to slightly reprogram the postmodernism generator it would probably spit out similar stuff. Here is what the 'better stocked toolkit' has achieved thus far: The so-called 'misery index' - a simple addition of the U3 unemployment rate and CPI - reaches a new multi-year high - click for higher resolution. The FutureIn connection with this unbroken willingness to foist more monetary experimentation on us, a recent remark by Bob Hoye is well worth quoting:

This latter point is no doubt true, as can be ascertained by considering all of the above. However, one should probably keep an open mind about whether it will come to the point where their tinkering will be allowed to blow everything up. As Bob Prechter notes, the change in social mood has made things far more difficult for the Fed. The political headwinds are getting stronger the more its extraordinary policies are seen to fail and the more unpleasant side effects they produce (think $4/gallon gas). On the other hand, it may not be too much of an exaggeration to state that four decades of unbridled credit expansion in a full-fledged fiat money system have brought us to a 'point of no return'. Consider again the money supply growth charts we showed above. The fractionally reserved banking system has flagrantly overtraded its capital and expanded its assets willy-nilly, while the economy's structure of production has concurrently gone through numerous distortion and discoordination phases and was never allowed to fully correct them. In short, even while the unproductive debtberg grew out of all proportion, the real economy's ability to generate wealth has been ever more impaired. As a result all it takes for a crisis to break out these days is a mere slowdown in money supply and credit growth. So there will constantly be new ostensible reasons to resume inflationary policy even if political headwinds should produce the occasional pause (the ECB currently faces such a situation - money supply growth in the euro area has slowed to a crawl over the past year and a crisis has broken out in the wake of this). The Western central bank that is the furthest along in abandoning even the last semblance of discipline is the Bank of England at this point in time. It has decided to completely ignore its price stability mandate in the face of the economic downturn, providing a string of excuses as to why it should no longer be guided by data that once were at the forefront of its decision making process. Note here that we are not saying that it should pursue a certain type of policy - as far as we are concerned the market economy would be best off without central banks. We are merely pointing out that the BoE is an example for how easy it is to abandon monetary discipline altogether in the face of a perceived economic emergency. Charles Evans proposes to abandon monetary easing if 'inflation' should increase above 3% - presumably in that case, even a 15% unemployment rate would not sway him from embarking on monetary tightening. However, if that is true, one wonders why he proposes further easing at this time, given that the year-on-year rate of change of CPI currently stands at 3.8%. The year-on-year rate of change of CPI is already way above Charles Evans' proposed 'upper bound'. What gives? Central bankers are in an unenviable situation; we have some sympathy for their increasing desperation. Cherished theories that were always held to be valid are not easily abandoned; cognitive bias will tend to overrule all objections, whether they are of a theoretical nature or consist of a growing body of empirical evidence. Moreover, they are indeed faced with a unique situation in a sense, as we have arrived at what is probably the endgame for the full-fledged fiat money system that has been in place since 1971. Never before have such daunting mountains of unproductive debt been amassed and rarely has the fractionally reserved banking cartel been in more profound trouble. To this we would note that the proposal to monetize more MBS will primarily help the banks, which continue to face enormous risks due to the decline in collateral values backing their real estate loans and the ongoing legacy challenges from the bubble period (such as California issuing a subpoena to BAC over 'toxic securities', or JPM and BAC admitting that they are receiving ever more refund demands from investors, concerning both pre- and post-bubble loans). Recently the Fed nodded and winked when BAC decided to transfer its derivatives risk to a subsidiary enjoying FDIC insurance (not surprisingly, the FDIC is somewhat less enamored of the prospect). While the Fed has been primarily founded to serve the banking cartel, we are not saying that its current members are not honestly interested in improving the economic situation. Charles Evans and others in his corner probably mean well. Nevertheless, their interventions are only making things worse and will continue to do so. When monetary pumping is stopped or paused for a while, the liquidation of malinvestments is bound to resume. The short run effect will very likely be an even more profound bust. Such short term outcomes will then serve as rationalizations for renewed pumping. Paul Krugman, whose economic philosophy Charles Evans identifies himself with, would undoubtedly let loose with a barrage of 'told-you-so's' while these short run effects play out. Curiously, we never hear from him when an alleged economic catastrophe on account of fiscal austerity and monetary rectitude turns into a success story after a little while (such as e.g. Estonia's and Iceland's strong recoveries; we have also noticed that ever since Ireland has fallen off the 'crisis map', Krugman doesn't mention it anymore). The truth of the matter is in fact demonstrated by these success stories. By allowing a bust to play out unhindered, one may suffer comparatively more short term pain, but the prize to be attained in the form of long term gain is well worth it. By contrast, the attempt to continually avoid suffering short term pain by means of deficit spending and monetary pumping condemns the economy to a never-ending malaise. It should be obvious that problems created by easy money and too much debt can not be solved by even more easy money and even more debt accumulation - alas, as illustrated above, this common sense realization has yet to dawn on our vaunted policymakers. |

|

|