Short Squeeze Coming? A Preview Of The Silver Market For The Month Of August Chris Marcus

Are we at increased risk for a short-term sell-off, or is a short squeeze coming? Here’s the outlook for silver in the month of August…

Disclaimer: This report contains strategies that could be risky for certain investors and is presented as research for further investigation. As always, you are trading and committing capital at your own risk

Current Silver Market Outlook:

Multiple analysts are reporting the presence of a large buyer in the silver market

The current silver COT positioning is bearish

The Fed meeting and labor report are likely to be catalysts for movement early in the month/late July

Silver ETF demand soars to highest levels since 2010-2011 prior to silver’s run to $49

Increasingly bullish medium to long-term, yet increased risk of a short-term selloff

Summary/Recommendations

While the factors suggesting increased prices in the medium to long term continue to grow, the current COT positioning indicates an elevated probability of a near term selloff.

Silver is still trading below the cost of production for most miners. While the leverage in the market remains high, amidst rumors of a “big whale” accumulating silver. Yet the banks are significantly short both gold and silver now, and over the past decade, that’s been a pretty consistent indicator that a selloff is near.

The Fed meets on July 31, and labor report is released 2 days later on August 2. Both events which traditionally feature significant moves in both gold and silver, and are likely to do so this time around as well. So again while the medium to long-term fundamentals are growing increasingly bullish at an accelerating rate, there is increased downside risk in the short-term.

As a result, I am reducing some of my core longer-term option positions by 25-50% and considering shorter term strangles (long call and long put but on different strikes – explained in the report) as a near term hedge, especially with options where volatility (price) is cheap.

July Silver Recap

Silver rallied in July, going from $15.22 to $16.39 (as of July 29). Which is the second month in a row where we’ve seen silver rally almost a dollar, as silver rallied from $14.48 to $15.22 in the month of June.

In some ways, this felt rather logical given gold’s recent ascent. Over these past two months the strength in the gold market has allowed me to be more aggressive in my positioning for an increase in the silver price. As while silver was climbing more slowly than gold during June, seeing the continued rise in gold provided another factor to suggest that silver would continue climbing.

To be clear, there’s no mathematical law stating how much silver is supposed to go up given a rise in the price of gold. Yet seeing the way gold traded, and looking at silver’s somewhat subdued response helped provide an additional reason to stay aggressively long silver. Which in this case I did.

Also interesting was seeing how often gold and silver were somewhat consistently up after the close in New York over the past month. Especially to see this several days in a row several times was noteworthy. As it feels like it’s been years since I remember seeing that in the silver market. Perhaps not since back in 2011.

It also seemed as if the downward spikes that have become so common over the past decade have had less strength behind them. In the last few years when silver would spike down, it would often be anywhere from 50 cents to a dollar or two. Whereas over the past month there were some occasions where it appeared as if one of those block offers was piled on the market, but rather than seeing silver plummet, the drop was somewhat muted.

While it’s hard to know for certain just based on the chart and without seeing who’s behind each trade, it sure felt different. And is something I’m keeping an eye on. Which is not to entirely rule out a 50-75 cent plummet in the future. But that it does seem as if the downward spikes are just occurring with less and less strength.

Which might be partially explained by the presence of a large buyer/buyers, as I comment on later in the report. Because while the paper COMEX price has often been divorced from the underlying supply and demand fundamentals in recent years, when the price goes down, it does allow investors to get physical at a cheaper price. Which has acted as somewhat of a floor to the market.

Yet for years I’ve been wondering when that physical demand would be enough to retake control of the price setting mechanism. And the latest data offers evidence that we might be getting closer to that point. Because if someone with deep enough pockets is really willing to stand up and buy in large enough quantities to halt the declines, that would alter the structure of the silver market that we’ve come to know over the past decade.

As a result, I feel as if we’ve reached a somewhat binary situation in the precious metals markets. In the sense that in the west, investors aren’t as inclined to buy when prices are low. But rather have more of an inclination to wait until something is going up, or has “momentum”.

Which means that as prices rise, there’s a tendency for the increase to draw in more buyers.

So it’s an interesting situation, especially with the banks being so short. Because this is typically the exact spot where we would expect to see gold and silver prices hammered. And frankly, I’ve been somewhat surprised not to see that happen yet. Especially because if that does not occur, the conditions are in place for more buying power to come into the market if the price continues to rise.

If silver continues to climb higher from here, that makes me wonder if something about the market structure has changed. Perhaps that would indicate that the paper market has lost control of the price.

We’ll find out soon enough. And perhaps it’s still a little to early to know for sure. But put another way, watch out for the spike down, and if that doesn’t happen, the probability that a greater bull market in silver is finally underway increases significantly. And at the conclusion of the report, I share how I’ve adjusted my positions to reflect this current outlook.

Latest Silver News

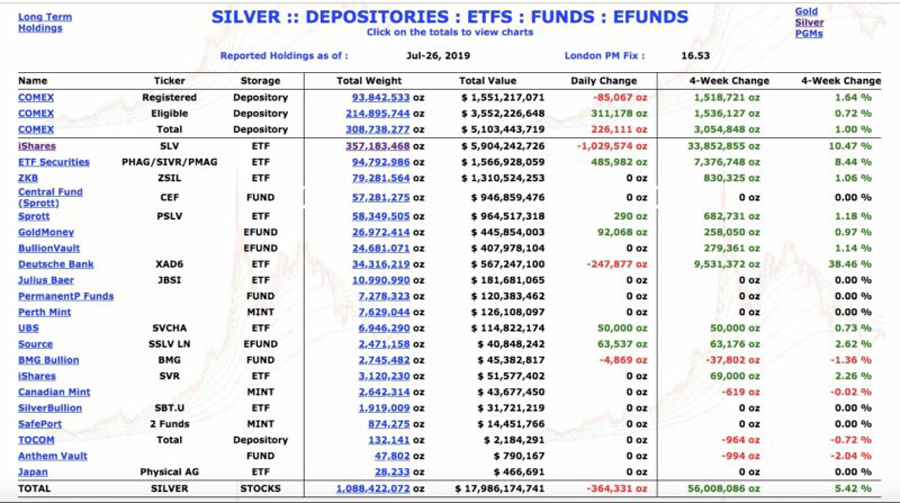

SLV and Silver ETF Inflows Surge

Perhaps the biggest development in July was the shocking amount of silver that was deposited into the silver ETF’s like SLV. Where as you can see in the chart below, 56 million ounces have been added in the last 4 weeks alone!

Which is a staggering amount. Especially in an already tight and over-levered market like silver, where I would maintain that the distance between the current environment and a short squeeze is smaller than most might imagine. Especially with silver trading below the cost of production for most miners, which has led to mine closures and falling supply (I am actually writing this from the Sprott Conference in Vancouver where I hope to get more insight into the actual numbers on this – which will be shared in this report in coming months).

The combination of large demand amidst falling supply is the exact recipe that could lead to the longer-term outcome I’ve been expecting ever since silver fell from its $49 peak in 2011. And to put into perspective how much 56 million ounces is, consider that in a recent interview, silver expert Ted Butler mentioned that back in 2010 following Ben Bernanke’s QE2, he felt the main driver for the runup to $49 was that 60 million ounces of silver were deposited into SLV.

So if 60 million ounces was enough to trigger the move in 2010, adding 56 million ounces in the past 4 weeks alone is pretty stunning. There were 9 million ounces added just over a 3 day period between July 19 and July 22 alone. So it is certainly one data point to keep an eye on. As should that increase continue at anywhere near that pace, that will really put a lot of pressure on the shorts.

Keep in mind this data only considers the ETF’s and doesn’t include what investors purchased from physical dealers. Yet nonetheless it’s certainly a key figure to watch going forward.

Is There a “Whale” In The Silver Market

In the past few weeks there’s been a lot of speculation and debate as to whether some group or entity has begun acquiring a large amount of physical silver.

Those familiar with Ted Butler’s research know he’s been writing for years about the massive amount of physical silver that he believes JP Morgan has acquired over the past decade. Which at this point he pegs at 800-850 million ounces.

Yet what sparked the more recent debate was an article from GoldMoney.com’s Alasdair Macleod, suggesting that a “whale is accumulating silver futures.” Which is certainly interesting, in that in a market with so much leverage (David Morgan and others estimate that there are in excess of 500 paper claims for each physical ounce), I’ve been somewhat surprised that some trading group or sovereign hasn’t forced this issue already.

In the weeks since Alasdair’s article there’s been some debate between him and Ted about the specifics of the arguments they’re both raising. Although while they disagree on some of the particular details, what stands out to me is that in the end we have 2 COT experts coming to the same broader conclusion. Specifically, that some entity is acquiring a large amount of silver. Which in my opinion is ultimately the most important thing.

Because whether that’s JP Morgan, China, or otherwise, to me what’s more significant is that there is a large buyer.

Of course if you can identify the buyer is and factor that into your analysis that can be a valuable clue. Yet in the end, we can look at the CME silver stock report and see that JP Morgan does have 153 million ounces in its account. And whether it’s theirs, or if it’s being held for a customer, someone (assuming that’s it’s primarily for one party) has accumulated more physical silver than even the Hunt Brothers or Warren Buffet held at their respective peaks.

Which is an interesting development. As I’ve long felt the supply and demand dynamics of the silver market have been overwhelmed by the excessive paper leverage. Which has created a situation that can go on (and has) for a long period of time.

Yet leaves the market vulnerable to a short squeeze. Because at some point, there’s simply not enough metal to satisfy all of the paper claims. Ultimately leading to some type of failure to deliver. And at the top of the list of events that could bring about this outcome is one (or more) large buyers who are buying physical. Or a product like SLV that’s required to add physical silver for each new share that’s created.

COT Positioning

As of July 26th, the COT report showed the commercials short 287,839 gold contracts. The largest short position the banks have held in gold since September of 2016.

Meanwhile in silver, the commercials are short 76,138 contracts. Which is again on the high side of the range.

The Fed Gets Ready To Cut Interest Rates

To add a further wild card into the equation is that this week there is a Federal Reserve meeting on July 30-31. Where it’s widely expected that the Fed will begin cutting interest rates again.

In the grand scheme of things, whether the Fed cuts interest rates at the July meeting, or waits until a future one ultimately will make little difference. The Fed found out last fall what any Austrian Economist has known for years. Primarily that things would look great while the presses were running, but watch out when the Fed tries to normalize.

So it comes as little surprise that the Fed has ultimately resorting to the only thing it knows. To create more credit. And it will be exciting to see how the markets react this week.

Currently the market is pricing in a 73.9% chance of a 25 basis point cut, and a 26.1% chance of a 50 basis point cut. With the probability of a 50 bp cut down a bit over the past few weeks, as previously many were pricing in 50 bp as fait accompli.

Which seemed high to me. Because while President Donald Trump and the Fed ultimately both want the same thing (lower rates), it seems hard to see the Fed justify a 50 bp cut with the stock market at all time highs and the most recent labor report (as fictional as it may be) giving the impression of a strong labor market.

So I’m certainly a seller of 50 bp. In fact if I were given an even money bet and could chose 50 bp or no cut, I think no cut would be slightly more likely.

Ultimately I think we will see 25 bp, and it will be fascinating to see how the market reacts. You could make the argument that 25 bp are already priced in, and that such a cut should not have a big market reaction. Yet we know how the gold and silver markets have a history of big moves on the Fed and labor report announcements, and I would be surprised if we didn’t see a significant move on at least one of those 2 events.

Which direction would silver move in the case of a 25 bp cut? That comes back to the binary outlook described already. Perhaps that will be when the market finally gets hammered. Or if the banks have lost control of the market, maybe the buying demand will overtake the shorts. And in the recommendations section below, I’ll explain how I’m using some options to position myself for the event.

Yet I do wonder that should we get the 25 bp cut, if that serves as a more widely recognizable symbol to the mainstream that the Fed’s decade long experiment has officially failed. Because while many sound money advocates have seen this coming for years, again I wonder if the actual interest rate cut opens more eyes in the broader Wall Street investment community. I would think there’s at least some possibility that getting a cut at all (whether 25 or 50 bp) cues a new group of investors to enter the silver and gold markets.

Should there be a 50 bp cut, we’re likely to see big moves up in both the metals and the stock market. If there’s no cut, expect both to get hammered.

Trade Recommendation

So in a situation like the one described throughout this report, how do you respond?

Perhaps the first thing to consider is that you don’t always have to have a position on. One of the most valuable principals I’ve learned throughout my trading career is that you don’t always have to have to trade something at all times. In fact, one of the advantages of trading in the markets it that you can really cherry pick the best opportunities.

Sometimes the odds of being right on a bet are 55/45. Or 51/49. Which doesn’t mean they aren’t good bets, but just that you can position your trades accordingly. If you’re making thousands of small bets with a sufficient bank role, even if the odds are only 51/49, you can still come out ahead. Much like the casino.

Of course if you find a situation where the odds are 80/20 or 90/10, then it makes sense to be more aggressive.

Yet the current situation is a bit more mixed than that. I’m keeping an eye on the longer term, but recognize the shorter term risk. So this isn’t a situation where I’m going to bet as aggressively in either direction. As opposed to if the banks were really long, and I thought there was a good chance the Fed would cut by more than is expected. Then it would be a better spot to be more aggressively long, as more factors would be lined up in the same direction.

For those who are long term investors, the easy call is to leave any physical holdings. The price might go down, but nothing has changed regarding the ultimate long-term outlook.

Yet for those who are more active short-term traders, one idea to consider is a short term “strangle”. Which is a buying a call on a higher strike and buying a put on a lower strike. Which turns your bet from being a directional play into one where you are simply betting on the volatility, or the extent of the move.

At the time of this writing, SLV is currently trading at $15.40. While the 15.5 strike weekly calls expiring August 2 are offered at 13 cents and the 15 strike puts are offered at 3 cents. Which means you can buy the strangle for 16 cents, and your break-even would be if SLV finished the week above $15.66 or below $14.84 (although should there be a move while there are still a few days before expiration you could possibly sell your strangle at a profit even if it hasn’t reached the break even point, since there will still be some option premium if it’s close to one of the strikes (if this isn’t entirely clear you are welcome to email me here).

These are relatively cheap options that have a good shot of coming out ahead given the market dynamics. Although to be clear, the way I approach these trades is not by asking if it’s “guaranteed” to be profitable. But rather by asking myself, “if I did this trade 10 or 100 or 1000 times in a similar situation, would I come out ahead. Because when you are long vol/options, remember that you have the benefit of unlimited upside.

So if you played this situation 10 times, you could lose on 9 of them, but if the 10th time the move was really large, you could still come out ahead. Personally, I think you’re likely to win far more than 1 out of 10 times. But at least that’s the way I approach these trades, particularly when using options.

This strategy can also be used with mining stocks (I often use variations of this with First Majestic Silver), or any type of stock where you aren’t sure about the direction, but expect a move to be great than what the option markets are implying.

Of course I will also issue my usual disclaimer that options carry a greater degree of risk and are not usually suitable for beginning investors. Although having a background as an equity options market maker, they are useful tools for the informed speculator. Especially in markets like silver where I would argue that there are some bigger points that most in the markets are overlooking.

One final note I’d like to pass along regarding options is that it’s worth considering the difference in perspectives. To explain, I would mention that in my last few years on the floor, I was trading about 600 different symbols. And if you’re wondering how it’s possible anyone could know the dynamics of all of those, the short answer is that it’s probably not.

The thing with options is that the market makers trade the order flow and the mathematical relationships between the options. So you can successfully trade without being in tune with the underlying fundamentals. Which for many of the products I had was the case.

Further, I remember how after I began researching the imbalances in the silver and gold markets, I remember talking to the trader at our shop who traded SLV. And let’s just say that guy was not concerned in the least about QE, whether silver is below the cost of production, or how all of the paper leverage will be resolved. Perhaps that seems difficult to believe, and maybe it’s changed since I left the NYSE in 2012, but I doubt it. More likely the case is that you have a better understanding of the fundamentals than most of the market makers.

Which I think is useful to keep in mind. Because again, it creates opportunities that you can cherry pick and skew the odds in your favor.

Trading Movie of the month

Each month I like to mention a trading movie I’ve been watching or thinking about.

This month I re-watched one of my favorites, “Limitless”. Where Bradley Cooper finds a drug that allows him to access the full power of his mind (in general I hear most of us are using only 1-10%). He uses this new found brilliance to find incredible success in the stock market (amongst other things), as he’s able to spot patterns and trends that are there, but that no one else is able to connect.

Fortunately, I don’t think you need to take a drug to achieve good results. There are good opportunities out there, and by paying attention to when others believe what you know that isn’t so, you can still come out ahead.

Hopefully this month’s report will be a valuable tool in doing so, and as always, you’re welcome to message me with any questions.

Until next month….

Sincerely,

Chris Marcus

I’ve certainly been blessed to have a fascinating financial career!

After graduating college my first job was at bond rating agency Moody’s.

Yes. The same folks who rated all of the sub-prime bonds with their highest Aaa rating, and ironically still rate U.S. debt similarly. To say the least it was an eye-opener.

After 2 years I left to attend Wharton, which also included a summer internship with Merrill Lynch. Which again has been fascinating in hindsight. Sitting on a trading desk in 2004 and seeing them sell any combination of mortgage products you could imagine, only to have it all take on a drastically different perspective years later.

However following Wharton I joined a small equity options trading firm called Susquehanna International Group (SIG). Which in hindsight turned out to be an incredibly fortunate break.

Unlike what I experienced in my brief time in banking culture, SIG had a unique training program that focused on decision making. In fact we were even required to log 100 hours of monitored poker playing, as SIG was a big proponent of poker being an excellent training tool for trading.

It was a critical part of my development, and years later when the housing bubble collapsed and understanding the markets on a larger level became the focus of my research, I was fortunate to have an incredible foundation.

Since then I’ve re-fallen in love with studying the financial markets and incorporating world events into successful trading. I’ve also felt a responsibility to pass along what I’ve discovered, so that as many people as possible can let the coming world events work to their advantage.

I appreciate you visiting this site and taking an interest in my research. Should you have any questions or comments I always look forward to hearing from you here.

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/silver/t24_ag_en_usoz_2.gif)