"The Global Bond Curve Just Inverted": Why JPM Thinks A Market Crash May Be Imminent

Tyler Durden

At the beginning of April, JPMorgan's Nikolaos Panigirtzoglou pointed out something unexpected: in a time when everyone was stressing out over the upcoming inversion in the Treasury yield curve, the JPM analyst showed that the forward curve for the 1-month US OIS rate, a proxy for the Fed policy rate, had already inverted after the two-year forward point. In other words, while cash instruments had yet to officially invert, the market had already priced this move in. At the beginning of April, JPMorgan's Nikolaos Panigirtzoglou pointed out something unexpected: in a time when everyone was stressing out over the upcoming inversion in the Treasury yield curve, the JPM analyst showed that the forward curve for the 1-month US OIS rate, a proxy for the Fed policy rate, had already inverted after the two-year forward point. In other words, while cash instruments had yet to officially invert, the market had already priced this move in.

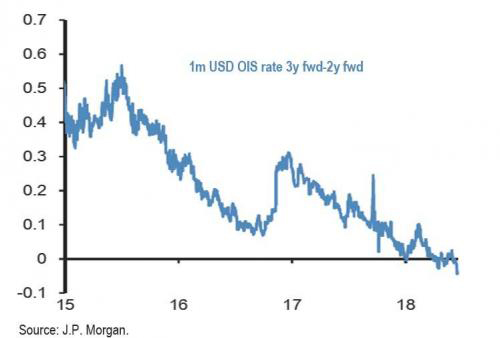

One way of visualizing this inversion was by charting the front end between the 2-year and 3-year forward points of the 1-month OIS. Here, as JPM showed two months ago, a curve inversion had arisen for the first time during the first week of January, but it only lasted for two days at the time and the curve re-steepened significantly in the beginning of April.

Fast forward to today when in a follow up note, Panigirtzoglou highlights that this inversion has gotten worse over the past week following Wednesday's hawkish FOMC meeting. As shown in the chart below which updates the 1-month OIS rate, the difference between the 3-year and the 2-year forward points has worsened, falling to a new low for the year of -5bp.

But in an unexpected development - because as a reminder we already knew that the market had priced in an inversion in the short-end of the curve - something remarkable happened last week: the entire global bond curve just inverted for the first time since just before the financial crisis erupted.

As JPM notes, while the Fed's hawkish move was sufficient to invert the short end further, it was not the only central bank inducing flattening this past week: the ECB also pressed lower on the curve via its "dovish QE end" policy meeting this week. And as a result of this week’s broad-based flattening, the yield curve inversion has spilled over to the long end of the global government bond yield curve also.

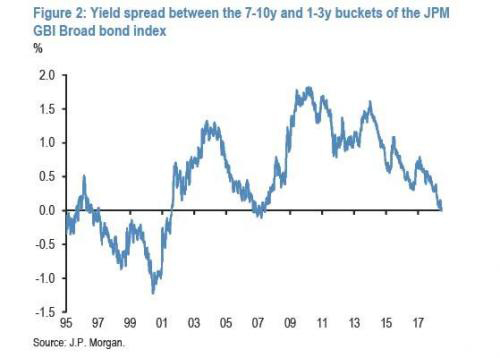

In particular, the yield spread between the 7-10 year minus the 1-3 year maturity buckets of our global government bond index (JPM GBI Broad bond index) shifted to negative territory this week for the first time since 2007. This can be seen in Figure 2.

But how is it possible that the global government bond yield curve can be inverted when most developed 2s10s cash curves are still at least a little steep? After all, as seen below, After all, the flattest 2s10s government yield curve is in Japan at +17bp and although the 2s10s US government curve - shown below - has been collapsing, it is still 35bp away from inversion.

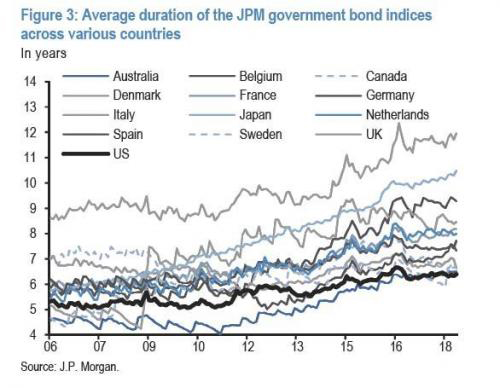

The answer is in the unequal weighing of US duration in the JPM global bond index: specifically, as Panigirtzoglou explains, the US has a much higher weight in the 1-3 year bucket, around 50%, than in the 7-10 year bucket, where it has a weight of only 25%.

This is because in terms of the relative stocks of government bonds globally, there are a lot more short-dated US government bonds relative to longer-dated ones as the US has lagged other countries in terms of the duration expansion trend that took place over the past ten years.

This is shown in Figure 3 which shows the average duration of various countries’ government bond indices over time. It is very clear that the US has failed to follow other countries in the past decade’s duration expansion race and as a result there are currently a lot more non-US government bonds in longer-dated buckets which are typically lower yielding than the US. And a lot more US government bonds in short-dated buckets which are typically higher yielding.

What are the practical implications? Well, in a word, global investors - those for whom Treasury flows are fungible and have exposure to the entire world's "safe securities" - now find themselves in inversion.

In other words, with the Fed having pushed the yield on short dated 1-3 year US government bonds to above 2.5%, global bond investors who, by construction, hold more US government bonds in the 1-3 year bucket and more non-US government bonds in the longer-dated buckets, finds themselves with a situation where extending maturities at a global level provides no extra yield compensation.

And the punchline:

This means that while at the local level bond investors are still demanding a premium for longer-dated bonds,at an aggregate level – abstracting from segmentation and currency hedging issues – bond investors globally are no longer demanding such a premium.

Needless to say, although JPM says it anyway, "this is rather unusual as can be seen in Figure 2."

As for the timing, well it's troubling to say the least: it did so just before the last two bubbles burst. In fact, the last time the 7-10y minus 1-3y yield spread of JPM's GBI Broad bond index turned negative was in 2007 ahead of an equity correction and recession at the time. Before then it had turned very negative in late 1990s also, after the 1997/1998 EM crisis but also in 1999 ahead of a burst in the equity bubble and a reversal of Fed policy.

And if that wasn't enough, here are some especially ominous parting thoughts from the JPM strategist:

In other words, in normal times, bond investors demand a premium to hold longer-dated bonds and to tie their money for a long period of time vs. investing in lower risk short-dated bonds. But when investors have little confidence in the trajectory of the economy or they think monetary policy tightening is overdone or they see a high risk of a correction in risky markets such as equities, they may prefer to buy longer-dated government bonds as a hedge even though they receive a lower yield than short-dated bonds. This is perhaps why empirical literature found that the slope of the yield curve is such a good predictor of economic slowdowns and/or equity market corrections.

In other words, contrary to all those awed but naive interpretations of the short-term market reaction invoked by Powell or Draghi, according to the market, not only the Fed but the ECB engaged in consecutive policy mistakes. And, as JPM confirms, "this week’s central bank meetings exacerbated this flattening trend."

As a result the yield curve inversion is no longer confined to the front-end of the US curve, but has also emerged at the longer end of the global government bond yield curve.

What this means is that a decade after the last such inversion, bond investors globally no longer require extra premium for holding longer-dated bonds vs short-dated bonds, something that happens rarely, e.g. when investors have little confidence in the trajectory of the economy, or they think monetary policy tightening is overdone or they see a high risk of a correction in risky markets such as equities.

our mission: our mission:

to widen the scope of financial, economic and political information available to the professional investing public.

to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become.

to liberate oppressed knowledge.

to provide analysis uninhibited by political constraint.

to facilitate information's unending quest for freedom.

our method: pseudonymous speech...

Anonymity is a shield from the tyranny of the majority. it thus exemplifies the purpose behind the bill of rights, and of the first amendment in particular: to protect unpopular individuals from retaliation-- and their ideas from suppression-- at the hand of an intolerant society.

...responsibly used.

The right to remain anonymous may be abused when it shields fraudulent conduct. but political speech by its nature will sometimes have unpalatable consequences, and, in general, our society accords greater weight to the value of free speech than to the dangers of its misuse.

Though often maligned (typically by those frustrated by an inability to engage in ad hominem attacks) anonymous speech has a long and storied history in the united states. used by the likes of mark twain (aka samuel langhorne clemens) to criticize common ignorance, and perhaps most famously by alexander hamilton, james madison and john jay (aka publius) to write the federalist papers, we think ourselves in good company in using one or another nom de plume. particularly in light of an emerging trend against vocalizing public dissent in the united states, we believe in the critical importance of anonymity and its role in dissident speech. like the economist magazine, we also believe that keeping authorship anonymous moves the focus of discussion to the content of speech and away from the speaker- as it should be. we believe not only that you should be comfortable with anonymous speech in such an environment, but that you should be suspicious of any speech that isn't.

www.zerohedge.com

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/silver/t24_ag_en_usoz_2.gif)