Send this article to a friend:

June

07

2017

|

Send this article to a friend: June |

|

Less Than Zero: How The Fed Killed Saving

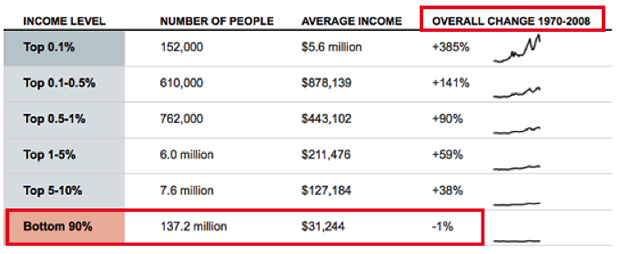

The other day I was in my local branch of a Too Big To Fail bank where I have a few accounts. One of them is a savings account in which I keep some of my "dry powder" cash stored. It had been a while since I had checked what kind of return the savings account offered. I knew it was pretty low, but there have been a few Fed rate hikes since the last time I had checked. So I asked the teller to look up the current rate the account was yielding. Any guesses? It's 0.06%. Not 0.6%. And definitely not the 6% I remember receiving when I was a teenager. 0.06%. As in, put $100,000 into your savings account and get back a whopping $60 per year. Are you kidding me? $60 to have a hundred grand parked in an account subject to withdrawal restrictions and penalties, along with the usual smattering of administrative fees both overt and hidden? At a bank that stumbled mightily during the Great Financial Crisis? One with the potential to legally confiscate your savings through a "bail in" should another crisis hit? Oh, and if you factor in the government's trailing 12-month inflation rate of 2.2%, your "savings" account has a negative (-2.14%) real rate of return. Your compounded savings actually loses purchasing power over time. And as we all know the official inflation rate is farcically understated, your loss of purchasing power is even more dire than it at first appears. "Thank" The Fed Savings accounts were created to provide an incentive for people to plan for the future. Put money away today, let it grow through the miracle of compounding interest, and have more tomorrow. Prudent savings is essential to a healthy economy. It offers resilience during downturns, and provides seed capital for productive enterprise. But we are no longer a nation of savers. Not only does our culture indoctrinate us to spend and consume -- and makes it possible to do so by spending future prosperity today through the use of debt (the very opposite of saving) -- but the Federal Reserve has very intentionally driven down interest rates to historic lows. To show just how far, let's take a look at historic interest rates savers have enjoyed over the past few decades. Here's a chart of the return offered on 6-month bank CDs, from the Fed's own data. Returns plummeted from 10% in the mid-1980s to less than 1% after the Great Recession began: Notice how the data series was discontinued in 2013. Perhaps the Fed was concerned the picture it painted showed too clearly the war being waged against savers? But a new similar data series was begun afterwards, which shows that the carnage continued. Between 2009 and today, 6-month CD returns have declined by a further 90%: So there's no incentive remaining to save your money in a "safe" place. As mentioned, you lose purchasing power due to today's negative real rates. Plus, you have bank risk (bail ins, etc) on top of that. As we write about extensively on PeakProsperity.com, this is not an accident of fate. The Federal Reserve has very deliberately engineered this situation. It has chosen to sacrifice the many -- the savers and those dependent on a fixed income -- to benefit an elite few. Rock-bottom interest rates are greatly helpful to the banks, as well as the financial assets that the bankers and their wealthy clients own. And just to add to the outrage factor here, when your local TBTF bank stores its own money at the Fed, the Fed pays it a full 1% in interest -- nearly 20 times what your bank is paying you. Your bank simply pockets the rest as pure risk-free profit. (Don't believe it? Watch Chris explain in this video) The data clearly shows that this suppression of interest rates, combined with the central banking cartel's Herculean efforts to flood the world with liquidity (to the tune of $1 trillion so far in 2017), accrues benefits in a grossly lopsided and unfair manner to those at the top of the wealth pyramid:

Meanwhile, while the income prospects for everyone in the bottom 90% have stagnated, the cost of living has skyrocketed. The masses are getting badly abused in both directions. Financial Repression As mentioned earlier, this is NOT accidental. As we have written about time and time again, the fundamental economic predicament facing the world is having Too Much Debt. This is a situation societies have found themselves in before. In fact, it has happened so often throughout history that there's actually a playbook (for the government) when you get to this stage. It's called Financial Repression. Here's a summary from our excellent podcast interview on the topic with Dan Amerman:

0.06% savings rates in a world of 2.2% (and actually much higher) inflation? That's a clear sign we're living in the era of negative real interest rates right now. The purchasing power of our savings is being siphoned off to sustain the government's debt orgy, making the elites filthy rich in the process. The financial repression playbook is well underway. But while financial repression extends the lifetime of an over-indebted economic system, it does not avoid the consequences of Too Much Debt. It merely serves to shift the worst of the inevitable losses from the government onto the public. As von Mises' guarantees:

Negative interest rates are a milestone down the slippery slope of the latter: currency destruction. The central banks are intentionally devaluing their currencies, but betting that they can do so at a controlled pace. But as von Mises warns and as history has shown again and again, currency regimes burdened by too much debt eventually reach a critical failure point where a uncontrollable cascading collapse becomes inevitable. Know Your Enemy At this stage, it's now critical for investors to ask: What are the central banks most likely to do next, and what will the repercussions be? If you haven't read our latest report Understanding The Fed's Endgame Is Key To Protecting Your Wealth, you really should do so now. In addition to negative real interest rates, it reveals the many other clandestine steps the Fed is performing in the shadows to separate the American people from their hard-earned wealth, and place it in the pockets of the bankers and their cronies. In most instances, it's a case of doing exactly the opposite of what it is publicly promising. You can read that report here (free executive summary, enrollment required for full access) Understanding the Fed's next moves is also why PeakProsperity.com is offering the upcoming webinar, The End of Money, on this coming Wednesday, June 7. It will bring together David Stockman, Axel Merk, G. Edward Griffin -- experts on the Federal Reserve, global currencies and financial markets. During this 3-hour event, you'll hear their latest intelligence and forecasts and be able to ask each speaker questions directly. Key themes addressed will be:

This is a not-to-be-missed experience for the prudent investor. And since it's only a few days away, the time to register for it is now. REGISTER FOR THE WEBINAR NOW

Adam is the President and Co-Founder of Peak Prosperity. He wears many hats, but his basic job is to handle the business side of things so that his fellow co-founder, Chris Martenson, is free to think and write. Adam is an experienced Silicon Valley internet executive and Stanford MBA. Prior to partnering with Chris (Adam was General Manager of our earlier site, ChrisMartenson.com), he was a Vice President at Yahoo!, a company he served for nine years. Before that, he did the 'startup thing' (mySimon.com, sold to CNET in 2001). As a fresh-faced graduate from Brown University in the early 1990s, Adam got a first-hand look at all that was broken with Wall Street as an investment banking analyst for Merrill Lynch. Most importantly, he's a devoted husband and dad.

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/silver/t24_ag_en_usoz_2.gif)