Send this article to a friend:

June

06

2017

|

Send this article to a friend: June |

|

"This Only Ends When The Bond Market Pukes"

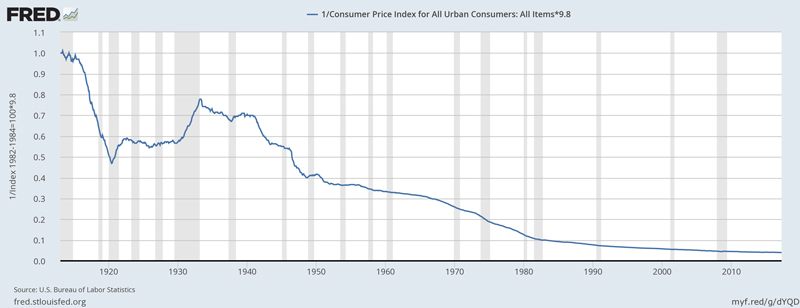

So when you take solace in the fact the stock market is running higher without you, I would be weary of consoling yourself that you are in smart company. Now please don’t mistake my unwillingness to join the chorus of those warning about the dangers ahead as my belief that everything is rosy. I understand the arguments about the huge imbalances in the financial system. I don’t need a lecture about the unsustainability of the current environment. I get it, we are screwed. We have made too many promises, have not saved enough and have created a can’t win financial situation. Yet why is everyone so sure it will end in a deflationary bust? I hear all these gurus talking about the optionality of cash. Yeah, I understand. If you hold cash when prices collapse, you are able to buy when everyone else is selling. You listen to these hedge fund managers tell the story, and it sounds so compelling. It makes you want to sell everything, sit back and wait for the inevitable collapse. But here’s another way of looking at cash. A dollar from 1913 is now worth less than a nickel.

And that’s using the government’s official CPI data! Imagine if you used the correct level of inflation… So I ask you, with Central Bankers determined to create inflation, why on earth would you want to hold cash? For this trade to work, you have to assume Central Bankers will suddenly change their tune and be willing to preserve the purchasing power of money.

I don’t see any signs of Central Banks becoming more responsible. In fact, the math makes it virtually impossible for them to ever normalize rates. Do you know the economic slowdown that would happen with proper interest rates? It would be devastating. It would make the 1929 depression look like a walk in the park. Central Bankers are becoming less responsible, not the other way round. I started following this interesting organic chemistry professor from Cornell that is a self professed Libertarian, and admits to being a fan of ZeroHedge (not something you see in most professors these days). Dave Collum had this terrific tweet that summed up the current situation perfectly:

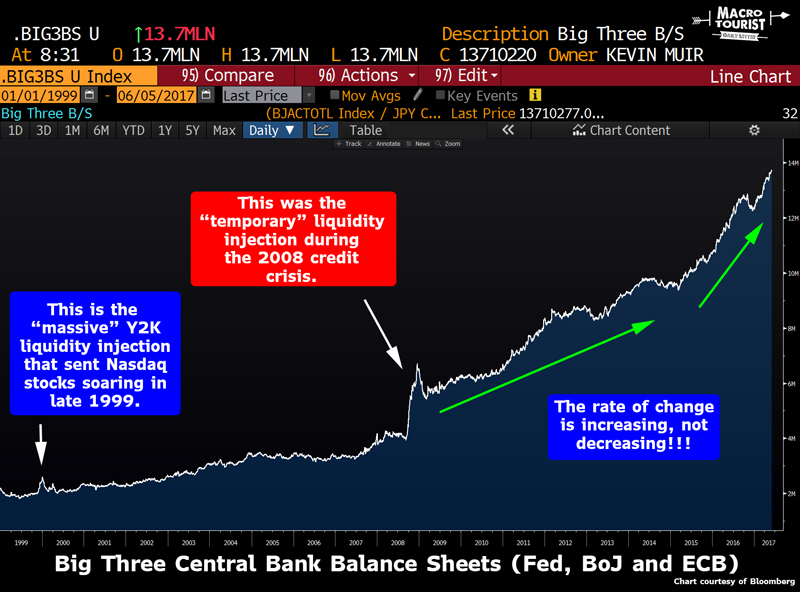

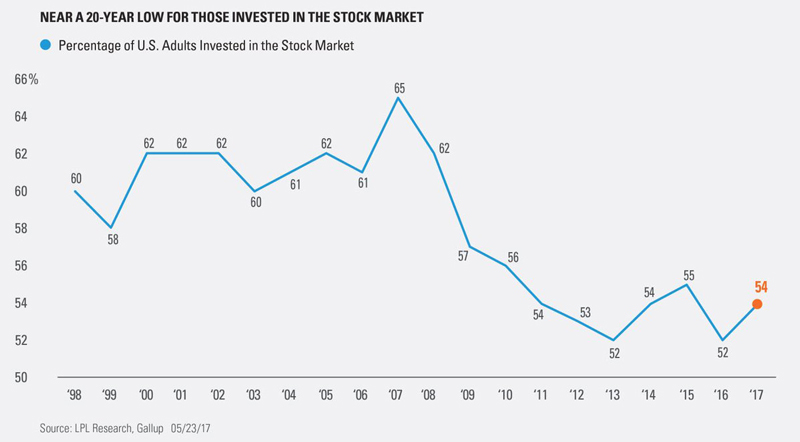

Dave is correct that the free market wants deflation. There is too much debt in the system, and the market is trying to reset through a credit destruction event. The 2008 great financial crisis was the result of the private sector trying to pay down credit. It was stopped when governments and Central Banks stepped in to replace the private sector, but it was a difficult, scary process. Officials underestimated how much credit expansion was needed, so the bounce ended up being choppy and prone to stops and starts. But as Central Bankers have become more comfortable with balance sheet expansion, they have increased the rate of increase. Have a look at the chart above. The rate of expansion has been increasing, not the other way round. Does this look like the chart where Central Bankers are about to reverse the constant inflating? Central Bankers, through their actions of financial repression, have told you that they don’t respect the value of your savings. Why on earth would you want to hold the asset they have constantly debased? I don’t think stocks, real estate or any other financial asset offers value at these lofty prices. Yet I believe the asset in which all these other securities are priced in, is an even worse investment. Which brings me back to today’s stock market. On Friday, the Non-Farm Payrolls missed. The US macro data has disappointed versus expectations for the past couple of months, and this has finally bled into the employment number. Although Central Bankers are inflating, they are not doing it uniformly. In the period after the 2008 credit crisis, the Federal Reserve was the most aggressive Central Bank out there, causing many distortions in the financial markets. The ECB was reluctant to join the party, and their stinginess resulted in their own 2011 European crisis. Eventually, Draghi & Co. had to turn on the liquidity taps. The Bank of Japan is on their own timeline, kicked off with the Fukushima nuclear disaster. It’s not as simple as saying all Central Bankers are printing without abandon. They have taken turns, sometimes one country doing more, while the others sit it out. And right now, the Federal Reserve is the one on the sideline. In fact, the Fed is trying to normalize interest rates, and even more boldly, setting up plans to shrink their balance sheet. I think it was Jim Bianco who said there has never been a modern day Central Bank that has successfully shrunk their balance sheet, so the Fed’s ambitious plans should prove interesting. If you believe the Fed will stay the course with higher rates and a lower balance sheet in the face of economic weakness, then, by all means, short U.S. equities. If you think the last century of dollar debasement will reverse and the Federal Reserve will become a saver’s friend instead of their enemy, then stock up on a big slug of cash. I don’t believe for a second the Federal Reserve will stick to their plan to normalize the balance sheet and raise rates when the economy slows down. In fact, I think markets will be shocked at how quickly the Fed changes their tune. They don’t really have a choice, the massive debts need to be serviced, and force feeding the economy cheap credit is the only way to keep the economy moving forward. This vicious cycle of a slow down being met with ever easier Central Bank policies will only be stopped when we enter into an inflationary bust. It’s only when the bond market does what Bill Fleckenstein has warned about, and finally takes away the keys, will governments be forced to deal with the massive imbalances in the financial system. So when Friday’s employment number disappointed, it was met with all sorts of glee from the stock market bears. I don’t view it the same way. Of course, a slowing economy will often be met with equity selling and bond buying, but this isn’t a regular market. What is the biggest risk to financial markets? Contrary to popular opinion, it’s not a slowing economy. No, it’s the withdrawal of Central Bank stimulus. Right now the Fed is tightening, probably a little too quickly given the huge amount of debt. A slowing economy will change the pace of this tightening, and eventually even cause easing. Therefore, ironically, an economic slowdown is stock market bullish. I am not scared of a slowing economy because I know Central Bankers will be there with a big fistful of blue tickets. I am scared of inflation finally spurting up and having the Central Bankers withdraw liquidity too quickly. It seems crazy to rely on these Central Bank knobs as a backstop as you buy assets. But that’s the problem. It is irresponsible to be invested at these levels based on a Central Bank put. And that’s why everyone is under-invested. Could you really go in front a pension board and suggest an overweighting in equities because Central Bankers have your back? Not a chance. Or if you are a retail investor, with nightmares of the 2008 crisis still swirling through your mind, do you really want to expose yourself to that sort of drawdown? When you combine those worries with the fact that you haven’t saved enough, add in the fact you are probably going to live longer than any other generation, you simply don’t want to lose it again. It’s no wonder less US adults are invested in the stock market than any period in the past twenty years.

And if you manage a hedge fund, you remember the fortunes made during the pricking of the last bubble. Hedge fund managers who were previously nobodies, became household names. Everyone wants to replicate that success. Everywhere you look there are managers with calls about the next “big short.” On Wall Street everyone hedges for the last crisis. I don’t know much, but I do know that the next crisis will look nothing like the previous one. Owning the asset Central Bankers seem most intent on debasing is perverse logic. If you really think government an I am a private investor who used to work for a big Canadian bank as a derivative index trader. I have been writing a journal for myself for many years. From time to time I have shared these posts with colleagues and friends. Many have encouraged me to write on a more regular basis and to allow others to read it. So, this journal is a response to these suggestions. This journal is simply a collection of my ideas and thoughts. They are not recommendations to buy or sell any specific securities. You have to be responsbible for your own trades. For my colleagues in the investment industy who understand how trading works, this goes without saying, but for those that don’t do this for a living, I just want to make it clear that you need to make your own decisions. I fully expect a good percentage of my trades not to work. Dealing with these trades is what makes a good trader a great trader (and don’t bother asking me how to be a great trader either, as I am still trying to figure that part out as well). As you come to read my ideas and thoughts, you will realize that my style is almost the opposite of a trend follower. In fact, during a big move, I am often trying to catch the falling knives. It is a both a strength and weakness, and as of yet, I am unsure if the missing fingers are worth it. You might also notice that I rely on other investors for a fair amount of the nitty gritty detailed stock analysis. When it comes to balance sheet anaylsys, I am no David Einhorn or Prem Watsa, but when they are buying a security in a name that I have a bigger macro themed view on, I am not ashamed to simply ride their coat tails. However I am extremely picky about whose analysis I rely on. I don’t simply read Seeking Alpha or Citibank’s research report and climb aboard an idea. I need to respect and trust the person whose idea I am emulating. These great investors trade with their own timeframe and risk preference, therefore I only rely on them to point me in the right direction, not to tell me when to buy or sell. You might be asking yourself, well why bother reading me at all? The benefits that I offer can be best summed up by Michael Steindhart, who in classic book Market Wizards, described one of his friends this way – “There is a very good investor I speak to frequently who said, ‘All I bring to the party is twenty-eight years of mistakes.’” Although I haven’t been trading for 28 years, I am getting closer than I would like to admit and I have made way more mistakes than I would care to remember. This journal is a way for me to share those mistakes with you. d Central Bankers are out of control, shouldn’t you be shorting them? And how do you do that? Well, I would argue shorting bonds is a much better trade than betting against stocks. After all, that’s where the real bubble is. This has turned into a long diatribe, but my main point is that I am not surprised that stocks went higher Friday in the face of bad economic news. A slowing economy will not end this period of overvaluation. It will only end when the bond market finally pukes. Until then, the Central Bank bubble will just continue to get more and more expensive. Most market participants believe it will end in a deflationary bust, and therefore hiding in long dated risk free fixed income is the best bet. Well, at the risk of being on the other side of the trade of most “smarter” hedge fund managers, I say, sold to them. There will be rallies in bonds that you can trade, but over the long run, I have complete faith that governments and Central Banks will do what they do best - inflate away your hard earned money. Betting against them is betting against history…

|

Send this article to a friend:

|

|

|

We all get it wrong, including Bass, Yusko, Icahn, Dalio, and [insert whatever guru you want in here].

We all get it wrong, including Bass, Yusko, Icahn, Dalio, and [insert whatever guru you want in here].

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/silver/t24_ag_en_usoz_2.gif)