Send this article to a friend:

May

06

2019

|

Send this article to a friend: May |

|

The Company Store Leaves almost nothing to live on

How exactly did the company store system operate?

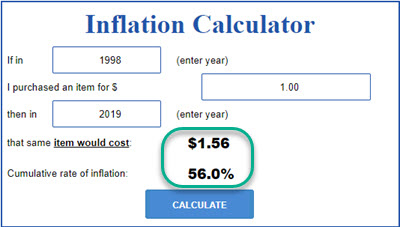

This model was simple enough to understand. “Pay” your workers with scrip vouchers, then sell them your marked up goods at the company store, pocketing a nice profit. On top of that, force your employees to live in company housing, too, also at terms very favorable to the company. Add it all up and the workers found themselves in perpetual service to their employer. No matter how hard and long they toiled, there was nothing left for their own private benefit after all was said and done. The company succeeded in skimming off any and all ‘excess’ for itself. This vast unfairness eventually led to the formation of unions as well as to regulations providing protection to the workers. However, capital never sleeps; and the human temptation to skim and take what they can for themselves is a constant in every hierarchical, post-agriculture society. If the idea of “the company store” was too obvious, then a better method of achieving the same outcome had to be hatched. Something with sufficient additional complexity to defeat the ability of the average worker to detect the nature of the scam. The Financialization Of The Company Store Which brings us to today’s so-called financial markets. Or ““markets”” as I prefer to refer to them, because they don’t actually represent a free and fair system where prices are set fairly. The scam today that’s enabled by these ““markets”” is every bit as egregious as the company store of old; only today’s victims are mostly blind to the way that the system is rigged against them. It’s just sophisticated enough that it mostly evades detection. Or is diffuse enough that even if the scam were detected by a participant, whom would they protest against? The markets? The exchanges? Any of the thousands of funds or private money institutions that are feasting off of the system? It’s a genius set-up. The harvesting is every bit of a violation as the old model, but it’s almost impossible to prosecute. The main losers in this battle, as before, are the primary producers of value: those who labor to extract the primary wealth of the Earth and bring it to market. The farmers, the ranchers, the fishermen, the loggers, the miners, and the refiners. FarmageddonLet’s illustrate how this works for farmers. Or, rather, works against them. The price of any commodity is now set in the financial markets, principally within the futures market where paper contracts are bought and sold by three main participants: producers (the farmers), consumers (ag and food companies) and speculators. In a free and fair world, the price of a commodity should reflect the actual supply and demand for its derived products. We should observe some sort of relationship between the primary source of wealth – the corn, wheat and soybeans for example – and the end food products that consumers buy in the store. I’m going to show you a bunch of commodity data that goes back to the late 1990’s. So let’s start here: inflation has advanced 56% since 1998 according to the BLS and has increased by 60% for food as a subcomponent:

This is a low-end estimate of how far food has actually advanced in price due to inflation over the past 20 years, as the CPI persistently underestimates inflation. Turning now to the farmer, how have the prices received for their products fared over that same stretch of time? In the case of corn, not one single bit. A bushel of corn sells for the exact same (nominal!) price today as it did back in 1996:

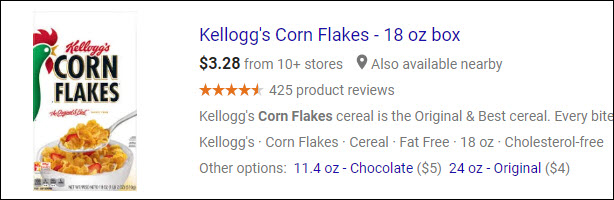

Now think of all the input costs a farmer has to pay to run his or her farm. In 1998, oil traded at $11.61 per barrel. Today its cost is 390% higher than that. At our recent annual seminar (April 26-28, Sebastopol CA, replay video available), a gentleman from Nebraska informed me that the cost of a bushel of seed corn has advanced from $40 to over $400 today. Fertilizers are much more expensive versus 20 years ago. So are tractors, farm land itself, water…you name it. Every single farm input cost has risen strongly over the few decades, but the price of corn is exactly the same as it was 23 years ago. Meanwhile, the consumer has seen the price of a box of cornflakes increase by 44% on average since 1998, from $2.29 per 18-ounce box to $3.28:

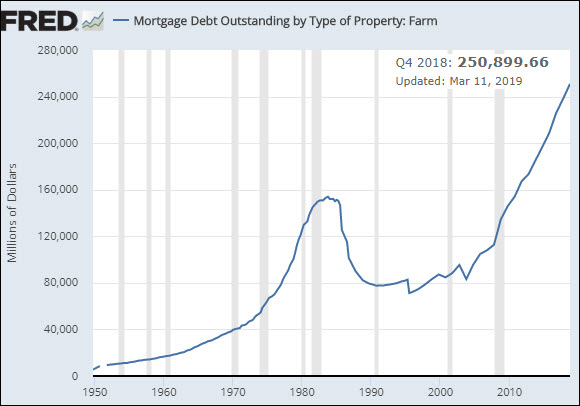

How do the farmers survive this squeeze on their (already tiny) profit margins? How do they cope with flat prices for corn and huge increases in input costs? One way is by abusing their soil — using GMOs, heavy fertilizer and herbicide applications and other tricks to squeeze as much short-term productivity out of every acre they can. But beyond these productivity improvements, which eventually hit a point of diminishing return, what else can a producer do with rising costs and flat revenue? Well, they can go deeper into debt:

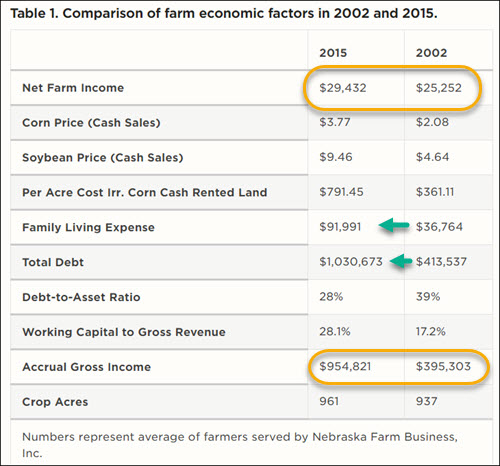

The above chart is of farm mortgage debt. Total farm debt across all credit instruments hit a new record in 2018 of more than $409 billion. Today’s remaining farmers are forced to take on more and more risk. Here’s a table for Nebraska that details the plight. Note that while net farm income remained relatively flat between 2002 and 2015, family living expenses exploded in parallel with total farm debt:

(Source) Expressed as a percentage of revenue, the net profit margins of farms have plunged from 6.3% to just 3.0%. That’s a very skinny margin which leaves very little room for error. One bad season and all reserves are chewed up (and then some):

See the narrative in play? “There’s farm oversupply”. If that were the case then food prices would come down to bring supply and demand into equilibrium. But that’s not happening. Instead, the farmers eat the losses. But the rest of the food delivery chain keeps its prices intact and pockets the difference. Our farmers work exceptionally hard, labor-intensive jobs to produce an absolute essential input to human life. And yet somehow, when all is said and done, they’re left with barely more for their efforts than the coal miners trapped in the system of the company store. Take away a bit of complexity and it’s the same exploitative system as before. It’s just a little less obvious. And instead of a company foreman or owner to rail against, the perpetrators are much more obscure and shadowy. The Scam The principle of any scam is the same as for any successful parasite: take as much as you can but leave the host somewhat alive. Here’s how the modern ‘company store’ scam works. First, you have to convince everyone that money has value, and that that value is very real. Make people crave it and work for it, and take away all of their property and belongings if they run out of it. Do this long enough to reinforce the idea that money is everything. You either have it or you don’t. It need to be regarded as tangible and essential . At the other end of the spectrum, for the big players, print up and distribute as much digital money as needed by the big players to run their various schemes and scams. If they ever get in big trouble, make up a fancy sounding name like TARP or TALF or QE and then talk about how you ‘had to do it’ to save the system and prevent a systemic crisis. Next, be sure that your regulators are unable (though incompetence and/or neglect) to detect price manipulation in the financial markets under even the most egregious of circumstances. No matter how obvious such manipulation is, it’s vital that no investigations be undertaken and, if they are, that they take many years to conduct and come to the conclusion that no wrongdoing happened. Finally, allow an unmanageable swamp of high frequency computer algorithms to take over securities trading, creating a system that is so complex, so secretive and so ripe for fraud and abuse that nobody can unravel the complexity to detect that a scam is even happening. Using this ecosystem of legalized theft, then have the various crooks involved monkey the prices of key commodities to levels that — surprise! — leave hardly any breathing room for the farmers, miners, loggers and refiners to live within. Now that the scam has been exposed, the appropriate question to ask is, “if the producers aren’t getting the benefit of their labor, then who is?” The people running this scam — the financiers, the bankers and their moneyed clients — are the beneficiaries. They make oodles of money, while performing no real work, and taking very little real risk, same as any other natural-born parasite. The Abuse Is Widespread In case you think that I cherry-picked corn as an example particularly favorable to my case, I assure you I didn’t. Here are several key commodities suffering the same abuse:

Regarding the above chart of silver, there are two important factors to note. First, it’s practically impossible to ‘get better’ at mining silver because the ore grades have been declining each year as companies burn through their very best ores in a quest to remain alive. From that alone, we’d expect to see prices climbing higher over long stretches of time like this. Second, the business is very energy and capital-intensive. Yet silver is now at the same price as it was back in 2006, 13 years ago. The orange oval in that chart reveals a decade of pure price suppression that many miners did not survive. This tells us that these scams have been alive and well for a long time. The Bitter Conclusion Run this scam long enough and one day we’ll discover that the banks and their proxy agents — private equity funds, hedge funds, endowments, and family offices, etc — own all of the productive farmland, all of the mines, all of the oil wells, all of the timberland, and every other means of primary wealth production. The former farm and mine owners will be offered roles as “managers” or other types of tenant-farmer arrangements, essentially working for whatever income the labor market can see fit to provide. It won’t be much. At that point, the entire economy will have become a “company store”. We’re well on our way there. The Federal Reserve prints up oodles of money and it goes into “the financial system” which is a code phrase for “to the big banks and big money outfits.” They in turn use these funds to make loans to the primary producers on the one hand, and to drive down the price of commodities with the other hand. Eventually, the farmer has a bad couple of years and his farm is foreclosed on. The land goes up for auction and bought by the highest bidder…which means the buyer with the most money. That increasingly means a big-money type that feasts at the trough of the banking system/money-printing machine. The next thing you know, vast swaths of farmland magically end up in the hands of those with money, which – surprise! – usually turn out to be the same entities feasting on the central bank/free-money machine that’s been operating ever since Alan Greenspan set this slow motion train wreck in process in the late 1990s:

Ageing farmers, increasing ownership of farmland by financial investors, and utterly dismal economics – what’s not to love? The sorry conclusion to all this is that one day, not too far away, we’ll wake up and discover that the majority of US farmland belongs to mega corporations and financial interests, most of whom came across their vast gobs of wealth as a consequence (and a predictable one at that), of the Federal Reserve policy that spurred today’s great wave of financialization. An explosion in farmland prices really kicked into high gear with the Fed’s quantitative easing (QE) programs following the Great Recession – freshly printed money that wound up in the hands of financial firms and interests with few good ideas of where to put it. So some of it leaked over into farmland. The same dynamic has seen firms like Blackrock tap into ultra-cheap Fed money to buy up vast swaths of US housing stock — just to rent back to the same people who couldn’t compete against this leviathan’s all-cash offers, using money that was 75% cheaper than the terms regular borrowers receive. Big Money coupled to Cheap Money leads to this outcome. Every time. Eventually you wake up and discover, with a few clicks on a keyboard, that the bankers and financiers have taken possession of every productive asset. And everybody else has to pay into the company store. This isn’t an accident either, which is why it really galls me to have Janet Yellen, the former Fed Chair, out there for years making the ludicrous claim that the Federal Reserve is ‘not political.’ What could possibly be more political than enabling the removal of the productive assets of a nation – it’s land, its houses, and its mineral rights – and facilitating and cheering their acquisition by a very tiny financial elite? That’s practically the most political act there is. More tragically, it’s just a gussied-up version of working for the company store. We’ve gone backwards. And not in a good way. As one tragic story in a recent article goes:

That’s straight up the 2019 version of the Sixteen Tons refrain: “I owe my soul to the company store”. What the politicians, financial institutions, and Federal Reserve are defending and supporting is a system that utterly lacks in integrity and is strikingly heartless. If we want to create a world worth inheriting, that means we cannot afford a system that forces farmers to fight for their very livelihoods each and every year, barely hanging on, and forced to cut costs to even survive. Cutting costs and boosting productivity means more pesticides, less soil building and a resting, fewer crop varieties, and every other measure of health and complexity upon which our very survival as a species depends. All in service of money. In Part 2: It’s Time To Respond, we detail why it’s so pressing right now to mobilize into action. The opportunity, such as it is, is for us to first recognize this game for what it is (rigged), to take steps to escape the smothering squeeze of financialization being applied to all of us in today’s economy, and then to realign our own actions with the future we wish to see. Click here to read Part 2 of this report (free executive summary, enrollment required for full access).

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/silver/t24_ag_en_usoz_2.gif)