Send this article to a friend:

May

22

2019

|

Send this article to a friend: May |

|

How To Earn More On Your Savings Deposits

Thank you for your interest in this Paper. It is intended to help you earn more money on your savings (while taking less risk), and to give you the ability to discern whether or not you are getting a ‘good deal’ on savings & deposit products, relative to a low-risk product category called: U.S. Treasuries. In this paper we’ll discuss:

Introduction How did we get to a place where teaching somebody how to earn more interest on their savings is like sharing a secret? It’s an open-secret in fact, and the reason, is that sharing the secret generates little to no profit for those who share it. But, by sharing the secret, there are some who stand to lose profits. The primary loser will be your local banker. Here is why: your banker profits from you not knowing this secret. But I’ll spill the beans for you and level the playing field in your direction. Here it is: When you deposit your savings in a bank, the bank has to invest your money, and generate a return greater than the amount they pay you. For example, if your bank pays you 1.00% annual interest rate on your savings, they must use your savings to earn investment returns greater than 1.00%, in order to pay their employees and stay in business. The bank may invest your money in a universe of things (such as providing loans to credit worthy borrowers), but one of the most basic asset classes are government debt obligations—also known as bonds, bills or notes. Government debt obligations issued by the U.S. Treasury Department are known as “U.S. Treasuries,” and are backed by the ‘full faith and credit’ of the United States Government. This is the same entity which issues and manages the U.S. dollar. Also, U.S. Treasuries are taxable at the Federal level, but are exempt from state and local income taxes.1 Bank interest income on the other hand, is taxable at local, state, and federal levels.2 These duration varieties allow the U.S. Treasury to offer convenience to buyers for their short and long term funding & investment needs. For example, a hospital group with $6,000,000.00 on hand may need to spend the entirety on medical equipment 2 years from today. Instead of purchasing the equipment early, or, letting the money sit in a savings account, the group decides to purchase 2-year U.S. Treasury Notes, and earn interest over the period. Or, a married couple sending a child off to college might be facing an upcoming $60,000.00 tuition bill, payable in 4 months. Instead of letting their cash sit in a savings account for 4 months, they decide to purchase a 90-day US Treasury bill, and collect the interest. These cash-management scenarios (and their respective lending/borrowing durations), might sound familiar. If you’ve ever purchased a Certificate of Deposit (CD) from a local savings bank, you’ll notice the deposit timeframes (and fixed interest rate) seem quite similar to U.S. Treasury obligations. There is a reason for that. ------------------ Editor's Note: Treasury “Terminology”3 – There are a few jargon-like terms used when referring to U.S. Treasury durations—those terms are: Bills, Notes, and Bonds.

U.S. Treasury “Bills” (also known as “T-Bills”) are obligations with a maturity (duration) less than 1 year. So a 6-monthTreasury obligation would be referred to as a 6-month Treasury Bill. “Notes” imply maturities between 1-10 years. So a 5-year Treasury obligation would be referred to as a 5-year Treasury Note. “Bonds” imply maturities greater than 10 years. So a 30-year Treasury obligation would be referred to as a 30-year Treasury Bond. ------------------- Capturing the Spread So let’s say you’ve worked very hard for a few decades (or years), and managed to save up USD $1,000,000.00. With the $1m, you decide to purchase an apartment building in your neighborhood. You find the perfect building, and settle on a purchase/closing date, 38 days from today. After discussing the transaction with your banker, a light bulb goes off in her head, and she decides to offer you a 30-day Certificate of Deposit (CD), which will pay you a 1.00% annual interest rate, for those 30 days while you wait for the deal to close. You accept the 30-day CD and earn roughly $833.00 in interest, while you wait. Your banker on the other hand, is now required to use those same monies to earn a greater return than 1.00%, in order to pay you. She decides to purchase a 30-day U.S. T-Bill, in the amount of $1m. At the time of this writing, a 30-day U.S. T-Bill generates about 2.40% annually. Using that rate, your bank earns roughly $2,000.00 interest on your money over the 30-day period—and pays you $833.00, before taxes— leaving them with earnings of $1,167.00! Out of the $1,167.00 gross, your banker earns a $250.00 sales bonus, and the bank itself generates $917.00 in revenue for its shareholders. In other words, your bank “captured the spread” of 1.40% on your money, for the duration of 30-days. Keeping The Spread It would be generous to continue purchasing CD’s from local banks—after all, it may contribute to “employment”. But there is another less charitable route: keeping the spread for yourself. In order to keep the spread, simply skip CD’s or other bank savings products, and buy U.S. Treasury Bills directly. By doing so, the diligent saver in our $1m CD example could take their 30-day interest earnings up to $2,000.00, before taxes – using today’s 2.40% +/- annual rate of interest. I’ll show you how. How To Buy U.S. Treasuries There are two basic methods of buying U.S. Treasury Bills, Notes, and Bonds. They are:

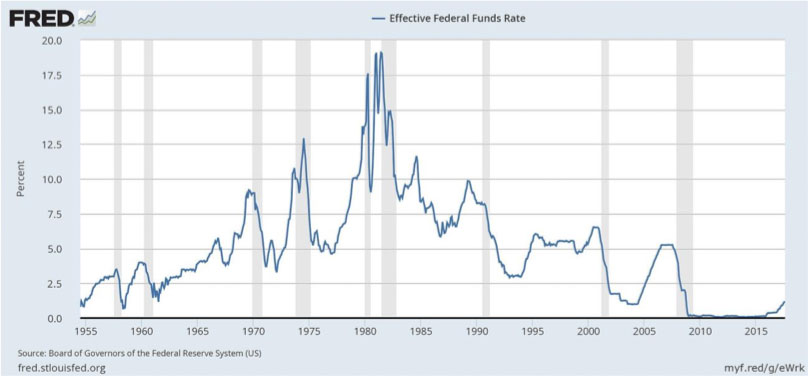

Buying From the U.S. Treasury Directly In 2002, the U.S. Treasury created a website called “Treasury Direct”, located at TreasuryDirect.gov. The website offers personalized accounts which can synchronize with bank checking accounts. After bank account synchronization, one can use Treasury Direct to purchase Bills, Notes, and Bonds directly from the U.S. Treasury. There are weekly treasury auction updates, and lists of various maturities and obligation types to choose from. Interest rate changes are also shown. For a page listing of treasury securities (updated continuously), click here: https://www.treasurydirect.gov/instit/annceresult/annceresult.htm For a page listing of recent interest rates based on maturity (updated continuously), click here: https://www.treasury.gov/resource-center/data-chart-center/interest- rates/pages/textview.aspx?data=yield The biggest advantage (in this writer’s opinion) of purchasing bills, notes, or bonds directly from the U.S. Treasury Dept. via Treasury Direct is cutting out the middleman and saving money. Treasury Direct charges ZERO fees: no account opening fee, no maintenance fee, no transaction fee, no account closing fee, no commission fee – no fees of any kind. Additionally, in this writer’s opinion, buying & holding Treasuries via Treasury Direct may offer lower counterparty risk than holding through a bank or broker-dealer. When an individual deposits monies in a bank or broker-dealer, they are in essence a creditor to that institution. If their account value exceeds FDIC or SIPC insurable amounts, they may be taking on unknown counterparty risk. U.S. Treasuries held at the U.S. Treasury Dept. via Treasury Direct, may be a form of ‘risk-diversification,’ for those individuals with large cash portfolios to manage. The disadvantages of purchasing directly from Treasury Direct include: lack of ‘insurance’ on your purchase, and illiquidity during the duration holding period of the Bill, Note, or Bond. Treasuries sold via Treasury Direct are not insured by the FDIC (Federal Deposit Insurance Corporation). The FDIC serves savings deposit institutions exclusively. Since the U.S. Treasury Dept. is not a savings institution, they are not an FDIC participant. In terms of selling/liquidating a treasury after purchase (ie. getting your money back before the maturity date) - since the U.S. Treasury Dept. is not a broker-dealer, they cannot assist with selling the bill, note, or bond before maturity. Savings Banks offer utility in this regard (along with broker-dealers) in that they allow early termination of the product if you need the funds for some reason. However, the early-termination fees charged by banks may be onerous. Additionally, broker-dealers will charge a sales commission on any selling transaction. Buying Treasuries Using a Broker-Dealer The second method of purchasing U.S. Treasuries (of all durations), is purchasing them on the ‘open market’ using a broker-dealer or other market participant. This process is similar to purchasing stocks using a broker- dealer. To start, simply confirm by telephone with your broker that she offers access to bond markets, and be sure to ask what fees and commissions apply. Once confirmed, simply choose the specific treasury you wish to purchase. Like stocks, treasuries have identifying CUSIP numbers, which function as ‘social security’ numbers for specific issues. It allows for quick reference to specific treasuries, which saves time when purchasing through a broker. A listing page containing CUSIP numbers for continuous offerings of treasuries is available, here: https://www.treasurydirect.gov/instit/annceresult/annceresult.htm The advantages of purchasing treasuries through a broker may include: liquidity and delegation of responsibility. For investors maintaining portfolio cash positions in excess of $100,000.00, inclusion of treasuries may be an important tool. A $100,000.00+ treasury position can be quickly liquidated for a modest commission cost of $10.00- $200.00. For example, if an investor has a $500,000.00 portfolio which is 50% cash ($250,000.00) – they can collect interest at prevailing treasury rates, and in the event of attractive market opportunities elsewhere, they can instruct their broker to liquidate the treasuries and reallocate the funds. Additionally, an individual may delegate the task of portfolio management to a qualified financial advisor. That advisor can rotate (or renew) treasuries as they mature. The disadvantages of purchasing treasuries through a broker-dealer include: commission and fees, size and price requirements, and counterparty risk. Commissions and fees charged by broker-dealers can range from $50.00- $200.00+ per transaction, or, fees may be in the form of a flat percentage charge based on assets under management (such as a 1.00% annual fee). There are also hidden expenses in the market which originate from bond trading desks, located within investment banks that provide access and liquidity in those markets. ‘Market-Makers’ as those groups are generally called, are interested in making money on every transaction, and one needs to expect that any “trade” of a treasury security using a broker-dealer, will generate a stated commission cost and a hidden market making expense. Those hidden expenses might be anywhere from $50.00-$250.00+. While the broker you deal with can best describe the costs associated with a trade, the ultimate effect is a lowering of the obtained (realized) annual yield. For example, if a 90-day Treasury Bill from Treasury Direct yields 2.40% annually, that same bill might yield only 1.80%-2.00% annually after fees, if purchased through a broker-dealer. Assuming a $100,000.00 investment amount, one would need to budget a $50.00-$250.00 expense for commissions and fees. Another disadvantage of purchasing treasuries through a broker-dealer may be minimum size and price requirements. As an example, a broker might require a $100,000.00 minimum size order requirement in order to buy or sell – or, they may require lower pricing that favors market participants, at the expense of the person who wishes to trade. For small size buyers (under $100,000.00), Treasury Direct is optimal as their size minimum is only $100.00 (and there are no fees associated with buying). Counterparty risk is also a concern when using a broker-dealer. If your account value exceeds FDIC or SIPC insured amounts, you might consider learning more about the broker-dealer’s financial health, to determine counterparty safety or risk. Today’s Interest Rate Market In the U.S. today, short-term interest rates are historically low. Short-term interest rates in the U.S. are determined (with monopoly privilege) by a bank called the Federal Reserve Bank. Since the formation of this bank in 1913, all U.S. Banks take their cue (generally) from interest-rate setting announcements by the Federal Reserve Bank. Here is a chart of the short-term “Federal Funds Rate,” as set by the Federal Reserve Bank:

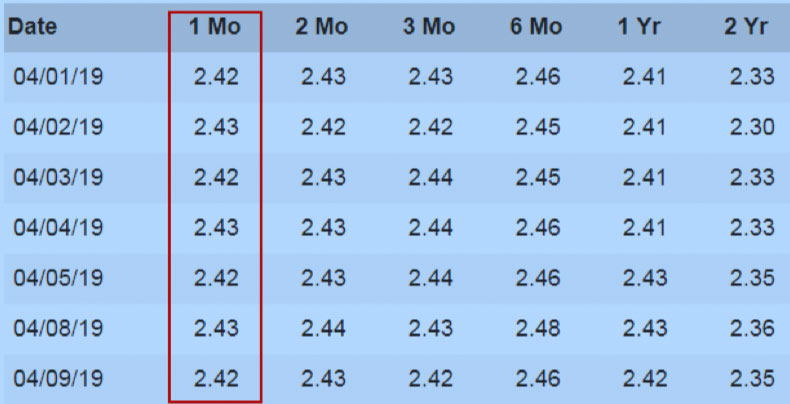

(Source: Wikipedia, “Federal Funds Rate”) The chart above illustrates 70 years of Federal Funds Rate history. Starting in 2009, the Federal Reserve Bank lowered short-term interest rates to nearly zero, in concert with a taxpayer-funded bailout of the U.S. banking industry. The Federal Reserve Bank held rates at 0.00%-0.25% for nearly eight years, while savings banks reduced checking & savings accounts interest rates in similar fashion. This was in effect, an ‘extended’ bailout of the banking industry that allowed banks to borrow from the Federal Reserve Bank at nearly zero – and use those funds to invest elsewhere, and capture the spread. Under the above circumstance, a bank could borrow at 0.25% annually, deploy the funds into government securities such as U.S. Treasury Bills— yielding 1.00%-2.00% annually – and make a fortune. The loser unfortunately, was the American saver – who was paid .10%-.20% (or less) annual interest on their savings, for nearly ten years. Coinciding with changing presidential administrations, the Federal Reserve Bank began raising rates in December 2016 (there was a single increase in Dec. 2015, however). The rate increases have continued into 2019, and as of April 2019, the Fed Funds Rate stands at 2.25%-2.50%. Short-term Treasury bills issued by the U.S. Treasury have also ‘moved up’ (in terms of annual yield) in lockstep with the Federal Funds Rate. As illustrated below by the U.S. Treasury Dept., a 30-day (1 Mo.) U.S. T-Bill now generates a 2.40%+ annual yield:

(Source: Treasury.Gov – Daily Treasury Yield Curve Rates) Still Keeping The Spread An interesting fact is that while short-term interest rates have moved steadily higher since Dec. 2016, checking & savings deposit rates have not followed suit. One might expect savings banks across the U.S. to ‘pass on’ rate increases to depositors, in the form of higher checking & savings account rates. Surprisingly, that hasn’t occurred (on average) across the country, as of the time of this writing. BankRate.com, a bank product website, notes that as of 4/27/2019, average bank product annual yields in the U.S., are:

These low rates indicate savings institutions across the U.S. are not ‘passing on’ higher yields to their customers. Why would they? They are in fact, financially motivated to keep customers in the dark about competing (better) rates available elsewhere. Therefore, if and when U.S. savers realize better rates elsewhere, and begin moving deposits out of savings institutions and into other higher-yielding areas—savings institutions may then decide to increase yields to win back customers. In the meantime, an opportunity exists for savers to move monies into higher yielding products issued by the U.S. Treasury Dept. ----------------- Editor’s Note:

Watch The Spread & Keep Accordingly An open secret in the financial services industry is that simple, low-risk obligations such as those issued by the U.S. Treasury Dept. (Treasuries) are often resold (or re-packaged) to customers at a higher cost. Treasuries are easy to purchase directly from the U.S. Treasury Dept. (via TreasuryDirect.Gov), or through a broker-dealer or other market participant. For individuals with savings amounts under $100,000.00, TreasuryDirect.Gov might be a more useful tool, whereas those with larger amounts might find convenience in using a broker-dealer. Interest rates change over time, but by watching the Federal Funds Rate, U.S. Treasury Rates, and those offered to us by our local bankers, we’ll be in a much better position to be able to “keep the spread” and get the best deal possible. Thank you for reading. [email protected]. Best Important Disclosures: This paper is for information purposes only and is not intended to be an offer or solicitation for the sale of any financial product or service or a recommendation or determination by Sprott Global Resource Investments Ltd. that any investment strategy is suitable for a specific investor. Investors should seek financial advice regarding the suitability of any investment strategy or product based on the objectives of the investor, financial situation, investment horizon, and their particular needs. This information is not intended to provide financial, tax, legal, accounting or other professional advice since such advice always requires consideration of individual circumstances. The products discussed herein are not insured by the FDIC or any other governmental agency, are subject to risks, including a possible loss of the principal amount invested. Investing in securities involves risk of loss that clients should be prepared to bear. No investment process is free of risk; no strategy or risk management technique can guarantee returns or eliminate risk in any market environment. There is no guarantee that our investment processes will be profitable. Past performance is not a guide to future performance. The value of investments, as well any investment income, is not guaranteed and can fluctuate based on market conditions. Diversification does not assure a profit or protect against loss. Generally, securities issued by the United States Treasury as subject to investment risk, including the following:

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/silver/t24_ag_en_usoz_2.gif)