Send this article to a friend:

May

02

2018

|

Send this article to a friend: May |

|

The Fed Has Successfully Destroyed The U.S. Housing Market

As I mentioned to my friend in a private message, I see the same fallacious arguments repeatedly within the housing industry. America is great, deficits and debt don’t matter. Rah, Rah, Rah! I get it. It’s a sales oriented business. What concerns me is when people put their hard-earned money into housing or any other supposed store of value thinking that the sky is the limit. We are living in an age of epic distortions, misinformation and outright fraud. Apparently we learned absolutely nothing from the Great Recession, save for the government and Federal Reserve’s determination/ability to cover it up and pretend like nothing ever happened. As I was writing about the shortage of affordable new homes this morning, I couldn’t help but think about how we arrived here and how the transgressions leading to the last housing crash have been completely swept under the rug. This is not to say that the responses after the housing crash have been any better. We are now surrounded by banks which are larger than ever even as they continue to break the law racking up huge fines that amount to nothing but a slap on the wrist while the CEO reaps a huge payday. Criminality within the U.S. banking system is now a feature, not a bug. This should not be surprising considering the events of the last decade. Getting back to the issue of affordable homes, one of the long cons on the American public continues to be the epic policy failures of the Federal Reserve that facilitated the destruction of the U.S. housing market as they buried the idea of “affordable” homes for the sake of their Wall Street roots. When a smallish, aging 3-bedroom, 2-bath detached home in need of repairs becomes a bidding war for the next young couple who just wants a decent roof over their head, that’s not exactly a healthy housing market or a healthy economy. It’s a sign that something is seriously out of whack with our priorities. Back in January money manager James Stack was making a prescient warning about an overheated housing market, pointing out the excesses and irrational exuberance that were driving home prices and valuations of many builder stocks to extremes. He also keyed in on one of the most critical factors igniting the last housing downturn…The Fed.

While the Federal Reserve continues to claim the U.S. economy is at or near “full employment”, many Americans know different. They know a con when they see one.

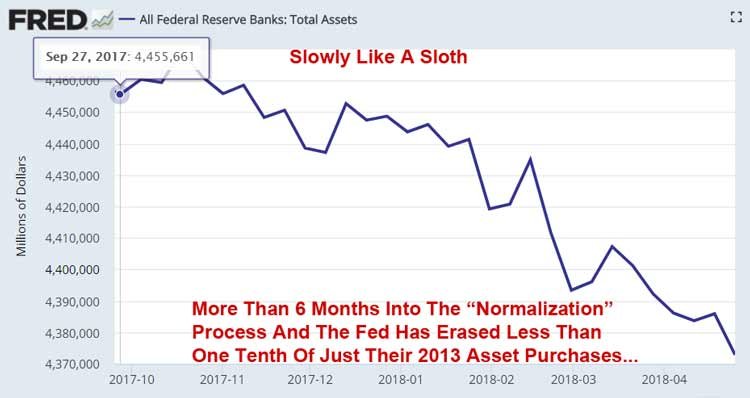

For Kaplan and other Goldman Sachs alumni I’m sure the U.S. economy is pretty close to full employment. Working for the Vampire Squid pays pretty well. For middle America and anybody not in the top 10 percent of wage earners, there is a whole other story to discuss. It’s a conversation the Fed would rather not have of course. The first rule of fight club is that you do not talk about fight club. The Federal Reserve is now embarking on a policy “normalization” to reduce it’s huge balance sheet. This quantitative tightening is already spooking markets and causing ripples within the housing market itself. Now that the Fed is finally pulling back the punch bowl, after nearly a decade of fueling Wall Street’s greed, interest rates are beginning to rise and new U.S. homes are now more UNaffordable than they have ever been compared to median U.S. wages. Of course the Federal Reserve’s army of economists will summarily dismiss the Fed’s culpability for the wreckage they have caused, but the Devil is in the details. There’s a reason the Fed is taking a sloth-like pace with their balance sheet reduction. We are now more than 6 months into this monetary adventure and the Fed hasn’t even drained off $100 billion from their balance sheet…

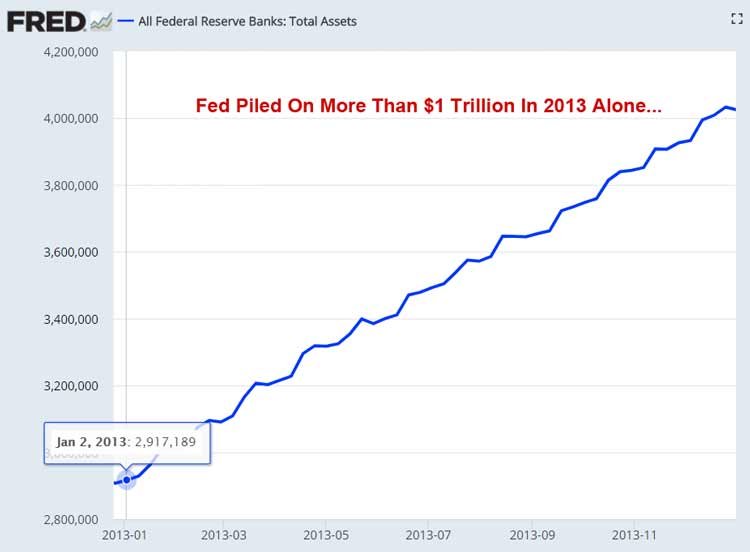

If the U.S. economy were really that healthy and we were truly at or near full employment, the Fed would have no problem at all draining off $85 billion per month, the same amount they were adding back in 2013 with QE-3!

While the Federal Reserve and other central banks have been busy inflating their balance sheets and virtually every asset under the sun, they have also been accelerating wealth and income inequality in the process as asset price inflation has far outpaced wage inflation…

It should go without saying that Federal Reserve officials are somewhat lacking in the credibility department. This should come as no surprise. If they were completely honest with the American public, I suspect Congress would be forced to revoke their charter. Author and Wall Street veteran Nomi Prins expounds on the collusion among central bankers… “Two months later, I found myself sitting in front of a room filled with central bankers from around the world, listening to Fed Chair Janet Yellen proclaim that the worst of the crisis and its causes were behind us. In response, the first thing I asked that distinguished crowd was this: “Do you want to know why big Wall Street banks aren’t helping Main Street as much as they could?” The room was silent. I paused before answering, “Because you never required them to.” Nomi Prins If you are out shopping for a home during this summer selling season and you are having a difficult time finding a good property at a reasonable price, be sure to thank the folks at the Fed for their fine work. Destroying a market takes some effort, particularly if you account for all of the PR necessary to cover your tracks. The Federal Reserve and their army of economists have created another fine mess in the U.S. housing market, destroying real price discovery and distorting the real value of a home which is end-user shelter.

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/silver/t24_ag_en_usoz_2.gif)