Send this article to a friend:

May

10

2018

|

Send this article to a friend: May |

|

The Donald's Fabulous Fiscal Folly And Wall Street's Wile E. Coyote Moment

In any event, fixing to borrow upwards of $1.2 trillion in FY 2019, Simple Steve apparently didn't get the memo about the Fed's unfolding QT campaign and the fact that it will be draining cash from the bond pits at a $600 billion annual rate by October. After all, no one who can do third-grade math would expect that the bond market can "easily handle" what will in effect be $1.8 trillion of homeless USTs:

Then again, Simple Steve is apparently not alone in his fog of incomprehension. Even if you did get the memo---like most of the Wall Street day traders---you might still be under the delusion that the Fed is your friend and that when push comes to shove, it will put QT on ice in order to forestall any unpleasant hissy-fitting in the casino. That is, it's allegedly still safe to buy the dips or play the swing trade between the 50-DMA and 200-DMA because the Powell Put undergirds the latter. So never fear dear punters: At about 2615 on the S&P 500 (the current 200-DMA), the Eccles Building cavalry will ride to the rescue. That would appear to be the meaning of the chart below---except it isn't. What it really says is that after nine years of buying the dips successfully, Wall Street has essentially deputized its own cavalry. Accordingly, for the last two years the 200-DMA has held---but the buying spurts have been entirely faith-based, not Fed enabled. Well, except in the passive sense that open-mouth policy in the form of benign "forward guidance" and a tepid pace of rate increases have mis-directed---even euthanized---the Wall Street punters (as possibly intended). But QT and the huge cash drain in the bond pits is really where it's at. And if Simple Steve doesn't know it, the day traders and robo-machines are now simply choosing to ignore it---until they can't. What we are saying is there is no "Powell Put" at 2615 (200-DMA) or 2460 (400-DMA) or even 2250 (800-DMA). To the contrary, there is in our judgment 15-20% of downside before the Fed relents, but by that point it will be too late. To wit, when the Powell Put fails to appear as expected, the casino will have its Wile E. Coyote moment. And at that point there will be nothing to stop the doomsday machine of ETFs/vol shorts/risk parity trades/levered bond funds/CTA trend followers and combustible bespoke gambles from plunging off the high cliffs of Bubble Finance.

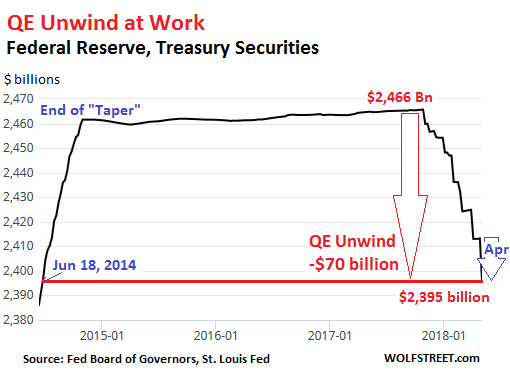

You could call it a perfect storm. Simple Steve and the Donald are completely clueless about the fiscal monster they have unleashed, while the arrogant overlords of the central bank truly believe they have bestowed the main street economy with ox-like strength and self-fueling forward momentum. Accordingly, QT is not "data dependent" and is viewed by Powell and his posse as operating on auto-pilot. They are, in fact, not even mentioning it any longer in their post-meeting commentary. As is clear from the chart, however, the great shrink is happening. And the $70 billion shown here is just the UST side of the bond dumping campaign. There is another 40% share of the shrinkage coming from the run-off of what was once the Fed's $1.8 trillion GSE portfolio, as well.

To be sure, the Fed heads may bobble-and-weave on the precise number and timing of the parallel interest rate rises depending up the second decimal point of gains in the PCE and AHE (average hourly earnings). But that's the misdirection. The main event is QT and the $600 billion bond dumping experiment, and the latter is not at all about forestalling inflation or staying ahead of the curve. Instead, it's about the Fed's permanent institutional franchise and the preservation of its unparalleled power base. In turn, that requires re-loading the Fed's dry powder with all deliberate speed--- in order to be adequately provisioned for the next recession. With only 13 months left before even the freakishly long expansion of the 1990s (119 months) is in the rearview mirror, even the Keynesian monetary central planners at the Fed can see the hand-writing on the wall. And they also know that they dare not risk a recession without a prompt Fed-bestowed stimulus cure---least they end up succumbing to the same public ridicule as the proverbial Naked Emperor. Perhaps that's why we are hearing such brave talk from the Fed's effective #2 head honcho, John Williams. The latter has spent a lifetime at the San Francisco Fed and is soon to takeover the top job at the New York Fed, which actually executes the central bank's day-to-day intrusions in the financial markets; and equally importantly, Williams embodies and formulates the FOMC group-think about as well as any among the inner circle. Having perhaps already forgotten the delusionary talk of the summer of 2007, Williams averred recently that there is no reason to hesitate on the Fed's normalization campaign. Said he,

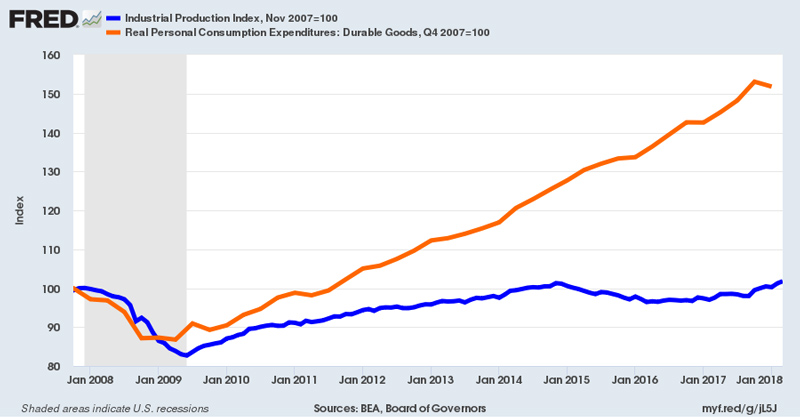

Folks, if that doesn't scare the bejesus out of you, we can't imagine what would. After all, unless you think that industrial production is totally dispensable in today's world of 24/7 social media enthrallment, what we have on main street is just about the polar opposite of "goldilocks". To wit, real production of industrial output is up a scant 1.2% since the pre-crisis peak ten years ago, while consumption of real durable goods has soared by 53%. We'd be more than willing to bet that isn't sustainable---nor is it a remotely reasonable basis for the Fed to declare "mission accomplished" with respect to main street prosperity.

Still, that get's us to the great bond market collision dead ahead. For the first time in history, the combined financial arms of the state---the Treasury and Fed--- will be selling government debt, existing and new, with malice aforethought. And it's not just the bloated size of the borrowing nut---although the record issuance of $488 billion during Q1 alone should be come kind of wake-up call even as to girth. The real scary part, however, is the timing and the cyclical setting. We are now in month #107 of the current so-called business expansion and Washington's combined financial arms will be dumping $1.8 trillion or nearly 9% of GDP into the bond pits. By contrast, at the peak back in Q4 2000, Uncle Sam was running a 2.3% of GDP surplus and the Fed was still absorbing existing debt at a $40 billion annual rate. At current economic size, that would amount to a $500 billion rate of combined arms supply of cash into the bond market. Needless to say, the difference between draining $1.8 trillion of cash from the bond market in the up-coming fiscal year versus supplying $500 billion back then is the difference between financial night and day. Likewise, even after two unfinanced tax cuts and two unfunded wars during the George W. Bush tenure, Washington's combined arms drain of cash from the bond market was only $140 billion in 2007 or just 1.0% of GDP. That puts us in truly uncharted waters where the sheer math of the thing promises carnage on both ends of the Acela Corridor. We'd bet that before long Simple Steve will be sweating profusely and the Wall Street punters will rue the day they placed their chips on the non-existent Powell Put. As for goldilocks, cursed will be her name in the corridors of the Eccles Building----even as the monetary central planners flee the building.

davidstockmanscontracorner.com

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/silver/t24_ag_en_usoz_2.gif)