Send this article to a friend:

May

08

2017

|

Send this article to a friend: May |

|

Sympathy For The Devil?

In our recent report, Banks Are Evil, we pulled no punches in makingthe accusation that the financial system is the root cause of injustice in today's society. It's a good blood-boiler. You should read it if you haven't already. Its main premise is this:

But all is not roses if you're a banker these days. Even within the evil machine, there is great disparity in how the plunder is being divided. Bad Times For Bankers? A guy I've known since childhood works on the 'sell side' (investment/commercial banking, stock brokers, market makers) and has been telling me how cutthroat things have become over the past few years. The pay structure and job security have deteriorated notably. And he says the same is true for many of his colleagues on the 'buy side' (hedge funds, asset managers, institutional investors), too. Really? Even with enjoying the "unabated bonanza" described above, even with the markets back partying at all time highs, things are getting worse for many bankers? Yes. And while I personally can't conjure any sense of empathy for these poor devils, it looks like things are going to get even harder for them. So what's going on here? Well, it's mostly a story of the banking system's plundering ways coming back to bite it. Capital Is Fleeing From Active To Passive Funds First off, by flooding world markets with over $12 Trillion since the Great Recession, the central banks have pretty much destroyed "alpha". Alpha is the "excess return" that fund managers' fees are based on -- i.e., "you're paying more for a smart guy like me to 'beat the market'". But when a tsunami of liquidity rises all boats at once, it's that money flood (i.e. the central bank money printing) that drives valuations. And its influence is so much larger than any other factor that it's really the only factor that matters. Great and crappy companies alike rise in price -- the "fundamentals" that fund managers use in their analysis become useless. Which is why 66% of large-cap active managers failed to top the S&P 500 in 2016, and why 90% missed their benchmarks over the past 15-year period. So it's no wonder that investment capital is fleeing from actively-managed funds to passively-managed ones. If the passive funds have much lower fees AND they perform better than the actively managed ones, why they heck shouldn't money flow into them? Per CNBC:

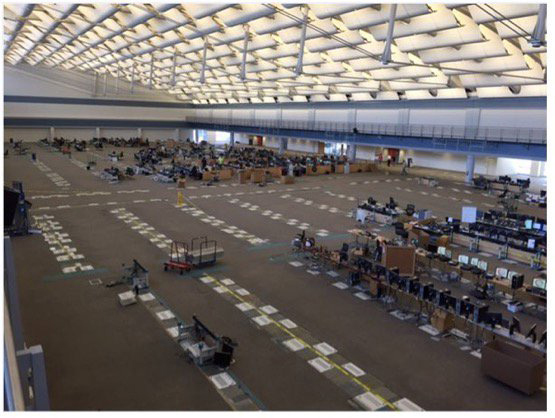

The result of this is tremendous mounting pressure for active managers to reduce their fees. Lower fees being charged on shrunken fund pools obviously affords fewer asset managers, who in many cases are now working for less compensation. Keep in mind, between just the ECB and the DOJ, nearly $200 Billion of additional liquidity has been -- and continues to be -- injected into world markets each month(!). So, as the above article says, don't expect the tidal wave of capital fleeing actively-managed funds to stop while the central banks' liquidity spigots are still flowing. The White-Collar Cost Of Automation Finance was one of the first industries to embrace the automation boom, given the obscene profits that could be made. In his book Flash Boys, Michael Lewis described how the arms race of high frequency algorithms literally changed the game in terms of how financial instruments are traded -- and made $billions upon $billions of unfair profits for the big banks that invested in the technology. Well, many of the bankers who cheered the boost the machines gave to their annual bonuses aren't cheering so much now. You know what algo-driven markets don't need? Human traders. Below is photo of the UBS trading floor from 8 years ago, contrasted with one from this year (source: Zero Hedge): 8 Years Ago

Now

Per the Wall Street Journal:

Here's another stark example:

As warned of in our earlier article Automating Ourselves To Unemployment, jobs lost to automation don't come back. More than that, the technology itself lowers the cost structure, ultimately lowering industry profits as other competitors invest in similar tech and the margins are competed down:

A Cultural Shift To Cost-Cutting And the jobs cuts aren't just related to technology. As profit margins are squeezed, players in the financial industry are looking for any and all reasons to cut costs. A current victim of this trend is equity research. For decades, sell side firms like the investment banks offered their clients "expert analysis" from their research departments. Historically, that was bundled into the bank's overall fee it charged its clients. But now, increasingly cost-conscious clients are demanding to know how much that research is costing them. Especially since almost all of that research doesn't even get read. A recent Reuters article showed that of the 40,000 research reports produced every week by the world's top 15 global investment banks, less than 1 percent are actually read by investors. It's long been a poorly-kept secret that the research departments were a dependable vehicle for investment banks to bilk their clients for unnecessary profit. Now it looks like that ruse is over. And billions in revenue per year along with it:

An industry long known for its "Wolf of Wall Street" culture of excess is now counting its pennies. That's a very significant perception shift. A Sign Of The End What's important about all this is not sympathy for the poor bankers who have to accept lower wages or a pink slip. Consciously or unwittingly, they've been foot soldiers for a cabal that's done the greatest evil towards global human rights and prosperity over the past century. Personally, I'll happily take a front row seat, open up a bag of popcorn, and delight in the schadenfreude of watching that industry collapse on itself. What is important is what all this tells us about where we are in this story. We are now getting close to the end. For decades and decades, more and more sharks found their way into the financial industry. And for decades and decades, there was plenty of prey for them all to feast and fatten on. But now we're at the point where there's much less to prey on. So the biggest sharks are now turning on the smaller ones. Those at the top of the industry are trying to preserve their share of the pie -- and if they have to do so by cannibalizing those below them on the org chart, so be it. It has now become a shark vs shark world. That's important. This is happening, mind you, at a time when the banks are in their 8th straight year of enjoying practically-free money from the world's central banks, which is essentially a great wealth transfer from the public's coffers. And at a time when financial assets have been re-inflated to all-time highs. If things have reached this cutthroat a state when Wall Street is booming, imagine how much more gruesome this "eating their young" dynamic can/will become during a market downturn. We're at the point where those at the apex of power are becoming increasingly desperate to maintain their unfair advantage. And as the economic pie refuses to grow due to the twin overload of too much debt and declining net energy, these apex predators will turn on each other -- first to maintain their spoils, and then simply to survive. Things will get nasty in a hurry during that stage, as we warned about in our recent report: Positioning Yourself For The Crash. While you still can, you want to make sure the bulk of your investment capital is positioned for safety, and you want to make your lifestyle as resilient as possible so that, no matter what jarring developments the future may bring, you and the ones you love are least impacted by them. Click here to read the report (free executive summary, enrollment required for full access)

Adam is the President and Co-Founder of Peak Prosperity. He wears many hats, but his basic job is to handle the business side of things so that his fellow co-founder, Chris Martenson, is free to think and write. Adam is an experienced Silicon Valley internet executive and Stanford MBA. Prior to partnering with Chris (Adam was General Manager of our earlier site, ChrisMartenson.com), he was a Vice President at Yahoo!, a company he served for nine years. Before that, he did the 'startup thing' (mySimon.com, sold to CNET in 2001). As a fresh-faced graduate from Brown University in the early 1990s, Adam got a first-hand look at all that was broken with Wall Street as an investment banking analyst for Merrill Lynch. Most importantly, he's a devoted husband and dad.

www.peakprosperity.com

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/silver/t24_ag_en_usoz_2.gif)