Send this article to a friend:

April

24

2019

|

Send this article to a friend: April |

|

The Fed’s key interest rate keeps climbing, and that could become a problem

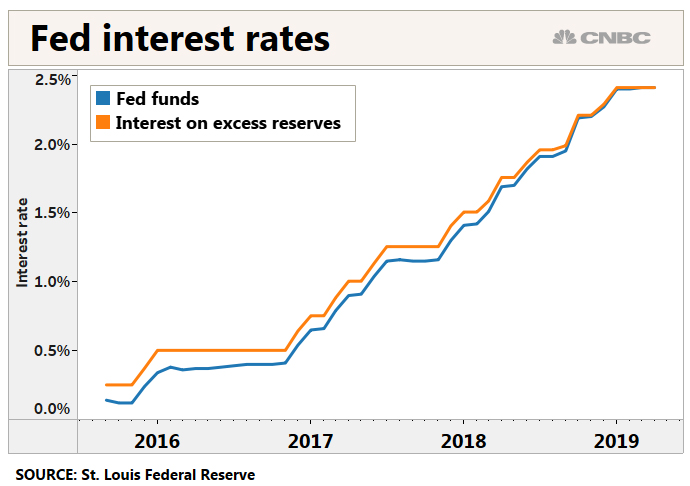

In recent days, the effective fed funds rate, which targets the overnight level that banks charge each other for loans, has moved up to 2.44%. That’s the highest since March 2008 and is just 6 basis points from the top of the target range and the closest to the top since December, when the Fed last raised rates. For now, the move is looked on as not being especially problematic given that there is still room between the current level and the top of the 2.25% to 2.5% range in which the rate is supposed to trade. But moves toward the upper end of the band have prompted action before, and the trend likely will be a topic of discussion at next week’s Federal Open Market Committee meeting.

When the Fed first began raising rates in December 2015, it succeeded in keeping the funds rate around the midpoint of the target range. But that has changed over the past year. “At 6 basis points from the top of the range, you’re still within the target. The question becomes whether they think technical pressure is driving this,” said Lou Crandall, chief economist at Wrightson ICAP and formerly of the New York Fed. “The only concern is whether you’ll have to make a technical adjustment in the future from preventing it from going higher.” The Fed, in fact, has made adjustments before to try to keep its benchmark rate in line. Twice in 2018 the FOMC approved 20 basis point increases in the interest it pays on excess bank reserves, or the IOER, rather than the 25 basis point hikes it approved for the funds rate. The IOER generally has been raised at the same time as the funds rate and has acted as a barrier against the benchmark’s rise. The 20 basis point hike was aimed at containing the rise of the funds rate as it reached the upper bounds of the target range. However, the funds rate for the first time is now trading above the IOER, which technically is set as a floor for the EFFR but has more often acted as a ceiling. The FOMC may consider another adjustment to the funds rate next week, though at this point that is unlikely. “That’s certainly possible down the road, But they’d have to actually be threatening to breach the target range for them to try to explain to the public why they are doing that,” Crandall said. A market puzzle Why the funds rate has risen above the IOER is somewhat of a market mystery, though Fed officials attribute it to higher yields on the reverse repo markets that have pushed up the EFFR. Some market participants have feared that the Fed’s balance sheet reduction program, in which it is allowing some proceeds from its bond portfolio to roll off each month, also could be exerting upward pressure on rates. For now, officials remain largely unconcerned with the funds rate passing IOER. “As long as these rates remain relatively stable and at modest spreads above IOER, we don’t see this as indicating that reserves are not well supplied,” Lorie K. Logan, senior vice president at the New York Fed, said in a speech last week. Another possible factor for the move higher in the funds rate is outflow from money market mutual funds around the April 15 federal income tax deadline, according to strategists at Bank of America Merrill Lynch who think there’s not much chance the Fed will make an IOER adjustment for now. “The recent FF rise has increased speculation the Fed might consider an imminent IOER reduction, possibly at the May meeting next week,” Mark Cabana and Olivia Lima, rates strategists at BofAML, said in a note. “We think this is premature. It would likely take FF increasing to and remaining at 2.45% before the Fed seriously considers such a move.” Different this time An adjustment to the IOER could come in an unfamiliar situation for the Fed. In the previous two technical adjustments, the Fed was raising rates a quarter point while moving the IOER up just 20 basis points. With no rate hikes on the horizon, it’s unclear how an IOER move would work. There’s also the question of communication: The market can be easily rattled by Fed rhetoric, and central bank officials might have a hard time explaining why it is taking more corrective action. With the Fed walking a monetary policy tightrope, any irregularities are bound to garner attention. The FOMC has telegraphed that it won’t be raising interest rates and it also set a timetable to halt the balance sheet reduction. Messaging around the policy normalization has been messy, with markets revolting after Fed Chairman Jerome Powell last year indicated more tightening was ahead. A policy pivot this year has reversed the damage. Bond market veteran Kevin Ferry said the current move of the funds rate is probably “technical” in nature but said it’s unusual for the rate to be rising while most traders would prefer it lower and as the Fed has indicated a dovish posture. “If there’s a danger, it’s that they’re beyond what the market would price in right now.That’s going to cause some tightening,” Ferry said. “They’ve never been ahead of the market. They’ve always been behind the market.” If the situation persists, he anticipates the Fed will have to make an adjustment to the IOER. “The question is, do you do it proactively and deal with all the repercussions, or do it retroactively with a big lee time?” Ferry said. “My favored methodology for efficacy is the first. But they’re opting for the latter.”

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/silver/t24_ag_en_usoz_2.gif)