Send this article to a friend:

April

13

2019

|

Send this article to a friend: April |

|

What Ballooning Corporate Debt Means for Investors

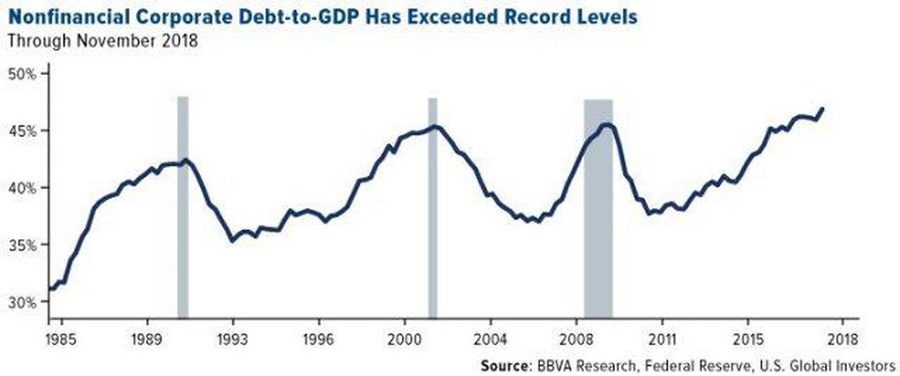

Considered by many to be a Wall Street permabear, Rosenberg successfully predicted the 2007-2008 financial crisis. Now he’s predicting another recession to make landfall as soon as the second half of this year. Why? In short, the Fed has been too aggressive tightening liquidity at a time when corporate debt is at an all-time high. What’s more, the Trump administration has already enacted fiscal stimulus in the form of tax reform, which has historically been reserved for times of economic turmoil, not expansion. “How are we going to stimulate fiscal policy [in the event of a recession]?” he asked recently on CNBC’s Trading Nation. “We already did that at the peak of the cycle. We don’t have the fiscal ammunition.” Corporate Debt Nearing Half of U.S. GDP Rosenberg recently spoke at the CFA Societies Texas Investor Summit in San Antonio, U.S. Global Investors’ hometown, where he laid out his thought process. Since the last recession, nonfinancial corporate debt has ballooned to more than $9 trillion as of November 2018, which is nearly half of U.S. GDP. As you can see below, each recession going back to the mid-1980s coincided with elevated debt-to-GDP levels—most notably the 2007-2008 financial crisis, the 2000 dot-com bubble and the early '90s slowdown.

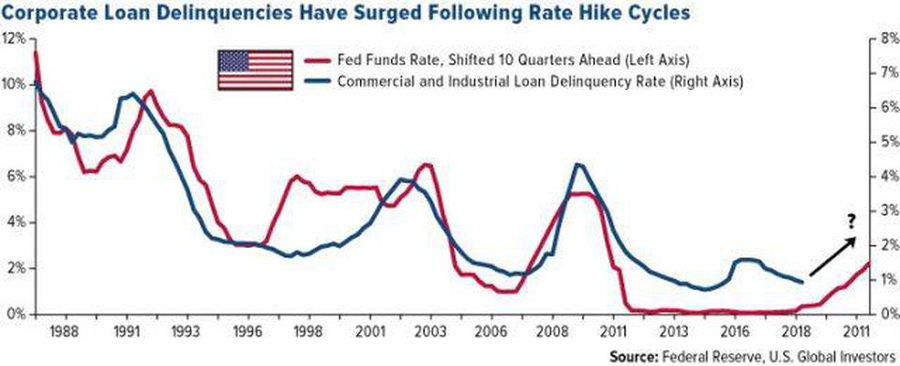

Nonfinancial Corporate Debt-to-GDP Has Exceeded Record Levels Through 2023, as much as $4.88 trillion of this debt is scheduled to mature. And because of higher rates, many companies are increasingly having difficulty making interest payments on their debt, which is growing faster than the U.S. economy, according to the Institute of International Finance (IIF). On top of that, the very fastest-growing type of debt is riskier BBB-rated bonds—just one step up from “junk.” This is literally the junkiest corporate bond environment we’ve ever seen. Combine this with tighter monetary policy, and it could be a recipe for trouble in the coming months. During his presentation, Rosenberg reiterated the saying that business cycles don’t die of old age, but rather they’re killed by the Fed. Take a look at the chart below. It shows commercial and industrial loan delinquency rates, overlaid by fed fund rates shifted 10 quarters ahead. What it suggests is that roughly 10 quarters after the Fed began to tighten, loan delinquencies surged.

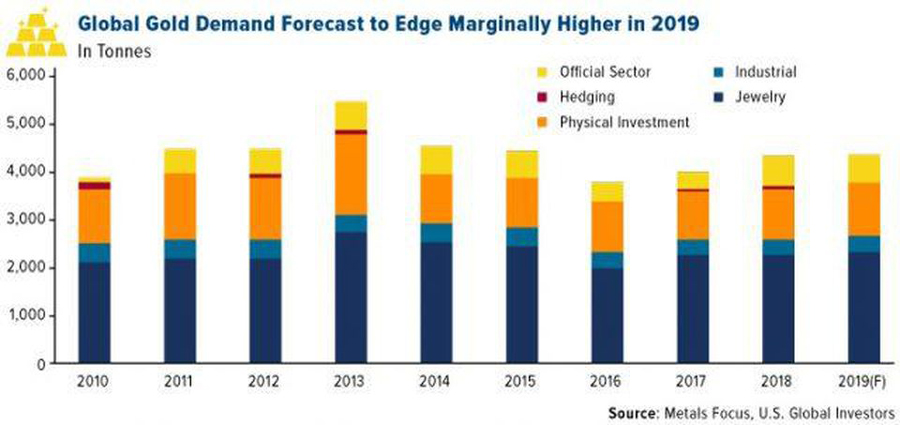

Corporate Loan Delinquencies Have Surged Following Rate Hike Cycles The good news is that it’s been more than 10 quarters since the Fed started lifting rates in December 2015, and so far we haven’t seen a noticeable increase in delinquencies. Could this be because the rate hikes this cycle have been small relative to those in past cycles? Not likely, says Rosenberg. According to him, it’s not the amount that matters so much as the change. Whether rates go up 2.50 percent or only 0.25 percent, it can still be a shock on the financial system. To be clear, I’m not predicting a recession any time soon, only passing along Rosenberg’s expert opinion. But if his position makes sense to you, it might be time to consider your options on how to prepare. Rosenberg recommends overweighting fixed-income and REITs (real estate investment trusts). I would add gold to that mix, as it’s performed well as a store of value during economic pullbacks. As always, I recommend a 10 percent weight in gold, with 5 percent in gold bars, coins and jewelry, and 5 percent in gold stocks, mutual funds and ETFs. Global Gold Demand Forecast for 2019 I want to end by sharing some excellent news from Metals Focus. The London-based commodities research group just released the 2019 edition of its widely-read Gold Focus report, and the big news is that global gold demand will climb to its highest level in four years. The uptick is expected to be driven by an increase in jewelry fabrication, with India, China and Italy leading consumption higher.

Global Gold Demand Forecast to Edge Marginally Higher in 2019 Interest in gold jewelry has indeed improved in recent years, a phenomenon we’ve noticed with the success of such companies as Menē. Late last year, Google inquiries for “gold jewelry” hit an 11-year high. But there’s more to the story than the Love Trade. Metals Focus analysts see gold also benefiting from a more dovish Federal Reserve and fears of a global economic slowdown. “We expect U.S. real gross domestic product (GDP) to slow in 2019 and 2020,” comments Metals Focus Director Nikos Kavalis. “This reflects a natural tapering, following two very strong years, the fading of windfall gains from the late-2017 tax reforms and, eventually, also the impact of trade wars on U.S. consumer spending.”

Frank Holmes is the CEO and chief investment officer of U.S. Global Investors. Mr. Holmes purchased a controlling interest in U.S. Global Investors in 1989 and became the firm’s chief investment officer in 1999. In 2006, Mr. Holmes was selected mining fund manager of the year by the Mining Journal, and in 2011 he was named a U.S. Metals and Mining “TopGun” by Brendan Wood International. He is also the co-author of The Goldwatcher: Demystifying Gold Investing. More than 30,000 subscribers follow his weekly commentary in the award-winning Investor Alert newsletter which is read in over 180 countries. Under his guidance, the company’s mutual funds have received recognition from Lipper and Morningstar, two trusted independent financial authorities. In 2015, Mr. Holmes led the company into the exchange traded fund (ETF) business with the launch of the U.S. Global Jets ETF, which invests in the global airline sector.

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/silver/t24_ag_en_usoz_2.gif)