April

23

2013

23

2013

|

April 23 2013 |

The 3 Faces Of Silver

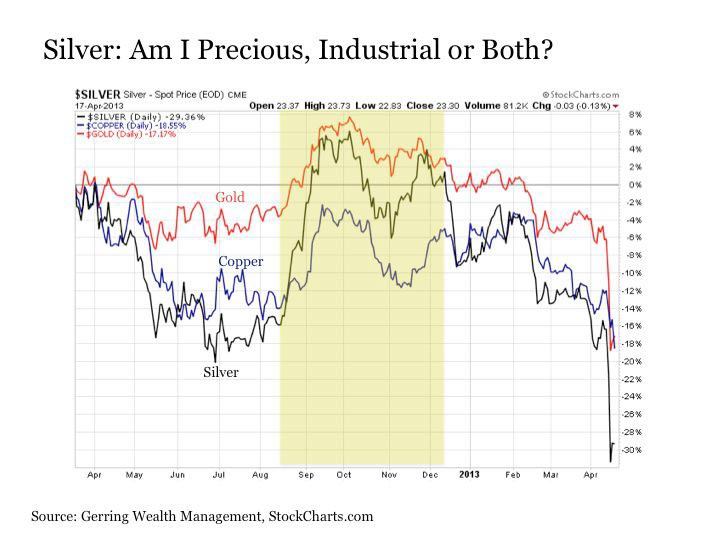

Silver has its own unique place in the investment universe. This is due to the fact that it has two very distinctly different personalities. And there is no telling exactly what face silver will be wearing at any point in time. At one moment, it is a precious metal serving as a hard asset store of value for investors seeking safety against currency debasement and global instability. The next moment, it is an industrial metal that is highly sensitive to the vagaries of the global economic cycle. But knowing that silver is prone to flipping between these two different identities can also be instructive, particularly when trying to assess its future path in the wake of what has been a most violent correction in the white metal over the last few days. It may also provide a leading signal of what we might expect from other important segments of investment markets. A closer look at silver (SLV) over the past year reveals how quickly its personality can flip from one identity to another. During the spring and summer of 2012, silver was behaving like an industrial metal as it moved in virtual lockstep with copper (JJC), which of course is widely considered a leading indicator of the economy. But starting in August 2012, silver's identity suddenly flipped into precious metals mode, as it quickly departed from copper's path and surged higher to join the path of gold (GLD). This behavior continued through mid December 2012 when silver's behavior abruptly switched once again, as the white metal plunged lower to rejoin the path of copper. And this remained the case up until last Friday, when all of the sudden silver assumed a third face and plunged by -17% into a violent episode of epic proportions.

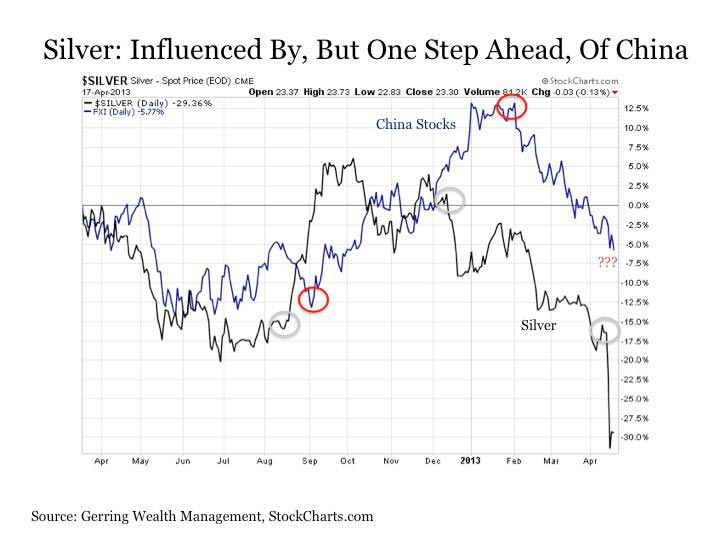

What exactly can silver's rapidly changing personalities be attributed to? This is where a new player comes into the picture. Since the outbreak of the financial crisis back in late 2008, the sentiment surrounding the China stock market has been highly correlated with price movements in silver. For when China stocks as measured by the iShares FTSE China 25 Index ETF (FXI) have been flat or rising, silver has fully embraced its identity as a precious metal. But if the China stock market falls into correction, silver switches to its industrial side. What is most notable about this relationship, however, is the fact that these abrupt personality transformations in silver will precede inflection points lower in China stocks by anywhere between two to six weeks.

It is difficult to say whether silver has assumed an entirely new third personality with its recent move to the downside starting on Friday. But it is more likely that silver reassumes one of its two more typical behaviors once the dust settles from its recently staggering move lower. As a result, it is reasonable to consider not only what path silver is likely to follow from here, but also what silver's recent move might suggest for other investments that have been related to it in the past. This leads to the following potential conclusions. Given that silver has disconnected so dramatically in a forced mass liquidation, one potential outcome is that it regresses back toward the mean and bounces back higher to rejoin what is still at least for now the downward path for both copper and China stocks. On the other hand, given that silver has demonstrated itself to be a leading indicator for movements in China stocks, perhaps the recent correction in silver is foreshadowing what may soon be a crash in Chinese shares. Such an outcome would also likely be equally damaging to copper, which has also shown an even stronger and more coincident relationship with China stocks. Of course, neither of these outcomes would be positive signals for global economic growth, which at some point is bound to have negative spillover effects on the U.S. stock market (SPY). A third possibility is that China stocks eventually stem their recent decline and silver at a minimum rejoins the path of its precious metal partner in gold. The catalyst for such an outcome could be the new government in China following through on recent speculation that they intend to launch a new monetary stimulus program during the current quarter. The net of these scenarios suggests the following. Unless both China stocks and copper crash down to match silver's recent move lower, which is certainly a real possibility, the white metal has the strong potential to experience at least a near-term sharp snap back to the upside as it regresses to the mean and rejoins the path of China and copper. And if China does opt to enter into a fresh new stimulus program in the near-term that stabilizes the China stock market, we may not only see silver return to its precious metals identity, but both gold and silver may find themselves moving sustainably to the upside in unison. The next several days and weeks will be most telling in determining exactly what scenario we see play out. In the meantime, I continue to hold positions in the Central Gold Trust (GTU), the Central Fund of Canada (CEF), the Sprott Physical Silver Trust (PSLV) and Silver Wheaton (SLW), as these all represent precious metals positions that have been in place for much of the last decade and continue to provide important portfolio diversification despite their recent volatility.

In addition to his work with Gerring Wealth Management, Eric serves as a professor in the Economics and Finance Department at West Chester University teaching courses in Finance, Economics and Statistics. Eric is a graduate of Dickinson College (BS Mathematics and BA Economics) and Drexel University (MS Finance). He also holds a variety of distinctions including the Chartered Financial Analyst (CFA) designation and is a member of Phi Beta Kappa. Prior to starting Gerring Wealth Management, Eric served as the Director of Investment Communications for SEI Investments and as an Economist for Moody's Analytics. This post is for information purposes only. There are risks involved with investing including loss of principal. Gerring Wealth Management (GWM) makes no explicit or implicit guarantee with respect to performance or the outcome of any investment or projections made by GWM. There is no guarantee that the goals of the strategies discussed by GWM will be met.

|

|---|

Send this article to a friend:

|

|

|

Eric Parnell is the Founder & Director of Gerring Wealth Management (

Eric Parnell is the Founder & Director of Gerring Wealth Management (