March

04

2013

04

2013

|

March 04 2013 |

On Gold, the S&P and a Vespa

As you know, we like such negative correlation -- indeed have been expecting it -- for upon the tables turning, (i.e. down for the S&P), ëtwill be correspondingly up for Gold, should such correlation hold. We're on record for this to occur during Q1 of 2013 and thus have just four weeks left for this perfectly sensible phenomenon to at least commence, as we've pointed out that it has done those many times over the past 12 years. And as we'll see below in this week's missive, the S&P remains up in the silly zone, whilst Gold is beyond due for its next material up leg whether you measure it fundamentally, structurally or technically. We begin straight away with demonstrating why the S&P is trending on borrowed price, (literally so for those on margin), and why upward Gold is good to go. And I mean GO! For once those who measure Gold fundamentally are buying, in concert those who measure Gold via its pricing structure are buying, along with those who measure Gold as technical measures then turn upward are buying, well, a lot of buying spanning a broad array of measures can go a very long way indeed.

To be sure, the sudden shock of the Italian election's deadlock, (as if this is something new, given that they call their electoral reforms' pigs mess), was yet another reminder going forward of the overall PIIGS uncertainty, (or should you therein prefer to include France, FIGPĪS). The markets were wary of any catalyst for an excuse to rile equities into the Il Plungo that we've been anticipating, (understatement), and indeed for a whole host of far more quantified fundamental reasons, (i.e. another mediocre earnings season in an already-expensive market, non-supportive moneyflow and a lackluster economic barometer). Perhaps some readers will recall this predictive chart below left of the daily S&P 500 futures bars that we herein posted on 26 January in anticipation of the stock market's potentially giving up a month's worth of gains in one fell swoop, (the black arrow). Well, there's the actual result below right in our 21-day view, as captured live following the market's close on Monday, (the entirety of that day's bar displayed as the red arrow for emphasis):p

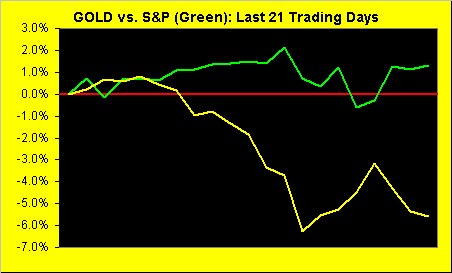

Yessiree, there they went: the entirety of February's painstakingly earned market profits gone in the few hours of a single trading session. ëTwas the S&P's fourth largest single-day point drop since 09 November 2011. And bizarrely on something as remote as yet another goofy Italian election. You don't think beneath all the media/analyst hype that this market is nervous? Clearly, it does not take much right now to set off this all too risky game of equities chicken: the mere sight of a bit more selling than of that which has become complacently the usual and a mad, piling-on dash for the exits ensued. Moreover, what we saw on Monday was hardly downside-expansive as opposed to what I suspect we'll witness going forward. Yes, the S&P futures did reclaim a good portion of this loss to close the week back up at that 1517 level, again with a tip of the cap to Italy for a well-received post-election bond auction. Live by Italy, die by Italy. What happens next time when, instead of Italy & Co., it's the USA? Here's the point: as represented by the S&P, we've a stock market racing across eggshells, the fragility of which is so sensitive that what just transpired above, paisano, will happen again. And again. And yet again. it's not about whether you hoid it here foist. Rather it's about being out. And I'll stand by that until further notice. As for Gold, it's about being in. Having at the outset discussed Gold's negative correlation to the S&P, here are those two markets' percentage tracks over the last 21 trading days, (i.e. one month). The S&P doesn't actually appear to be as robust as the FinMedia might have us believe...

...but then I forget: it's all about The Dow being so near an all-time closing high. (Jeepers, what if it doesn't happen?) More importantly, you can see Gold's continuing to trade directionally contra to the S&P on balance, and as noted earlier, the most so since the latter half of 2011 which brought us its All-Time High of 1923. Now let's look at Gold's Weekly Bars, as (I admittedly keep saying), this is where it really starts to become interesting. The state of the current parabolic Short trend as defined by the declining red dots is now 18 weeks in length, just two weeks shy of the all-time record when measuring Short trends since 2001. Regular readers know that such record is 20 consecutive weeks, which still appears on the chart below during mid-2012:

As for Gold's parabolic Long trends, there've been six faux global money supplies. And as ECB President Mario whatever it takes Draghi reiterated this past week: "Our monetary policy remains accommodative. These Italians are indeed everywhere, so it seems; sort of a mini-reincarnate of the Empire. Ti vogliamo bene.

Valuation This week we offer up a combo view of what it's oft-dubbed as everybody's favourite chart, primarily as we're looking for Gold to attack and the S&P to crack. This is where we take the pricing of one specific product in the BEGOS complex (Bond/Euro/Gold/Oil/S&P) and measure it, (rather than on static basis, by one that a flexes and thus keeps the relationships fresh), to the other markets in that mix. This enables us to establish a near-term valuation for any specific market in the complex along with its daily deviation thereto over a moving three-month period. Below on the left we've Gold, and on the right, in green, the S&P:

Notice how Gold in the oscillator, (distance of price from the smooth pearly valuation line), at the foot of its chart just recently broke under the -100 level? This is a very rare occurrence, having just happened for only the seventh time, (with one or several days below -100), since the March lows of 2009. Here's the important bit: the ensuing rallies in Gold from such extreme low oscillator readings typically have been far enough up that they'd likely trip the current Parabolic Short trend just shown earlier on Gold's Weekly Bars to Long. As we've been perennially hearkening, don't be caught on the sidelines when this occurs. As for the stock market, note as well in the right-hand panel that for all the FinMedia ballyhoo about the marvelous equities run we're experiencing, the S&P appears to be struggling of late to maintain upside direction, and further that its own smooth pearly valuation line may well be running out of puff. Time to tip the scales of financial justice, what?

Hold it right there, mmb: you haven't even mentioned that horrific Sequester. Could that be a Gold negative? You mean cutting spending to the equivalent of having our federal government shut down in toto for four days during 2013? I'd say it's a non-event. The real-event is this new reduction in personal income that could have folks scrambling to liquidate equity holdings in order to pay bills. And were the economy to shrink, I ought think the Fed to accommodate rather than fiscally deflate. Nonetheless, I'm reminded of the nucleus for the whole spending problem per this dose of reality from one Margaret Thatcher, who whilst the young Leader of Britain's opposition party, said on the 05 February 1976 edition of Thames TV This Week:

"...and Socialist governments traditionally do make a financial mess. They [socialists] always run out of other people's money. It's quite a characteristic of them." As to how to cope with it all, Squire, I suppose one could so describe in a rap for our otherwise low-information friends out there as follows:

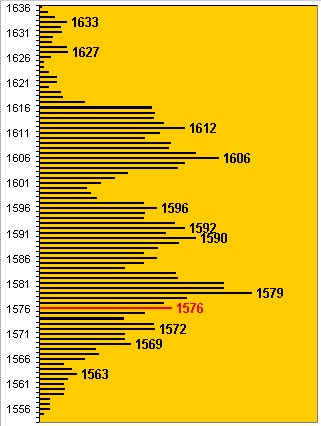

You can see therein the trading work that need be done to the upside, however this current structure suggests getting above 1612 would begin to draw in the momentum/structure buyers as the door then opens to still higher levels. Gold's weighted-average weekly trading range is currently 47 points. So, for example, were Gold not to trade sub-1565 in the new week, then applying such average yields 1565 + 47 = 1612. Perhaps even beyond. For the moment however, it's time to say Ciao for now |

|---|

Send this article to a friend:

|

|

|

Gold has now been negatively correlated to the S&P 500 for the last 26 trading days, (which for you WestPalmBeachers down there means these two markets have, on balance, being moving in opposite directions since 24 January). Such streak marks Gold's longest run of negative correlation to the S&P since the 56-trading day run in 2011 that spanned from 11 July through 27 September, during which period Gold traded from 1555 to its All-Time High of 1923.

Gold has now been negatively correlated to the S&P 500 for the last 26 trading days, (which for you WestPalmBeachers down there means these two markets have, on balance, being moving in opposite directions since 24 January). Such streak marks Gold's longest run of negative correlation to the S&P since the 56-trading day run in 2011 that spanned from 11 July through 27 September, during which period Gold traded from 1555 to its All-Time High of 1923. Nero may have fiddled whilst Rome burned, however Vespasian eventually righted the Empire enough to expand it well up into Scotland and so forth. Little could have been conceived way back then that every financial herk and jerk of Italia 2,000 years hence would have such a sudden, geometrically-compounded reaction upon the markets of our good old USA as we saw this past week. Monti said

Nero may have fiddled whilst Rome burned, however Vespasian eventually righted the Empire enough to expand it well up into Scotland and so forth. Little could have been conceived way back then that every financial herk and jerk of Italia 2,000 years hence would have such a sudden, geometrically-compounded reaction upon the markets of our good old USA as we saw this past week. Monti said