Send this article to a friend:

January

08

2019

|

Send this article to a friend: January |

|

Monetization & Markets (Or Why Fundamentals Don't Matter, Liquidity Does)

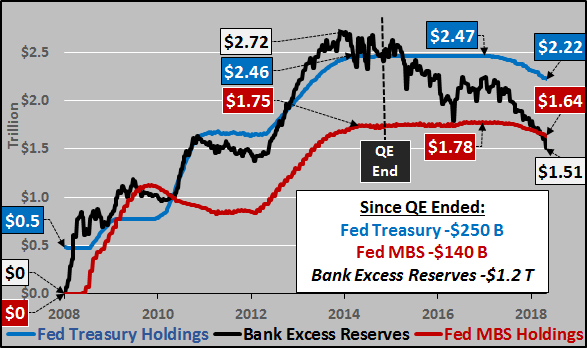

In that spirit, I round back on the Federal Reserves balance sheet versus the curious case of excess reserves of the mega-banks. Last week I detailed that every time the Fed has ceased adding to its balance sheet or outright reduced, the outcome has been decidedly negative for asset prices (HERE). However, like everything, there is a little more to the story. The chart below shows the rise in the Fed's Treasury's (blue line), Mortgage Backed Securities (red line), and rise plus fall of Bank Excess Reserves. What is so interesting is that bank excess reserves didn't begin declining when the Fed's Quantitative Tightening began, but immediately upon the conclusion of QE in late 2014. And excess reserves have already declined by $1.2 trillion while the Fed's balance sheet has declined by "only" about $400 billion. Now, if I were cynical, I'd say it's almost like the Fed's plan with the excess reserves was to use them like a sponge to soak up liquidity during QE and then continue releasing liquidity long after QE ended... and even well after QT was underway (actually, I'm quite cynical). The term for this is "monetization", something the Fed said it would "never do".

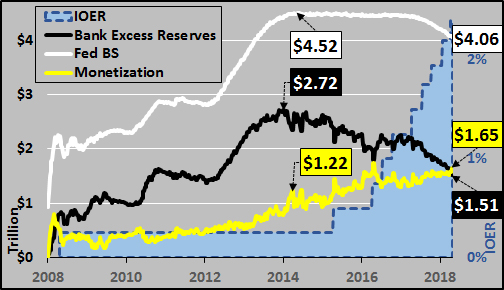

The chart below shows the massive rise in the Fed's balance sheet (white line), bank excess reserves (black line), and the quantity of monetization (yellow line) floating in the system just waiting to be leveraged into 5x's or 10x's or perhaps even 20x's that amount.

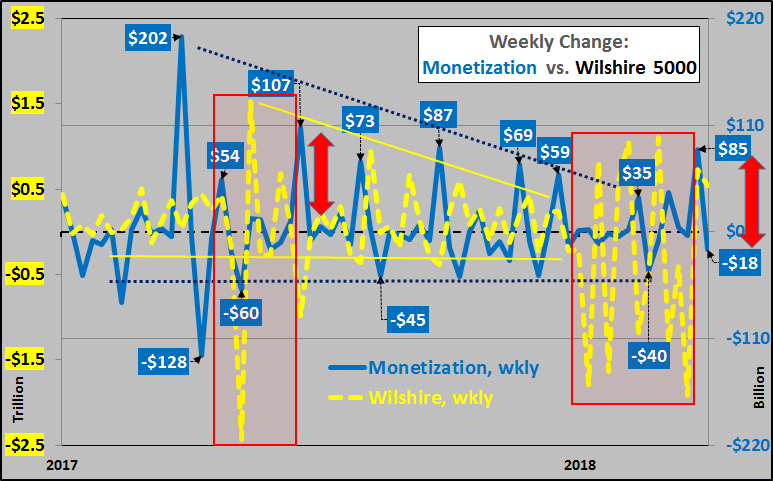

So, in a world where the flow of liquidity seems to be everything, the chart below should be interesting. It is the weekly change in the Wilshire 5000 (yellow dashed line...representing all publicly traded US equities) versus the weekly change in monetization (blue line) since Quantitative Tightening began in late 2017.

What is perhaps not so surprising as the Fed's QT has been ramping up (and decreasing the flow of monetization), US equities have been responding in kind. The two red shaded boxes show the impact on the Wilshire during periods when the flow of monetization turned negative...massive volatility during the periods when no further liquidity was available. Again, not surprisingly, the market rebound following Christmas was preceded by the largest monetization since the market was last relieved by a similarly large net monetization in March, 2018 (both highlighted with red arrows). It's almost like all the stories about trade wars, employment, etc. etc. are just noise in a market that only truly responds to the rise and/or fall in liquidity. So, late last week when chairman Powell said the Fed is listening, I believe the sound of systemic seizure during illiquidity is what he may have heard...and liquidity is likely what he and the team will "coordinate" (aka, more monetization via excess reserves exiting faster than the Fed's QT) if the goal is to maintain the status quo, at least until the excess reserves are exhausted and a new round of QE plus NIRP ready? Of course, this is all just putting lipstick on the pig, as the real issues are recently detailed HERE and HERE. The moment for those holding precious metals and like hedges is likely very nearly at hand, when perpetual monetizati becomes acknowledged US policy.

econimica.blogspot.com

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/silver/t24_ag_en_usoz_2.gif)